盯盘-平均K线图This is a Pine Script v6 indicator/strategy designed to assist traders with clear, configurable trend and momentum signals. It combines adaptive filters and volatility-aware logic to highlight high‑quality entries and exits, includes optional multi‑timeframe confirmation, and supports risk controls such as stop loss/target levels. Signals are visualized directly on the chart with arrows/labels and can trigger TradingView alerts for real‑time notifications. The tool offers smoothing and sensitivity settings to tune responsiveness, overlay mode for price action, and strategy mode for backtesting performance. It’s built to be lightweight, transparent, and easy to adjust, helping traders streamline decision‑making while maintaining control over parameters and risk.

Indicadores e estratégias

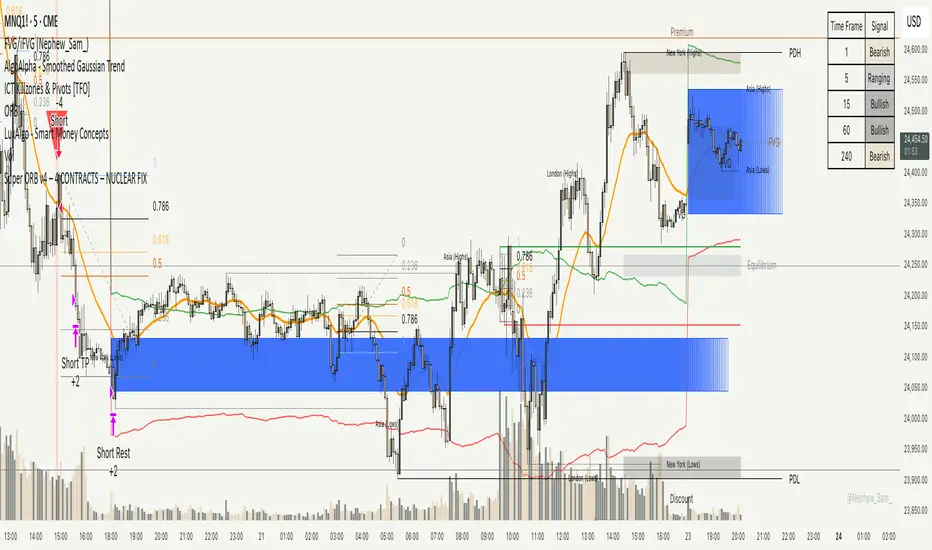

Super ORB v4 – 4 CONTRACTS – NUCLEAR FIXORB hands off printer, this is to gauge how few trades can happen off the ORB while not trading after hours either. Should be in the 5% a month range 4 contracts, no more than 5 trades a month.

Optimized EMA Ribbon Strategy v6 Based on EMA rotations, ADX we create a system of entering trades. Watch out for the sell and buy signals.

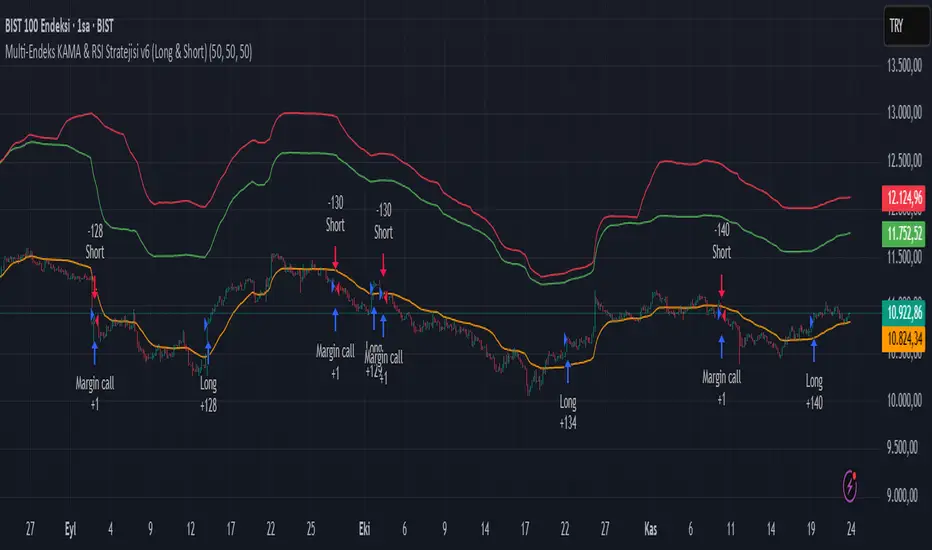

Multi-Endeks KAMA & RSI Stratejisi v6 (Long & Short)Multi-Index KAMA & RSI Strategy v6 (Long & Short)

This is a hybrid trading strategy that combines two powerful technical analysis tools—the Kaufman's Adaptive Moving Average (KAMA) for trend following and the Relative Strength Index (RSI) for measuring momentum and identifying overbought/oversold conditions.

The term "Multi-Index" suggests that the decision-making process might incorporate data or conditions from several different market indices or timeframes, rather than just the single asset being traded.

🧭 Core Components

1. KAMA (Kaufman's Adaptive Moving Average)

KAMA is an adaptive moving average developed by quantitative financial theorist Perry J. Kaufman.

Adaptivity: Unlike standard moving averages, KAMA automatically adjusts its smoothing factor (speed) based on market volatility.

Mechanism:

Trending Markets (Low Noise): When prices move clearly in one direction (low volatility), KAMA speeds up, hugging the price closely and providing fast signals.

Sideways Markets (High Noise): When prices are choppy (high volatility/noise), KAMA slows down, smoothing out price fluctuations to reduce the risk of whipsaws (false signals).

Role in Strategy: To define the main trend direction. The position of the price relative to the KAMA line determines the base directional bias (Long or Short).

2. RSI (Relative Strength Index)

RSI is a momentum oscillator developed by J. Welles Wilder Jr. that measures the speed and change of price movements.

Overbought/Oversold: It oscillates between 0 and 100. Conventionally, a reading above 70 suggests overbought conditions (potential sell signal), and a reading below 30 suggests oversold conditions (potential buy signal).

Role in Strategy: Timing and Confirmation. Once the trend is confirmed by KAMA, the RSI acts as a timing filter, often confirming an entry as it moves away from extreme overbought (for Short) or oversold (for Long) levels.

📉 Potential Trading Logic (V6)

This "v6" strategy likely aims to capture more reliable entries by requiring both trend (KAMA) and momentum (RSI) alignment:

1. LONG (Buy) Entry Conditions

Trend Confirmation (KAMA): The asset's price (Closing Price) must be above the KAMA line (confirming an uptrend).

Momentum Confirmation (RSI):

Option A (Reversal): The RSI must cross above the 30 level (exiting oversold) or decisively move above the 50 level.

Option B (Trend-Continuation): In a strong uptrend, the RSI might bounce off the 40-50 zone and turn upwards, confirming trend continuation.

2. SHORT (Sell) Entry Conditions

Trend Confirmation (KAMA): The asset's price (Closing Price) must be below the KAMA line (confirming a downtrend).

Momentum Confirmation (RSI):

Option A (Reversal): The RSI must cross below the 70 level (exiting overbought) or decisively move below the 50 level.

Option B (Trend-Continuation): In a strong downtrend, the RSI might be rejected from the 50-60 zone and turn downwards, confirming continuation.

3. Exit Management

The strategy likely utilizes dynamic risk controls:

Stop-Loss: A dynamic stop placed on the opposite side of the KAMA, or an ATR-based distance to adjust to volatility.

Take-Profit: Conditions such as the RSI reaching extreme levels or the KAMA line being crossed in the reverse direction.

🌟 Implication of the "V6" Version

The "v6" designation implies that the strategy has been refined and iterated upon over time to address weaknesses in prior versions (v1, v2, etc.). These improvements might include:

Filters: Adding stricter RSI or KAMA cross filters to reduce false signals.

Multi-Index Logic: Using the RSI or KAMA of a secondary instrument (e.g., a major index or volatility measure) as a macro filter for the main trade execution.

Optimization: Optimizing the default lookback periods for KAMA and RSI for different asset classes.

EMA Velocity Dual TF Momentum 1h (v2)BINANCE:SOLUSDT

The result is calculated on futures x10

### EMA Velocity Dual TF Momentum (v2) – Public Description

**Overview**

EMA Velocity Dual TF Momentum (v1) is a trend-following momentum strategy that uses the *speed of change* of Exponential Moving Averages (EMA) on two timeframes: the chart timeframe 1h.

The strategy looks for moments when both timeframes point in the same direction and the short‑term momentum is significantly stronger than usual, then manages trades with configurable ATR filtering, stop‑loss / take‑profit and early exit logic.

---

### Core Idea (high level, without formulas)

- On the **lower timeframe** (LTF), the strategy tracks how fast the EMA is moving (its “velocity”) and detects **impulse bars** where this velocity is unusually strong compared to its recent history.

- On the **higher timeframe** (HTF), it also measures EMA velocity and requires that the HTF trend direction is **aligned** with the LTF (both bullish or both bearish), if enabled.

- A **long trade** is opened when:

- LTF EMA velocity is positive (upward momentum),

- LTF momentum is strong enough (impulse),

- HTF EMA velocity is also upwards (if HTF filter is enabled),

- and ATR‑based volatility is above the minimum threshold.

- A **short trade** is opened in the symmetric situation (downward momentum on both timeframes).

- Positions are closed using configurable stop‑loss and take‑profit, and can be partially exited, moved to break‑even and trailed using early‑exit options.

---

### Inputs and Parameters

#### Trend & Momentum (Lower Timeframe)

- **`LTF EMA length (emaLenLTF)`**

Length of the EMA on the chart timeframe used to measure short‑term trend and momentum. Smaller values react faster; larger values are smoother and slower.

- **`LTF velocity lookback (velKLTF)`**

Lookback for computing EMA “velocity” on LTF. Controls how sensitive the momentum calculation is to recent price changes.

- **`LTF impulse lookback bars (impLookback)`**

Window size used to estimate the “normal” average absolute velocity. The strategy compares current momentum against this baseline to detect strong impulse moves.

- **`LTF |velocity| multiplier vs average (impMult)`**

Multiplier for defining what counts as a strong impulse. Higher values = fewer but stronger signals; lower values = more frequent, weaker impulses.

#### Trend & Momentum (Higher Timeframe)

- **`Use higher timeframe alignment (useHTF)`**

If enabled, trades are only taken when the higher‑timeframe EMA velocity confirms the same direction as the lower timeframe.

- **`HTF timeframe (htf_tf)`**

Higher timeframe used for confirmation (e.g. 60 minutes). Defines the “macro” context above the chart timeframe.

- **`HTF EMA length (emaLenHTF)`**

Length of the EMA on the higher timeframe. Controls how smooth and slow the higher‑timeframe trend filter is.

- **`HTF velocity lookback (velKHTF)`**

Lookback for the EMA velocity on HTF. Smaller values react quicker to changes in the higher‑timeframe trend.

#### Volatility / ATR Filter

- **`Use ATR filter (useAtrFilter)`**

Enables a volatility filter based on Average True Range. When active, trades are allowed only if market volatility is not too low.

- **`ATR Period (atrPeriod)`**

Lookback period for ATR calculation. Shorter periods react faster to recent volatility shifts; longer ones are more stable.

- **`ATR Min % for trading (atrMinPerc)`**

Minimum ATR as a percentage of price required to trade. Filters out very quiet, choppy periods where the strategy is more likely to be whipsawed.

#### Risk Management

- **`Use stops (SL/TP) (useStops)`**

Enables fixed stop‑loss and take‑profit exits. If disabled, positions are managed only by early exit logic and manual closing.

- **`Stop Loss % (stopLossPerc)`**

Distance of the protective stop from entry, in percent. Higher values give trades more room but increase risk per trade.

- **`Take Profit % (takeProfitPerc)`**

Distance of the primary profit target from entry, in percent. Controls the reward‑to‑risk profile of each trade.

#### Early Exit / Break‑Even / Trailing

- **`Enable early exit module (useEarlyExit)`**

Master switch for all early exit features: partial profit taking, break‑even stops and trailing exits.

- **`Take partial profit at +% (close 50%) (partialTP)`**

Profit level (in %) at which the strategy closes a partial portion of the position (e.g. 50%), locking in gains while leaving a runner.

- **`Trailing TP distance (%) (trailTP)`**

Distance (in %) for dynamic trailing stop after entry. When positive, the strategy trails the price to protect profits as the move extends.

- **`Break-even stop after +% profit (useBreakEven)`**

Enables automatic move of the stop to the entry price once a certain profit threshold is reached.

- **`Break-even activation (+%) (breakEvenPerc)`**

Profit level (in %) at which the stop is moved to break‑even. Higher values require a larger unrealized profit before break‑even protection kicks in.

#### Visuals

- **`Show labels (showLabels)`**

Toggles on‑chart labels that mark long and short entry signals for easier visual analysis.

- **`Label offset (labelOffset)`**

Horizontal offset (in bars) for placing labels relative to the signal bar. Used only for visual clarity; does not affect trading logic.

---

Если нужно, могу на основе этого текста сразу подготовить компактную версию (ограниченную по символам) специально под поле описания публичного скрипта в TradingView.

EMA Velocity Volatility Clamp (v1)A strategy based on the rate of price change using EMA.

Configured for the 5M Solana.

BINANCE:SOLUSDT

Hash Supertrend [Hash Capital Research]Hash Supertrend Strategy by Hash Capital Research

Overview

Hash Supertrend is a professional-grade trend-following strategy that combines the proven Supertrend indicator with institutional visual design and flexible time filtering.

The strategy uses ATR-based volatility bands to identify trend direction and executes position reversals when the trend flips.This implementation features a distinctive fluorescent color system with customizable glow effects, making trend changes immediately visible while maintaining the clean, professional aesthetic expected in quantitative trading environments.

Entry Signals:

Long Entry: Price crosses above the Supertrend line (trend flips bullish)

Short Entry: Price crosses below the Supertrend line (trend flips bearish)

Controls the lookback period for volatility calculation

Lower values (7-10): More sensitive to price changes, generates more signals

Higher values (12-14): Smoother response, fewer signals but potentially delayed entries

Recommended range: 7-14 depending on market volatility

Factor (Default: 3.0)

Restricts trading to specific hours

Useful for avoiding low-liquidity sessions, overnight gaps, or known choppy periods

When disabled, strategy trades 24/7

Start Hour (Default: 9) & Start Minute (Default: 30)

Define when the trading session begins

Uses exchange timezone in 24-hour format

Example: 9:30 = 9:30 AM

End Hour (Default: 16) & End Minute (Default: 0)

Controls the vibrancy of the fluorescent color system

1-3: Subtle, muted colors

4-6: Balanced, moderate saturation

7-10: Bright, highly saturated fluorescent appearance

Affects both the Supertrend line and trend zones

Glow Effect (Default: On)

Adds luminous halo around the Supertrend line

Creates a multi-layered visual with depth

Particularly effective during strong trends

Glow Intensity (Default: 5.0)

Displays tiny fluorescent dots at entry points

Green dot below bar: Long entry

Red dot above bar: Short entry

Provides clear visual confirmation of executed trades

Show Trend Zone (Default: On)

Strong trending markets (2020-style bull runs, sustained bear markets)

Markets with clear directional bias

Instruments with consistent volatility patterns

Timeframes: 15m to Daily (optimal on 1H-4H)

Challenging Conditions:

Choppy, range-bound markets

Low volatility consolidation periods

Highly news-driven instruments with frequent gaps

Very low timeframes (1m-5m) prone to noise

Recommended AssetsCryptocurrency:

PA Builder [PrimeAutomation]1. PA Builder – Overview

PA Builder is not a fixed strategy; it’s a framework for building strategies. Instead of giving traders one rigid system, it provides a toolbox where entries, exits, filters, risk parameters, and automation rules can all be defined and combined. The core philosophy is confluence: the idea that a trade should only be taken when multiple independent signals agree. The Builder is built around this principle. Every module; trend, reactors, bands, reversals, volume, structure, divergences, externals can be treated as one layer of confidence. The stronger the alignment across layers, the higher the quality of the setup in theory.

In practice, this means PA Builder encourages traders to think in terms of “confluence,” not single indicators. Trend and positioning define whether you should even be looking for longs or shorts. Timing tools such as bands, reversals and candlestick structures determine when inside that broader bias you want to engage. Confirmation tools like volume and flow tell you whether capital is actually supporting the move. Filter systems then ensure that even if everything looks good locally, you still respect higher-timeframe or opposing warnings. The Builder’s philosophy is simple: enter less often, but only when conditions are genuinely in your favour.

2. Core Entry Signal Components

The entry logic in PA Builder is built on a set of signal engines that can be combined in many ways. Trend Signals form a natural foundation. They use low-lag low-pass filters, borrowed from audio signal processing, to extract directional bias from price without the classic delay of classical moving averages. The sensitivity parameter controls how reactive this engine is: lower values favour cleaner trends and fewer whipsaws, while higher values are better suited to short-term intraday trading where speed matters more than smoothness. Many traders start by requiring that Trend Signals show “all bullish” or “all bearish” before allowing any entries in that direction.

Trend signals firing short positions

On top of this directional backbone, the Dynamic Reactor behaves as an adaptive baseline. It accelerates in volatile phases and slows down during consolidation, effectively acting as a moving reference point for both trend and price position. A typical use of this module is to insist that, for long trades, the price sits above a bullish reactor; for shorts, below a bearish one. At the higher-timeframe level, the Quantum Reactor provides a VWAP-style reference that can be anchored to larger candles than the chart you are trading. A common configuration is to trade on a 15-minute chart while requiring that price is above the 4-hour Quantum Reactor for longs or below it for shorts. The “fast” and “slow” options determine how quickly this reference adapts to new information.

Timing is then refined with tools like Quantum Bands, reversals and candle structure analysis. Quantum Bands identify extremes within the current environment. In an uptrend, a tag of the lower band can be treated as a pullback rather than a breakdown; in a downtrend, the upper band acts like a shorting zone. Many traders combine “trend up and above higher-timeframe reactor” with “price temporarily below lower band” to construct a mean-reversion entry inside a larger uptrend. Reversal detection modules examine recent bars to find turning points, with shorter lookbacks capturing fast flips and longer lookbacks tracking deeper structural changes. Candle structure logic goes beyond classical candlestick names and instead focuses on whether price action confirms follow-through or reversion behaviour, with options like “2X” modes that wait for two successive confirmations before acting.

Before and after filtering using reactor applied.

Additional confirmation layers come from Volume Matrix, Money Flow, OSC True7 and divergence detection. Volume and flow tools answer whether actual capital is participating in the move or whether price is drifting on thin activity. OSC True7 categorises the state of the trend into intuitive buckets, strong, healthy, neutral, or exhausted, making it easier to avoid chasing extremes. Divergences between price and momentum can be used either as entry triggers in contrarian systems or as hard filters that block trades when warning signs are present. Finally, two external indicator inputs make it possible to integrate RSI, MACD, custom indicators or even other strategies into the Builder, either as simple thresholds or as comparative logic between two external sources (for example, requiring a fast EMA to be above a slow EMA before allowing longs).

3. Exit System & Trade Management

The exit systems in PA Builder are designed to be as vital as the entry logic. It assumes exits are not an afterthought, but half of the edge. Instead of forcing a single take profit point, the system uses a three-tier structure where you can assign different portions of the position to different targets. A common pattern is to scale out a small portion early (for example at one ATR), another portion at an intermediate level, and keep the largest slice for a deeper move. This creates a natural balance: you book something early to reduce emotional stress, while leaving room to participate in the full potential of a trend.

Targets can be defined using ATR multiples or risk-to-reward ratios that are directly tied to the initial stop distance. Using ATR keeps exits proportional to current volatility. A two ATR target in a quiet environment is very different in absolute price distance from the same multiple in a high-volatility environment, yet conceptually it represents the same “size” move. Risk-to-reward exits build on this by ensuring that if you risk one unit (1R), the reward targets are set at predefined multiples of that risk. This enforces positive expectancy at the structural level: the strategy cannot generate entries with inherently negative payoffs.

Once price begins to move in your favour, trailing logic takes over if you choose to enable it. Trailing can begin immediately from entry or only after a target has been hit. Many users prefer to let TP1 and TP2 behave as fixed profit points and then apply a trailing stop or trailing take profit to the final remainder. That way, routine winners are banked mechanically, while occasional explosive moves can be ridden for as long as the market allows. The breakeven module supports this behaviour by automatically moving stops to entry (or slightly through entry into profit) after a specified condition such as TP1 being hit. This transforms the risk profile mid trade: once breakeven has been secured, remaining size can be managed with much less psychological pressure.

The system also recognises the cost of time. Kill Switch functionality exits trades that have been open too long under mediocre conditions, typically when they are in modest profit but not progressing. This protects you from capital being tied up while better opportunities appear elsewhere. Underlying all of this are several trailing stop mechanisms: percentage-based, tick-based for very short-term strategies, TP linked trailing that activates only once a certain profit threshold has been achieved, and ATR based trailing that automatically scales the trail distance with volatility. Each method serves a slightly different profile of strategy, but all share the same aim: preserve gains and limit downside in a structured way rather than rely on discretionary judgement after the fact.

4. Filters and Risk Management

The filter systems in PA Builder formalise the idea that good trading is often about knowing when not to act. “Do Not Trade” conditions can be configured so that even a perfectly aligned bullish entry stack is overridden if certain bearish evidence is present. These can include higher timeframe reversal structures, powerful opposing divergences, or conflicting signals in key modules. By assigning conditions specifically to “Do Not Long” and “Do Not Short” rather than only to entries, you create asymmetry: buying requires bullish evidence and an absence of strong bearish warnings; selling requires the mirror.

Volatility filters extend this logic to the regime level. Some strategies are inherently suited to low volatility, range bound environments where fading extremes is profitable; others require expansion and energy to function properly. By binding trading permission to volatility ranges, you ensure that a mean-reversion system does not blindly attempt to fade a breakout, and that a momentum system does not spin its wheels in a dead, sideways market. You can even reference volatility from a higher timeframe than the one you trade, so that a five-minute strategy is still aware of the broader one-hour volatility regime it sits inside.

Applied DO NOT TRADE - removes poor signal

Risk management and position sizing are configured so each trade is expressed in units of risk rather than arbitrary size. Leverage, in this framework, is simply a scaling factor for capital efficiency; the actual risk per trade is still controlled by the distance between entry and stop and the percentage of equity you choose to expose. Reinvestment options then decide what proportion of accumulated profit is fed back into position sizing. A more aggressive reinvestment setting accelerates compounding but increases the amplitude of drawdowns; a more conservative one smooths the equity curve at the cost of slower growth. The Base Trade Value parameter ties all of this together by deciding how much nominal capital or how many contracts are committed per trade in light of your maximum allowed simultaneous positions and your intended use of leverage.

External exit conditions provide further flexibility. For example, you might design a system whose entries rely purely on PA Builder’s internal modules, but whose exits use RSI readings, moving average crosses, or a proprietary external indicator. The separation of entry and exit logic allows you to bolt on different behaviours at the tail end of trades while keeping your core signal engine intact. In all cases, the objective is the same: express risk in a controlled, repeatable way that can survive long stretches of unfavourable market conditions.

5. PDT, Cooldowns and Visual Modes

For traders subject to Pattern Day Trading rules, PA Builder includes a day-trade tracking system that counts business days correctly and respects the three-trades-in-five-days limit. This goes beyond simple compliance; it forces discipline. When intraday trading is heavily constrained, you are naturally pushed toward swing-oriented strategies with fewer, more selective entries. The tool visually marks your PDT status so you never inadvertently cross the line and trigger a lockout.

Cooldown systems address another reality: psychological vulnerability after streaks. Following several consecutive wins, many traders unconsciously loosen their standards, take marginal signals, oversize positions, or overtrade. A win-streak cooldown deliberately pauses trading after a configured number of wins, giving you time to reset. The same applies to losing streaks. After a run of losses, the strongest temptation is often to “make it back now,” which is exactly when discipline is weakest. A loss-streak cooldown enforces a break in activity during this high-risk emotional state, helping to prevent cascading damage driven by revenge trading.

Visualisation comes in two main modes. Classic mode emphasises precision: it draws explicit entry lines, stop levels, target levels and fill zones, making it easy to audit risk/reward on each trade, verify that the exit logic behaves as intended, and review historical trades in detail. Modern mode emphasises market feel: instead of focusing on exact levels, it colours candles and backgrounds to reflect momentum, profit state and dynamics.

This helps you see at a glance whether a strategy is operating in a smooth trending environment or a choppy, fragmented one, and whether current trades are broadly working or struggling. Many users develop and debug in Classic mode and then monitor live performance in Modern mode, so both representations become part of the workflow.

6. Strategy Design Workflow, Examples and Cautions

Designing with PA Builder is inherently iterative. You begin with a simple theory and a minimal configuration, perhaps just a trend filter and a basic stop/target structure, and run a backtest. You then examine where the system fails. If you see many losses occurring in counter-trend conditions, you add an additional directional filter or restrict entries with a higher-timeframe reactor condition. If you observe many small whipsaw losses, you might require candle structure confirmation or volume confirmation before allowing an entry. Each change is made one at a time and evaluated. This process gradually builds a layered system where every component has a clear purpose: some reduce drawdown, some increase win rate, some cut out only the worst trades, and others help capture more of the best ones.

A conservative swing strategy might need an agreement between short-term trend signals, a higher-timeframe Quantum position, and a bullish Dynamic Reactor state, while checking that volume supports the move and that no significant bearish reversals or divergences are present on higher timeframes. It might accept relatively few trades, but each trade would be tightly controlled, scaled out over several ATR-based targets and protected with breakeven and trailing logic. On the opposite end, an aggressive scalping configuration would relax some filters, favour faster sensitivities, use short lookback reversals, and tighten stops and targets dramatically, relying on high frequency and careful volatility filtering to maintain edge.

Throughout all of this, overfitting remains the main danger. The more parameters you tune and the more coincidental rules you add to make the backtest equity curve smoother, the more likely it is that you are capturing noise rather than a real, repeatable edge. Signs of overfitting include heavily optimised numeric values with no intuitive justification, large differences between in-sample and out-of-sample results, or strategies that work spectacularly in very specific regimes and collapse elsewhere. To mitigate this, keep strategies as simple as possible, test across different market regimes (bull, bear, range), and accept that robust systems usually look less “perfect” on the historical chart.

Bridging the gap from backtest to live trading is another critical step. Before risking capital, it is wise to paper trade the configuration for a number of trades to confirm that signal frequency, behaviour and execution align with expectations. When going live, starting with minimal size and gradually scaling up based on real-world performance helps manage both financial and psychological risk. If live results diverge significantly from backtest expectations due to slippage, fees, or changing market conditions, you can adjust, reduce size, or temporarily pause rather than commit fully to a failing configuration.

Ultimately, PA Builder is designed to be a tool for building structured, rules-driven trading systems. It gives you the tools to express your ideas, test them, refine them, and run them under controlled risk. It does not remove uncertainty or guarantee results, but it does provide a clear, transparent way to translate trading concepts into executable, testable logic, and to evolve those systems as markets change and your understanding deepens.

smart honey 2.0The smart honey 2.0 is a long-only trading strategy based on averaging entries.

At "Entry" you can set to enter a trade at a specified averaging level. The best backtest result at "only 4th averaging".

"Tp" is take profit.

"Sensitivity" controls the frequency of trades - lower sensitivity means fewer, but higher-quality trades.

Settings recommendations

For 1m-5m timeframes, use low sensitivity and take profit values. For higher timeframes, increase the take profit value.

For example, a profitable setting for many coins on a 5-minute timeframe is

Tp = 1.5%

Sensitivity = 2.7

Entry = only 4th averaging

The strategy features a "Blue line" showing liquidity clusters influenced by Sensitivity. Price often bounces off this line.

You can also set alerts for lists of coins, receiving notifications at each new candle about active positions

Paulinho Signals – Cripto 5m/15m com Filtro de LateralidadeThis script is an automated Pine Script v6 strategy designed for short-term cryptocurrency trading, especially on 5-minute and 15-minute timeframes. It combines moving average crossovers, trend strength (ADX), volatility (ATR), and candlestick patterns to generate buy and sell signals with a fixed risk/reward management system.

How to Use:

- Apply to cryptocurrency charts on 5m or 15m timeframes.

- Adjust parameters to fit your preferences (EMA, RSI, ADX, ATR).

- Use for backtesting or as a decision-support tool.

Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Always test on demo accounts before applying to live trading.

AlosAlgo V2 (BETA)— V2 BETA —

V2 – 2025-11-21 (Update)

• Rebuilt the core signal engine to remove repainting – higher-timeframe Heikin Ashi / Renko now use confirmed bars only for more stable signals & alerts.

• Added Trend Filter MA so longs are only taken above the MA and shorts only below (optional).

• Added MACD momentum filter and Price Action filter (Higher Low for longs, Lower High for shorts) to cut a lot of chop.

• Introduced a loss-streak “circuit breaker” – after X consecutive losing trades the strategy pauses for a set number of bars.

• New TP/SL engine with 2 modes: ATR-based or Fixed % moves, with 4 staged TPs plus an optional runner and break-even SL after TP2.

• Cleaned up TP/SL lines & labels so levels are fixed per trade and easier to read.

• General refactor for more realistic backtests, better live behaviour and easier parameter tuning compared to V1.

ABOUT

AlosAlgo V2 is a multi-timeframe trend + momentum strategy designed for BTC and other high-liquidity markets. It takes directional bias from a higher timeframe, then filters that bias with volatility, momentum and simple price-action structure before it ever opens a trade.

Purely rule-based, no AI / Bayesian / ML.

Core idea

– Use higher-timeframe structure for direction.

– Only trade when trend, momentum and basic price action agree.

– Manage exits with multiple TPs, an optional runner and a hard SL so risk is defined from the start.

Setups

Two main engines:

• Open/Close – Higher-timeframe Heikin Ashi body direction (close vs open) as the core trend signal.

• Renko – ATR-based Renko feed with EMA cross (fast vs slow) as the core trend signal.

Classic sideways filters (ATR + RSI) can be layered on top if you want to only trade in trending or ranging conditions.

Filters added in V2

• Trend Filter MA – Longs only above the MA, shorts only below (length configurable).

• Momentum Filter – Optional MACD filter; only takes longs when MACD is bullish and shorts when MACD is bearish.

• Price Action Filter – Optional HL/LH logic using pivots: longs after a Higher Low, shorts after a Lower High.

• Loss-Streak Circuit Breaker – After N losing trades in a row, the strategy pauses entries for a set number of bars to avoid bad regimes / tilt.

Risk & exits

Two TP/SL modes:

• ATR mode – SL and TP1–TP4 based on ATR at entry (stopFactor / profitFactor).

• Fixed % mode – SL and TP1–TP4 defined as % moves from entry.

On entry the strategy:

• Opens a single position.

• Places 4 staged TPs (TP1–TP4) with user-defined % sizing.

• Optionally leaves a “runner” managed only by SL and trend changes.

• Can move SL to break-even automatically after TP2 (toggle).

All TP/SL levels are locked at entry and drawn on the chart with labels so you can see exactly what the trade is trying to do.

Non-repainting behaviour

V2 is refactored to avoid the repainting behaviour that V1 used. Higher-timeframe and Renko data are taken from confirmed bars only, and entries are based on state (e.g. > / <) instead of repaint-prone crosses. Backtests are much closer to what you’ll see live, and alerts line up with executed trades more reliably.

How to use (suggested defaults)

• Setup: Open/Close

• TPSType: Fixed %

• Trend Filter: ON

• Momentum Filter: ON

• Price Action Filter: ON

• Sideways Filter: No Filtering

Then tweak TP/SL distances and filters per asset + timeframe, and forward-test before sizing up.

Disclaimer

This is not financial advice, not a guarantee of profit and not a “set and forget” money printer. Always forward-test, paper trade and tune risk before using real capital or automation. Markets change – this is a tool, not a promise.

YCGH Mean Reversion StrategyThis strategy applies a classic mean-reversion framework inspired by the concepts popularized by Ernest P. Chan in his quantitative trading books.

It uses Bollinger Bands and RSI to identify statistically stretched conditions where price has moved too far from its average. When price dips below the lower band with weakening momentum, the strategy accumulates small long positions, expecting reversion toward the mean. As price rebounds above the upper band, it exits positions gradually. Position sizing limits help control risk and avoid excessive exposure.

Special thanks to Ernest P. Chan for his influential work in quantitative trading, which motivated the structure and logic behind this model.

Crypto EditionThis strategy is built on a trend-following approach, designed to capture sustained market momentum rather than predict reversals.its a pullback strategy. The goal is to stay aligned with the prevailing trend, ride strong moves, avoid ranging-market noise

SMC Trend Filter Strategy (EMA50/EMA200 + FVG)Overview

This strategy implements a multi-timeframe Smart Money Concept (SMC) trading system designed for intraday and swing trading.

It combines a Daily trend filter, Break of Structure (BOS) detection, Order Block (OB) zones, Fair Value Gap (FVG) confirmation, and an ATR-based trailing stop system to achieve structured and rule-based entries.

The strategy is fully automated for backtesting and allows users to evaluate SMC concepts without repainting or discretionary interpretation.

- Core Components

1. Higher-Timeframe Trend Filter (Daily EMA50/EMA200)

The strategy retrieves D1 data and determines market direction using EMA50 and EMA200:

Uptrend → EMA50 > EMA200

Downtrend → EMA50 < EMA200

Trades are only taken in the direction of the Daily trend to avoid counter-trend setups.

2. Market Structure & Break of Structure (BOS)

The strategy identifies swing highs/lows and detects when price breaks beyond them:

Bullish BOS: price closes above previous swing high

Bearish BOS: price closes below previous swing low

This forms the foundation of SMC market structure recognition.

3. Order Block Zone (OB)

Upon detecting a BOS, the strategy marks the previous candle as a potential Order Block:

For bullish BOS → OB = previous candle’s high/low

For bearish BOS → OB = previous candle’s high/low

The OB zone is visualized using a semi-transparent box extended forward

Infinity 26📈 Infinity 26 – Long-Term Investment Signal Indicator

Infinity 26 is a long-term trend-based investment indicator designed to identify high-quality buy and exit points using weekly or monthly candles.

It filters out market noise and focuses only on strong, long-term momentum shifts—making it ideal for wealth creation and slow, steady portfolio growth.

🔹 Key Features

Buy Signals: Automatically highlights strong trend-reversal points where long-term investors can accumulate.

Exit Signals: Shows when the long-term trend weakens, helping protect gains and reduce major drawdowns.

Weekly & Monthly Optimized: Best results when used on 1-week or 1-month timeframe for long-term investing.

Clear Trend Structure: Helps you stay invested during major bull trends and avoid emotional short-term decisions.

Noise-Free: Designed for long-horizon investors—no overtrading, no frequent whipsaws.

🔹 Best For

Long-term investors

Swing-to-position traders

Wealth creation strategies

Portfolio-based investing

🔹 How It Helps You

✔ Avoid wrong entries

✔ Capture major uptrend moves

✔ Reduce risk with timely exits

✔ Build wealth with simple, rule-based signals

Aquas TrendIt’s a trend-following crossover system with:

A local fast/slow EMA cross for timing entries

A higher-timeframe EMA filter to only trade in the dominant trend

An ATR-based volatility filter so it only trades when the market is moving

ATR-based stop loss and take profit with fixed RR

It tries to catch swings in the direction of the larger trend and ignore chop.

AlgomaticPro - Trend Sniper (BTC, ETH, SOL) 4H timeframeBest performing coins - BTC, ETH, SOL, ADA, DOGE, AVAX, DOT, NEAR, VET, KAS

Best Performing timeframe - 4H

Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!

R4D1 Algo Standard🚀 R4D1 Algo Standard— Smart Supertrend Trading System

The R4D1 Algo Standard is a next-generation Supertrend-based trading system designed for traders who want a clean, reliable, and highly automated strategy.

Built with premium filters, visual dashboards, and institutional-grade session mapping, this algo gives you the clarity you need to dominate any market.

⚠️ Important: For accurate calculations on Heikin Ashi charts, please make sure real OHLC values are enabled in the script settings.

Otherwise, HA-smoothing may distort price-based indicators.

📌 Note: Netflix Inc. was used only as a reference example for demonstration and visualization purposes.

The strategy is Tickerly Ready and works seamlessly with any symbol, across all markets and asset classes.

🔥 Key Features

📈 Supertrend Engine

Ultra-responsive trend detection

Clean reversal entries (Long 📈 / Short 📉)

Automatic trade reversals for maximum momentum capture

🎛️ Customizable Filters

ADX Filter 📡 — Detect true trend strength

MACD Filter 📊 — Block trades during weak or conflicting market phases

Toggle instantly on/off for full control

This time, less is more. Great for Python Code,finding the Right values to be one step ahead.

🧭 Interactive Dashboard (HUD)

A real-time on-chart control center showing:

Current Position: LONG / SHORT

Entry Price

Live P&L 💰

Trend State (Bullish 🟢 / Bearish 🔴)

ADX Strength

MACD Momentum

ATR Volatility

Everything updates automatically on the latest bar.

🇺🇸 US Market Sessions (Optional)

Highlight key Wall Street phases with a single click:

🟩 US Open (09:30–11:30)

🟨 Lunch Session

🟧 Afternoon Session

Perfect for traders who love structure and timing.

🎯 Who Is This Algo For?

✔ Day traders

✔ Swing traders

✔ Supertrend enthusiasts

✔ Traders who want clean charts + intelligent automation

✔ Anyone seeking consistent, rule-based entries & exits

⚡ Why Traders Love It

Zero repainting

Highly intuitive signals

Designed for all markets (Crypto, Forex, Stocks, Indices)

Ultra-fast performance with built-in visual clarity

🛠️ Plug, Play & Trade

Load the script, enable your preferred filters, and let the algo handle the heavy lifting.

You get precision entries, dynamic labels, and a modern dashboard—everything a trader needs to stay ahead.

Scalping FVG Breakout (3R RR, 時間可調)Scalping

1. Taipei Open Time (time adjustable)

2. First 15mK Bar

3. Risk 1:3

4. Stop Loss

STRATEGY 1 │ Red Dragon │ Model 1 │ [Titans_Invest]The Red Dragon Model 1 is a fully automated trading strategy designed to operate BTC/USDT.P on the 4-hour chart with precision, stability, and consistency. It was built to deliver reliable behavior even during strong market movements, maintaining operational discipline and avoiding abrupt variations that could interfere with the trader’s decision-making.

Its core is based on a professionally engineered logical structure that combines trend filters, confirmation criteria, and balanced risk management. Every component was designed to work in an integrated way, eliminating noise, avoiding unnecessary trades, and protecting capital in critical moments. There are no secret mechanisms or hidden logic: everything is built to be objective, clean, and efficient.

Even though it is based on professional quantitative engineering, Red Dragon Model 1 remains extremely simple to operate. All logic is clearly displayed and fully accessible within TradingView itself, making it easy to understand for both beginners and experienced traders. The structure is organized so that any user can quickly view entry conditions, exit criteria, additional filters, adjustable parameters, and the full mechanics behind the strategy’s behavior.

In addition, the architecture was built to minimize unnecessary complexity. Parameters are straightforward, intuitive, and operate in a balanced way without requiring deep adjustments or advanced knowledge. Traders have full freedom to analyze the strategy, understand the logic, and make personal adaptations if desired—always with total transparency inside TradingView.

The strategy was also designed to deliver consistent operational behavior over the long term. Its confirmation criteria reduce impulsive trades; its filters isolate noise; and its overall logic prioritizes high-quality entries in structured market movements. The goal is to provide a stable, clear, and repeatable flow—essential characteristics for any medium-term quantitative approach.

Combining clarity, professional structure, and ease of use, Red Dragon Model 1 offers a solid foundation both for users who want a ready-to-use automated strategy and for those looking to study quantitative models in greater depth.

This entire project was built with extreme dedication, backed by more than 14,000 hours of hands-on experience in Pine Script, continuously refining patterns, techniques, and structures until reaching its current level of maturity. Every line of code reflects this long process of improvement, resulting in a strategy that unites professional engineering, transparency, accessibility, and reliable execution.

🔶 MAIN FEATURES

• Fully automated and robust: Operates without manual intervention, ideal for traders seeking consistency and stability. It delivers reliable performance even in volatile markets thanks to the solid quantitative engineering behind the system.

• Multiple layers of confirmation: Combines 10 key technical indicators with 15 adaptive filters to avoid false signals. It only triggers entries when all trend, market strength, and contextual criteria align.

• Configurable and adaptable filters: Each of the 15 filters can be enabled, disabled, or adjusted by the user, allowing the creation of personalized statistical models for different assets and timeframes. This flexibility gives full freedom to optimize the strategy according to individual preferences.

• Clear and accessible logic: All entry and exit conditions are explicitly shown within the TradingView parameters. The strategy has no hidden components—any user can quickly analyze and understand each part of the system.

• Integrated exclusive tools: Includes complete backtest tables (desktop and mobile versions) with annualized statistics, along with real-time entry conditions displayed directly on the chart. These tools help monitor the strategy across devices and track performance and risk metrics.

• No repaint: All signals are static and do not change after being plotted. This ensures the trader can trust every entry shown without worrying about indicators rewriting past values.

🔷 ENTRY CONDITIONS & RISK MANAGEMENT

Red Dragon Model 1 triggers buy (long) or sell (short) signals only when all configured conditions are satisfied. For example:

• Volume:

• The system only trades when current volume exceeds the volume moving average multiplied by a user-defined factor, indicating meaningful market participation.

• RSI:

• Confirms bullish bias when RSI crosses above its moving average, and bearish bias when crossing below.

• ADX:

• Enters long when +DI is above –DI with ADX above a defined threshold, indicating directional strength to the upside (and the opposite conditions for shorts).

• Other indicators (MACD, SAR, Ichimoku, Support/Resistance, etc.)

Each one must confirm the expected direction before a final signal is allowed.

When all bullish criteria are met simultaneously, the system enters Long; when all criteria indicate a bearish environment, the system enters Short.

In addition, the strategy uses fixed Take Profit and Stop Loss targets for risk control:

Currently: TP around 1.5% and SL around 2.0% per trade, ensuring consistent and transparent risk management on every position.

⚙️ INDICATORS

__________________________________________________________

1) 🔊 Volume: Avoids trading on flat charts.

2) 🍟 MACD: Tracks momentum through moving averages.

3) 🧲 RSI: Indicates overbought or oversold conditions.

4) 🅰️ ADX: Measures trend strength and potential entry points.

5) 🥊 SAR: Identifies changes in price direction.

6) ☁️ Cloud: Accurately detects changes in market trends.

7) 🌡️ R/F: Improves trend visualization and helps avoid pitfalls.

8) 📐 S/R: Fixed support and resistance levels.

9)╭╯MA: Moving Averages.

10) 🔮 LR: Forecasting using Linear Regression.

__________________________________________________________

🟢 ENTRY CONDITIONS 🔴

__________________________________________________________

IF all conditions are 🟢 = 📈 Long

IF all conditions are 🔴 = 📉 Short

__________________________________________________________

🚨 CURRENT TRIGGER SIGNAL 🚨

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🟢 ALL ENTRY CONDITIONS AVAILABLE 🔴

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult) and (close) > (open)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult) and (close) < (open)

🍟 MACD

🟢 LONG = (MACD) > (Signal Smoothing)

🔴 SHORT = (MACD) < (Signal Smoothing)

🧲 RSI

🟢 LONG = (RSI) < (Upper)

🔴 SHORT = (RSI) > (Lower)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🅰️ ADX

🟢 LONG = (+DI) > (-DI) and (ADX) > (Treshold)

🔴 SHORT = (+DI) < (-DI) and (ADX) > (Treshold)

🥊 SAR

🟢 LONG = (close) > (SAR)

🔴 SHORT = (close) < (SAR)

☁️ Cloud

🟢 LONG = (Cloud A) > (Cloud B)

🔴 SHORT = (Cloud A) < (Cloud B)

☁️ Cloud

🟢 LONG = (Kama) > (Kama )

🔴 SHORT = (Kama) < (Kama )

🌡️ R/F

🟢 LONG = (high) > (UP Range) and (upward) > (0)

🔴 SHORT = (low) < (DOWN Range) and (downward) > (0)

🌡️ R/F

🟢 LONG = (high) > (UP Range)

🔴 SHORT = (low) < (DOWN Range)

📐 S/R

🟢 LONG = (close) > (Resistance)

🔴 SHORT = (close) < (Support)

╭╯MA2️⃣

🟢 LONG = (Cyan Bar MA2️⃣)

🔴 SHORT = (Red Bar MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (close) > (MA2️⃣)

🔴 SHORT = (close) < (MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (Positive MA2️⃣)

🔴 SHORT = (Negative MA2️⃣)

__________________________________________________________

🎯 TP / SL 🛑

__________________________________________________________

🎯 TP: 1.5 %

🛑 SL: 2.0 %

__________________________________________________________

🪄 UNIQUE FEATURES OF THIS STRATEGY

____________________________________

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

_____________________________

𝄜 BACKTEST / PERFORMANCE 𝄜

_____________________________

• Net Profit: +634.47%, Maximum Drawdown: -18.44%.

🪙 PAIR / TIMEFRAME ⏳

🪙 PAIR: BINANCE:BTCUSDT.P

⏳ TIME: 4 hours (240m)

✅ ON ☑️ OFF

✅ LONG

✅ SHORT

🎯 TP / SL 🛑

🎯 TP: 1.5 (%)

🛑 SL: 2.0 (%)

⚙️ CAPITAL MANAGEMENT

💸 Initial Capital: 10000 $ (TradingView)

💲 Order Size: 10 % (Of Equity)

🚀 Leverage: 10 x (Exchange)

💩 Commission: 0.03 % (Exchange)

📆 BACKTEST

🗓️ Start: Setember 24, 2019

🗓️ End: November 21, 2025

🗓️ Days: 2250

🗓️ Yers: 6.17

🗓️ Bars: 13502

📊 PERFORMANCE

💲 Net Profit: + 63446.89 $

🟢 Net Profit: + 634.47 %

💲 DrawDown Maximum: - 10727.48 $

🔴 DrawDown Maximum: - 18.44 %

🟢 Total Closed Trades: 1042

🟡 Percent Profitable: 63.92 %

🟡 Profit Factor: 1.247

💲 Avg Trade: + 60.89 $

⏱️ Avg # Bars in Trades

🕯️ Avg # Bars: 4

⏳ Avg # Hrs: 15

✔️ Trades Winning: 666

❌ Trades Losing: 376

✔️ Maximum Consecutive Wins: 11

❌ Maximum Consecutive Losses: 7

📺 Live Performance : br.tradingview.com

• Use this strategy on the recommended pair and timeframe above to replicate the tested results.

• Feel free to experiment and explore other settings, assets, and timeframes.

MTF Scalper - alemicihanMulti-Timeframe Scalper Strategy: Aligning the Big Picture for Quick Gains

This article presents a robust futures trading strategy designed for high-frequency scalping in the crypto market. It’s built on the principle of minimizing risk by ensuring that short-term entries are always aligned with the dominant, higher-timeframe trend.

The Core Concept: Alignment is Key

A Balanced Trend Follower approach, now refined for rapid scalping, uses a Multi-Timeframe (MTF) confirmation system to filter out market noise and increase the probability of a successful trade.

The strategy operates on a Low Timeframe (LTF) chart (e.g., 3m, 5m, or 15m) but only executes trades if the direction is validated by three Higher Timeframes (HTF).

ComponentPurposeFunctionHTF (D, 4h, 1h) EMA => Trend Confirmation =>Checks if the current price is above/below all three Exponential Moving Averages (EMA 20). This provides a strong directional bias.

LTF (5m) Stochastic RSI => Momentum Entry => Generates the actual buy/sell signal by spotting a swift crossover, indicating fresh momentum in the direction of the confirmed HTF trend.

How The Signal Is Generated

Trend Alignment: The system first confirms the trend. If the price is trading above the Daily, 4-Hour, and 1-Hour EMAs, the market is deemed to be in a Strong LONG Trend. Only LONG signals are permitted.

Momentum Trigger: Once the trend is confirmed, a Long Signal is generated only when the Stochastic K-Line crosses above the D-Line, indicating a momentum shift (a pullback ending) towards the main trend direction.

Short Signal: The inverse logic applies to the Short Trend confirmation and entry signal.

Mandatory Risk Management: ATR-Based Exit

Given the high leverage nature of futures and scalping, static Stop-Loss (SL) and Take-Profit (TP) levels are inefficient. This strategy uses the Average True Range (ATR) indicator to dynamically set profit and loss targets based on current market volatility.

Stop Loss (SL): Set dynamically at 1.5 x ATR below (for long) or above (for short) the entry price. This gives the trade enough room to breathe without risking excessive capital.

Take Profit (TP): Set dynamically at 3.0 x ATR, establishing a robust Risk-to-Reward Ratio of 1:2.

Final Thoughts on Testing

This sophisticated approach combines the reliability of MTF analysis with the speed of momentum indicators. However, data analysis is key. Backtesting these parameters (EMA, ATR Multipliers, RSI/Stochastic lengths) on your chosen asset (like BTC/USDT or ETH/USDT) and timeframe is crucial to achieving optimal performance.