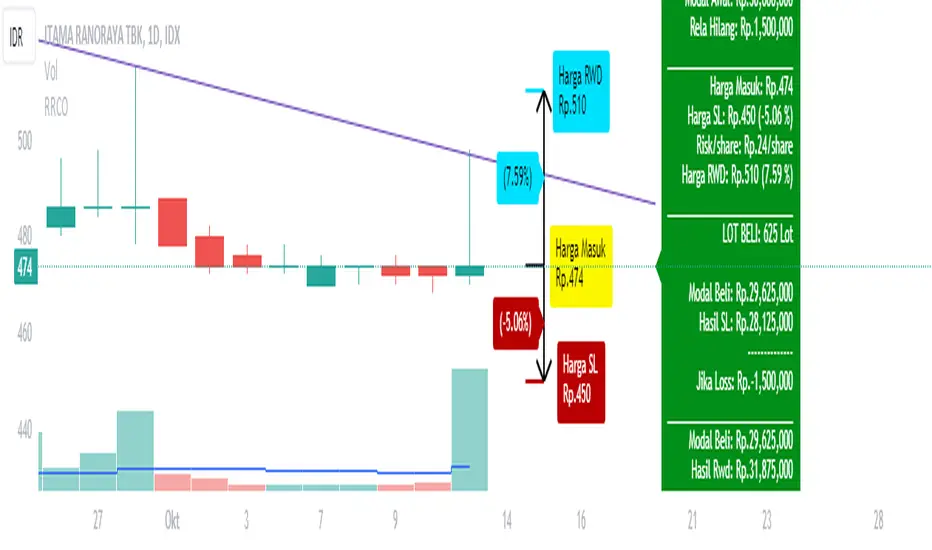

Risk Reward CalculatorPlanning your trading is an important step that you must do before buying the stock.

Risk and Reward Calculator is an important tool for the trader.

With this calculator, you only need to put the capital for one trade and it will automaticaly put the plan for you. But if you want to enter your plan for buy and sell, you just need to check the button and enter the number. the risk and reward calculator will suggest position size based on the information.

The Steps to use Risk Reward Calculator

1. enter how many percentage you can accept if your analysis is wrong.

2. enter how much money you want to trade

3. it will automaticaly calculate the plan for you

4. you can change the reward

5. but if you want to enter your own number, you can check the box. After that enter the number you want for your new plan.

Gestão de carteira

Risk Manage Position SizerThis is a risk management tool for traders. It calculates position sizes based on account balance and risk tolerance, and provides automated stop-loss suggestions. The script displays key information in a small table on the chart and plots important price levels.

How to use it:

Input Parameters:

Account Size: Enter your total trading account balance.

Risk Percentage: Set the percentage of your account you're willing to risk per trade.

Use Custom Stop Loss: Toggle this to use a manually entered stop loss price.

Custom Stop Loss Price: If enabled, enter your desired stop loss price.

Reading the Table:

The table displays:

Current Price

Stop Loss Price

Total Position Size (number of shares/contracts to trade)

1/3 Position Size (for scaling in/out)

Auto Stop 1, 2, and 3 (suggested stop loss levels)

Chart Indicators:

Red Line: Your stop loss level

Green Line: Auto Stop 1 (33% of range from entry to stop)

Yellow Line: Auto Stop 2 (67% of range)

Red Line: Auto Stop 3 (final stop, same as initial stop loss)

Trading Application:

Use the Total Position Size to determine how many shares/contracts to trade.

Consider using the 1/3 Position Size for scaling in or out of trades.

Use the Auto Stops to manage your risk as the trade progresses.

Customization:

Adjust the input parameters to fit your trading style and risk tolerance.

The script can be modified to add more features or change the calculation methods if needed.

This tool helps traders make more informed decisions about position sizing and stop placement, potentially improving risk management in their trading strategy. Remember, while this script provides suggestions, all trading decisions should be made based on your own analysis and risk tolerance.

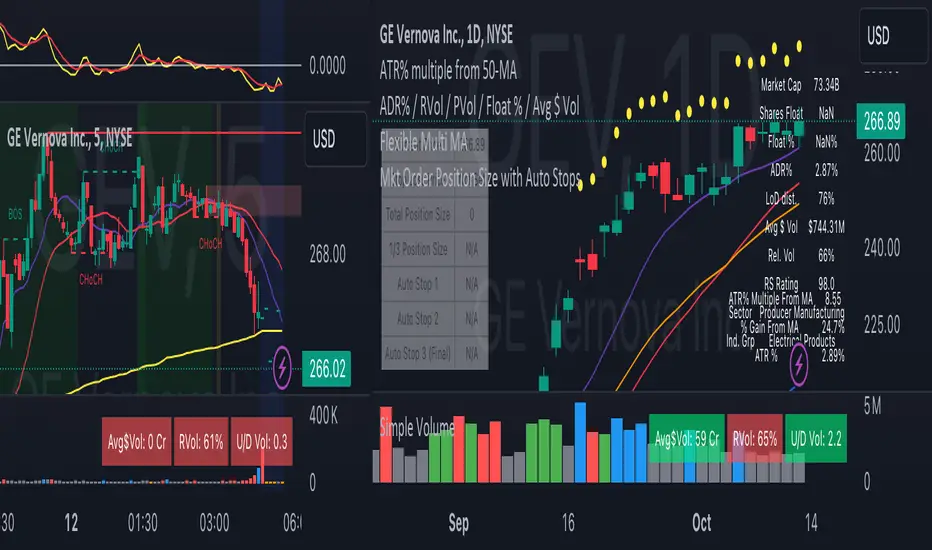

Industry Group StrengthThe Industry Group Strength indicator is designed to help traders identify the best-performing stocks within specific industry groups. The movement of individual stocks is often closely tied to the overall performance of their industry. By focusing on industry groups, this indicator allows you to find the top-performing stocks within an industry.

Thanks to a recent Pine Script update, an indicator like this is now possible. Special thanks to @PineCoders for introducing the dynamic requests feature.

How this indicator works:

The indicator contains predefined lists of stocks for each industry group. To be included in these lists, stocks must meet the following basic filters:

Market capitalization over 2B

Price greater than $10

Primary listing status

Once the relevant stocks are filtered, the indicator automatically recognizes the industry group of the current stock displayed on the chart. It then retrieves and displays data for that entire industry group.

Data Points Available:

The user can choose between three different data points to rank and compare stocks:

YTD (Year-To-Date) Return: Measures how much a stock has gained or lost since the start of the year.

RS Rating: A relative strength rating for a user-selected lookback period (explained below).

% Return: The percentage return over a user-selected lookback period.

Stock Ranking:

Stocks are ranked based on their performance within their respective industry groups, allowing users to easily identify which stocks are leading or lagging behind others in the same sector.

Visualization:

The indicator presents stocks in a table format, with performance metrics displayed both as text labels and color-coded lines. The color gradient represents the percentile rank, making it visually clear which stocks are outperforming or underperforming within their industry group.

Relative Strength (RS):

Relative Strength (RS) measures a stock’s performance relative to a benchmark, typically the S&P 500 (the default setting). It is calculated by dividing the closing price of the stock by the closing price of the S&P 500.

If the stock rises while the S&P 500 falls, or if the stock rises more sharply than the S&P 500, the RS value increases. Conversely, if the stock falls while the S&P 500 rises, the RS value decreases. This indicator normalizes the RS value into a range from 1 to 99, allowing for easier comparison across different stocks, regardless of their raw performance. This normalized RS value helps traders quickly assess how a stock is performing relative to others.

Options Strategy Straddle StrangleThe "Options Strategy Straddle Strangle" indicator is designed to assist traders in identifying and executing optimal options trading strategies by leveraging the foundational principles of option greeks. This tool focuses on two prevalent strategies in options trading: straddles and strangles, providing a systematic approach to determining appropriate strike prices based on real-time market data.

At its core, the indicator calculates strike prices by analyzing key option greeks, including Delta, Gamma, Theta, and Vega. By evaluating these sensitivities, the tool assesses the potential risks and rewards associated with different strike prices, ensuring that the selected levels align with the trader's specified thresholds. Users can input their desired thresholds for each greek, allowing for a customized approach that reflects individual risk tolerance and market outlook.

Once the thresholds are set, the indicator applies its underlying logic to filter and identify the most suitable strike prices for both straddle and strangle strategies. A straddle involves purchasing both a call and a put option at the same strike price, benefiting from significant price movements in either direction. Conversely, a strangle involves buying a call and a put option at different strike prices, which can be more cost-effective while still capitalizing on substantial market shifts.

The output of the "Options Strategy Straddle Strangle" indicator is presented in a clear and organized table format. This table displays the recommended strike prices for implementing either a straddle or a strangle strategy, based on the current market conditions and the predefined greek thresholds. By providing this information in an accessible manner, the indicator enables traders to make informed decisions quickly, enhancing their ability to respond to market volatility effectively.

Note:

Used methodology of the following indicator:

Universal Ratio Trend Matrix [InvestorUnknown]The Universal Ratio Trend Matrix is designed for trend analysis on asset/asset ratios, supporting up to 40 different assets. Its primary purpose is to help identify which assets are outperforming others within a selection, providing a broad overview of market trends through a matrix of ratios. The indicator automatically expands the matrix based on the number of assets chosen, simplifying the process of comparing multiple assets in terms of performance.

Key features include the ability to choose from a narrow selection of indicators to perform the ratio trend analysis, allowing users to apply well-defined metrics to their comparison.

Drawback: Due to the computational intensity involved in calculating ratios across many assets, the indicator has a limitation related to loading speed. TradingView has time limits for calculations, and for users on the basic (free) plan, this could result in frequent errors due to exceeded time limits. To use the indicator effectively, users with any paid plans should run it on timeframes higher than 8h (the lowest timeframe on which it managed to load with 40 assets), as lower timeframes may not reliably load.

Indicators:

RSI_raw: Simple function to calculate the Relative Strength Index (RSI) of a source (asset price).

RSI_sma: Calculates RSI followed by a Simple Moving Average (SMA).

RSI_ema: Calculates RSI followed by an Exponential Moving Average (EMA).

CCI: Calculates the Commodity Channel Index (CCI).

Fisher: Implements the Fisher Transform to normalize prices.

Utility Functions:

f_remove_exchange_name: Strips the exchange name from asset tickers (e.g., "INDEX:BTCUSD" to "BTCUSD").

f_remove_exchange_name(simple string name) =>

string parts = str.split(name, ":")

string result = array.size(parts) > 1 ? array.get(parts, 1) : name

result

f_get_price: Retrieves the closing price of a given asset ticker using request.security().

f_constant_src: Checks if the source data is constant by comparing multiple consecutive values.

Inputs:

General settings allow users to select the number of tickers for analysis (used_assets) and choose the trend indicator (RSI, CCI, Fisher, etc.).

Table settings customize how trend scores are displayed in terms of text size, header visibility, highlighting options, and top-performing asset identification.

The script includes inputs for up to 40 assets, allowing the user to select various cryptocurrencies (e.g., BTCUSD, ETHUSD, SOLUSD) or other assets for trend analysis.

Price Arrays:

Price values for each asset are stored in variables (price_a1 to price_a40) initialized as na. These prices are updated only for the number of assets specified by the user (used_assets).

Trend scores for each asset are stored in separate arrays

// declare price variables as "na"

var float price_a1 = na, var float price_a2 = na, var float price_a3 = na, var float price_a4 = na, var float price_a5 = na

var float price_a6 = na, var float price_a7 = na, var float price_a8 = na, var float price_a9 = na, var float price_a10 = na

var float price_a11 = na, var float price_a12 = na, var float price_a13 = na, var float price_a14 = na, var float price_a15 = na

var float price_a16 = na, var float price_a17 = na, var float price_a18 = na, var float price_a19 = na, var float price_a20 = na

var float price_a21 = na, var float price_a22 = na, var float price_a23 = na, var float price_a24 = na, var float price_a25 = na

var float price_a26 = na, var float price_a27 = na, var float price_a28 = na, var float price_a29 = na, var float price_a30 = na

var float price_a31 = na, var float price_a32 = na, var float price_a33 = na, var float price_a34 = na, var float price_a35 = na

var float price_a36 = na, var float price_a37 = na, var float price_a38 = na, var float price_a39 = na, var float price_a40 = na

// create "empty" arrays to store trend scores

var a1_array = array.new_int(40, 0), var a2_array = array.new_int(40, 0), var a3_array = array.new_int(40, 0), var a4_array = array.new_int(40, 0)

var a5_array = array.new_int(40, 0), var a6_array = array.new_int(40, 0), var a7_array = array.new_int(40, 0), var a8_array = array.new_int(40, 0)

var a9_array = array.new_int(40, 0), var a10_array = array.new_int(40, 0), var a11_array = array.new_int(40, 0), var a12_array = array.new_int(40, 0)

var a13_array = array.new_int(40, 0), var a14_array = array.new_int(40, 0), var a15_array = array.new_int(40, 0), var a16_array = array.new_int(40, 0)

var a17_array = array.new_int(40, 0), var a18_array = array.new_int(40, 0), var a19_array = array.new_int(40, 0), var a20_array = array.new_int(40, 0)

var a21_array = array.new_int(40, 0), var a22_array = array.new_int(40, 0), var a23_array = array.new_int(40, 0), var a24_array = array.new_int(40, 0)

var a25_array = array.new_int(40, 0), var a26_array = array.new_int(40, 0), var a27_array = array.new_int(40, 0), var a28_array = array.new_int(40, 0)

var a29_array = array.new_int(40, 0), var a30_array = array.new_int(40, 0), var a31_array = array.new_int(40, 0), var a32_array = array.new_int(40, 0)

var a33_array = array.new_int(40, 0), var a34_array = array.new_int(40, 0), var a35_array = array.new_int(40, 0), var a36_array = array.new_int(40, 0)

var a37_array = array.new_int(40, 0), var a38_array = array.new_int(40, 0), var a39_array = array.new_int(40, 0), var a40_array = array.new_int(40, 0)

f_get_price(simple string ticker) =>

request.security(ticker, "", close)

// Prices for each USED asset

f_get_asset_price(asset_number, ticker) =>

if (used_assets >= asset_number)

f_get_price(ticker)

else

na

// overwrite empty variables with the prices if "used_assets" is greater or equal to the asset number

if barstate.isconfirmed // use barstate.isconfirmed to avoid "na prices" and calculation errors that result in empty cells in the table

price_a1 := f_get_asset_price(1, asset1), price_a2 := f_get_asset_price(2, asset2), price_a3 := f_get_asset_price(3, asset3), price_a4 := f_get_asset_price(4, asset4)

price_a5 := f_get_asset_price(5, asset5), price_a6 := f_get_asset_price(6, asset6), price_a7 := f_get_asset_price(7, asset7), price_a8 := f_get_asset_price(8, asset8)

price_a9 := f_get_asset_price(9, asset9), price_a10 := f_get_asset_price(10, asset10), price_a11 := f_get_asset_price(11, asset11), price_a12 := f_get_asset_price(12, asset12)

price_a13 := f_get_asset_price(13, asset13), price_a14 := f_get_asset_price(14, asset14), price_a15 := f_get_asset_price(15, asset15), price_a16 := f_get_asset_price(16, asset16)

price_a17 := f_get_asset_price(17, asset17), price_a18 := f_get_asset_price(18, asset18), price_a19 := f_get_asset_price(19, asset19), price_a20 := f_get_asset_price(20, asset20)

price_a21 := f_get_asset_price(21, asset21), price_a22 := f_get_asset_price(22, asset22), price_a23 := f_get_asset_price(23, asset23), price_a24 := f_get_asset_price(24, asset24)

price_a25 := f_get_asset_price(25, asset25), price_a26 := f_get_asset_price(26, asset26), price_a27 := f_get_asset_price(27, asset27), price_a28 := f_get_asset_price(28, asset28)

price_a29 := f_get_asset_price(29, asset29), price_a30 := f_get_asset_price(30, asset30), price_a31 := f_get_asset_price(31, asset31), price_a32 := f_get_asset_price(32, asset32)

price_a33 := f_get_asset_price(33, asset33), price_a34 := f_get_asset_price(34, asset34), price_a35 := f_get_asset_price(35, asset35), price_a36 := f_get_asset_price(36, asset36)

price_a37 := f_get_asset_price(37, asset37), price_a38 := f_get_asset_price(38, asset38), price_a39 := f_get_asset_price(39, asset39), price_a40 := f_get_asset_price(40, asset40)

Universal Indicator Calculation (f_calc_score):

This function allows switching between different trend indicators (RSI, CCI, Fisher) for flexibility.

It uses a switch-case structure to calculate the indicator score, where a positive trend is denoted by 1 and a negative trend by 0. Each indicator has its own logic to determine whether the asset is trending up or down.

// use switch to allow "universality" in indicator selection

f_calc_score(source, trend_indicator, int_1, int_2) =>

int score = na

if (not f_constant_src(source)) and source > 0.0 // Skip if you are using the same assets for ratio (for example BTC/BTC)

x = switch trend_indicator

"RSI (Raw)" => RSI_raw(source, int_1)

"RSI (SMA)" => RSI_sma(source, int_1, int_2)

"RSI (EMA)" => RSI_ema(source, int_1, int_2)

"CCI" => CCI(source, int_1)

"Fisher" => Fisher(source, int_1)

y = switch trend_indicator

"RSI (Raw)" => x > 50 ? 1 : 0

"RSI (SMA)" => x > 50 ? 1 : 0

"RSI (EMA)" => x > 50 ? 1 : 0

"CCI" => x > 0 ? 1 : 0

"Fisher" => x > x ? 1 : 0

score := y

else

score := 0

score

Array Setting Function (f_array_set):

This function populates an array with scores calculated for each asset based on a base price (p_base) divided by the prices of the individual assets.

It processes multiple assets (up to 40), calling the f_calc_score function for each.

// function to set values into the arrays

f_array_set(a_array, p_base) =>

array.set(a_array, 0, f_calc_score(p_base / price_a1, trend_indicator, int_1, int_2))

array.set(a_array, 1, f_calc_score(p_base / price_a2, trend_indicator, int_1, int_2))

array.set(a_array, 2, f_calc_score(p_base / price_a3, trend_indicator, int_1, int_2))

array.set(a_array, 3, f_calc_score(p_base / price_a4, trend_indicator, int_1, int_2))

array.set(a_array, 4, f_calc_score(p_base / price_a5, trend_indicator, int_1, int_2))

array.set(a_array, 5, f_calc_score(p_base / price_a6, trend_indicator, int_1, int_2))

array.set(a_array, 6, f_calc_score(p_base / price_a7, trend_indicator, int_1, int_2))

array.set(a_array, 7, f_calc_score(p_base / price_a8, trend_indicator, int_1, int_2))

array.set(a_array, 8, f_calc_score(p_base / price_a9, trend_indicator, int_1, int_2))

array.set(a_array, 9, f_calc_score(p_base / price_a10, trend_indicator, int_1, int_2))

array.set(a_array, 10, f_calc_score(p_base / price_a11, trend_indicator, int_1, int_2))

array.set(a_array, 11, f_calc_score(p_base / price_a12, trend_indicator, int_1, int_2))

array.set(a_array, 12, f_calc_score(p_base / price_a13, trend_indicator, int_1, int_2))

array.set(a_array, 13, f_calc_score(p_base / price_a14, trend_indicator, int_1, int_2))

array.set(a_array, 14, f_calc_score(p_base / price_a15, trend_indicator, int_1, int_2))

array.set(a_array, 15, f_calc_score(p_base / price_a16, trend_indicator, int_1, int_2))

array.set(a_array, 16, f_calc_score(p_base / price_a17, trend_indicator, int_1, int_2))

array.set(a_array, 17, f_calc_score(p_base / price_a18, trend_indicator, int_1, int_2))

array.set(a_array, 18, f_calc_score(p_base / price_a19, trend_indicator, int_1, int_2))

array.set(a_array, 19, f_calc_score(p_base / price_a20, trend_indicator, int_1, int_2))

array.set(a_array, 20, f_calc_score(p_base / price_a21, trend_indicator, int_1, int_2))

array.set(a_array, 21, f_calc_score(p_base / price_a22, trend_indicator, int_1, int_2))

array.set(a_array, 22, f_calc_score(p_base / price_a23, trend_indicator, int_1, int_2))

array.set(a_array, 23, f_calc_score(p_base / price_a24, trend_indicator, int_1, int_2))

array.set(a_array, 24, f_calc_score(p_base / price_a25, trend_indicator, int_1, int_2))

array.set(a_array, 25, f_calc_score(p_base / price_a26, trend_indicator, int_1, int_2))

array.set(a_array, 26, f_calc_score(p_base / price_a27, trend_indicator, int_1, int_2))

array.set(a_array, 27, f_calc_score(p_base / price_a28, trend_indicator, int_1, int_2))

array.set(a_array, 28, f_calc_score(p_base / price_a29, trend_indicator, int_1, int_2))

array.set(a_array, 29, f_calc_score(p_base / price_a30, trend_indicator, int_1, int_2))

array.set(a_array, 30, f_calc_score(p_base / price_a31, trend_indicator, int_1, int_2))

array.set(a_array, 31, f_calc_score(p_base / price_a32, trend_indicator, int_1, int_2))

array.set(a_array, 32, f_calc_score(p_base / price_a33, trend_indicator, int_1, int_2))

array.set(a_array, 33, f_calc_score(p_base / price_a34, trend_indicator, int_1, int_2))

array.set(a_array, 34, f_calc_score(p_base / price_a35, trend_indicator, int_1, int_2))

array.set(a_array, 35, f_calc_score(p_base / price_a36, trend_indicator, int_1, int_2))

array.set(a_array, 36, f_calc_score(p_base / price_a37, trend_indicator, int_1, int_2))

array.set(a_array, 37, f_calc_score(p_base / price_a38, trend_indicator, int_1, int_2))

array.set(a_array, 38, f_calc_score(p_base / price_a39, trend_indicator, int_1, int_2))

array.set(a_array, 39, f_calc_score(p_base / price_a40, trend_indicator, int_1, int_2))

a_array

Conditional Array Setting (f_arrayset):

This function checks if the number of used assets is greater than or equal to a specified number before populating the arrays.

// only set values into arrays for USED assets

f_arrayset(asset_number, a_array, p_base) =>

if (used_assets >= asset_number)

f_array_set(a_array, p_base)

else

na

Main Logic

The main logic initializes arrays to store scores for each asset. Each array corresponds to one asset's performance score.

Setting Trend Values: The code calls f_arrayset for each asset, populating the respective arrays with calculated scores based on the asset prices.

Combining Arrays: A combined_array is created to hold all the scores from individual asset arrays. This array facilitates further analysis, allowing for an overview of the performance scores of all assets at once.

// create a combined array (work-around since pinescript doesn't support having array of arrays)

var combined_array = array.new_int(40 * 40, 0)

if barstate.islast

for i = 0 to 39

array.set(combined_array, i, array.get(a1_array, i))

array.set(combined_array, i + (40 * 1), array.get(a2_array, i))

array.set(combined_array, i + (40 * 2), array.get(a3_array, i))

array.set(combined_array, i + (40 * 3), array.get(a4_array, i))

array.set(combined_array, i + (40 * 4), array.get(a5_array, i))

array.set(combined_array, i + (40 * 5), array.get(a6_array, i))

array.set(combined_array, i + (40 * 6), array.get(a7_array, i))

array.set(combined_array, i + (40 * 7), array.get(a8_array, i))

array.set(combined_array, i + (40 * 8), array.get(a9_array, i))

array.set(combined_array, i + (40 * 9), array.get(a10_array, i))

array.set(combined_array, i + (40 * 10), array.get(a11_array, i))

array.set(combined_array, i + (40 * 11), array.get(a12_array, i))

array.set(combined_array, i + (40 * 12), array.get(a13_array, i))

array.set(combined_array, i + (40 * 13), array.get(a14_array, i))

array.set(combined_array, i + (40 * 14), array.get(a15_array, i))

array.set(combined_array, i + (40 * 15), array.get(a16_array, i))

array.set(combined_array, i + (40 * 16), array.get(a17_array, i))

array.set(combined_array, i + (40 * 17), array.get(a18_array, i))

array.set(combined_array, i + (40 * 18), array.get(a19_array, i))

array.set(combined_array, i + (40 * 19), array.get(a20_array, i))

array.set(combined_array, i + (40 * 20), array.get(a21_array, i))

array.set(combined_array, i + (40 * 21), array.get(a22_array, i))

array.set(combined_array, i + (40 * 22), array.get(a23_array, i))

array.set(combined_array, i + (40 * 23), array.get(a24_array, i))

array.set(combined_array, i + (40 * 24), array.get(a25_array, i))

array.set(combined_array, i + (40 * 25), array.get(a26_array, i))

array.set(combined_array, i + (40 * 26), array.get(a27_array, i))

array.set(combined_array, i + (40 * 27), array.get(a28_array, i))

array.set(combined_array, i + (40 * 28), array.get(a29_array, i))

array.set(combined_array, i + (40 * 29), array.get(a30_array, i))

array.set(combined_array, i + (40 * 30), array.get(a31_array, i))

array.set(combined_array, i + (40 * 31), array.get(a32_array, i))

array.set(combined_array, i + (40 * 32), array.get(a33_array, i))

array.set(combined_array, i + (40 * 33), array.get(a34_array, i))

array.set(combined_array, i + (40 * 34), array.get(a35_array, i))

array.set(combined_array, i + (40 * 35), array.get(a36_array, i))

array.set(combined_array, i + (40 * 36), array.get(a37_array, i))

array.set(combined_array, i + (40 * 37), array.get(a38_array, i))

array.set(combined_array, i + (40 * 38), array.get(a39_array, i))

array.set(combined_array, i + (40 * 39), array.get(a40_array, i))

Calculating Sums: A separate array_sums is created to store the total score for each asset by summing the values of their respective score arrays. This allows for easy comparison of overall performance.

Ranking Assets: The final part of the code ranks the assets based on their total scores stored in array_sums. It assigns a rank to each asset, where the asset with the highest score receives the highest rank.

// create array for asset RANK based on array.sum

var ranks = array.new_int(used_assets, 0)

// for loop that calculates the rank of each asset

if barstate.islast

for i = 0 to (used_assets - 1)

int rank = 1

for x = 0 to (used_assets - 1)

if i != x

if array.get(array_sums, i) < array.get(array_sums, x)

rank := rank + 1

array.set(ranks, i, rank)

Dynamic Table Creation

Initialization: The table is initialized with a base structure that includes headers for asset names, scores, and ranks. The headers are set to remain constant, ensuring clarity for users as they interpret the displayed data.

Data Population: As scores are calculated for each asset, the corresponding values are dynamically inserted into the table. This is achieved through a loop that iterates over the scores and ranks stored in the combined_array and array_sums, respectively.

Automatic Extending Mechanism

Variable Asset Count: The code checks the number of assets defined by the user. Instead of hardcoding the number of rows in the table, it uses a variable to determine the extent of the data that needs to be displayed. This allows the table to expand or contract based on the number of assets being analyzed.

Dynamic Row Generation: Within the loop that populates the table, the code appends new rows for each asset based on the current asset count. The structure of each row includes the asset name, its score, and its rank, ensuring that the table remains consistent regardless of how many assets are involved.

// Automatically extending table based on the number of used assets

var table table = table.new(position.bottom_center, 50, 50, color.new(color.black, 100), color.white, 3, color.white, 1)

if barstate.islast

if not hide_head

table.cell(table, 0, 0, "Universal Ratio Trend Matrix", text_color = color.white, bgcolor = #010c3b, text_size = fontSize)

table.merge_cells(table, 0, 0, used_assets + 3, 0)

if not hide_inps

table.cell(table, 0, 1,

text = "Inputs: You are using " + str.tostring(trend_indicator) + ", which takes: " + str.tostring(f_get_input(trend_indicator)),

text_color = color.white, text_size = fontSize), table.merge_cells(table, 0, 1, used_assets + 3, 1)

table.cell(table, 0, 2, "Assets", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, x + 1, 2, text = str.tostring(array.get(assets, x)), text_color = color.white, bgcolor = #010c3b, text_size = fontSize)

table.cell(table, 0, x + 3, text = str.tostring(array.get(assets, x)), text_color = color.white, bgcolor = f_asset_col(array.get(ranks, x)), text_size = fontSize)

for r = 0 to (used_assets - 1)

for c = 0 to (used_assets - 1)

table.cell(table, c + 1, r + 3, text = str.tostring(array.get(combined_array, c + (r * 40))),

text_color = hl_type == "Text" ? f_get_col(array.get(combined_array, c + (r * 40))) : color.white, text_size = fontSize,

bgcolor = hl_type == "Background" ? f_get_col(array.get(combined_array, c + (r * 40))) : na)

for x = 0 to (used_assets - 1)

table.cell(table, x + 1, x + 3, "", bgcolor = #010c3b)

table.cell(table, used_assets + 1, 2, "", bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, used_assets + 1, x + 3, "==>", text_color = color.white)

table.cell(table, used_assets + 2, 2, "SUM", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

table.cell(table, used_assets + 3, 2, "RANK", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, used_assets + 2, x + 3,

text = str.tostring(array.get(array_sums, x)),

text_color = color.white, text_size = fontSize,

bgcolor = f_highlight_sum(array.get(array_sums, x), array.get(ranks, x)))

table.cell(table, used_assets + 3, x + 3,

text = str.tostring(array.get(ranks, x)),

text_color = color.white, text_size = fontSize,

bgcolor = f_highlight_rank(array.get(ranks, x)))

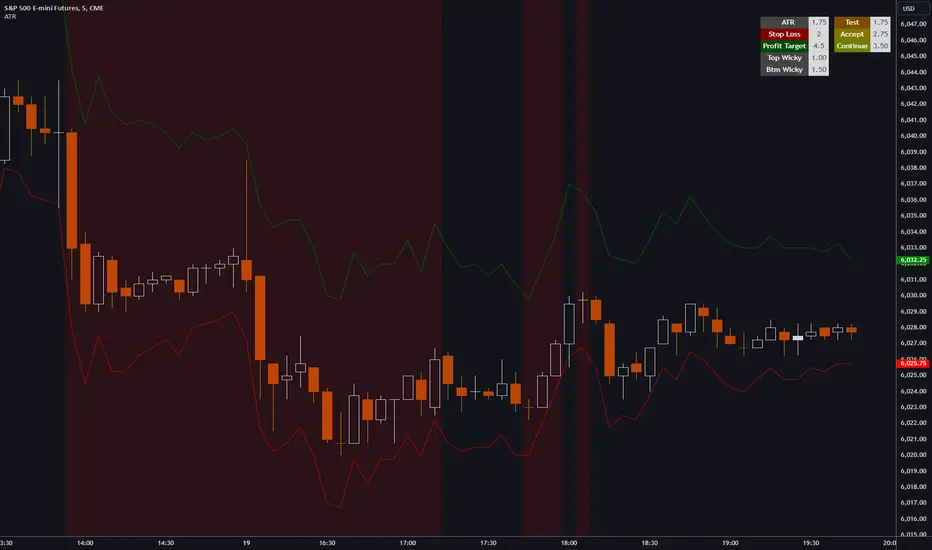

ATR, Chop, Profit Target and Stop Loss TableThe ATR Table indicator is a versatile tool that helps traders visually and quantitatively manage risk, identify market conditions, and set profit targets and stop-loss levels. It is designed to enhance decision-making by incorporating key volatility and chop (market consolidation) signals into a comprehensive table format.

Key Features:

Average True Range (ATR) Calculation : The indicator computes the ATR over a user-defined period (default 14). ATR helps to measure market volatility, providing insights into how much an asset's price typically moves within a given period.

Stop Loss and Profit Target Calculation : You can configure stop-loss and profit target levels using multipliers based on the ATR. This allows dynamic risk management that adjusts to market volatility:

Stop Loss : Defined as a multiple of the ATR to help control losses.

Profit Target : Also based on a multiple of the ATR to lock in gains. The user can specify whether they are trading long or short, and the indicator adjusts the levels accordingly.

Customizable Plot Lines : The indicator can display the Stop Loss and Profit Target levels directly on the chart. Users can toggle these lines on or off and customize their colors.

Chop Signa l: The indicator highlights potential consolidation periods (chop) using a wick-based analysis. It calculates the highest upper or lower wick values and compares them to the ATR to detect periods of indecision or consolidation.

Table Display : When these wick values exceed the ATR by a user-defined multiplier, the corresponding table rows are highlighted.

Background Alerts : Optionally, users can activate background color changes on the chart to visually alert them when chop conditions are detected.

Customizable Table Layout : A table displaying the key values (ATR, Stop Loss, Profit Target, Upper/Lower Wickiness) is placed on the chart. You can choose the table's position, adjust its color scheme, and decide which rows to display.

Chop Background Customization : For users who prefer more visual cues, the indicator allows you to enable or disable background shading when chop conditions are met. You can also choose the color of this background for better customization.

(Early Test) Weekly Seasonality with Dynamic Kelly Criterion# Enhancing Trading Strategies with the Weekly Seasonality Dynamic Kelly Criterion Indicator

Amidst this pursuit to chase price, a common pitfall emerges: an overemphasis on price movements without adequate attention to risk management, probabilistic analysis, and strategic position sizing. To address these challenges, I developed the **Weekly Seasonality with Dynamic Kelly Criterion Indicator**. It is designed to refocus traders on essential aspects of trading, such as risk management and probabilistic returns, thereby catering to both short-term swing traders and long-term investors aiming for tax-efficient positions.

## The Motivation Behind the Indicator

### Overemphasis on Price: A Common Trading Pitfall

Many traders concentrate heavily on price charts and technical indicators, often neglecting the underlying principles of risk management and probabilistic analysis. This overemphasis on price can lead to:

- **Overtrading:** Making frequent trades based solely on price movements without considering the associated risks.

- **Poor Risk Management:** Failing to set appropriate stop-loss levels or position sizes, increasing the potential for significant losses.

- **Emotional Trading:** Letting emotions drive trading decisions rather than objective analysis, which can result in impulsive and irrational trades.

### The Need for Balanced Focus

To achieve sustained trading success, it is crucial to balance price analysis with robust risk management and probabilistic strategies. Key areas of focus include:

1. **Risk Management:** Implementing strategies to protect capital, such as setting stop-loss orders and determining appropriate position sizes based on risk tolerance.

2. **Probabilistic Analysis:** Assessing the likelihood of various market outcomes to make informed trading decisions.

3. **Swing Trading Percent Returns:** Capitalizing on short- to medium-term price movements by buying assets below their average return and selling them above.

## Introducing the Weekly Seasonality with Dynamic Kelly Criterion Indicator

The **Weekly Seasonality with Dynamic Kelly Criterion Indicator** is designed to integrate these essential elements into a comprehensive tool that aids traders in making informed, risk-aware decisions. Below, we explore the key components and functionalities of this indicator.

### Key Components of the Indicator

1. **Average Return (%)**

- **Definition:** The mean percentage return for each week across multiple years.

- **Purpose:** Serves as a benchmark to identify weeks with above or below-average performance, guiding buy and sell decisions.

2. **Positive Percentage (%)**

- **Definition:** The proportion of weeks that yielded positive returns.

- **Purpose:** Indicates the consistency of positive returns, helping traders gauge the reliability of certain weeks for trading.

3. **Volatility (%)**

- **Definition:** The standard deviation of weekly returns.

- **Purpose:** Measures the variability of returns, providing insights into the risk associated with trading during specific weeks.

4. **Kelly Ratio**

- **Definition:** A mathematical formula used to determine the optimal size of a series of bets to maximize the logarithmic growth of capital.

- **Purpose:** Balances potential returns against risks, guiding traders on the appropriate position size to take.

5. **Adjusted Kelly Fraction**

- **Definition:** The Kelly Ratio adjusted based on user-defined risk tolerance and external factors like Federal Reserve (Fed) stance.

- **Purpose:** Personalizes the Kelly Criterion to align with individual risk preferences and market conditions, enhancing risk management.

6. **Position Size ($)**

- **Definition:** The calculated amount to invest based on the Adjusted Kelly Fraction.

- **Purpose:** Ensures that position sizes are aligned with risk management strategies, preventing overexposure to any single trade.

7. **Max Drawdown (%)**

- **Definition:** The maximum observed loss from a peak to a trough of a portfolio, before a new peak is attained.

- **Purpose:** Assesses the worst-case scenario for losses, crucial for understanding potential capital erosion.

### Functionality and Benefits

- **Weekly Data Aggregation:** Aggregates weekly returns across multiple years to provide a robust statistical foundation for decision-making.

- **Quarterly Filtering:** Allows users to filter weeks based on quarters, enabling seasonality analysis and tailored strategies aligned with specific timeframes.

- **Dynamic Risk Adjustment:** Incorporates the Dynamic Kelly Criterion to adjust position sizes in real-time based on changing risk profiles and market conditions.

- **User-Friendly Visualization:** Presents all essential metrics in an organized Summary Table, facilitating quick and informed decision-making.

## The Origin of the Kelly Criterion and Addressing Its Limitations

### Understanding the Kelly Criterion

The Kelly Criterion, developed by John L. Kelly Jr. in 1956, is a formula used to determine the optimal size of a series of bets to maximize the long-term growth of capital. The formula considers both the probability of winning and the payout ratio, balancing potential returns against the risk of loss.

**Kelly Formula:**

\

Where:

- \( b \) = the net odds received on the wager ("b to 1")

- \( p \) = probability of winning

- \( q \) = probability of losing ( \( q = 1 - p \) )

### The Risk of Ruin

While the Kelly Criterion is effective in optimizing growth, it carries inherent risks:

- **Overbetting:** If the input probabilities or payout ratios are misestimated, the Kelly Criterion can suggest overly aggressive position sizes, leading to significant losses.

- **Assumption of Constant Probabilities:** The criterion assumes that probabilities remain constant, which is rarely the case in dynamic markets.

- **Ignoring External Factors:** Traditional Kelly implementations do not account for external factors such as Federal Reserve rates, margin requirements, or market volatility, which can impact risk and returns.

### Addressing Traditional Limitations

Recognizing these limitations, the **Weekly Seasonality with Dynamic Kelly Criterion Indicator** introduces enhancements to the traditional Kelly approach:

- **Incorporation of Fed Stance:** Adjusts the Kelly Fraction based on the current stance of the Federal Reserve (neutral, dovish, or hawkish), reflecting broader economic conditions that influence market behavior.

- **Margin and Leverage Considerations:** Accounts for margin rates and leverage, ensuring that position sizes remain within manageable risk parameters.

- **Dynamic Adjustments:** Continuously updates position sizes based on real-time risk assessments and probabilistic analyses, mitigating the risk of ruin associated with static Kelly implementations.

## How the Indicator Aids Traders

### For Short-Term Swing Traders

Short-term swing traders thrive on capitalizing over weekly price movements. The indicator aids them by:

- **Identifying Favorable Weeks:** Highlights weeks with above-average returns and favorable volatility, guiding entry and exit points.

- **Optimal Position Sizing:** Utilizes the Adjusted Kelly Fraction to determine the optimal amount to invest, balancing potential returns with risk exposure.

- **Probabilistic Insights:** Provides metrics like Positive Percentage (%) and Kelly Ratio to assess the likelihood of favorable outcomes, enhancing decision-making.

### For Long-Term Tax-Free Investors

This is effectively a drop-in replacement for DCA which uses fixed position size that doesn't change based on market conditions, as a result, it's like catching multiple falling knifes by the blade and smiling with blood on your hand... I don't know about you, but I'd rather juggle by the hilt and look like an actual professional...

Long-term investors, especially those seeking tax-free positions (e.g., through retirement accounts), benefit from:

- **Consistent Risk Management:** Ensures that position sizes are aligned with long-term capital preservation strategies.

- **Seasonality Analysis:** Allows for strategic positioning based on historical performance trends across different weeks and quarters.

- **Dynamic Adjustments:** Adapts to changing market conditions, maintaining optimal risk profiles over extended investment horizons.

### Developers

Please double check the logic and functionality because I think there are a few issue and I need to crowd source solutions and be responsible about the code I publish. If you have corrections, please DM me or leave a respectful comment.

I want to publish this by the end of the year and include other things like highlighting triple witching weeks, adding columns for volume % stats, VaR and CVaR, alpha, beta (to see the seasonal alpha and beta based off a benchmark ticker and risk free rate ticker and other little goodies.

Leonid's Bitcoin Sharpe RatioThe Sharpe ratio is an old formula used to value the risk-adjusted return of an asset. It was developed by Nobel Laureate William F. Sharpe. In this case, I have applied it to Bitcoin with an adjustable look-back date.

The Sharpe Ratio shows you the average return earned after subtracting out the risk-free rate per unit of volatility (I've defaulted this to 0.02 ).

Volatility is a measure of the price fluctuations of an asset or portfolio. Subtracting the risk-free rate from the mean return allows you to understand what the extra returns are for taking the risk.

If the indicator is flashing red, Bitcoin is temporarily overbought (expensive).

If the indicator is flashing green, Bitcoin is temporarily oversold (cheap).

The goal of this indicator is to signal out local tops & bottoms. It can be adjusted as far as the lookback time but I have found 25-26 days to be ideal.

Commitment of Trader %R StrategyThis Pine Script strategy utilizes the Commitment of Traders (COT) data to inform trading decisions based on the Williams %R indicator. The script operates in TradingView and includes various functionalities that allow users to customize their trading parameters.

Here’s a breakdown of its key components:

COT Data Import:

The script imports the COT library from TradingView to access historical COT data related to different trader groups (commercial hedgers, large traders, and small traders).

User Inputs:

COT data selection mode (e.g., Auto, Root, Base currency).

Whether to include futures, options, or both.

The trader group to analyze.

The lookback period for calculating the Williams %R.

Upper and lower thresholds for triggering trades.

An option to enable or disable a Simple Moving Average (SMA) filter.

Williams %R Calculation: The script calculates the Williams %R value, which is a momentum indicator that measures overbought or oversold levels based on the highest and lowest prices over a specified period.

SMA Filter: An optional SMA filter allows users to limit trades to conditions where the price is above or below the SMA, depending on the configuration.

Trade Logic: The strategy enters long positions when the Williams %R value exceeds the upper threshold and exits when the value falls below it. Conversely, it enters short positions when the Williams %R value is below the lower threshold and exits when the value rises above it.

Visual Elements: The script visually indicates the Williams %R values and thresholds on the chart, with the option to plot the SMA if enabled.

Commitment of Traders (COT) Data

The COT report is a weekly publication by the Commodity Futures Trading Commission (CFTC) that provides a breakdown of open interest positions held by different types of traders in the U.S. futures markets. It is widely used by traders and analysts to gauge market sentiment and potential price movements.

Data Collection: The COT data is collected from futures commission merchants and is published every Friday, reflecting positions as of the previous Tuesday. The report categorizes traders into three main groups:

Commercial Traders: These are typically hedgers (like producers and processors) who use futures to mitigate risk.

Non-Commercial Traders: Often referred to as speculators, these traders do not have a commercial interest in the underlying commodity but seek to profit from price changes.

Non-reportable Positions: Small traders who do not meet the reporting threshold set by the CFTC.

Interpretation:

Market Sentiment: By analyzing the positions of different trader groups, market participants can gauge sentiment. For instance, if commercial traders are heavily short, it may suggest they expect prices to decline.

Extreme Positions: Some traders look for extreme positions among non-commercial traders as potential reversal signals. For example, if speculators are overwhelmingly long, it might indicate an overbought condition.

Statistical Insights: COT data is often used in conjunction with technical analysis to inform trading decisions. Studies have shown that analyzing COT data can provide valuable insights into future price movements (Lund, 2018; Hurst et al., 2017).

Scientific References

Lund, J. (2018). Understanding the COT Report: An Analysis of Speculative Trading Strategies.

Journal of Derivatives and Hedge Funds, 24(1), 41-52. DOI:10.1057/s41260-018-00107-3

Hurst, B., O'Neill, R., & Roulston, M. (2017). The Impact of COT Reports on Futures Market Prices: An Empirical Analysis. Journal of Futures Markets, 37(8), 763-785.

DOI:10.1002/fut.21849

Commodity Futures Trading Commission (CFTC). (2024). Commitment of Traders. Retrieved from CFTC Official Website.

High/Low Breakout Statistical Analysis StrategyThis Pine Script strategy is designed to assist in the statistical analysis of breakout systems on a monthly, weekly, or daily timeframe. It allows the user to select whether to open a long or short position when the price breaks above or below the respective high or low for the chosen timeframe. The user can also define the holding period for each position in terms of bars.

Core Functionality:

Breakout Logic:

The strategy triggers trades based on price crossing over (for long positions) or crossing under (for short positions) the high or low of the selected period (daily, weekly, or monthly).

Timeframe Selection:

A dropdown menu enables the user to switch between the desired timeframe (monthly, weekly, or daily).

Trade Direction:

Another dropdown allows the user to select the type of trade (long or short) depending on whether the breakout occurs at the high or low of the timeframe.

Holding Period:

Once a trade is opened, it is automatically closed after a user-defined number of bars, making it useful for analyzing how breakout signals perform over short-term periods.

This strategy is intended exclusively for research and statistical purposes rather than real-time trading, helping users to assess the behavior of breakouts over different timeframes.

Relevance of Breakout Systems:

Breakout trading systems, where trades are executed when the price moves beyond a significant price level such as the high or low of a given period, have been extensively studied in financial literature for their potential predictive power.

Momentum and Trend Following:

Breakout strategies are a form of momentum-based trading, exploiting the tendency of prices to continue moving in the direction of a strong initial movement after breaching a critical support or resistance level. According to academic research, momentum strategies, including breakouts, can produce returns above average market returns when applied consistently. For example, Jegadeesh and Titman (1993) demonstrated that stocks that performed well in the past 3-12 months continued to outperform in the subsequent months, suggesting that price continuation patterns, like breakouts, hold value .

Market Efficiency Hypothesis:

While the Efficient Market Hypothesis (EMH) posits that markets are generally efficient, and it is difficult to outperform the market through technical strategies, some studies show that in less liquid markets or during specific times of market stress, breakout systems can capitalize on temporary inefficiencies. Taylor (2005) and other researchers have found instances where breakout systems can outperform the market under certain conditions.

Volatility and Breakouts:

Breakouts are often linked to periods of increased volatility, which can generate trading opportunities. Coval and Shumway (2001) found that periods of heightened volatility can make breakouts more significant, increasing the likelihood that price trends will follow the breakout direction. This correlation between volatility and breakout reliability makes it essential to study breakouts across different timeframes to assess their potential profitability .

In summary, this breakout strategy offers an empirical way to study price behavior around key support and resistance levels. It is useful for researchers and traders aiming to statistically evaluate the effectiveness and consistency of breakout signals across different timeframes, contributing to broader research on momentum and market behavior.

References:

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Fama, E. F., & French, K. R. (1996). Multifactor Explanations of Asset Pricing Anomalies. Journal of Finance, 51(1), 55-84.

Taylor, S. J. (2005). Asset Price Dynamics, Volatility, and Prediction. Princeton University Press.

Coval, J. D., & Shumway, T. (2001). Expected Option Returns. Journal of Finance, 56(3), 983-1009.

High Yield Spread Strategy with SMA FilterThis Pine Script strategy is designed for statistical analysis and research purposes only, not for live trading or financial decision-making. The script evaluates the relationship between financial volatility (measured by either the VIX or the High Yield Spread) and market positioning strategies (long or short) based on user-defined conditions. Specifically, it allows users to test the assumption that elevated levels of VIX or the High Yield Spread may justify short positions in the market—a widely held belief in financial circles—but this script demonstrates that shorting is not always the optimal choice, even under these conditions.

Key Components:

1. High Yield Spread and VIX:

• High Yield Spread is the difference between the yields of corporate high-yield (or “junk”) bonds and U.S. Treasury securities. A rising spread often reflects increased market risk perception.

• VIX (Volatility Index) is often referred to as the market’s “fear gauge.” Higher VIX levels usually indicate heightened market uncertainty or expected volatility.

2. Strategy Logic:

• The script allows users to specify a threshold for the VIX or High Yield Spread, and it automatically evaluates if the spread exceeds this level, which traditionally would suggest an environment for higher market risk and thus potentially favoring short trades.

• However, the strategy provides flexibility to enter long or short positions, even in a high-risk environment, emphasizing that a high VIX or High Yield Spread does not always warrant shorting.

3. SMA Filter:

• A Simple Moving Average (SMA) filter can be applied to the price data, where positions are only entered if the price is above or below the SMA (depending on the trade direction). This adds a technical component to the strategy, incorporating price trends into decision-making.

4. Hold Duration:

• The script also allows users to define how long to hold a position after entering, enabling an analysis of different timeframes.

Theoretical Background:

The traditional belief that high VIX or High Yield Spreads favor short positions is not universally supported by research. While a spike in the VIX or credit spreads is often associated with increased market risk, research suggests that excessive volatility does not always lead to negative returns. In fact, high volatility can sometimes signal an approaching market rebound.

For example:

• Studies have shown that long-term investments during periods of heightened volatility can yield favorable returns due to mean reversion. Whaley (2000) notes that VIX spikes are often followed by market recoveries as volatility tends to revert to its mean over time .

• Research by Blitz and Vliet (2007) highlights that low-volatility stocks have historically outperformed high-volatility stocks, suggesting that volatility may not always predict negative returns .

• Furthermore, credit spreads can widen in response to broader market stress, but these may overshoot the actual credit risk, presenting opportunities for long positions when spreads are high and risk premiums are mispriced .

Educational Purpose:

The goal of this script is to challenge assumptions about shorting during volatile periods, showing that long positions can be equally, if not more, effective during market stress. By incorporating an SMA filter and customizable logic for entering trades, users can test different hypotheses regarding the effectiveness of both long and short positions under varying market conditions.

Note: This strategy is not intended for live trading and should be used solely for educational and statistical exploration. Misinterpreting financial indicators can lead to incorrect investment decisions, and it is crucial to conduct comprehensive research before trading.

References:

1. Whaley, R. E. (2000). “The Investor Fear Gauge”. The Journal of Portfolio Management, 26(3), 12-17.

2. Blitz, D., & van Vliet, P. (2007). “The Volatility Effect: Lower Risk Without Lower Return”. Journal of Portfolio Management, 34(1), 102-113.

3. Bhamra, H. S., & Kuehn, L. A. (2010). “The Determinants of Credit Spreads: An Empirical Analysis”. Journal of Finance, 65(3), 1041-1072.

This explanation highlights the academic and research-backed foundation of the strategy and the nuances of volatility, while cautioning against the assumption that high VIX or High Yield Spread always calls for shorting.

Simplified Gap Strategy with SMA FilterThe Simplified Gap Strategy leverages price gaps as a trading signal, focusing on their significance in market behavior. Gaps occur when the opening price of a security differs significantly from the previous closing price, often signaling potential continuation or reversal patterns.

Key Features:

Gap Threshold:

This strategy requires a minimum percentage gap (defined by the user) to qualify for trading signals.

Directional Trading:

Users can select from various gap types, including "Long Up Gap" and "Short Down Gap," allowing for tailored trading approaches.

SMA Filter:

An optional Simple Moving Average (SMA) filter helps refine trade entries based on trend direction, increasing the probability of successful trades.

Hold Duration:

Positions can be held for a user-defined duration, providing flexibility in trade management.

Statistical Significance of Gaps:

Research has shown that gaps can provide insights into future price movements. According to studies such as those by Hutton and Jiang (2008), price gaps are often followed by momentum in the direction of the gap, indicating that they can serve as reliable indicators for traders. The "Gap Theory" suggests that gaps are filled approximately 90% of the time, emphasizing their relevance in market dynamics (Nikkinen, Sahlström, & Kinnunen, 2006).

Important Note:

This strategy is designed solely for statistical analysis and should not be construed as financial advice. Users are encouraged to conduct their own research and analysis before applying this strategy in live trading scenarios.

By understanding the underlying mechanisms of price gaps and their statistical significance, traders can enhance their decision-making processes and potentially improve trading outcomes.

References:

Hutton, A. W., & Jiang, W. (2008). "Price Gaps: A Guide to Trading Gaps."

Nikkinen, J., Sahlström, P., & Kinnunen, J. (2006). "The Gaps in Financial Markets: An Empirical Study."

This description provides an overview of the strategy while emphasizing its analytical purpose and backing it with relevant academic insights.

Streak-Based Trading StrategyThe strategy outlined in the provided script is a streak-based trading strategy that focuses on analyzing winning and losing streaks. It’s important to emphasize that this strategy is not intended for actual trading but rather for statistical analysis of streak series.

How the Strategy Works

1. Parameter Definition:

• Trade Direction: Users can choose between “Long” (buy) and “Short” (sell).

• Streak Threshold: Defines how many consecutive wins or losses are needed to trigger a trade.

• Hold Duration: Specifies how many periods the position will be held.

• Doji Threshold: Determines the sensitivity for Doji candles, which indicate market uncertainty.

2. Streak Calculation:

• The script identifies Doji candles and counts winning and losing streaks based on the closing price compared to the previous closing price.

• Streak counting occurs only when no position is currently held.

3. Trade Conditions:

• If the loss streak reaches the defined threshold and the trade direction is “Long,” a buy position is opened.

• If the win streak is met and the trade direction is “Short,” a sell position is opened.

• The position is held for the specified duration.

4. Visualization:

• Winning and losing streaks are plotted as histograms to facilitate analysis.

Scientific Basis

The concept of analyzing streaks in financial markets is well-documented in behavioral economics and finance. Studies have shown that markets often exhibit momentum and trend-following behavior, meaning the likelihood of consecutive winning or losing periods can be higher than what random statistics would suggest (see, for example, “The Behavior of Stock-Market Prices” by Eugene Fama).

Additionally, empirical research indicates that investors often make decisions based on psychological factors influenced by streaks. This can lead to irrational behavior, as they may focus on past wins or losses (see “Behavioral Finance: Psychology, Decision-Making, and Markets” by R. M. F. F. Thaler).

Overall, this strategy serves as a tool for statistical analysis of streak series, providing deeper insights into market behavior and trends rather than being directly used for trading decisions.

Winning and Losing StreaksThe Pine Script indicator "Winning and Losing Streaks" tracks and visualizes the length of consecutive winning and losing streaks in a financial series, such as stock prices. Here’s a detailed description of the indicator, including the relevance of statistical analysis and streak tracking.

Indicator Description

The "Winning and Losing Streaks" indicator in Pine Script is designed to analyze and display streaks of consecutive winning and losing days in trading data. It helps traders and analysts understand the persistence of trends in price movements.

Here’s how it functions:

Streak Calculation:

Winning Streak: A series of consecutive days where the closing price is higher than the previous day's closing price.

Losing Streak: A series of consecutive days where the closing price is lower than the previous day's closing price.

Doji Candles: The indicator also considers Doji candles, where the difference between the opening and closing prices is minimal relative to the high-low range, and excludes these from being counted as winning or losing days.

Statistical Analysis:

The indicator computes the maximum and average lengths of winning and losing streaks.

It also tracks the current streak lengths and maintains arrays to store the historical streak data.

Visualization:

Histograms: Winning and losing streaks are visualized using histograms, which provide a clear graphical representation of streak lengths over time.

Relevance of Statistical Analysis and Streak Tracking

1. Statistical Significance of Streaks

Tracking winning and losing streaks has significant statistical implications for trading strategies and risk management:

Autocorrelation: Streaks in financial time series can reveal autocorrelation, where past returns influence future returns. Studies have shown that financial time series often exhibit autocorrelation, which can be used to forecast future price movements (Lo, 1991; Jegadeesh & Titman, 1993). Understanding streaks helps in identifying and leveraging these patterns.

Behavioral Finance: Streak analysis aligns with concepts from behavioral finance, such as the "hot-hand fallacy," where investors may perceive trends as more persistent than they are (Gilovich, Vallone, & Tversky, 1985). Statistical streak analysis provides a more objective view of trend persistence, helping to avoid biases.

2. Risk Management and Strategy Development

Risk Assessment: Identifying the length and frequency of losing streaks is crucial for managing risk and adjusting trading strategies. Long losing streaks can indicate potential strategy weaknesses or market regime changes, prompting a reassessment of trading rules and risk management practices (Brock, Lakonishok, & LeBaron, 1992).

Strategy Optimization: Statistical analysis of streaks can aid in optimizing trading strategies. For example, understanding the average length of winning and losing streaks can help in setting more effective stop-loss and take-profit levels, as well as in determining the optimal position sizing (Fama & French, 1993).

Scientific References:

Lo, A. W. (1991). "Long-Term Memory in Stock Market Prices." Econometrica, 59(5), 1279-1313. This paper discusses the presence of long-term memory in stock prices, which is relevant for understanding the persistence of streaks.

Jegadeesh, N., & Titman, S. (1993). "Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency." Journal of Finance, 48(1), 65-91. This study explores momentum and reversal strategies, which are related to the concept of streaks.

Gilovich, T., Vallone, R., & Tversky, A. (1985). "The Hot Hand in Basketball: On the Misperception of Random Sequences." Cognitive Psychology, 17(3), 295-314. This paper provides insight into the psychological aspects of streaks and persistence.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). "Simple Technical Trading Rules and the Stochastic Properties of Stock Returns." Journal of Finance, 47(5), 1731-1764. This research examines the effectiveness of technical trading rules, relevant for streak-based strategies.

Fama, E. F., & French, K. R. (1993). "Common Risk Factors in the Returns on Stocks and Bonds." Journal of Financial Economics, 33(1), 3-56. This paper provides a foundation for understanding risk factors and strategy performance.

By analyzing streaks, traders can gain valuable insights into market dynamics and refine their trading strategies based on empirical evidence.

TPS Short Strategy by Larry ConnersThe TPS Short strategy aims to capitalize on extreme overbought conditions in an ETF by employing a scaling-in approach when certain technical indicators signal potential reversals. The strategy is designed to short the ETF when it is deemed overextended, based on the Relative Strength Index (RSI) and moving averages.

Components:

200-Day Simple Moving Average (SMA):

Purpose: Acts as a long-term trend filter. The ETF must be below its 200-day SMA to be eligible for shorting.

Rationale: The 200-day SMA is widely used to gauge the long-term trend of a security. When the price is below this moving average, it is often considered to be in a downtrend (Tushar S. Chande & Stanley Kroll, "The New Technical Trader: Boost Your Profit by Plugging Into the Latest Indicators").

2-Period RSI:

Purpose: Measures the speed and change of price movements to identify overbought conditions.

Criteria: Short 10% of the position when the 2-period RSI is above 75 for two consecutive days.

Rationale: A high RSI value (above 75) indicates that the ETF may be overbought, which could precede a price reversal (J. Welles Wilder, "New Concepts in Technical Trading Systems").

Scaling-In Mechanism:

Purpose: Gradually increase the short position as the ETF price rises beyond previous entry points.

Scaling Strategy:

20% more when the price is higher than the first entry.

30% more when the price is higher than the second entry.

40% more when the price is higher than the third entry.

Rationale: This incremental approach allows for an increased position size in a worsening trend, potentially increasing profitability if the trend continues to align with the strategy’s premise (Marty Schwartz, "Pit Bull: Lessons from Wall Street's Champion Day Trader").

Exit Conditions:

Criteria: Close all positions when the 2-period RSI drops below 30 or the 10-day SMA crosses above the 30-day SMA.

Rationale: A low RSI value (below 30) suggests that the ETF may be oversold and could be poised for a rebound, while the SMA crossover indicates a potential change in the trend (Martin J. Pring, "Technical Analysis Explained").

Risks and Considerations:

Market Risk:

The strategy assumes that the ETF will continue to decline once shorted. However, markets can be unpredictable, and price movements might not align with the strategy's expectations, especially in a volatile market (Nassim Nicholas Taleb, "The Black Swan: The Impact of the Highly Improbable").

Scaling Risks:

Scaling into a position as the price increases may increase exposure to adverse price movements. This method can amplify losses if the market moves against the position significantly before any reversal occurs.

Liquidity Risk:

Depending on the ETF’s liquidity, executing large trades in increments might affect the price and increase trading costs. It is crucial to ensure that the ETF has sufficient liquidity to handle large trades without significant slippage (James Altucher, "Trade Like a Hedge Fund").

Execution Risk:

The strategy relies on timely execution of trades based on specific conditions. Delays or errors in order execution can impact performance, especially in fast-moving markets.

Technical Indicator Limitations:

Technical indicators like RSI and SMA are based on historical data and may not always predict future price movements accurately. They can sometimes produce false signals, leading to potential losses if used in isolation (John Murphy, "Technical Analysis of the Financial Markets").

Conclusion

The TPS Short strategy utilizes a combination of long-term trend filtering, overbought conditions, and incremental shorting to potentially profit from price reversals. While the strategy has a structured approach and leverages well-known technical indicators, it is essential to be aware of the inherent risks, including market volatility, liquidity issues, and potential limitations of technical indicators. As with any trading strategy, thorough backtesting and risk management are crucial to its successful implementation.

Currency Futures StatisticsThe "Currency Futures Statistics" indicator provides comprehensive insights into the performance and characteristics of various currency futures. This indicator is crucial for portfolio management as it combines multiple metrics that are instrumental in evaluating currency futures' risk and return profiles.

Metrics Included:

Historical Volatility:

Definition: Historical volatility measures the standard deviation of returns over a specified period, scaled to an annual basis.

Importance: High volatility indicates greater price fluctuations, which translates to higher risk. Investors and portfolio managers use volatility to gauge the stability of a currency future and to make informed decisions about risk management and position sizing (Hull, J. C. (2017). Options, Futures, and Other Derivatives).

Open Interest:

Definition: Open interest represents the total number of outstanding futures contracts that are held by market participants.

Importance: High open interest often signifies liquidity in the market, meaning that entering and exiting positions is less likely to impact the price significantly. It also reflects market sentiment and the degree of participation in the futures market (Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities).

Year-over-Year (YoY) Performance:

Definition: YoY performance calculates the percentage change in the futures contract's price compared to the same week from the previous year.

Importance: This metric provides insight into the long-term trend and relative performance of a currency future. Positive YoY performance suggests strengthening trends, while negative values indicate weakening trends (Fama, E. F. (1991). Efficient Capital Markets: II).

200-Day Simple Moving Average (SMA) Position:

Definition: This metric indicates whether the current price of the currency future is above or below its 200-day simple moving average.

Importance: The 200-day SMA is a widely used trend indicator. If the price is above the SMA, it suggests a bullish trend, while being below indicates a bearish trend. This information is vital for trend-following strategies and can help in making buy or sell decisions (Bollinger, J. (2001). Bollinger on Bollinger Bands).

Why These Metrics are Important for Portfolio Management:

Risk Assessment: Historical volatility and open interest provide essential information for assessing the risk associated with currency futures. Understanding the volatility helps in estimating potential price swings, which is crucial for managing risk and setting appropriate stop-loss levels.

Liquidity and Market Participation: Open interest is a critical indicator of market liquidity. Higher open interest usually means tighter bid-ask spreads and better liquidity, which facilitates smoother trading and better execution of trades.

Trend Analysis: YoY performance and the SMA position help in analyzing long-term trends. This analysis is crucial for making strategic investment decisions and adjusting the portfolio based on changing market conditions.

Informed Decision-Making: Combining these metrics allows for a holistic view of the currency futures market. This comprehensive view helps in making informed decisions, balancing risks and returns, and optimizing the portfolio to align with investment goals.

In summary, the "Currency Futures Statistics" indicator equips investors and portfolio managers with valuable data points that are essential for effective risk management, liquidity assessment, trend analysis, and overall portfolio optimization.

Sygnały Long/Short z SL i TPChoosing the Best Timeframe for Your Trading Strategy

The ideal timeframe for your trading strategy depends on several factors, including your trading style, risk preferences, and the goals of your strategy. Here’s a guide to different timeframes and their applications:

Timeframes and Their Uses:

Short-Term Timeframes (e.g., 5-minute, 15-minute):

Advantages: Provide more frequent signals and allow for quick responses to market changes. Ideal for day traders who prefer short, rapid trades.

Disadvantages: Can generate more false signals and be more susceptible to market noise. Requires more frequent attention and monitoring.

Medium-Term Timeframes (e.g., 1-hour, 4-hour):

Advantages: Offer fewer false signals compared to shorter timeframes. Suitable for swing traders looking to capture short-term trends.

Disadvantages: Fewer signals compared to shorter timeframes. Requires less frequent monitoring.

Long-Term Timeframes (e.g., daily, weekly):

Advantages: Provide more stable signals and are less affected by market noise. Ideal for long-term investors and those trading based on trends.

Disadvantages: Fewer signals, which may be less frequent but more reliable. Requires longer confirmation times.

Recommendation for Your Strategy:

For a strategy based on moving averages (MA) and generating long/short signals, the 5-minute and 15-minute timeframes might be suitable if:

You are a day trader and want to generate multiple signals per day.

You prefer quick responses to price changes and want to execute trades within a shorter timeframe.

For more stable signals and fewer false signals:

1-hour or 4-hour timeframes might be more appropriate.

Testing and Optimization:

Test Different Timeframes: See how your strategy performs on various timeframes to find the one that works best for you.

Adjust Parameters: Modify the lengths of the short and long SMAs, as well as the SL and TP levels, to fit the chosen timeframe.

How to Test:

Add the script to your chart on different timeframes on TradingView.

Observe the effectiveness and accuracy of the signals.

Adjust settings based on results and personal preferences.

Summary:

There isn’t a single “best” timeframe as it depends on your trading style and objectives. Start by testing on shorter timeframes if you are interested in day trading, and then explore how the strategy performs on longer timeframes for more stable signals.

Lot Size per CandleThis script indicates the lotsize based on your accountsize and risk per trade.

You have the option to select account in EUR or USD. You can set account size and risk%.

Valid for next combination of currencies:

EUR

JPY

GBP

AUD

CHF

CAD

XAUUSD

Correlation with AveragesThe "Correlation with Averages" indicator is designed to visualize and analyze the correlation between a selected asset's price and a base symbol's price, such as the S&P 500 (SPY). This indicator allows users to evaluate how closely an asset’s price movements align with those of the base symbol over various time periods, providing insights into market trends and potential portfolio adjustments.

Key Features:

Base Symbol and Correlation Period:

Users can specify the base symbol (default is SPY) and the period for correlation measurement (default is 252 trading days, approximating one year).

Correlation Calculation:

The indicator computes the correlation between the asset’s closing price and the base symbol’s closing price for the defined period.

Visualization:

The correlation value is plotted on the chart, with conditional background colors indicating the strength and direction of the correlation:

Red for negative correlation (below -0.5)

Green for positive correlation (above 0.5)

Yellow for neutral correlation (between -0.5 and 0.5)

Average Correlation Over Time:

Average correlations are calculated and displayed for various periods: one week, one month, one year, and five years.

A table on the chart provides dynamic updates of these average values with color-coded backgrounds to indicate correlation strength.

The Role of Correlation in Portfolio Management

Correlation is a crucial concept in portfolio management because it measures the degree to which two securities move in relation to each other. Understanding correlation helps investors construct diversified portfolios that balance risk and return. Here's why correlation is important:

Diversification:

By including assets with low or negative correlation in a portfolio, investors can reduce overall portfolio volatility and risk. For instance, if one asset is negatively correlated with another, when one performs poorly, the other may perform well, thus smoothing the overall returns.

Risk Management:

Correlation analysis helps in identifying the potential impact of one asset’s performance on the entire portfolio. Assets with high correlation can lead to concentrated risk, while those with low correlation offer better risk management.

Performance Analysis:

Correlation measures the degree to which asset returns move together. This can inform strategic decisions, such as whether to adjust positions based on expected market conditions.

Scientific References

Markowitz, H. M. (1952). "Portfolio Selection." Journal of Finance, 7(1), 77-91.

This foundational paper introduced Modern Portfolio Theory, highlighting the importance of diversification and correlation in reducing portfolio risk.

Jorion, P. (2007). Financial Risk Manager Handbook. Wiley.

This handbook provides an in-depth exploration of risk management techniques, including the use of correlation in portfolio management.

Elton, E. J., Gruber, M. J., Brown, S. J., & Goetzmann, W. N. (2014). Modern Portfolio Theory and Investment Analysis. Wiley.

This book elaborates on the concepts of correlation and diversification, offering practical insights into portfolio construction and risk management.

By utilizing the "Correlation with Averages" indicator, traders and portfolio managers can make informed decisions based on the relationship between asset prices and the base symbol, ultimately enhancing their investment strategies.

Risk TrackerThis Risk Tracker Pine Script provides traders with a customizable tool for tracking and managing trade risk directly on their chart. The script is designed to accommodate both futures and crypto trades, allowing you to monitor risk and reward parameters, adjust contract sizes, and manage leverage in real-time.

Key Features:

1. Trade Direction and Risk-Reward Ratio:

• Select between Long or Short trade directions.

• Set a custom Risk-Reward Ratio (RRR) to calculate potential profit and loss levels based on your trade setup.

2. Customizable Parameters:

• Input fields for contract size, leverage, margin, and maximum drawdown allow you to adjust the risk settings depending on the market you are trading.

• You can toggle between using a dollar-based or percentage-based risk calculation depending on whether you’re trading futures (USD-based) or crypto.

3. Real-time Stop-Loss and Take-Profit Calculation:

• The script automatically calculates and draws the Stop-Loss (SL) and Take-Profit (TP) levels on the chart based on your entry price and selected risk settings.

• The color of the SL and TP lines is customizable, allowing you to visually distinguish profit and loss levels.

4. Historical Price Levels:

• If there is no active trade, the script scans historical price data to find the last instances when the price hit the predefined stop-loss or take-profit levels, helping you understand past price behavior.

5. Risk Management Table:

• A summary table is displayed on the chart, showing the key metrics of your trade, including:

• Tick value and Dollar value for futures.

• Margin and Leverage for crypto.

• Risk-Reward Ratio, Entry price, Risk and Profit in USD or percentage terms.