Osciladores

Ichimoku Cloud Strategy - 1H HyperliquidStategy for Hyperliquid 1hr time frame using Ichimoku's Cloud.

Best RSI (SIIT) By Nagaraj HiremathBest RSI (SIIT) By Nagaraj Hiremath is based on RSI shows when to By and sell .

Tether Dynamics - Statistical Exhaustion EngineOverview

This strategy detects statistical exhaustion in price movement by modeling price as a particle tethered to a dynamic anchor. When price stretches too far from equilibrium and multiple independent statistical detectors confirm anomalous behavior, the strategy identifies high-probability mean-reversion opportunities.

Unlike simple oversold/overbought indicators, this system fuses concepts from classical mechanics , stochastic filtering , multivariate statistics , and statistical process control into a unified detection framework.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THEORETICAL FOUNDATION

1. The Tethered Particle Model

The framework draws inspiration from Polyak's heavy ball method in optimization theory, where a particle with momentum navigates a loss landscape. Here, price is modeled as a particle connected to a moving anchor (adaptive EMA) by an elastic "chain" whose length scales with volatility (ATR). This creates a natural physics framework:

Displacement (x) : Distance from anchor, normalized by chain length

Velocity (v) : Rate of change of displacement

Acceleration (a) : Rate of change of velocity

This state vector defines the system's "phase space" — a complete description of price dynamics relative to equilibrium.

2. Adaptive Anchor (Kaufman Efficiency)

The anchor uses an adaptive smoothing approach inspired by Perry Kaufman's Adaptive Moving Average. The Efficiency Ratio measures trend strength:

ER = |Direction| / Volatility = |Price - Price | / Σ|ΔPrice|

High efficiency (trending) → faster adaptation

Low efficiency (choppy) → slower, more stable anchor

This prevents whipsaws in ranging markets while staying responsive in trends.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DETECTION ARCHITECTURE

The strategy employs three independent statistical detectors , each grounded in distinct mathematical frameworks. A signal fires when price shows extended tension AND any detector confirms anomalous behavior AND momentum is decelerating (exhaustion).

Detector 1: Mahalanobis Distance (Multivariate Outlier Detection)

The Mahalanobis distance measures how "unusual" the current state vector is, accounting for correlations between displacement, velocity, and acceleration:

D² = (x - μ)ᵀ Σ⁻¹ (x - μ)

Where Σ is the full 3×3 covariance matrix. Under multivariate normality, D² follows a chi-squared distribution with 3 degrees of freedom:

χ²(3, 0.90) = 6.25 → 10% of observations exceed this

χ²(3, 0.95) = 7.81 → 5% of observations exceed this

This detector identifies states that are jointly extreme — even if no single variable looks unusual alone.

Why it matters: A price might have moderate displacement and moderate velocity, but the combination could be highly improbable. Mahalanobis captures this multivariate structure that univariate indicators miss.

Detector 2: CUSUM Change-Point Detection

Cumulative Sum (CUSUM) is a sequential analysis technique from statistical process control. It accumulates standardized deviations from the mean:

S⁺ₜ = max(0, S⁺ₜ₋₁ + zₜ - drift)

S⁻ₜ = min(0, S⁻ₜ₋₁ + zₜ + drift)

When either cumulative sum breaches a threshold, a "change point" is detected — the process has shifted from its baseline regime.

Why it matters: CUSUM detects subtle, persistent shifts that might not trigger on any single bar. It's sensitive to regime changes that precede reversals.

Detector 3: Kalman Innovation Filter (Ornstein-Uhlenbeck Model)

This detector models displacement as an Ornstein-Uhlenbeck process — the continuous-time analog of AR(1) mean-reversion:

dx = θ(μ - x)dt + σdW

A Kalman filter tracks the expected displacement and computes the innovation (prediction error):

νₜ = (yₜ - x̂ₜ|ₜ₋₁) / √Sₜ

Under correct model specification, normalized innovations should be ~N(0,1). Large innovations indicate the mean-reversion model is breaking down — price is behaving "unexpectedly" relative to equilibrium dynamics.

Adaptive Q Estimation: The filter continuously adjusts its process noise estimate based on innovation autocorrelation, maintaining calibration across different volatility regimes.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SIGNAL LOGIC

Long Signal Requirements:

Z-Displacement < -σ threshold (price stretched below anchor)

ANY detector fires (Mahalanobis outlier OR CUSUM change OR Kalman innovation < -2σ)

Z-Acceleration > 0 (downward momentum decelerating)

Short Signal Requirements:

Z-Displacement > +σ threshold (price stretched above anchor)

ANY detector fires

Z-Acceleration < 0 (upward momentum decelerating)

The deceleration requirement ensures we're catching exhaustion rather than fighting momentum.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

RISK MANAGEMENT

Scale-Out Exit Strategy

Rather than all-or-nothing exits, the strategy takes profits at multiple R-levels:

Scale 1: 20% at 0.5R

Scale 2: 20% at 1.0R

Scale 3: 10% at 1.5R (optional)

Remainder: Trailing stop

This locks in gains while allowing winners to run.

Adaptive Trailing Stop

After reaching the activation threshold (default 1R), the stop trails from the highest high (longs) or lowest low (shorts) at a configurable ATR multiple.

Reversal Logic

When an opposite signal fires while in position, the strategy can close and flip direction rather than waiting for a stop-out.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

PARAMETER GUIDANCE

Anchor Period (24) : Base period for adaptive anchor

ATR Period (14) : Volatility measurement

Chain Length Mult (2.5) : Tether elasticity — higher = more stretch allowed

Long Tension σ (1.5) : Lower = more signals

Short Tension σ (2.0) : Higher threshold for shorts (trend asymmetry)

Mahalanobis Threshold (6.25) : χ²(3, 0.90) — adjust for signal frequency

CUSUM Threshold (3.0) : Lower = more sensitive to regime shifts

Lookback Window (100) : Statistical estimation window

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BACKTEST NOTES

Historical testing on NQ (2020-2025) suggests:

Long signals show stronger edge than shorts in equity indices

1H and 30-min timeframes balance signal quality vs. frequency

"Long Only" mode recommended for equity index futures

Important: Past performance does not guarantee future results. This strategy involves significant risk of loss.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

MATHEMATICAL REFERENCES

Polyak, B.T. (1964). "Some methods of speeding up the convergence of iteration methods" (Heavy ball method)

Bertsekas, D.P. (1999). "Nonlinear Programming" (Heavy ball method / momentum dynamics)

Mahalanobis, P.C. (1936). "On the generalized distance in statistics"

Page, E.S. (1954). "Continuous inspection schemes" (CUSUM)

Kalman, R.E. (1960). "A new approach to linear filtering and prediction problems"

Uhlenbeck, G.E. & Ornstein, L.S. (1930). "On the theory of Brownian motion"

Kaufman, P. (1995). "Smarter Trading" (Adaptive Moving Average)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DISCLAIMER

This strategy is provided for educational and research purposes. Trading futures involves substantial risk of loss. The statistical methods employed do not guarantee profitable outcomes. Always use appropriate position sizing and risk management.

Monthly DI+ & RSI StrategyOverview This strategy is designed to capture significant trend reversals and continuations on the Monthly timeframe. It combines the trend-following capability of the Directional Movement Index (DMI) with the fast momentum detection of RSI (Period 6).

Core Logic The strategy triggers a long position based on a dual-confirmation system. It looks for a specific "handshake" between Trend (DI) and Momentum (RSI).

Entry Conditions (OR Logic) A Buy signal is generated if EITHER of the following occurs:

Trend Trigger: DI+ crosses over DI- (while RSI is already bullish, trading above its SMA).

Momentum Trigger: RSI(6) crosses over RSI SMA(14) (while the trend is already bullish, with DI+ > DI-).

Exit Condition (Stop Loss)

Trend Reversal: The position is closed immediately if DI- crosses over DI+, indicating the bullish trend has been invalidated.

Default Settings

Timeframe: Optimized for 1M (Monthly) charts.

RSI: Length 6

RSI SMA: Length 14

DMI: Length 14 / Smoothing 14

Risk Warning This script is for educational purposes only. Past performance does not guarantee future results. Always backtest on your specific asset classes before trading.

Velocity SwingtraderThe intended objective of this indicator to gauge trend and momentum and find trades that are at the beginning of a trend change for longer periods of time (days, weeks, months).

Range Strategy (kasatura84)Winning Range Strategy (Set Heikin Ashi Candles)

Incredible winning strategy. You have to set Heikin Ashi Candles to activate strategy! It works both long and short trades.

SVTR [Ultimate]SVTR v1.0 is a fully automated trading strategy designed to identify high-probability market opportunities using structured momentum, trend validation, and risk-controlled execution logic.

This strategy is not a simple signal generator.

It is a complete decision engine that evaluates market conditions, confirms entries with multiple filters, and manages trades automatically according to predefined logic.

Built for traders who want consistency, discipline, and objective execution, SVTR removes emotional bias and delivers rule-based trading across different market environments.

KEY FEATURES

• Fully automated entry and exit logic

• Multi-layer confirmation system

• Momentum and trend validation

• Smart trade filtering to reduce noise

• Works on multiple markets and timeframes

• Non-repainting logic

• Alert-ready for automation and integrations

AUTOMATED STRATEGY LOGIC

SVTR continuously analyzes the market and only executes trades when all required conditions align.

This prevents overtrading and avoids weak or low-quality setups.

The strategy is designed to:

Enter when momentum and direction are confirmed

Avoid choppy and uncertain market phases

Exit trades based on objective, rule-driven logic

Maintain consistency regardless of emotions or bias

WHY THIS STRATEGY?

Most traders fail not because of bad ideas, but because of:

Late entries

Emotional decisions

Overtrading

Lack of discipline

SVTR v1.0 solves these problems by automating the decision process and executing trades exactly as designed, every time.

You trade the system.

Not your emotions.

WHO IS IT FOR?

• Traders looking for automated execution

• System-based and rule-driven traders

• Swing traders and intraday traders

• Traders who want consistency over discretion

• Users who want a ready-to-use strategy framework

IMPORTANT NOTES

• Invite-Only / Private access

• Source code is protected

• Designed for backtesting, automation, and live monitoring

• Strategy behavior may vary depending on market conditions and settings

VERSION

v1.0 – Initial Private Release

Future updates may include optimizations, additional filters, and performance improvements.

FINAL STATEMENT

SVTR v1.0 is built for traders who value structure, confirmation, and automation over guesswork.

If you are looking for a strategy that executes with discipline, filters weak setups, and operates as a complete automated system, this strategy is designed for you.

Strategy with VWRSI and SAVE orders Long or Short or BothVWRSI is very powerful indicator coded by Algo Alpha and I Make Strategy of it

But there is no stop loss instate the Strategy is using Save orders to minimize the market manipulation

The best to used is side way market with long and short enable

The Strategy trigger long or short market order -

long - ta.crossover(rsi, 20)

short - ta.crossunder(rsi, 80)

And if is not take profit from the first trade start with the save trades until will do

the sum of the first order - base order and the save order can be adjust from the user

as well the deviation from the first order

IF some user have questions let me know

[SM-021] Gaussian Trend System [Optimized]This script is a comprehensive trend-following strategy centered around a Gaussian Channel. It is designed to capture significant market movements while filtering out noise during consolidation phases. This version (v2) introduces code optimizations using Pine Script v6 Arrays and a new Intraday Time Control feature.

1. Core Methodology & Math

The foundation of this strategy is the Gaussian Filter, originally conceptualized by @DonovanWall.

Gaussian Poles: Unlike standard moving averages (SMA/EMA), this filter uses "poles" (referencing signal processing logic) to reduce lag while maintaining smoothness.

Array Optimization: In this specific iteration, the f_pole function has been refactored to utilize Pine Script Arrays. This improves calculation efficiency and rendering speed compared to recursive variable calls, especially when calculating deep historical data.

Channel Logic: The strategy calculates a "Filtered True Range" to create High and Low bands around the main Gaussian line.

Long Entry: Price closes above the High Band.

Short Entry: Price closes below the Low Band.

2. Signal Filtering (Confluence)

To reduce false signals common in trend-following systems, the strategy employs a "confluence" approach using three additional layers:

Baseline Filter: A 200-period (customizable) EMA or SMA acts as a regime filter. Longs are only taken above the baseline; Shorts only below.

ADX Filter (Volatility): The Average Directional Index (ADX) is used to measure trend strength. If the ADX is below a user-defined threshold (default: 20), the market is considered "choppy," and new entries are blocked.

Momentum Check: A Stochastic RSI check ensures that momentum aligns with the breakout direction.

3. NEW: Intraday Session Filter

Per user requests, a time-based filter has been added to restrict trading activity to specific market sessions (e.g., the New York Open).

How it works: Users can toggle a checkbox to enable/disable the filter.

Configuration: You can define a specific time range (Default: 09:30 - 16:00) and a specific Timezone (Default: New York).

Logic: The strategy longCondition and shortCondition now check if the current bar's timestamp falls within this window. If outside the window, no new entries are generated, though existing trades are managed normally.

4. Risk Management

The strategy relies on volatility-based exits rather than fixed percentage stops:

ATR Stop Loss: A multiple of the Average True Range (ATR) is calculated at the moment of entry to set a dynamic Stop Loss.

ATR Take Profit: An optional Reward-to-Risk (RR) ratio can be set to place a Take Profit target relative to the Stop Loss distance.

Band Exit: If the trend reverses and price crosses the opposite band, the trade is closed immediately to prevent large drawdowns.

Credits & Attribution

Original Gaussian Logic: Developed by @DonovanWalll. This script utilizes his mathematical formula for the pole filters.

Strategy Wrapper & Array Refactor: Developed by @sebamarghella.

Community Request: The Intraday Session Filter was added to assist traders focusing on specific liquidity windows.

Disclaimer: This strategy is for educational purposes. Past performance is not indicative of future results. Please use the settings menu to adjust the Session Time and Risk parameters to fit your specific asset class.

King StrategyKing Strategy is an all-in-one TradingView edge for scalpers, swing traders and prop- or hedge-fund pros alike. It blends classic pattern flags with institutional-grade filters to pinpoint high-probability long entries and exits—and displays them with instant visual cues (buy/sell flags, dynamic backgrounds, trend-lines, support/resistance and volume-zones).

Built-in time-of-day and cycle locks help tame overtrading, and every signal lives in a single Inputs panel so you can toggle filters, tweak risk parameters and dial in exits in seconds. Whether you’re chasing 1-minute scalps or planning multi-day swings, S85 keeps you in sync with the market—just fine-tune its tools to match your timeframe, liquidity and comfort with risk.

StrategyScript77 Is a rule-based strategy built on top of an Ichimoku based engine.

Ichimoku concepts are used as the backbone for trend and momentum filtering, so the strategy tends to stay on the side of the dominant move instead of fighting it.

The name “Super77” comes from the behavior I consistently observed in testing because the win rate tends to hover around the 70–80% range, often clustering around ~77% when used as intended.

It’s not a promise or guarantee, but it reflects the core design philosophy: frequent, relatively small but steady wins, with controlled and manageable losses.

Trading Style – Built for Conservative Traders

Super77 is intentionally designed for traders who prefer a conservative and calm approach:

Entries only at bar close

The strategy waits for bar close confirmation before entering a position. No intrabar guessing, no chasing half-formed signals. If the signal is still valid at close, only then will it enter.

Exits automated on bar close

Exits are also managed on bar close, which makes the logic transparent, easy to review on the chart, and more robust in backtesting compared to tick-based or intrabar hacks.

Semi-auto friendly

If you like to keep some discretion, you can treat it as semi-automatic:

Let the strategy generate entry signals

Manually cancel or skip certain trades if market context changes (news, extreme volatility, etc.)

This combination makes Super77 suitable for traders who don’t want to stare at the screen all day but still want structure and automation.

How to Use

Works best with bar-close execution (avoid trying to simulate intrabar fills if you want consistent behavior).

Designed for conservative, trend-aligned trading, not for hyper-scalping or news gambling.

Can be used as:

Fully automated (let all entries/exits trigger on bar close), or

Semi-automated (use alerts/signals but manually cancel some entries).

Step-by-Step: Automation with Cornix (Webhook Setup)

You can automate Super77 using Cornix by connecting TradingView alerts to your Cornix group via webhook.

Note: Exact button names may differ slightly depending on Cornix / TradingView updates, but the flow is always the same:

Cornix group → get webhook URL & mapping → TradingView alerts → signals sent to Cornix.

(Optional) Map specific pairs / directions

If you use UUID / signal mapping per symbol and per side (long/short), set them up in Cornix according to your own template.

Super77 can be used either:

On a single pair (simple setup), or

On multiple pairs if your alert / webhook structure supports that. So you can pick many pairs with 1 script.

Final Notes & Disclaimer

Super77 is an educational and experimental trading tool, not financial advice.

Past performance in back tests does not guarantee future results.

Always:

Test on demo or paper first

Adjust risk to match your own profile

Accept that losses and drawdowns are a natural part of any strategy

If you’re looking for a strategy that reflects a conservative, confirmation-based trading style with a focus on steady win rate and smoother equity behavior, Super77 was built exactly with that mindset in mind.

Disoxis Capital Club📊 Strategy B✅This indicator has been exclusively developed for Disoxis Capital Club members, combining advanced volume-weighted analytics with institutional trading concepts.

The indicator automatically resets at the start of each trading session and uses volume-weighted statistical calculations to ensure accuracy that aligns with professional trading platforms. All visual elements, including customizable color schemes and line styles, have been optimized for clarity and real-time decision-making. Designed specifically for active intraday traders within the Disoxis Capital Club community, this indicator incorporates time-based filtering capabilities and session-specific analytics to help identify high-probability trading opportunities.

The tool displays key institutional levels through clean visual representation, making it easier to recognize market behavior around volume-weighted price zones. Whether you're analyzing futures, forex, or equity markets, this indicator provides the technical foundation needed to align your trading with smart money movements and institutional order flow patterns.

Trend Vector Pro v2.0Trend Vector Pro v2.0

👨💻 Developed by: Mohammed Bedaiwi

💡 Strategy Overview & Coherence

Trend Vector Pro (TVPro) is a momentum-based trend & reversal strategy that uses a custom smoothed oscillator, an optional ADX filter, and classic Pivot Points to create a single, coherent trading framework.

Instead of stacking random indicators, TVPro is built around these integrated components:

A custom momentum engine (signal generation)

An optional ADX filter (trend quality control)

Daily Pivot Points (context, targets & S/R)

Swing-based “Golden Bar” trailing stops (trade management)

Optional extended bar detection (overextension alerts)

All parts are designed to work together and are documented below to address originality & usefulness requirements.

🔍 Core Components & Justification

1. Custom Momentum Engine (Main Signal Source)

TVPro’s engine is a custom oscillator derived from the bar midpoint ( hl2 ), similar in spirit to the Awesome Oscillator but adapted and fully integrated into the strategy. It measures velocity and acceleration of price, letting the script distinguish between strong impulses, weakening trends, and pure noise.

2. ADX Filter (Trend Strength Validation – Optional)

Uses Average Directional Index (ADX) as a gatekeeper.

Why this matters: This prevents the strategy from firing signals in choppy, non-trending environments (when ADX is below the threshold) and keeps trades focused on periods of clear directional strength.

3. Classic Pivot Points (Context & Targets)

Calculates Daily Pivot Points ( PP, R1-R3, S1-S3 ) via request.security() using prior session data.

Why this matters: Momentum gives the signal, ADX validates the environment, and Pivots add external structure for risk and target planning. This is a designed interaction, not a random mashup.

🧭 Trend State Logic (5-State Bar Coloring)

The strategy uses the momentum's value + slope to define five states, turning the chart into a visual momentum map:

🟢 STRONG BULL (Bright Green): Momentum accelerating UP. → Strong upside impulse.

🌲 WEAK BULL (Dark Green): Momentum decelerating DOWN (while positive). → Pullback/pause zone.

🔴 STRONG BEAR (Bright Red): Momentum accelerating DOWN. → Strong downside impulse.

🍷 WEAK BEAR (Dark Red): Momentum decelerating UP (while negative). → Rally/short-covering zone.

🔵 NEUTRAL / CHOP (Cyan): Momentum is near zero (based on noise threshold). → Consolidation / low volatility.

🎯 Signal Logic Modes

TVPro provides two selectable entry styles, controlled by input:

Reversals Only (Cleaner Mode – Default): Targets trend flips. Entry triggers when the current state is Bullish (or Bearish) and the previous state was not. This reduces noise and over-trading.

All Strong Pulses (Aggressive Mode): Targets acceleration phases. Entry triggers when the bar turns to STRONG BULL or STRONG BEAR after any other state. This mode produces more trades.

📌 Risk Management Tools

🟡 Golden Bars – Trailing Stops: Yellow “Trail” Arrows mark confirmed Swing Highs/Lows. These are used as logical trailing stop levels based on market structure.

Extended Bars: Detects when price closes outside a 2-standard-deviation channel, flagging overextension where a pullback is more likely.

Pivot Points: Used as external targets for Take Profit and structural stop placement.

⚙️ Strategy Defaults (Crucial for Publication Compliance)

To keep backtest results realistic and in line with House Rules, TVPro is published with the following fixed default settings:

Order Size: 5% of equity per trade ( default_qty_value = 5 )

Commission: 0.04% per order ( commission_value = 0.04 )

Slippage: 2 ticks ( slippage = 2 )

Initial Capital: 10,000

📘 How to Trade with Trend Vector Pro

Entry: Take Long when a Long signal appears and confirm the bar is Green (Bull state). Short for Red (Bear state).

Stop Loss: Place the initial SL near the latest swing High/Low, or near a relevant Pivot level.

Trade Management: Follow Golden (Trail) Arrows to trail your stop behind structure.

Exits: Exit when: the trailing stop is hit, Price reaches a major Pivot level, or an opposite signal prints.

🛑 Disclaimer

This script is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always forward-test and use proper risk management before applying any strategy to live trading.

Gyspy Bot Trade Engine - V1.2B - Strategy 12-7-25 - SignalLynxGypsy Bot Trade Engine (MK6 V1.2B) - Ultimate Strategy & Backtest

Brought to you by Signal Lynx | Automation for the Night-Shift Nation 🌙

1. Executive Summary & Architecture

Gypsy Bot (MK6 V1.2B) is not merely a strategy; it is a massive, modular Trade Engine built specifically for the TradingView Pine Script environment. While most strategies rely on a single dominant indicator (like an RSI cross or a MACD flip) to generate signals, Gypsy Bot functions as a sophisticated Consensus Algorithm.

The engine calculates data from up to 12 distinct Technical Analysis Modules simultaneously on every bar closing. It aggregates these signals into a "Vote Count" and only executes a trade entry when a user-defined threshold of concurring signals is met. This "Voting System" acts as a noise filter, requiring multiple independent mathematical models—ranging from volume flow and momentum to cyclical harmonics and trend strength—to agree on market direction before capital is committed.

Beyond entries, Gypsy Bot features a proprietary Risk Management suite called the Dump Protection Team (DPT). This logic layer operates independently of the entry modules, specifically scanning for "Moon" (Parabolic) or "Nuke" (Crash) volatility events to force-exit positions, overriding standard stops to preserve capital during Black Swan events.

2. ⚠️ The Philosophy of "Curve Fitting" (Must Read)

One must be careful when applying Gypsy Bot to new pairs or charts.

To be fully transparent: Gypsy Bot is, by definition, a very advanced curve-fitting engine. Because it grants the user granular control over 12 modules, dozens of thresholds, and specific voting requirements, it is extremely easy to "over-fit" the data. You can easily toggle switches until the backtest shows a 100% win rate, only to have the strategy fail immediately in live markets because it was tuned to historical noise rather than market structure.

To use this engine successfully, you must adopt a specific optimization mindset:

Ignore Raw Net Profit: Do not tune for the highest dollar amount. A strategy that makes $1M in the backtest but has a 40% drawdown is useless.

Prioritize Stability: Look for a high Profit Factor (1.5+), a high Percent Profitable, and a smooth equity curve.

Regular Maintenance is Mandatory: Markets shift regimes (e.g., from Bull Trend to Crab Range). Parameters that worked perfectly in 2021 may fail in 2024. Gypsy Bot settings should be reviewed and adjusted at regular intervals (e.g., quarterly) to ensure the voting logic remains aligned with current market volatility.

Timeframe Recommendations:

Gypsy Bot is optimized for High Time Frame (HTF) trend following. It generally produces the most reliable results on charts ranging from 1-Hour to 12-Hours, with the 4-Hour timeframe historically serving as the "sweet spot" for most major cryptocurrency assets.

3. The Voting Mechanism: How Entries Are Generated

The heart of the Gypsy Bot engine is the ActivateOrders input (found in the "Order Signal Modifier" settings).

The engine constantly monitors the output of all enabled Modules.

Long Votes: GoLongCount

Short Votes: GoShortCount

If you have 10 Modules enabled, and you set ActivateOrders to 7:

The engine will ONLY trigger a Buy Entry if 7 or more modules return a valid "Buy" signal on the same closed candle.

If only 6 modules agree, the trade is rejected.

This allows you to mix "Leading" indicators (Oscillators) with "Lagging" indicators (Moving Averages) to create a high-probability entry signal that requires momentum, volume, and trend to all be in alignment.

4. Technical Deep Dive: The 12 Modules

Gypsy Bot allows you to toggle the following modules On/Off individually to suit the asset you are trading.

Module 1: Modified Slope Angle (MSA)

Logic: Calculates the geometric angle of a moving average relative to the timeline.

Function: It filters out "lazy" trends. A trend is only considered valid if the slope exceeds a specific steepness threshold. This helps avoid entering trades during weak drifts that often precede a reversal.

Module 2: Correlation Trend Indicator (CTI)

Logic: Based on John Ehlers' work, this measures how closely the current price action correlates to a straight line (a perfect trend).

Function: It outputs a confidence score (-1 to 1). Gypsy Bot uses this to ensure that we are not just moving up, but moving up with high statistical correlation, reducing fake-outs.

Module 3: Ehlers Roofing Filter

Logic: A sophisticated spectral filter that combines a High-Pass filter (to remove long-term drift) with a Super Smoother (to remove high-frequency noise).

Function: It attempts to isolate the "Roof" of the price action. It is excellent at catching cyclical turning points before standard moving averages react.

Module 4: Forecast Oscillator

Logic: Uses Linear Regression forecasting to predict where price "should" be relative to where it is.

Function: When the Forecast Oscillator crosses its zero line, it indicates that the regression trend has flipped. We offer both "Aggressive" and "Conservative" calculation modes for this module.

Module 5: Chandelier ATR Stop

Logic: A volatility-based trend follower that hangs a "leash" (ATR multiple) from the highest high (for longs) or lowest low (for shorts).

Function: Used here as an entry filter. If price is above the Chandelier line, the trend is Bullish. It also includes a "Bull/Bear Qualifier" check to ensure structural support.

Module 6: Crypto Market Breadth (CMB)

Logic: This is a macro-filter. It pulls data from multiple major tickers (BTC, ETH, and Perpetual Contracts) across different exchanges.

Function: It calculates a "Market Health" percentage. If Bitcoin is rising but the rest of the market is dumping, this module can veto a trade, ensuring you don't buy into a "fake" rally driven by a single asset.

Module 7: Directional Index Convergence (DIC)

Logic: Analyzes the convergence/divergence between Fast and Slow Directional Movement indices.

Function: Identifies when trend strength is expanding. A buy signal is generated only when the positive directional movement overpowers the negative movement with expanding momentum.

Module 8: Market Thrust Indicator (MTI)

Logic: A volume-weighted breadth indicator. It uses Advance/Decline data and Up/Down Volume data.

Function: This is one of the most powerful modules. It confirms that price movement is supported by actual volume flow. We recommend using the "SSMA" (Super Smoother) MA Type for the cleanest signals on the 4H chart.

Module 9: Simple Ichimoku Cloud

Logic: Traditional Japanese trend analysis using the Tenkan-sen and Kijun-sen.

Function: Checks for a "Kumo Breakout." Price must be fully above the Cloud (for longs) or below it (for shorts). This is a classic "trend confirmation" module.

Module 10: Simple Harmonic Oscillator

Logic: Analyzes the harmonic wave properties of price action to detect cyclical tops and bottoms.

Function: Serves as a counter-trend or early-reversal detector. It tries to identify when a cycle has bottomed out (for buys) or topped out (for sells) before the main trend indicators catch up.

Module 11: HSRS Compression / Super AO

Logic: Two options in one.

HSRS: Hirashima Sugita Resistance Support. Detects volatility compression (squeezes) relative to dynamic support/resistance bands.

Super AO: A combination of the Awesome Oscillator and SuperTrend logic.

Function: Great for catching explosive moves that result from periods of low volatility (consolidation).

Module 12: Fisher Transform (MTF)

Logic: Converts price data into a Gaussian normal distribution.

Function: Identifies extreme price deviations. This module uses Multi-Timeframe (MTF) logic to look at higher-timeframe trends (e.g., looking at the Daily Fisher while trading the 4H chart) to ensure you aren't trading against the major trend.

5. Global Inhibitors (The Veto Power)

Even if 12 out of 12 modules vote "Buy," Gypsy Bot performs a final safety check using Global Inhibitors. If any of these are triggered, the trade is blocked.

Bitcoin Halving Logic:

Hardcoded dates for past and projected future Bitcoin halvings (up to 2040).

Trading is inhibited or restricted during the chaotic weeks immediately surrounding a Halving event to avoid volatility crushes.

Miner Capitulation:

Uses Hash Rate Ribbons (Moving averages of Hash Rate).

If miners are capitulating (Shutting down rigs due to unprofitability), the engine flags a "Bearish" regime and can flip logic to Short-only or flat.

ADX Filter (Flat Market Protocol):

If the Average Directional Index (ADX) is below a specific threshold (e.g., 20), the market is deemed "Flat/Choppy." The bot will refuse to open trend-following trades in a flat market.

CryptoCap Trend:

Checks the total Crypto Market Cap chart. If the broad market is in a downtrend, it can inhibit Long entries on individual altcoins.

6. Risk Management & The Dump Protection Team (DPT)

Gypsy Bot separates "Entry Logic" from "Risk Management Logic."

Dump Protection Team (DPT)

This is a specialized logic branch designed to save the account during Black Swan events.

Nuke Protection: If the DPT detects a volatility signature consistent with a flash crash, it overrides all other logic and forces an immediate exit.

Moon Protection: If a parabolic pump is detected that violates statistical probability (Bollinger deviations), DPT can force a profit take before the inevitable correction.

Advanced Adaptive Trailing Stop (AATS)

Unlike a static trailing stop (e.g., "trail by 5%"), AATS is dynamic.

Penthouse Level: If price is at the top of the HSRS channel (High Volatility), the stop loosens to allow for wicks.

Dungeon Level: If price is compressed at the bottom, the stop tightens to protect capital.

Staged Take Profits

TP1: Scalp a portion (e.g., 10%) to cover fees and secure a win.

TP2: Take the bulk of profit.

TP3: Leave a "Runner" position with a loose trailing stop to catch "Moon" moves.

7. Recommended Setup Guide

When applying Gypsy Bot to a new chart, follow this sequence:

Set Timeframe: 4 Hours (4H).

Reset: Turn OFF Trailing Stop, Stop Loss, and Take Profits. (We want to see raw entry performance first).

Tune DPT: Adjust "Dump/Moon Protection" inputs first. These have the highest impact on net performance.

Tune Module 8 (MTI): This module is a heavy filter. Experiment with the MA Type (SSMA is recommended).

Select Modules: Enable/Disable modules 1-12 based on the asset's personality (Trending vs. Ranging).

Voting Threshold: Adjust ActivateOrders. A lower number = More Trades (Aggressive). A higher number = Fewer, higher conviction trades (Conservative).

Final Polish: Re-enable Stop Losses, Trailing Stops, and Staged Take Profits to smooth the equity curve and define your max risk per trade.

8. Technical Specs

Engine Version: Pine Script V6

Repainting: This strategy uses Closed Candle data for all Risk Management and Entry decisions. This ensures that Backtest results align closely with real-time behavior (no repainting of historical signals).

Alerts: This script generates Strategy alerts. If you require visual-only alerts, see the source code header for instructions on switching to "Study" (Indicator) mode.

Disclaimer:

This script is a complex algorithmic tool for market analysis. Past performance is not indicative of future results. Use this tool to assist your own decision-making, not to replace it.

9. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

Profitable Pair Correlation Divergence Scanner v6This strategy identifies divergence opportunities between two correlated assets using a combination of Z-Score spread analysis, trend confirmation, RSI & MACD momentum checks, correlation filters, and ATR-based stop-loss/take-profit management. It’s optimized for positive P&L and realistic trade execution.

Key Features:

Pair Divergence Detection:

Measures deviation between returns of two assets and identifies overbought/oversold spread conditions using Z-Score.

Trend Alignment:

Trades only in the direction of the primary asset’s trend using a fast EMA vs slow EMA filter.

Momentum Confirmation:

Confirms trades with RSI and MACD to reduce false signals.

Correlation Filter:

Ensures the pair is strongly correlated before taking trades, avoiding noisy signals.

Risk Management:

Dynamic ATR-based stop-loss and take-profit ensures proper reward-to-risk ratio.

Exit Conditions:

Automatically closes positions when Z-Score normalizes, or ATR-based exits are hit.

How It Works:

Calculate Returns:

Computes returns for both assets over the selected timeframe.

Z-Score Spread:

Calculates the spread between returns and normalizes it using moving average and standard deviation.

Trend Filter:

Only takes long trades if the fast EMA is above the slow EMA, and short trades if the fast EMA is below the slow EMA.

Momentum Confirmation:

Confirms trade direction with RSI (>50 for longs, <50 for shorts) and MACD alignment.

Correlation Check:

Ensures the pair’s recent correlation is strong enough to validate divergence signals.

Trade Execution:

Opens positions when Z-Score crosses thresholds and all conditions align. Positions close when Z-Score normalizes or ATR-based SL/TP is hit.

Plot Explanation:

Z-Score: Blue line shows divergence magnitude.

Entry Levels: Red/Green lines mark long/short thresholds.

Exit Zone: Gray lines show normalization zone.

EMA Trend Lines: Purple (fast), Orange (slow) for trend alignment.

Correlation: Teal overlay shows current correlation strength.

Usage Tips:

Use highly correlated pairs for best results (e.g., EURUSD/GBPUSD).

Run on higher timeframe charts (1h or 4h) to reduce noise.

Adjust ATR multiplier based on volatility to avoid premature stops.

Combine with alerts for automated notifications or webhook execution.

Conclusion:

The Profitable Pair Correlation Divergence Scanner v6 is designed for traders who want systematic, low-risk, positive P&L trading opportunities with minimal manual monitoring. By combining trend alignment, momentum confirmation, correlation filters, and dynamic exits, it reduces false signals and improves execution reliability.

Run it on TradingView and watch how it captures divergence opportunities while maintaining positive P&L across trades.

Momentum Reversal / Dip Buyer [Score Based]Strategy Overview

Momentum Reversal / Dip Buyer is a quantitative reversal engine designed to fade stretched moves and buy dips / sell rallies when multiple momentum and context factors line up. It’s built for liquid instruments especially for ticker CME_MINI:ES1! and works best on intraday timeframes like the 5-minute or 1-minute chart.

Core Logic

This strategy builds a composite Momentum Score by combining:

Price Location: Relative to 100 SMA, 1000 EMA, and VWAP (trend / regime filter).

RSI: Overbought/oversold and mid-zone strength.

VWMO (Volume-Weighted Momentum): Direction and strength of volume-weighted price drift.

ADX: Trend strength filter (high vs low trend environment).

Full Stoch (%K): Short-term exhaustion and mean-reversion context.

CCI: Overbought/oversold turns (key trigger).

MFI: Volume-confirmed buying/selling pressure.

ATR Regime: High vs low volatility environment.

Cumulative Delta: Whether net aggressor flow is rising or falling.

From this, a single Momentum Score is computed each bar:

Longs: Taken when the score is depressed (scoreLow) and CCI crosses up from oversold.

Shorts: Taken when the score is elevated (scoreHigh) and CCI crosses down from overbought.

Risk Management & Trade Logic

Max Daily Trades: Hard cap on entries per day.

Hard Stop: Fixed % stop based on entry price.

Profit Target: Target ATR Multiplier × main ATR from entry.

Breakeven Logic: Optional; moves stop to breakeven (plus optional offset) after price moves a configurable multiple of the main ATR in your favor.

Trailing Stop (Separate ATR): Optional; uses its own ATR length and ATR-based trigger and distance. This lets you run slower ATR for targets while using a tighter, more reactive ATR for the trail.

Session Control

Trading Window: Optional session filter (e.g., 09:30–16:00). Entries are only allowed inside the defined window.

Force Flat at Session End: Option to automatically close all open positions when the session ends.

Visuals

The script plots entry arrows and a compact dashboard displaying: current Momentum Score, daily trade usage, and CCI status.

Disclaimer:

This script is for educational and research purposes only and is not financial advice. Past performance does not guarantee future results. Always forward-test and adjust parameters to your own risk tolerance and market.

Shoutout and all credit goes to AuclairsCapital for building the base foundation of this strategy on ThinkScript

Bollinger Bands Mean Reversion using RSI [Krishna Peri]How it Works

Long entries trigger when:

- RSI reaches oversold levels, and

- At least one bullish candle closes inside the lower Bollinger Band

Short entries trigger when:

- RSI reaches overbought levels, and

- At least one bearish candle closes inside the upper Bollinger Band

This approach aims to capture exhaustion moves where price pushes into extreme deviation from its mean and then snaps back toward the middle band.

Important Disclaimer

This is a mean-reversion strategy, which means it performs best in sideways, ranging, or slowly oscillating market conditions. When markets shift into strong trends, Bollinger Bands expand and volatility increases, which may cause some signals to become inaccurate or fail altogether.

For best results, combine this script with:

- Price action

- Market structure

- Higher-timeframe trend context

- Previous day/week/month highs & lows

- Untested liquidity levels or imbalance zones

- Session timing (Asia, London, NY)

Using these confluences helps filter out low-probability trades and significantly improves consistency and precision.

Sniper Perfect: Institutional Flow & Adaptive Risk ProtocolOverview Sniper Perfect is an advanced trend-following system designed to filter out "fakeouts" and institutional traps using a multi-layered verification protocol. It combines Volume Flow (VFI), Volatility (CHOP), and Momentum (RSI) to ensure entry only occurs in high-probability setups.

Key Features

🛡️ The Triple Filter Protocol

Strict Choppiness Filter: Uses a strict CHOP threshold (40). If the market is moving sideways, the algorithm locks all new entries to prevent whipsaws.

RSI Extremes Protection: Prevents FOMO buying at tops (Overbought > 70) and panic selling at bottoms (Oversold < 30).

Conflict Zone Detection: Identifies divergence between Price action and Money Flow. If price rises but institutional money exits, the background turns Gray and trading is disabled.

🔒 Adaptive Risk Management

Heat-Breathing Stop Loss: The SL distance adjusts dynamically based on market Volume and Volatility ("Heat").

Ratchet Mechanism: A mechanical lock ensures the Stop Loss can ONLY move in the direction of profit. It never loosens, guaranteeing that paper profits are protected.

📊 Live Dashboard A real-time panel in the bottom-right corner displays:

VFI Flow: Positive/Negative money flow.

Market Status: Active vs. Locked (Choppy).

RSI Status: Neutral, Overbought, or Oversold.

Visual Guide

🟢 Lime Zone: Clean Bullish Trend.

🔴 Red Zone: Clean Bearish Trend.

🟠 Orange Zone: High Choppiness (Stay Out).

🟣 'X' Marker: Exact price where the Stop Loss was triggered.

Disclaimer: For educational and research purposes only. Always manage your risk.

Sniper PerfectOverview Sniper Perfect is an advanced trend-following system designed to filter out "fakeouts" and institutional traps using a multi-layered verification protocol. It combines Volume Flow (VFI), Volatility (CHOP), and Momentum (RSI) to ensure entry only occurs in high-probability setups.

Key Features

🛡️ The Triple Filter Protocol

Strict Choppiness Filter: Uses a strict CHOP threshold (40). If the market is moving sideways, the algorithm locks all new entries to prevent whipsaws.

RSI Extremes Protection: Prevents FOMO buying at tops (Overbought > 70) and panic selling at bottoms (Oversold < 30).

Conflict Zone Detection: Identifies divergence between Price action and Money Flow. If price rises but institutional money exits, the background turns Gray and trading is disabled.

🔒 Adaptive Risk Management

Heat-Breathing Stop Loss: The SL distance adjusts dynamically based on market Volume and Volatility ("Heat").

Ratchet Mechanism: A mechanical lock ensures the Stop Loss can ONLY move in the direction of profit. It never loosens, guaranteeing that paper profits are protected.

📊 Live Dashboard A real-time panel in the bottom-right corner displays:

VFI Flow: Positive/Negative money flow.

Market Status: Active vs. Locked (Choppy).

RSI Status: Neutral, Overbought, or Oversold.

Visual Guide

🟢 Lime Zone: Clean Bullish Trend.

🔴 Red Zone: Clean Bearish Trend.

🟠 Orange Zone: High Choppiness (Stay Out).

🟣 'X' Marker: Exact price where the Stop Loss was triggered.

Disclaimer: For educational and research purposes only. Always manage your risk.

The Truth Sniper: Breathing Edition**Overview**

This is a highly advanced trend-following strategy designed to filter out market noise ("Fakeouts") and manage risk using a dynamic "Breathing Ratchet" mechanism. It combines traditional trend analysis with institutional money flow logic to identify the true market direction.

**Key Features**

**1. The Conflict Zone (Gray Zone Filter)**

Most strategies fail during low-volume accumulation or distribution phases. This algorithm introduces a "Conflict Zone" logic:

* **True Rally (Green):** Price is above EMA50 AND Money Flow (VFI) is positive.

* **True Drop (Red):** Price is below EMA50 AND Money Flow (VFI) is negative.

* **Conflict (Gray Background):** When Price and Money Flow disagree (e.g., Price rising on negative volume), the background turns Gray. **Trading is disabled** in these zones to avoid bull/bear traps.

**2. Breathing Stop-Loss Mechanism (Volatility Adjusted)**

The Stop Loss isn't static. It "breathes" based on market heat (Volume/RSI):

* **High Heat (High Volatility):** The SL loosens its grip, moving towards the bottom of the Fibonacci zone to allow price fluctuation without premature exits.

* **Low Heat (Low Volatility):** The SL tightens aggressively towards the price to lock in profits during slow momentum.

**3. The Ratchet Lock (Slippage Prevention)**

To ensure maximum profit retention, the "Breathing" mechanism is governed by a **Ratchet Logic**:

* **For Longs:** The Stop Loss can ONLY move UP. If the "Breathing" calculation suggests lowering the stop (due to increased volatility), the Ratchet blocks it, keeping the SL at the highest historical level.

* **For Shorts:** The Stop Loss can ONLY move DOWN.

**4. Fibonacci Exit Zones**

Exits are calculated based on a 60-day dynamic High/Low lookback, creating "Zones" (0-23.6%, 23.6-38.2%, etc.) that the price must conquer. The SL trails these zones mechanically.

**Visual Guide**

* **Lime/Red Background:** Active Trade Zone (Confirmed Trend).

* **Gray Background:** Conflict Zone (Stay Out / Hold).

* **Purple 'X':** The exact price level where the Stop Loss was hit (Fixed marker).

* **Stepline:** The active Stop Loss level (Visible only during open trades).

**Disclaimer**

This script is for educational and research purposes only. Always manage your risk.

XRP Non-Stop Strategy (TP 25% / SL 15%)This strategy performs continuous automated trading exclusively on XRP. It opens long positions during favorable trend conditions, using a fixed Take Profit target of 25% above the entry price and a fixed Stop Loss of 15% below the entry. Once a trade is closed (either TP or SL), the strategy automatically re-enters on the next valid signal, enabling uninterrupted trading.

The script includes:

Dynamic Take Profit & Stop Loss lines

Optional EMA trend filter

Visual BUY and EXIT markers

TradingView alerts for automation or notifications

This strategy is built for traders who want a simple, price-action-driven system without fixed price levels, relying only on percentage-based movement from each entry.

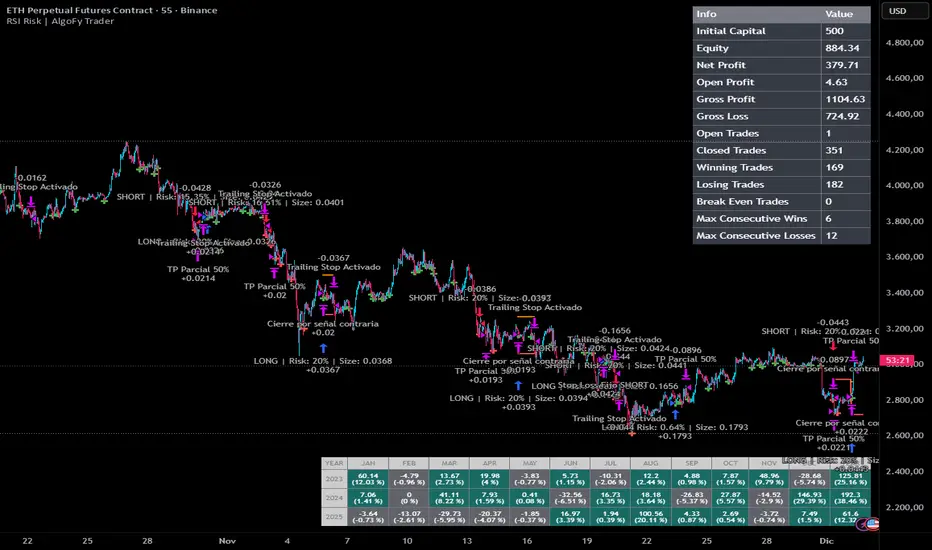

RSI Risk | AlgoFy TraderRSI Risk | AlgoFy Trader

Overview

The RSI Risk | AlgoFy Trader is a trading system that combines RSI-based entry signals with automated capital management. This strategy identifies potential momentum shifts while controlling risk through calculated position sizing.

Key Features

Dynamic Risk Management:

Fixed Risk Per Trade: Users set maximum risk percentage per trade.

Automatic Position Sizing: Calculates position size based on stop-loss distance.

Capital Protection: Limits each trade's risk to user-defined percentage.

RSI Entry System:

Momentum Detection: Uses RSI crossovers above/below defined thresholds.

Clear Signals: Provides long/short entries on momentum transitions.

Multiple Exit Layers:

Dynamic Stop Loss: Stop based on recent price structure.

Fixed Safety Stop: Optional percentage-based stop loss.

Partial Take Profit: Optional early profit-taking.

Trailing Stop: Optional dynamic profit protection.

Performance Tracking:

Trade Statistics: Tracks win/loss streaks and performance metrics.

Monthly Dashboard: Shows monthly/yearly P&L with equity views.

Trade Details: Displays risk percentage and position size.

How It Works

Signal Detection: Monitors RSI for crossover events.

Risk Calculation: Determines stop-loss based on recent volatility.

Position Sizing: Calculates exact position to match risk percentage.

Example:

Account: $10,000 | Risk: 2% ($200 max)

Stop loss at 4% distance

Position size: $5,000

Result: 4% loss on $5,000 = $200 (2% of account)

Recommended Settings

Risk: 1-2% per trade

Enable fixed stop at 3-4%

Consider trailing stop activation

This script provides disciplined RSI trading with automated risk control, adjusting exposure while maintaining strict risk limits.