curveLibrary "curve"

Regression array Creator. Handy for weights, Auto Normalizes array while holding curves.

curve(_size, _power)

Curve Regression Values Tool

Parameters:

_size : (float) Number of Steps required (float works, future consideration)

_power : (float) Strength of value decrease

Returns: (float ) Array of multipliers from 1 downwards to 0.

Regression

Everything Bitcoin [Kioseff Trading]Hello!

This script retrieves most of the available Bitcoin data published by Quandl; the script utilizes the new request.security_lower_tf() function.

Included statistics,

True price

Volume

Difficulty

My Wallet # Of Users

Average Block Size

api.blockchain size

Median Transaction Confirmation Time

Miners' Revenue

Hash Rate

Cost Per Transaction

Cost % of Transaction Volume

Estimated Transaction Volume USD

Total Output Volume

Number Of Transactions Per Block

# of Unique BTC Addresses

# of BTC Transactions Excluding Popular Addresses

Total Number of Transactions

Daily # of Transactions

Total Transaction Fees USD

Market Cap

Total BTC

Retrieved data can be plotted as line graphs; however, the data is initially split between two tables.

The image above shows how the requested Bitcoin data is displayed.

However, in the user inputs tab, you can modify how the data is displayed.

For instance, you can append the data displayed in the floating statistics box to the stagnant statistics box.

The image above exemplifies the instance.

You can hide any and all data via the user inputs tab.

In addition to data publishing, the script retrieves lower timeframe price/volume/indicator data, to which the values of the requested data are appended to center-right table.

The image above shows the script retrieving one-minute bar data.

Up arrows reflect an increase in the more recent value, relative to the immediately preceding value.

Down arrows reflect a decrease in the more recent value relative to the immediately preceding value.

The ascending minute column reflects the number of minutes/hours (ago) the displayed value occurred.

For instance, 15 minutes means the displayed value occurred 15 minutes prior to the current time (value).

Volume, price, and indicator data can be retrieved on lower timeframe charts ranging from 1 minute to 1440 minutes.

The image above shows retrieved 5-minute volume data.

Several built-in indicators are included, to which lower timeframe values can be retrieved.

The image above shows LTF VWAP data. Also distinguished are increases/decreases for sequential values.

The image above shows a dynamic regression channel. The channel terminates and resets each fiscal quarter. Previous channels remain on the chart.

Lastly, you can plot any of the requested data.

The new request.security_lower_tf() function is immensely advantageous - be sure to try it in your scripts!

Infiten's Regressive Trend Channel An experiment using Pinescript's candle plotting feature. This indicator performs a linear regression on the lows, highs, and moving average, and plots them all in the form of a candlestick. If the close is below the prediction, the candlestick is red, if the close is above the regression, the candlestick is green. Effective and aesthetic way to analyze trends.

Regression Channel with projectionEXPERIMENTAL:

Auto adjusting regressive channel with projection.

Linear regression is a linear approach to modeling the relationship between a dependent variable and one or more independent variables.

In linear regression , the relationships are modeled using linear predictor functions whose unknown model parameters are estimated from the data.

Disclaimer :

Success in trading is all about following your trading strategy and indicators should fit into your own strategy, and not be traded purely on.

This script is for informational and educational purposes only. Use of the script does not constitute professional and / or financial advice. You are solely responsible for evaluating the outcome of the script and the risks associated with using the script. In exchange for the use of the script, you agree not to hold monpotejulien TradingView user responsible for any possible claims for damages arising out of any decisions you make based on the use of the script.

ZigZag Channel with projection forecastThis indicator is created on top of existing Zigzag indicator .

The projection channel starts at the end of the last ZigZag line.

Disclaimer

Success in trading is all about following your trading strategy and indicators should fit into your own strategy, and not be traded purely on.

This script is for informational and educational purposes only. Use of the script does not constitute professional and / or financial advice. You are solely responsible for evaluating the outcome of the script and the risks associated with using the script. In exchange for the use of the script, you agree not to hold monpotejulien TradingView user responsible for any possible claims for damages arising out of any decisions you make based on the use of the script.

Relative slopeRelative slope metric

Description:

I was in need to create a simple, naive and elegant metric that was able to tell how strong is the trend in a given rolling window. While abstaining from using more complicated and arguably more precise approaches, I’ve decided to use Linearly Weighted Linear Regression slope for this goal. Outright values are useful, but the problem was that I wasn’t able to use it in comparative analysis, i.e between different assets & different resolutions & different window sizes, because obviously the outputs are scale-variant.

Here is the asset-agnostic, resolution-agnostic and window size agnostic version of the metric.

I made it asset agnostic & resolution agnostic by including spread information to the formula. In our case it's weighted stdev over differenced data (otherwise we contaminate the spread with the trend info). And I made it window size agnostic by adding a non-linear relation of length to the output, so finally it will be aprox in (-1, 1) interval, by taking square root of length, nothing fancy. All these / 2 and * 2 in unexpected places all around the formula help us to return the data to it’s natural scale while keeping the transformations in place.

Peace TV

Pro Ecometrics [by @Amu_Arsalan] ✔ Intro

As a day trader, this is one of my main strategies to trade with, I have been developing this strategy last 6 months. this strategy helps me make great trades more confident. I wish this could help you make great trades as well

✔ OVERVIEW

This is a combination of linear regression for trend analysis and auto plot channel and divergences for 9 oscillators and indicators in 5 different candle range lookback.

✔ CONCEPTS

As a trader, you probably know how to trade with channels and trend lines, but we need more confirmation before we dive into a trade, Divergences are one of the most accurate and reliable confirmations for this purpose. So I combine these as a strategy. when I see a confluence in divergence signal and trend line (regression), it has a great chance to see a reversal.

✔ Divergences

Show both Bearish and Bullish Divergences fully detailed for normal and hidden divergences it plots a label with indicator names and its values that make this divergence occur. it could calculate divergences for 9 oscillators and indicators for 5 lookback periods.

✔ Trend Line

It has editable settings such as lookback period, source, and even color changing. by default, it makes a linear regression for the past 100 candles.

FunctionPolynomialFitLibrary "FunctionPolynomialFit"

Performs Polynomial Regression fit to data.

In statistics, polynomial regression is a form of regression analysis in which

the relationship between the independent variable x and the dependent variable

y is modelled as an nth degree polynomial in x.

reference:

en.wikipedia.org

www.bragitoff.com

gauss_elimination(A, m, n) Perform Gauss-Elimination and returns the Upper triangular matrix and solution of equations.

Parameters:

A : float matrix, data samples.

m : int, defval=na, number of rows.

n : int, defval=na, number of columns.

Returns: float array with coefficients.

polyfit(X, Y, degree) Fits a polynomial of a degree to (x, y) points.

Parameters:

X : float array, data sample x point.

Y : float array, data sample y point.

degree : int, defval=2, degree of the polynomial.

Returns: float array with coefficients.

note:

p(x) = p * x**deg + ... + p

interpolate(coeffs, x) interpolate the y position at the provided x.

Parameters:

coeffs : float array, coefficients of the polynomial.

x : float, position x to estimate y.

Returns: float.

Smart Reg channel [monpotejulien]This indicator calculates an adaptative regression channel over a specified period or interval.

Resources:

rosettacode.org

en.wikipedia.org

StrengthA mathematically elegant, native & modern way how to measure velocity/ strength/ momentum. As you can see it looks like MACD, but !suddenly! has N times shorter code (disregard the functions), and only 1 parameter instead of 3. OMG HOW DID HE DO IT?!?

MACD: "Let's take one filter (1 parameter), than another filter (2 parameters), then let's take dem difference, then let's place another filter over the difference (3rd parameter + introduction of a nested calculation), and let's write a whole book about it, make thousands of multi-hours YouTube videos about it, and let's never mention about the amount of uncertainty being introduced by multiple parameters & introduction of the nested calculation."

Strength: "let's get real, let's drop a weighted linear regression & usual linear regression over the data of the same length, take dem slopes, then make the difference over these slopes, all good. And then share it with people w/o putting an ® sign".

Fyi, regressions were introduced centuries ago, maybe decades idk, the point is long time ago, and computational power enough to calculate what I'm saying is slightly more than required for macd.

Rationale.

Linearly weighted linear regression has steeper slope (W) than the usual linear regression slope (S) due to the fact that the recent datapoints got more weight. This alone is enough of a metric to measure velocity. But still I've recalled macd and decided to make smth like it cuz I knew it'll might make you happy. I realized that S can be used instead of smoothing the W, thus eliminating the nested calculation and keeping entropy & info loss in place. And see, what we get is natural, simple, makes sense and brings flex. I also wanna remind you that by applying regression we maximize the info gain by using all the data in the window, instead of taking difference between the first and the last datapoints.

This script is dedicated to my friend Fabien. Man, you were the light in the darkness in that company. You'll get your alien green Lambo if you'll really want it, no doubts on my side bout that.

Good hunting

Сatching knivesThis strategy is based on the regression line and volume

The Linear Regression Channel is a three-line technical indicator that displays the high, low and midpoint of the current trend.

How does it work in strategy?

If there is a deviation by a given percentage, the entry occurs

//LOGIC ENTRY

-Length-сhannel length

-Deviation-deviation of the boundaries, the higher , the rarer the entries

-% low for regression-deviation directly from the boundaries, the higher the number, the less frequent the entries

-Required % down bar-additional condition for entry (the candle on which the entry takes place from the logic must necessarily fall by a given percentage)

-Volume-the volume, which must be larger by the number of times you specify ( you can set the volume lower, but for better entries, you need to set the deviation percentages higher!)

//EXIT SETTING

Take profit and stop loss when a certain percentage is reached

//SETTINGS NEXT ENTRY AND GRID

Allow signal lower than,% - the next entry into a trade from logic occurs only when a decrease by a certain percentage

Allow grid,% - when the price drops by the percentage specified in the settings, the entry will take place, but only on the next bar.

//DATA RANGE

-Testing results for any period of time

//

Default settings for infrequent but relatively accurate entries for TF 1 hour.

It costs pyramiding 5 and take profit 5%. Choose the flavors of your choice!

Good luck!

Weighted Least Squares Moving AverageLinearly Weighted Ordinary Least Squares Moving Regression

aka Weighted Least Squares Moving Average -> WLSMA

^^ called it this way just to for... damn, forgot the word

Totally pwns LSMA for some purposes here's why (just look up):

- 'realistically' the same smoothness;

- less lag;

- less overshoot;

- more or less same computationally intensive.

"Pretty cool, huh?", Bucky Roberts©, thenewboston

Now, would you please (just look down) and see the comparison of impulse & step responses:

Impulse responses

Step responses

Ain't it beautiful?

"Motivation behind the concept & rationale", by gorx1

Many been trippin' applying stats methods that require normally distributed data to time series, hence all these B*ll**** Bands and stuff don't really work as it should, while people blame themselves and buy snake oil seminars bout trading psychology, instead of using proper tools. Price... Neither population nor the samples are neither normally nor log-normally distributed. So we can't use all the stuff if we wanna get better results. I'm not talking bout passing each rolling window to a stat test in order to get the proper descriptor, that's the whole different story.

Instead we can leverage the fact that our data is time-series hence we can apply linear weighting, basically we extract another info component from the data and use it to get better results. Volume, range weighting don't make much sense (saying that based on both common sense and test results). Tick count per bar, that would be nice tho... this is the way to measure "intensity". But we don't have it on TV unfortunately.

Anyways, I'm both unhappy that no1 dropped it before me during all these years so I gotta do it myself, and happy that I can give smth cool to every1

Here is it, for you.

P.S.: the script contains standalone functions to calculate linearly weighted variance, linearly weighted standard deviation, linearly weighted covariance and linearly weighted correlation.

Good hunting

Linear Regression Channel - Auto Volume BasedBased on oryginal TV indicator BUT with a little twist. ;)

I really like the regression channel - but the problem is that the length needs to be always manually adjusted.

In this script I try to solve this issue.

This is modified version on TV indicator - Linear Regression Channel.

The main difference is that now you don't get static length - it is automatically adjuested to the recent price action (determined by highest volume in last 300 bars).

Linear Regression Relative Strength[image/x/iZvwDWEY/

Relative Strength indicator comparing the current symbol to SPY (or any other benchmark). It may help to pick the right assets to complement the portfolio build around core ETFs such as SPY.

The general idea is to show if the current symbol outperforms or underperforms the benchmark (SPY by default) when bought some certain time ago. Relative performance is displayed as percent and is calculated for three different time ranges - short (1 mo by default), mid (1 quarter), and long (half a year). To smooth the volatility, the script uses linear regression to estimate the trend and takes the start and the end points of the linear regression line to compute the relative strength.

It is important to remember that the script shows the gain relative to SPY (or other selected benchmark), not the asset's gain. Therefore, it may indicate that the asset is profitable, but it still may lose value if SPY is in downtrend.

Therefore, it is crucial to check other indicators before making a decision. In the example above, standard linear regression for one quarter is used to indicate the direction of the trend.

vix_vx_regressionAn example of the linear regression library, showing the regression of VX futures on the VIX. The beta might help you weight VX futures when hedging SPX vega exposure. A VX future has point multiplier of 1000, whereas SPX options have a point multiplier of 100. Suppose the front month VX future has a beta of 0.6 and the front month SPX straddle has a vega of 8.5. Using these approximations, the VX future will underhedge the SPX straddle, since (0.6 * 1000) < (8.5 * 100). The position will have about 2.5 ($250) vega. Use the R^2 (coefficient of determination) to check how well the model fits the relationship between VX and VIX. The further from one this value, the less useful the model.

(Note that the mini, VXM futures also have a 100 point multiplier).

regressLibrary "regress"

produces the slope (beta), y-intercept (alpha) and coefficient of determination for a linear regression

regress(x, y, len) regress: computes alpha, beta, and r^2 for a linear regression of y on x

Parameters:

x : the explaining (independent) variable

y : the dependent variable

len : use the most recent "len" values of x and y

Returns: : alpha is the x-intercept, beta is the slope, an r2 is the coefficient of determination

Note: the chart does not show anything, use the return values to compute model values in your own application, if you wish.

Universal logarithmic growth curves, with support and resistanceLogarithmic regression is used to model data where growth or decay accelerates rapidly at first and then slows over time. This model is for the long term series data (such as 10 years time span).

The user can consider entering the market when the price below 25% or 5% confidence and consider take profit when the price goes above 75% or 95% confidence line.

This script is:

- Designed to be usable in all tickers. (not only for bitcoin now!)

- Logarithmic regression and shows support-resistance level

- Shape of lines are all linear adjustable

- Height difference of levels and zones are customizable

- Support and resistance levels are highlighted

Input panel:

- Steps of drawing: Won't change it unless there are display problems.

- Resistance, support, other level color: self-explanatory.

- Stdev multipliers: A constant variable to adjust regression boundaries.

- Fib level N: Base on the relative position of top line and base line. If you don't want all fib levels, you might set all fib levels = 0.5.

- Linear lift up: vertically lift up the whole set of lines. By linear multiplication.

- Curvature constant: It is the base value of the exponential transform before converting it back to the chart and plotting it. A bigger base value will make a more upward curvy line.

FAQ:

Q: How to use it?

A: Click "Fx" in your chart then search this script to get it into your chart. Then right click the price axis, then select "Logarithmic" scale to show the curves probably.

Q: Why release this script?

A: - This script is intended to to fix the current issues of bitcoins growth curve script, and to provide a better version of the logarithmic curve, which is not only for bitcoin , but for all kinds of tickers.

- In the public library there is a hardcoded logarithmic growth curve by @quantadelic . But unfortunately that curve was hardcoded by his manual inputs, which makes the curve stop updating its value since 2019 the date he publish that code. Many users of that script love using it but they realize it was stop updating, many users out there based on @quantadelic version of "bitcoin logarithmic growth curves" and they tried their best to update the coordinates with their own hardcode input values. Eventually, a lot of redundant hardcoded "Bitcoin growth curve" scripts was born in the public library. Which is not a good thing.

Q: What about looking at the regression result with a log scale price axis?

A: You can use this script that I published in a year ago. This script display the result in a log scale price axis.

Logarithmic Trend ChannelThis indicator automatically draws a regression channel plotted on logarithmic scale from the first quotation.

This model is useful for the long term series data (such as 10 or 20 years time span).

The Pearson correlation measures the strength of the linear relationship between two variables. It has a value between to 1, with a value of 0 meaning no correlation, and + 1 meaning a total positive correlation.

Logarithmic price scales are a type of scale used on a chart, plotted such that two equivalent price changes are represented by the same vertical changes on the scale.

They differ from linear price scales because they display percentage points and not dollar price increases for a stock.

Technical issues

*The user have to pan over the chart from the beginning to the end of the study range (such as 10 years of bars) so the pine script could generate those lines on the chart.

*If on the chart the number of bar is less than the lookback period, it won't generate any lines as well.

KURD_TRADE Bitcoin Fibonacci Log Regressionthis indicatore show fibonacci logarithmic regression for BITCOIN and we can analyse the crypto market with it.

[YUTAS] Linear Regression Trend Channel

・Indicator for linear regression channel.

・Multiple deviations can be displayed.

・The color changes by reading the angle of the center line according to the direction of the market.

Rising market → blue

Down market → Red

----------------------------------------------

・線形回帰チャネルのインジケーター。

・偏差を複数表示可能。

・相場の向きに合わせてセンターラインの角度を読み取り色が変わります。

上げ相場 → 青

下げ相場 → 赤

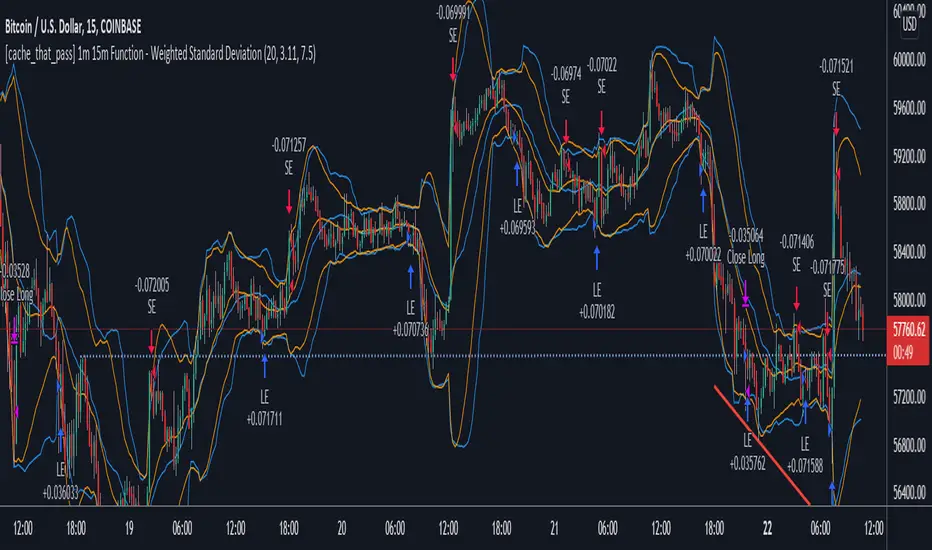

[cache_that_pass] 1m 15m Function - Weighted Standard DeviationTradingview Community,

As I progress through my journey, I have come to the realization that it is time to give back. This script isn't a life changer, but it has the building blocks for a motivated individual to optimize the parameters and have a production script ready to go.

Credit for the indicator is due to @rumpypumpydumpy

I adapted this indicator to a strategy for crypto markets. 15 minute time frame has worked best for me.

It is a standard deviation script that has 3 important user configured parameters. These 3 things are what the end user should tweak for optimum returns. They are....

1) Lookback Length - I have had luck with it set to 20, but any value from 1-1000 it will accept.

2) stopPer - Stop Loss percentage of each trade

3) takePer - Take Profit percentage of each trade

2 and 3 above are where you will see significant changes in returns by altering them and trying different percentages. An experienced pinescript programmer can take this and build on it even more. If you do, I ask that you please share the script with the community in an open-source fashion.

It also already accounts for the commission percentage of 0.075% that Binance.US uses for people who pay fees with BNB.

How it works...

It calculates a weighted standard deviation of the price for the lookback period set (so 20 candles is default). It recalculates each time a new candle is printed. It trades when price lows crossunder the bottom of that deviation channel, and sells when price highs crossover the top of that deviation channel. It works best in mid to long term sideways channels / Wyckoff accumulation periods.

Ripple (XRP) Model PriceAn article titled Bitcoin Stock-to-Flow Model was published in March 2019 by "PlanB" with mathematical model used to calculate Bitcoin model price during the time. We know that Ripple has a strong correlation with Bitcoin. But does this correlation have a definite rule?

In this study, we examine the relationship between bitcoin's stock-to-flow ratio and the ripple(XRP) price.

The Halving and the stock-to-flow ratio

Stock-to-flow is defined as a relationship between production and current stock that is out there.

SF = stock / flow

The term "halving" as it relates to Bitcoin has to do with how many Bitcoin tokens are found in a newly created block. Back in 2009, when Bitcoin launched, each block contained 50 BTC, but this amount was set to be reduced by 50% every 210,000 blocks (about 4 years). Today, there have been three halving events, and a block now only contains 6.25 BTC. When the next halving occurs, a block will only contain 3.125 BTC. Halving events will continue until the reward for minors reaches 0 BTC.

With each halving, the stock-to-flow ratio increased and Bitcoin experienced a huge bull market that absolutely crushed its previous all-time high. But what exactly does this affect the price of Ripple?

Price Model

I have used Bitcoin's stock-to-flow ratio and Ripple's price data from April 1, 2014 to November 3, 2021 (Daily Close-Price) as the statistical population.

Then I used linear regression to determine the relationship between the natural logarithm of the Ripple price and the natural logarithm of the Bitcoin's stock-to-flow (BSF).

You can see the results in the image below:

Basic Equation : ln(Model Price) = 3.2977 * ln(BSF) - 12.13

The high R-Squared value (R2 = 0.83) indicates a large positive linear association.

Then I "winsorized" the statistical data to limit extreme values to reduce the effect of possibly spurious outliers (This process affected less than 4.5% of the total price data).

ln(Model Price) = 3.3297 * ln(BSF) - 12.214

If we raise the both sides of the equation to the power of e, we will have:

============================================

Final Equation:

■ Model Price = Exp(- 12.214) * BSF ^ 3.3297

Where BSF is Bitcoin's stock-to-flow

============================================

If we put current Bitcoin's stock-to-flow value (54.2) into this equation we get value of 2.95USD. This is the price which is indicated by the model.

There is a power law relationship between the market price and Bitcoin's stock-to-flow (BSF). Power laws are interesting because they reveal an underlying regularity in the properties of seemingly random complex systems.

I plotted XRP model price (black) over time on the chart.

Estimating the range of price movements

I also used several bands to estimate the range of price movements and used the residual standard deviation to determine the equation for those bands.

Residual STDEV = 0.82188

ln(First-Upper-Band) = 3.3297 * ln(BSF) - 12.214 + Residual STDEV =>

ln(First-Upper-Band) = 3.3297 * ln(BSF) – 11.392 =>

■ First-Upper-Band = Exp(-11.392) * BSF ^ 3.3297

In the same way:

■ First-Lower-Band = Exp(-13.036) * BSF ^ 3.3297

I also used twice the residual standard deviation to define two extra bands:

■ Second-Upper-Band = Exp(-10.570) * BSF ^ 3.3297

■ Second-Lower-Band = Exp(-13.858) * BSF ^ 3.3297

These bands can be used to determine overbought and oversold levels.

Estimating of the future price movements

Because we know that every four years the stock-to-flow ratio, or current circulation relative to new supply, doubles, this metric can be plotted into the future.

At the time of the next halving event, Bitcoins will be produced at a rate of 450 BTC / day. There will be around 19,900,000 coins in circulation by August 2025

It is estimated that during first year of Bitcoin (2009) Satoshi Nakamoto (Bitcoin creator) mined around 1 million Bitcoins and did not move them until today. It can be debated if those coins might be lost or Satoshi is just waiting still to sell them but the fact is that they are not moving at all ever since. We simply decrease stock amount for 1 million BTC so stock to flow value would be:

BSF = (19,900,000 – 1.000.000) / (450 * 365) =115.07

Thus, Bitcoin's stock-to-flow will increase to around 115 until AUG 2025. If we put this number in the equation:

Model Price = Exp(- 12.214) * 114 ^ 3.3297 = 36.06$

Ripple has a fixed supply rate. In AUG 2025, the total number of coins in circulation will be about 56,000,000,000. According to the equation, Ripple's market cap will reach $2 trillion.

Note that these studies have been conducted only to better understand price movements and are not a financial advice.

NEXT Regressive VWAPOverview:

This version of the Volume-Weighted Average Price (VWAP) indicator features an extended algorithm, which, in addition to volume and price, also incorporates regression analysis. The result is a more responsive, often leading VWAP slope with a degree of statistical predictability built in. Just like with the original VWAP, NEXT Regressive VWAP offers two optional Standard Deviation bands that parallel it. These can be set to any deviation level, with the default being 1 and -1, indicating one standard deviation above and one below Regressive VWAP, respectively.

Below is a screenshot comparing NEXT Regressive VWAP (green) to the original VWAP (blue) on CME_MINI:ES1! M3 chart.

Application and Strategy Ideas:

Price above NEXT Regressive VWAP is interpreted to have a bullish bias, and below, bearish. You can use TradingView's native Set Alert functionality to be notified, in real-time, when price crosses Regressive VWAP, and/or any of its standard deviation bands. Another popular "probability play" strategy is to scalp price when it crosses under the upper band (short) and crosses over the lower band (long). The screenshot below visualizes such a strategy on NASDAQ:QQQ M1 chart:

Input Parameters:

There are 3 groups of input.

Regression Settings

Length - controls the length of time (in bars) for regression analysis with higher values yielding smoother, more responsive values.

Regression Weighting - controls the degree of regression analysis incorporated into VWAP, with 5 being average, 0-4 less, 6-10 more. The higher the value, the more responsive the Regressive VWAP curve.

VWAP Settings

Anchor Period - controls the origin of VWAP calculations, start of session being the default.

Source - data used for calculating the VWAP, typically HLC/3, but can be used with other price formats and data sources as well.

Offset - shifting of the VWAP line forward (+) or backward (-).

Standard Deviation Bands Settings

Calculate Bands - checking this will add 2 bands, each equidistant (by the amount of Multiplier) from the NEXT Regressive VWAP line.

Bands Multiplier - standard deviation multiplier, with 1 being the default

Signals and Alerts:

Here is how to set price (close) crossing NEXT Regressive VWAP alerts: open a chart, attach NEXT Regressive VWAP, and right-click on chart -> Add Alert. Condition: Symbol e.g. ES (close) >> Crossing >> Regressive VWAP >> VWAP >> Once Per Bar Close.