Trend Strength [OmegaTools]Trend Strength is a quantitative regime oscillator designed to measure directional pressure and trend quality by blending price structure, return-dependence, realized intrabar expansion, and volume participation into a single normalized signal. The goal is not to predict, but to classify market state: when price action is in an expansionary/distributionary phase versus when it is in a contractionary/accumulation phase, so you can align execution and risk with the prevailing environment.

Core concept and methodology

The indicator aggregates four components computed on stable rolling windows and mapped into comparable ranges:

1. Price location / structural positioning (100-bar range)

A normalized price-location metric (position of close within the rolling high–low range) is transformed into a non-linear “strength” profile. This emphasizes meaningful departures from the middle of the range and penalizes indecision, producing a structure-aware contribution rather than a raw oscillator.

2. Return-dependence / directional persistence (100 bars)

A correlation term measures the relationship between the current return (close − close ) and the prior price level (close ). This helps detect environments where movement is more persistent or more mean-reverting, providing a statistical component that complements pure price-location signals.

3. Realized expansion / volatility proxy (50-bar accumulation, 300-bar normalization)

Intrabar expansion is approximated via the absolute candle body relative to the full range, aggregated over a short window to represent realized “effort” and then normalized over a longer window. This captures whether price is moving with meaningful body expansion versus compressing and stalling.

4. Volume participation (11-bar accumulation, 300-bar normalization)

A rolling volume sum is normalized over a longer window to quantify participation. This helps separate “thin” moves from moves supported by broader activity, without relying on exchange-specific volume assumptions.

The final oscillator is a weighted blend of these four normalized components, scaled for readability. The output is intentionally centered around two actionable regimes rather than a symmetric overbought/oversold framework.

How to read the oscillator

Trend Strength is designed around two main thresholds:

- Distribution / Expansion regime (oscillator above 0)

When the oscillator is above 0, the market is classified as being in a higher-pressure expansion regime. This often corresponds to directional continuation potential, stronger impulse behavior, and reduced suitability for tight mean-reversion tactics.

- Accumulation / Contraction regime (oscillator below −1.3)

When the oscillator is below −1.3, the market is classified as being in a contraction/accumulation regime. This frequently corresponds to compression, rotation, and lower directional efficiency, where breakouts may be more fragile and mean-reversion tactics may be more appropriate (depending on instrument and session conditions).

Values between 0 and −1.3 are treated as transitional/neutral, where the market is not clearly committing to either regime.

Continuous Mode vs Standard Mode

Trend Strength includes an optional Continuous Mode to improve interpretability during regime transitions:

- Standard Mode colors only when the oscillator is firmly in one of the two regimes (above 0 or below −1.3). Neutral zones remain uncolored, keeping the display conservative.

- Continuous Mode adds persistence logic: once a regime is confirmed, intermediate values are rendered with a lighter shade of the last confirmed regime until the opposite regime is confirmed. This reduces visual noise, helps maintain a consistent directional bias framework, and is particularly useful for intraday execution and session trend management.

Visual design and bar coloring

The oscillator line is color-coded:

- Purple: distribution / expansion regime

- Orange: accumulation / contraction regime

Neutral/transitional values are displayed in grey (or lightly shaded in Continuous Mode based on last confirmed regime).

Optionally, the indicator can color price bars using the same regime logic, allowing rapid at-a-glance regime recognition directly on the chart.

Practical use cases

- Regime filter for strategies: enable trend-following logic only in expansion regimes; enable mean-reversion or range logic in contraction regimes.

- Risk adjustment: increase/decrease position sizing or tighten/widen stops based on regime classification.

- Confirmation layer: combine with structure tools (market structure, VWAP, key levels) to validate whether conditions support continuation or imply compression.

- Session management: identify when a session is behaving as a trend day versus a rotational day, improving trade selection and reducing overtrading.

Notes

Trend Strength is a regime classifier and contextual tool. It does not guarantee future direction and should be integrated into a complete decision process (risk management, market structure, session context, and instrument-specific behavior).

© OmegaTools

Phaseaccumulation

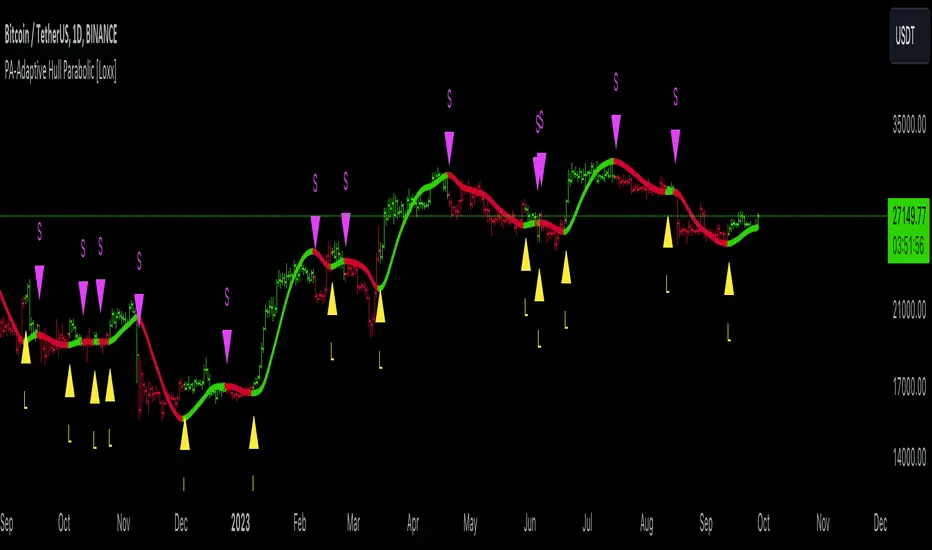

PA-Adaptive Hull Parabolic [Loxx]The PA-Adaptive Hull Parabolic is not your typical trading indicator. It synthesizes the computational brilliance of two famed technicians: John Ehlers and John Hull. Let's demystify its sophistication.

█ Ehlers' Phase Accumulation

John Ehlers is well-known in the trading community for his digital signal processing approach to market data. One of his standout techniques is phase accumulation. This method identifies the dominant cycle in the market by accumulating the phases of individual cycles. By doing so, it "adapts" to real-time market conditions.

Here's the brilliance of phase accumulation in this code

The indicator doesn't merely use a static look-back period. Instead, it dynamically determines the dominant market cycle through phase accumulation.

The calcComp function, rooted in Ehlers' methodology, provides a complex computation using a digital signal processing approach to filter out market noise and pinpoint the current cycle's frequency.

By measuring and adapting to the instantaneous period of the market, it ensures that the indicator remains relevant, especially in non-stationary market conditions.

Hull's Moving Average

John Hull introduced the Hull Moving Average (HMA) aiming to reduce lag and improve smoothing. The HMA's essence lies in its weighted average computation, prioritizing more recent prices.

This code takes an adaptive twist on the HMA

Instead of a fixed period, the HMA uses the dominant cycle length derived from Ehlers' phase accumulation. This makes the HMA not just fast and smooth, but also adaptive to the dominant market rhythm.

The intricate iLwmp function in the script provides this adaptive HMA computation. It's a weighted moving average, but its length isn't static; it's based on the previously determined dominant market cycle.

█ Trading Insights

The indicator paints the bars to represent the immediate trend: green for bullish and red for bearish.

Entry points, both long ("L") and short ("S"), are presented visually. These are derived from crossovers of the adaptive HMA, a clear indication of a potential shift in the trend.

Additionally, alert conditions are set, ready to notify a trader when these crossovers occur, ensuring real-time actionable insights.

█ Conclusion

The PA-Adaptive Hull Parabolic is a masterclass in advanced technical indicator design. By marrying John Ehlers' adaptive phase accumulation with John Hull's HMA, it creates a dynamic, responsive, and precise tool for traders. It's not just about capturing the trend; it's about understanding the very rhythm of the market.

PA-Adaptive T3 Loxxer [Loxx]PA-Adaptive T3 Loxxer is a Loxxer indicator that is Phase Accumulation Cycle adaptive and uses T3 moving average for smoothing instead of the typical SMA or EMA . this allows for smoother signals by reducing noise.

What is Loxxer?

The Loxxer indicator is a technical analysis tool that compares the most recent maximum and minimum prices to the previous period's equivalent price to measure the demand of the underlying asset.

What is the Phase Accumulation Cycle?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included

Bar coloring

Signals

Alerts

Loxx's Expanded Source Types

Divergences

PA-Adaptive Polynomial Regression Fitted Moving Average [Loxx]PA-Adaptive Polynomial Regression Fitted Moving Average is a moving average that is calculated using Polynomial Regression Analysis. The purpose of this indicator is to introduce polynomial fitting that is to be used in future indicators. This indicator also has Phase Accumulation adaptive period inputs. Even though this first indicator is for demonstration purposes only, its still one of the only viable implementations of Polynomial Regression Analysis on TradingView is suitable for trading, and while this same method can be used to project prices forward, I won't be doing that since forecasting is generally worthless and causes unavoidable repainting. This indicator only repaints on the current bar. Once the bar closes, any signal on that bar won't change.

For other similar Polynomial Regression Fitted methodologies, see here

Poly Cycle

What is the Phase Accumulation Cycle?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

What is Polynomial Regression?

In statistics, polynomial regression is a form of regression analysis in which the relationship between the independent variable x and the dependent variable y is modelled as an nth degree polynomial in x. Polynomial regression fits a nonlinear relationship between the value of x and the corresponding conditional mean of y, denoted E(y |x). Although polynomial regression fits a nonlinear model to the data, as a statistical estimation problem it is linear, in the sense that the regression function E(y | x) is linear in the unknown parameters that are estimated from the data. For this reason, polynomial regression is considered to be a special case of multiple linear regression.

Things to know

You can select from 33 source types

The source is smoothed before being injected into the Polynomial fitting algorithm, there are 35+ moving averages to choose from for smoothing

The output of the Polynomial fitting algorithm is then smoothed to create the signal, there are 35+ moving averages to choose from for smoothing

Included

Alerts

Signals

Bar coloring

PA-Adaptive TRIX Log [Loxx]PA-Adaptive TRIX Log is a Phase Accumulation Adaptive TRIX Log indicator. This adaptation smooths the signal to catch larger trends.

What is TRIX?

TRIX is a momentum oscillator that displays the percent rate of change of a TEMA . It was developed in the early 1980's by Jack Hutson, an editor for "Technical Analysis of Stocks and Commodities" magazine. With its triple smoothing, TRIX is designed to filter insignificant price movements. In his article he uses a logarithm of a price (which is in many versions, left out).

What is the Phase Accumulation Cycle?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included

Bar coloring

2 signal options

Alerts

PA-Adaptive, Stepped-MA of Composite RSI [Loxx]PA-Adaptive, Stepped-MA of Composite RSI is an RSI indicator using a different kind of RSI called Composite RSI. This indicator is Phase Accumulation Cycle Adaptive and uses a stepped moving average.

What is Composite RSI?

The name of the composite RSI might mislead a bit.

Composite RSI is not "compositing" RSIs but is a rather new way of calculating the RSI. Unlike the RSI that is a sort of a momentum indicators, composite RSI is more a trending indicator. It tends to filter out insignificant price changes and seems to be good in identifying the underlying trends.

What is the Phase Accumulation Cycle?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included

Bar coloring

Signals

Alerts

Loxx's Expanded Source Types

Loxx's Special Phase Accumulation Cycle

PA-Adaptive MACD w/ Variety Levels [Loxx]PA-Adaptive MACD w/ Variety Levels is a Phase Accumulation Adaptive MACD with both floating and quantile levels. This is tuned for Forex. You'll have to adjust the Phase Accumulation Cycle settings to work for crypto and stock markets.

What is MACD?

Moving average convergence divergence ( MACD ) is a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price. The MACD is calculated by subtracting the 26-period exponential moving average ( EMA ) from the 12-period EMA .

What is the Phase Accumulation Cycle?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included:

Zero-line and signal cross options for bar coloring, signals, and alerts

Alerts

Signals

Loxx's Expanded Source Types

4 moving average types

Phase Accumulation Adaptive Fisher Transform [Loxx]Phase Accumulation Adaptive Fisher Transform is an adaptive Fisher Transform using a modified version of Ehlers Phase Accumulation Cycle Period. This version of Phase Accumulation Cylce Period accepts as inputs: 1) total number of cycles you wish to inject into the calculation, this works as a multiplier so the higher this number, the longer the period output; 2) filter is to change the alpha value of the final smother before returning the period output.

What is the Phase Accumulation Cycle?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

What is Fisher Transform?

The Fisher Transform is a technical indicator created by John F. Ehlers that converts prices into a Gaussian normal distribution.

The indicator highlights when prices have moved to an extreme, based on recent prices. This may help in spotting turning points in the price of an asset. It also helps show the trend and isolate the price waves within a trend.

Included:

Zero-line and signal cross options for bar coloring

Customizable overbought/oversold thresh-holds

Alerts

Signals

loxxpaaspecialLibrary "loxxpaaspecial"

loxxpaaspecial: Ehlers Phase Accumulation Dominant Cycle Period with multiplier and filter

paa(src, mult, filt)

(src, mult, filt)

Parameters:

src : float

mult : float

filt : float

Returns: result float

Phase-Accumulation Adaptive RSX w/ Expanded Source Types [Loxx]Phase-Accumulation Adaptive RSX w/ Expanded Source Types is a Phase Accumulation Adaptive Jurik RSX.

What is RSX?

RSI is a very popular technical indicator, because it takes into consideration market speed, direction and trend uniformity. However, the its widely criticized drawback is its noisy (jittery) appearance. The Jurk RSX retains all the useful features of RSI , but with one important exception: the noise is gone with no added lag.

What is Phase Accumulation?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included:

-Toggle on/off bar coloring

Phase-Accumulation Adaptive EMA w/ Expanded Source Types [Loxx]Phase-Accumulation Adaptive EMA w/ Expanded Source Types is a Phase Accumulation Adaptive Exponential Moving Average with Loxx's Expanded Source Types. This indicator is meant to better capture trend movements using dominant cycle inputs. Alerts are included.

What is Phase Accumulation?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included:

-Toggle on/off bar coloring

-Alerts

Phase Accumulation, Smoothed Williams %R Histogram [Loxx]Phase Accumulation, Smoothed Williams %R Histogram is a Williams %R indicator using dynamic inputs from Ehlers Phase Accumulation Dominant Cycle Period Algorithm. This indicator includes alerts and signals and is in a smoothed histogram form. The version of Phase Accumulation in this indicator is a modified form of of Ehlers algorithm to allow for better smoothing and cycle length selection.

What is Williams %R?

Williams %R , also known as the Williams Percent Range, is a type of momentum indicator that moves between 0 and -100 and measures overbought and oversold levels. The Williams %R may be used to find entry and exit points in the market. The indicator is very similar to the Stochastic oscillator and is used in the same way. It was developed by Larry Williams and it compares a stock’s closing price to the high-low range over a specific period, typically 14 days or periods.

What is Phase Accumulation?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included:

-Toggle on/off bar coloring

-Toggle on/off signals

-Alerts long/short

-Loxx's Expanded Source Types Library

DominantCycleCollection of Dominant Cycle estimators. Length adaptation used in the Adaptive Moving Averages and the Adaptive Oscillators try to follow price movements and accelerate/decelerate accordingly (usually quite rapidly with a huge range). Cycle estimators, on the other hand, try to measure the cycle period of the current market, which does not reflect price movement or the rate of change (the rate of change may also differ depending on the cycle phase, but the cycle period itself usually changes slowly). This collection may become encyclopaedic, so if you have any working cycle estimator, drop me a line in the comments below. Suggestions are welcome. Currently included estimators are based on the work of John F. Ehlers

mamaPeriod(src, dynLow, dynHigh) MESA Adaptation - MAMA Cycle

Parameters:

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

Returns: Calculated period

Based on MESA Adaptive Moving Average by John F. Ehlers

Performs Hilbert Transform Homodyne Discriminator cycle measurement

Unlike MAMA Alpha function (in LengthAdaptation library), this does not compute phase rate of change

Introduced in the September 2001 issue of Stocks and Commodities

Inspired by the @everget implementation:

Inspired by the @anoojpatel implementation:

paPeriod(src, dynLow, dynHigh, preHP, preSS, preHP) Pearson Autocorrelation

Parameters:

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

preHP : Use High Pass prefilter (default)

preSS : Use Super Smoother prefilter (default)

preHP : Use Hann Windowing prefilter

Returns: Calculated period

Based on Pearson Autocorrelation Periodogram by John F. Ehlers

Introduced in the September 2016 issue of Stocks and Commodities

Inspired by the @blackcat1402 implementation:

Inspired by the @rumpypumpydumpy implementation:

Corrected many errors, and made small speed optimizations, so this could be the best implementation to date (still slow, though, so may revisit in future)

High Pass and Super Smoother prefilters are used in the original implementation

dftPeriod(src, dynLow, dynHigh, preHP, preSS, preHP) Discrete Fourier Transform

Parameters:

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

preHP : Use High Pass prefilter (default)

preSS : Use Super Smoother prefilter (default)

preHP : Use Hann Windowing prefilter

Returns: Calculated period

Based on Spectrum from Discrete Fourier Transform by John F. Ehlers

Inspired by the @blackcat1402 implementation:

High Pass, Super Smoother and Hann Windowing prefilters are used in the original implementation

phasePeriod(src, dynLow, dynHigh, preHP, preSS, preHP) Phase Accumulation

Parameters:

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

preHP : Use High Pass prefilter (default)

preSS : Use Super Smoother prefilter (default)

preHP : Use Hamm Windowing prefilter

Returns: Calculated period

Based on Dominant Cycle from Phase Accumulation by John F. Ehlers

High Pass and Super Smoother prefilters are used in the original implementation

doAdapt(type, src, len, dynLow, dynHigh, chandeSDLen, chandeSmooth, chandePower, preHP, preSS, preHP) Execute a particular Length Adaptation or Dominant Cycle Estimator from the list

Parameters:

type : Length Adaptation or Dominant Cycle Estimator type to use

src : Series to use

len : Reference lookback length

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

chandeSDLen : Lookback length of Standard deviation for Chande's Dynamic Length

chandeSmooth : Smoothing length of Standard deviation for Chande's Dynamic Length

chandePower : Exponent of the length adaptation for Chande's Dynamic Length (lower is smaller variation)

preHP : Use High Pass prefilter for the Estimators that support it (default)

preSS : Use Super Smoother prefilter for the Estimators that support it (default)

preHP : Use Hann Windowing prefilter for the Estimators that support it

Returns: Calculated period (float, not limited)

doEstimate(type, src, dynLow, dynHigh, preHP, preSS, preHP) Execute a particular Dominant Cycle Estimator from the list

Parameters:

type : Dominant Cycle Estimator type to use

src : Series to use

dynLow : Lower bound for the dynamic length

dynHigh : Upper bound for the dynamic length

preHP : Use High Pass prefilter for the Estimators that support it (default)

preSS : Use Super Smoother prefilter for the Estimators that support it (default)

preHP : Use Hann Windowing prefilter for the Estimators that support it

Returns: Calculated period (float, not limited)