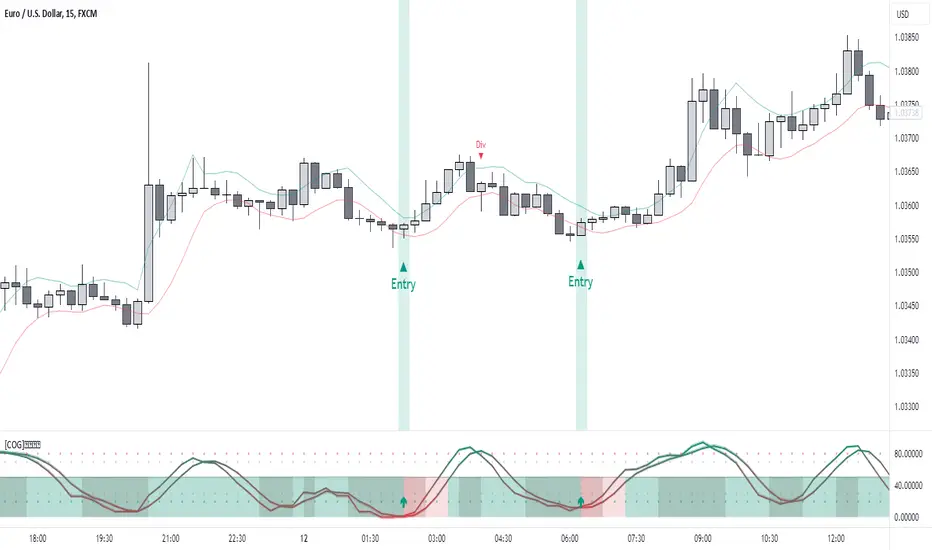

WaveTrend Divergences, Candle Colouring and TP Signal [LuciTech]WaveTrend is a momentum-based oscillator designed to track trend strength, detect divergences, and highlight potential take-profit zones using Bollinger Bands. It provides a clear visualization of market conditions to help traders identify trend shifts and exhaustion points.

The WaveTrend Oscillator consists of a smoothed momentum line (WT Line) and a signal line, which work together to indicate trend direction and possible reversals. When the WT Line crosses above the signal line, it suggests bullish momentum, while crossing below signals bearish momentum.

Candle colouring changes dynamically based on WaveTrend crossovers. If the WT Line crosses above the signal line, candles turn bullish. If the WT Line crosses below the signal line, candles turn bearish. This provides an immediate visual cue for trend direction.

Divergence Detection identifies when price action contradicts the WaveTrend movement.

Bullish Divergence appears when price makes a lower low, but the WT Line forms a higher low, suggesting weakening bearish pressure.

Bearish Divergence appears when price makes a higher high, but the WT Line forms a lower high, indicating weakening bullish pressure.

Plus (+) Divergences are stronger signals that occur when the first pivot of the divergence happens at an extreme level—above +60 for bearish divergence or below -60 for bullish divergence. These levels suggest the market is overbought or oversold, making the divergence more significant.

Bollinger Band Signals highlight potential take-profit zones by detecting when the WT Line moves beyond its upper or lower Bollinger Band.

If the WT Line crosses above the upper band, it signals stretched bullish momentum, suggesting a possible pullback or reversal.

If the WT Line crosses below the lower band, it indicates stretched bearish momentum, warning of a potential bounce.

How It Works

The WaveTrend momentum calculation is based on an EMA-smoothed moving average to filter out noise and provide a more reliable trend indication.

The WT Line (momentum line) fluctuates based on market momentum.

The signal line smooths out the WT Line to help identify trend shifts.

When the WT Line crosses above the signal line, it suggests buying pressure, and when it crosses below, it indicates selling pressure.

Divergences are detected by comparing pivot highs and lows in price with pivot highs and lows in the WT Line.

A pivot forms when a local high or low is confirmed after a certain number of bars.

The indicator tracks whether price action and the WT Line are making opposite movements.

If a divergence occurs and the first pivot was beyond ±60, it is marked as a Plus Divergence, making it a stronger reversal signal.

Bollinger Bands are applied directly to the WT Line instead of price, identifying when the WT Line moves outside its volatility range. This helps traders recognize when momentum is overstretched and a potential reversal or retracement is likely.

Settings

Channel Length (default: 8) controls the period used to calculate the WT Line.

Average Length (default: 16) smooths the WT Line for better trend detection.

Divergences (on/off) enables or disables divergence plotting.

Candle colouring (on/off) applies or removes trend-based candle colour changes.

Bollinger Band Signals (on/off) toggles take-profit signals when the WT Line crosses the bands.

Bullish/Bearish colours allow customization of divergence and signal colours.

Interpretation

The WaveTrend Oscillator helps traders assess market momentum and trend strength.

Crossovers between the WT Line and signal line indicate potential trend reversals.

Divergences warn of weakening momentum and possible reversals, with Plus Divergences acting as stronger signals.

Bollinger Band Crosses highlight areas where momentum is overstretched, signaling potential profit-taking opportunities.

Oscillaltor

[COG]StochRSI Zenith📊 StochRSI Zenith

This indicator combines the traditional Stochastic RSI with enhanced visualization features and multi-timeframe analysis capabilities. It's designed to provide traders with a comprehensive view of market conditions through various technical components.

🔑 Key Features:

• Advanced StochRSI Implementation

- Customizable RSI and Stochastic calculation periods

- Multiple moving average type options (SMA, EMA, SMMA, LWMA)

- Adjustable signal line parameters

• Visual Enhancement System

- Dynamic wave effect visualization

- Energy field display for momentum visualization

- Customizable color schemes for bullish and bearish signals

- Adaptive transparency settings

• Multi-Timeframe Analysis

- Higher timeframe confirmation

- Synchronized market structure analysis

- Cross-timeframe signal validation

• Divergence Detection

- Automated bullish and bearish divergence identification

- Customizable lookback period

- Clear visual signals for confirmed divergences

• Signal Generation Framework

- Price action confirmation

- SMA-based trend filtering

- Multiple confirmation levels for reduced noise

- Clear entry signals with customizable display options

📈 Technical Components:

1. Core Oscillator

- Base calculation: 13-period RSI (adjustable)

- Stochastic calculation: 8-period (adjustable)

- Signal lines: 5,3 smoothing (adjustable)

2. Visual Systems

- Wave effect with three layers of visualization

- Energy field display with dynamic intensity

- Reference bands at 20/30/50/70/80 levels

3. Confirmation Mechanisms

- SMA trend filter

- Higher timeframe alignment

- Price action validation

- Divergence confirmation

⚙️ Customization Options:

• Visual Parameters

- Wave effect intensity and speed

- Energy field sensitivity

- Color schemes for bullish/bearish signals

- Signal display preferences

• Technical Parameters

- All core calculation periods

- Moving average types

- Divergence detection settings

- Signal confirmation criteria

• Display Settings

- Chart and indicator signal placement

- SMA line visualization

- Background highlighting options

- Label positioning and size

🔍 Technical Implementation:

The indicator combines several advanced techniques to generate signals. Here are key components with code examples:

1. Core StochRSI Calculation:

// Base RSI calculation

rsi = ta.rsi(close, rsi_length)

// StochRSI transformation

stochRSI = ((ta.highest(rsi, stoch_length) - ta.lowest(rsi, stoch_length)) != 0) ?

(100 * (rsi - ta.lowest(rsi, stoch_length))) /

(ta.highest(rsi, stoch_length) - ta.lowest(rsi, stoch_length)) : 0

2. Signal Generation System:

// Core signal conditions

crossover_buy = crossOver(sk, sd, cross_threshold)

valid_buy_zone = sk < 30 and sd < 30

price_within_sma_bands = close <= sma_high and close >= sma_low

// Enhanced signal generation

if crossover_buy and valid_buy_zone and price_within_sma_bands and htf_allows_long

if is_bullish_candle

long_signal := true

else

awaiting_bull_confirmation := true

3. Multi-Timeframe Analysis:

= request.security(syminfo.tickerid, mtf_period,

)

The HTF filter looks at a higher timeframe (default: 4H) to confirm the trend

It only allows:

Long trades when the higher timeframe is bullish

Short trades when the higher timeframe is bearish

📈 Trading Application Guide:

1. Signal Identification

• Oversold Opportunities (< 30 level)

- Look for bullish crosses of K-line above D-line

- Confirm with higher timeframe alignment

- Wait for price action confirmation (bullish candle)

• Overbought Conditions (> 70 level)

- Watch for bearish crosses of K-line below D-line

- Verify higher timeframe condition

- Confirm with bearish price action

2. Divergence Trading

• Bullish Divergence

- Price makes lower lows while indicator makes higher lows

- Most effective when occurring in oversold territory

- Use with support levels for entry timing

• Bearish Divergence

- Price makes higher highs while indicator shows lower highs

- Most reliable in overbought conditions

- Combine with resistance levels

3. Wave Effect Analysis

• Strong Waves

- Multiple wave lines moving in same direction indicate momentum

- Wider wave spread suggests increased volatility

- Use for trend strength confirmation

• Energy Field

- Higher intensity in trading zones suggests stronger moves

- Use for momentum confirmation

- Watch for energy field convergence with price action

The energy field is like a heat map that shows momentum strength

It gets stronger (more visible) when:

Price is in oversold (<30) or overbought (>70) zones

The indicator lines are moving apart quickly

A strong signal is forming

Think of it as a "strength meter" - the more visible the energy field, the stronger the potential move

4. Risk Management Integration

• Entry Confirmation

- Wait for all signal components to align

- Use higher timeframe for trend direction

- Confirm with price action and SMA positions

• Stop Loss Placement

- Consider placing stops beyond recent swing points

- Use ATR for dynamic stop calculation

- Account for market volatility

5. Position Management

• Partial Profit Taking

- Consider scaling out at overbought/oversold levels

- Use wave effect intensity for exit timing

- Monitor energy field for momentum shifts

• Trade Duration

- Short-term: Use primary signals in trading zones

- Swing trades: Focus on divergence signals

- Position trades: Utilize higher timeframe signals

⚠️ Important Usage Notes:

• Avoid:

- Trading against strong trends

- Relying solely on single signals

- Ignoring higher timeframe context

- Over-leveraging based on signals

Remember: This tool is designed to assist in analysis but should never be used as the sole decision-maker for trades. Always maintain proper risk management and combine with other forms of analysis.

Smart Money Index + True Strength IndexThe Smart Money Index + True Strength Index indicator is a combination of two popular technical analysis indicators: the Smart Money Index (SMI) and the True Strength Index (TSI). This combined indicator helps traders identify potential entry points for long and short positions based on signals from both indexes.

Main Components:

Smart Money Index (SMI):

The SMI measures the difference between the closing and opening price of a candle multiplied by the trading volume over a certain period of time. This allows you to assess the activity of large players ("smart money") in the market. If the SMI value is above a certain threshold (smiThreshold), it may indicate a bullish trend, and if lower, it may indicate a bearish trend.

True Strength Index (TSI):

The TSI is an oscillator that measures the strength of a trend by comparing the price change of the current bar with the previous bar. It uses two exponential moving averages (EMAS) to smooth the data. TSI values can fluctuate around zero, with values above the overbought level indicating a possible downward correction, and values below the oversold level signaling a possible upward correction.

Parameters:

SMI Length: Defines the number of candles used to calculate the average SMI value. The default value is 14.

SMI Threshold: A threshold value that is used to determine a buy or sell signal. The default value is 0.

Length of the first TSI smoothing (tsiLength1): The length of the first EMA for calculating TSI. The default value is 25.

Second TSI smoothing length (tsiLength2): The length of the second EMA for additional smoothing of TSI values. The default value is 13.

TSI Overbought level: The level at which the market is considered to be overbought. The default value is 25.

Oversold level TSI: The level at which it is considered that the market is in an oversold state. The default value is -25.

Logic of operation:

SMI calculation:

First, the difference between the closing and opening price of each candle (close - open) is calculated.

This difference is then multiplied by the trading volume.

The resulting product is averaged using a simple moving average (SMA) over a specified period (smiLength).

Calculation of TSI:

The price change relative to the previous bar is calculated (close - close ).

The first EMA with the length tsiLength1 is applied.

Next, a second EMA with a length of tsiLength2 is applied to obtain the final TSI value.

The absolute value of price changes is calculated in the same way, and two emas are also applied.

The final TSI index is calculated as the ratio of these two values multiplied by 100.

Graphical representation:

The SMI and TSI lines are plotted on the graph along with their respective thresholds.

For SMI, the line is drawn in orange, and the threshold level is dotted in gray.

For the TSI, the line is plotted in blue, the overbought and oversold levels are indicated by red and green dotted lines, respectively.

Conditions for buy/sell signals:

A buy (long) signal is generated when:

SMI is greater than the threshold (smi > smiThreshold)

TSI crosses the oversold level from bottom to top (ta.crossover(tsi, oversold)).

A sell (short) signal is generated when:

SMI is less than the threshold (smi < smiThreshold)

TSI crosses the overbought level from top to bottom (ta.crossunder(tsi, overbought)).

Signal display:

When the conditions for a long or short are met, labels labeled "LONG" or "SHORT" appear on the chart.

The label for the long is located under the candle and is colored green, and for the short it is above the candle and is colored red.

Notification generation:

The indicator also supports notifications via the TradingView platform. Notifications are sent when conditions arise for a long or short position.

This combined indicator provides the trader with the opportunity to use both SMI and TSI signals simultaneously, which can improve the accuracy of trading decisions.

[COG] Adaptive Squeeze Intensity 📊 Adaptive Squeeze Intensity (ASI) Indicator

🎯 Overview

The Adaptive Squeeze Intensity (ASI) indicator is an advanced technical analysis tool that combines the power of volatility compression analysis with momentum, volume, and trend confirmation to identify high-probability trading opportunities. It quantifies the degree of price compression using a sophisticated scoring system and provides clear entry signals for both long and short positions.

⭐ Key Features

- 📈 Comprehensive squeeze intensity scoring system (0-100)

- 📏 Multiple Keltner Channel compression zones

- 📊 Volume analysis integration

- 🎯 EMA-based trend confirmation

- 🎨 Proximity-based entry validation

- 📱 Visual status monitoring

- 🎨 Customizable color schemes

- ⚡ Clear entry signals with directional indicators

🔧 Components

1. 📐 Squeeze Intensity Score (0-100)

The indicator calculates a total squeeze intensity score based on four components:

- 📊 Band Convergence (0-40 points): Measures the relationship between Bollinger Bands and Keltner Channels

- 📍 Price Position (0-20 points): Evaluates price location relative to the base channels

- 📈 Volume Intensity (0-20 points): Analyzes volume patterns and thresholds

- ⚡ Momentum (0-20 points): Assesses price momentum and direction

2. 🎨 Compression Zones

Visual representation of squeeze intensity levels:

- 🔴 Extreme Squeeze (80-100): Red zone

- 🟠 Strong Squeeze (60-80): Orange zone

- 🟡 Moderate Squeeze (40-60): Yellow zone

- 🟢 Light Squeeze (20-40): Green zone

- ⚪ No Squeeze (0-20): Base zone

3. 🎯 Entry Signals

The indicator generates entry signals based on:

- ✨ Squeeze release confirmation

- ➡️ Momentum direction

- 📊 Candlestick pattern confirmation

- 📈 Optional EMA trend alignment

- 🎯 Customizable EMA proximity validation

⚙️ Settings

🔧 Main Settings

- Base Length: Determines the calculation period for main indicators

- BB Multiplier: Sets the Bollinger Bands deviation multiplier

- Keltner Channel Multipliers: Three separate multipliers for different compression zones

📈 Trend Confirmation

- Four customizable EMA periods (default: 21, 34, 55, 89)

- Optional trend requirement for entry signals

- Adjustable EMA proximity threshold

📊 Volume Analysis

- Customizable volume MA length

- Adjustable volume threshold for signal confirmation

- Option to enable/disable volume analysis

🎨 Visualization

- Customizable bullish/bearish colors

- Optional intensity zones display

- Status monitor with real-time score and state information

- Clear entry arrows and background highlights

💻 Technical Code Breakdown

1. Core Calculations

// Base calculations for EMAs

ema_1 = ta.ema(close, ema_length_1)

ema_2 = ta.ema(close, ema_length_2)

ema_3 = ta.ema(close, ema_length_3)

ema_4 = ta.ema(close, ema_length_4)

// Proximity calculation for entry validation

ema_prox_raw = math.abs(close - ema_1) / ema_1 * 100

is_close_to_ema_long = close > ema_1 and ema_prox_raw <= prox_percent

```

### 2. Squeeze Detection System

```pine

// Bollinger Bands setup

BB_basis = ta.sma(close, length)

BB_dev = ta.stdev(close, length)

BB_upper = BB_basis + BB_mult * BB_dev

BB_lower = BB_basis - BB_mult * BB_dev

// Keltner Channels setup

KC_basis = ta.sma(close, length)

KC_range = ta.sma(ta.tr, length)

KC_upper_high = KC_basis + KC_range * KC_mult_high

KC_lower_high = KC_basis - KC_range * KC_mult_high

```

### 3. Scoring System Implementation

```pine

// Band Convergence Score

band_ratio = BB_width / KC_width

convergence_score = math.max(0, 40 * (1 - band_ratio))

// Price Position Score

price_range = math.abs(close - KC_basis) / (KC_upper_low - KC_lower_low)

position_score = 20 * (1 - price_range)

// Final Score Calculation

squeeze_score = convergence_score + position_score + vol_score + mom_score

```

### 4. Signal Generation

```pine

// Entry Signal Logic

long_signal = squeeze_release and

is_momentum_positive and

(not use_ema_trend or (bullish_trend and is_close_to_ema_long)) and

is_bullish_candle

short_signal = squeeze_release and

is_momentum_negative and

(not use_ema_trend or (bearish_trend and is_close_to_ema_short)) and

is_bearish_candle

```

📈 Trading Signals

🚀 Long Entry Conditions

- Squeeze release detected

- Positive momentum

- Bullish candlestick

- Price above relevant EMAs (if enabled)

- Within EMA proximity threshold (if enabled)

- Sufficient volume confirmation (if enabled)

🔻 Short Entry Conditions

- Squeeze release detected

- Negative momentum

- Bearish candlestick

- Price below relevant EMAs (if enabled)

- Within EMA proximity threshold (if enabled)

- Sufficient volume confirmation (if enabled)

⚠️ Alert Conditions

- 🔔 Extreme squeeze level reached (score crosses above 80)

- 🚀 Long squeeze release signal

- 🔻 Short squeeze release signal

💡 Tips for Usage

1. 📱 Use the status monitor to track real-time squeeze intensity and state

2. 🎨 Pay attention to the color gradient for trend direction and strength

3. ⏰ Consider using multiple timeframes for confirmation

4. ⚙️ Adjust EMA and proximity settings based on your trading style

5. 📊 Use volume analysis for additional confirmation in liquid markets

📝 Notes

- 🔧 The indicator combines multiple technical analysis concepts for robust signal generation

- 📈 Suitable for all tradable markets and timeframes

- ⭐ Best results typically achieved in trending markets with clear volatility cycles

- 🎯 Consider using in conjunction with other technical analysis tools for confirmation

⚠️ Disclaimer

This technical indicator is designed to assist in analysis but should not be considered as financial advice. Always perform your own analysis and risk management when trading.

Two-Pole Oscillator [BigBeluga]

The Two-Pole Oscillator is an advanced smoothing oscillator designed to provide traders with precise market signals by leveraging deviation-based calculations combined with a unique two-pole filtering technique. It offers clear visual representation and actionable signals for smart trading decisions.

🔵Key Features:

Two-Pole Filtering: Smooths out the main oscillator signal to reduce noise, providing a cleaner and more reliable view of market momentum and trend strength.

// Two-pole smooth filter function

f_two_pole_filter(source, length) =>

var float smooth1 = na

var float smooth2 = na

alpha = 2.0 / (length + 1)

if na(smooth1)

smooth1 := source

else

smooth1 := (1 - alpha) * smooth1 + alpha * source

if na(smooth2)

smooth2 := smooth1

else

smooth2 := (1 - alpha) * smooth2 + alpha * smooth1

Deviation-Based Oscillator: Utilizes price deviations from the mean to generate dynamic signals, making it ideal for detecting overbought and oversold conditions.

float sma1 = ta.sma(close, 25)

float sma_n1 = ((close - sma1) - ta.sma(close - sma1, 25)) / ta.stdev(close - sma1, 25)

Signal Gradient Strength: Signals on the main oscillator line feature gradient coloring based on their proximity to the 0 level:

➔ Closer to 0: More transparent, indicating weaker signals.

➔ Closer to 1 or -1: Less transparent, highlighting stronger signals.

Level-Based Signal Validation: Parallel levels are plotted on the chart for each signal:

➔ If a level is crossed by price, the signal is invalidated, marked by an "X" at the invalidation point.

Trend Continuation

Invalidation Levels: Serve as potential stop-loss or trade-reversal zones, enabling traders to make more informed and disciplined trading decisions.

Dynamic Chart Plotting: Signals are plotted directly on the chart with corresponding levels, providing a comprehensive visual representation for easy interpretation.

🔵How It Works:

The oscillator calculates price deviation from a mean value and applies two-pole filtering to smooth the resulting signal.

Gradient-colored signals reflect their strength, with transparency indicating proximity to the 0 level on the oscillator scale.

Buy and sell signals are generated based on crossovers and crossunders of the oscillator line with a signal line.

If a level is crossed, the corresponding signal is marked with a "X" plotted on the chart at the crossover point.

🔵Use Cases:

Detecting overbought or oversold market conditions with a smoother, noise-free oscillator.

Using invalidation levels to set clear stop-loss or trade exit points.

Identifying strong momentum signals and filtering out weaker, less reliable ones.

Combining oscillator signals with price action for more precise trade entries and exits.

This indicator is perfect for traders seeking a refined approach to oscillator analysis, combining signal strength visualization with actionable invalidation levels to enhance trading precision and strategy.

VWAP Divergence | dobofulopOverview :

This script identifies potential bullish and bearish divergence signals using the Volume Weighted Average Price (VWAP). It calculates VWAP resets based on a selected “Anchor Period” (Session, Week, Month, Quarter, Year, Decade, Century, or corporate events like Earnings, Dividends, Splits). When price action and VWAP move in opposite directions with a sufficiently large ATR-based move over a chosen lookback period, the script plots divergence dots on the chart.

Key Features:

VWAP Anchoring : Choose an anchor period for resetting VWAP. This could be daily, weekly, monthly, or based on specific corporate events (Earnings, Dividends, Splits).

Divergence Detection : Looks for instances where the price is moving up while VWAP moves down (potential bullish divergence), and vice versa for bearish divergence.

ATR Filter : Uses the ATR (Average True Range) to filter out minor or insignificant price moves, helping to reduce noise.

Gap Check : Automatically invalidates signals if large price gaps occur within the lookback range.

Visual Signals : Bullish divergences are plotted below the bar, while bearish divergences are plotted above, making it easy to spot potential reversal zones.

How to Us

Inputs:

- Anchor Period (Session, Week, Month, etc.) – determines when the VWAP calculation restarts.

- Source (Default: HLC3) – Price source for the VWAP.

- ATR Multiplier and Lookback Period – Fine-tune the threshold for detecting significant moves vs. VWAP.

Interpretation:

- Bullish Divergence Dot: Suggests potential price strength when price moves higher but VWAP moves lower.

- Bearish Divergence Dot: Suggests potential price weakness when price moves lower but VWAP moves higher.

Disclaimer:

This script is provided for educational purposes only and should not be interpreted as financial advice. Past performance does not guarantee future results. Always conduct your own analysis and consider consulting a financial professional before making trading decisions.

Flow-Weighted Volume Oscillator (FWVO)Volume Dynamics Oscillator (VDO)

Description

The Volume Dynamics Oscillator (VDO) is a powerful and innovative tool designed to analyze volume trends and provide traders with actionable insights into market dynamics. This indicator goes beyond simple volume analysis by incorporating a smoothed oscillator that visualizes the flow and momentum of trading activity, giving traders a clearer understanding of volume behavior over time.

What It Does

The VDO calculates the flow of volume by scaling raw volume data relative to its highest and lowest values over a user-defined period. This scaled volume is then smoothed using an exponential moving average (EMA) to eliminate noise and highlight significant trends. The oscillator dynamically shifts above or below a zero line, providing clear visual cues for bullish or bearish volume pressure.

Key features include:

Smoothed Oscillator: Displays the direction and momentum of volume using gradient colors.

Threshold Markers: Highlights overbought or oversold zones based on upper and lower bounds of the oscillator.

Visual Fill Zones: Uses color-filled areas to emphasize positive and negative volume flow, making it easy to interpret market sentiment.

How It Works

The calculation consists of several steps:

Smoothing with EMA: An EMA of the scaled volume is applied to reduce noise and enhance trends. A separate EMA period can be adjusted by the user (Volume EMA Period).

Dynamic Thresholds: The script determines upper and lower bounds around the smoothed oscillator, derived from its recent highest and lowest values. These thresholds indicate critical zones of volume momentum.

How to Use It

Bullish Signals: When the oscillator is above zero and green, it suggests strong buying pressure. A crossover from negative to positive can signal the start of an uptrend.

Bearish Signals: When the oscillator is below zero and blue, it indicates selling pressure. A crossover from positive to negative signals potential bearish momentum.

Overbought/Oversold Zones: Use the upper and lower threshold levels as indicators of extreme volume momentum. These can act as early warnings for trend reversals.

Traders can adjust the following inputs to customize the indicator:

High/Low Period: Defines the period for volume scaling.

Volume EMA Period: Adjusts the smoothing factor for the oscillator.

Smooth Factor: Controls the responsiveness of the smoothed oscillator.

Originality and Usefulness

The VDO stands out by combining dynamic volume scaling, EMA smoothing, and gradient-based visualization into a single, cohesive tool. Unlike traditional volume indicators, which often display raw or cumulative data, the VDO emphasizes relative volume strength and flow, making it particularly useful for spotting reversals, confirming trends, and identifying breakout opportunities.

The integration of color-coded fills and thresholds enhances usability, allowing traders to quickly interpret market conditions without requiring deep technical expertise.

Chart Recommendations

To maximize the effectiveness of the VDO, use it on a clean chart without additional indicators. The gradient coloring and filled zones make it self-explanatory, but traders can overlay basic trendlines or support/resistance levels for additional context.

For advanced users, the VDO can be paired with price action strategies, candlestick patterns, or other trend-following indicators to improve accuracy and timing.

PGO For Loop | mad_tiger_slayerPGO For Loop Indicator

The PGO For Loop indicator, inspired by Alex Orekhov's "Pretty Good Oscillator," and indicator originally made by Mark Johnson, the PGO designed as a fast and responsive tool to capture quick price movements in financial markets. This oscillator leverages a combination of moving averages and Average True Range (ATR) to measure price deviations, providing a concise yet powerful framework for identifying potential trade entry and exit points. What makes this

"enhanced" PGO indicator special is its ability to identify trending periods more accurately. By using thresholds, this allows the script to enter accurate long and short conditions extremely quickly.

Intended Uses:

Used to capture long-term trends:

Used to identify quick reversals:

Used on higher timeframes above 8hrs for more accurate signals

Used in strategies to enter and exit trades quickly

Can be used for Scalping

NOT Intended Uses:

Not to be used as Mean Reversion

Not to be used as valuation (Overbought or Oversold)

Key Features:

Quick Detection of Market Movements:

The indicator's primary focus is on speed, making it suitable for medium-term traders looking to capitalize on rapid price changes. It is particularly effective in trending or volatile markets.

Customizable Thresholds:

Users can set upper and lower thresholds to define long and short conditions, offering flexibility to adapt the indicator to different trading styles and asset classes.

Noisy but Purposeful:

While the PGO For Loop may generate frequent signals, it is specifically tuned for traders aiming to enter and exit trades quickly, embracing the noise as part of its effectiveness in capturing rapid market dynamics.

Integrated Visuals:

The script plots key levels and provides dynamic visual feedback through colored candles and shapes, enabling intuitive and quick decision-making.

How It Works:

Oscillator Calculation:

The PGO value is derived by comparing the source price's deviation from its moving average to the ATR. This highlights price movements relative to recent volatility.

Signal Identification:

When the oscillator exceeds the upper threshold, it signals potential long opportunities UNTIL the PGO reaches the lower threshold.

When the oscillator drops below the lower threshold, it signals potential short opportunities UNTIL the oscillator reaches above the upper threshold.

No signals occur when the oscillator lies between these thresholds.

Visual Cues:

Color-coded candles indicate market bias (green for long, red for short, gray for neutral).

Upward and downward triangles highlight changes in signal direction.

Note:

This indicator is intentionally "noisy," as it prioritizes capturing fast movements over filtering out minor fluctuations. Users should pair it with other tools or techniques to confirm signals and manage risk effectively.

Enhanced Price Z-Score OscillatorThe Enhanced Price Z-Score Oscillator by tkarolak is a powerful tool that transforms raw price data into an easy-to-understand statistical visualization using Z-Score-derived candlesticks. Simply put, it shows how far prices stray from their average in terms of standard deviations (Z-Scores), helping traders identify when prices are unusually high (overbought) or unusually low (oversold).

The indicator’s default feature displays Z-Score Candlesticks, where each candle reflects the statistical “distance” of the open, high, low, and close prices from their average. This creates a visual map of market extremes and potential reversal points. For added flexibility, you can also switch to Z-Score line plots based on either Close prices or OHLC4 averages.

With clear threshold lines (±2σ and ±3σ) marking moderate and extreme price deviations, and color-coded zones to highlight overbought and oversold areas, the oscillator simplifies complex statistical concepts into actionable trading insights.

True Amplitude Envelopes (TAE)The True Envelopes indicator is an adaptation of the True Amplitude Envelope (TAE) method, based on the research paper " Improved Estimation of the Amplitude Envelope of Time Domain Signals Using True Envelope Cepstral Smoothing " by Caetano and Rodet. This indicator aims to create an asymmetric price envelope with strong predictive power, closely following the methodology outlined in the paper.

Due to the inherent limitations of Pine Script, the indicator utilizes a Kernel Density Estimator (KDE) in place of the original Cepstral Smoothing technique described in the paper. While this approach was chosen out of necessity rather than superiority, the resulting method is designed to be as effective as possible within the constraints of the Pine environment.

This indicator is ideal for traders seeking an advanced tool to analyze price dynamics, offering insights into potential price movements while working within the practical constraints of Pine Script. Whether used in dynamic mode or with a static setting, the True Envelopes indicator helps in identifying key support and resistance levels, making it a valuable asset in any trading strategy.

Key Features:

Dynamic Mode: The indicator dynamically estimates the fundamental frequency of the price, optimizing the envelope generation process in real-time to capture critical price movements.

High-Pass Filtering: Uses a high-pass filtered signal to identify and smoothly interpolate price peaks, ensuring that the envelope accurately reflects significant price changes.

Kernel Density Estimation: Although implemented as a workaround, the KDE technique allows for flexible and adaptive smoothing of the envelope, aimed at achieving results comparable to the more sophisticated methods described in the original research.

Symmetric and Asymmetric Envelopes: Provides options to select between symmetric and asymmetric envelopes, accommodating various trading strategies and market conditions.

Smoothness Control: Features adjustable smoothness settings, enabling users to balance between responsiveness and the overall smoothness of the envelopes.

The True Envelopes indicator comes with a variety of input settings that allow traders to customize the behavior of the envelopes to match their specific trading needs and market conditions. Understanding each of these settings is crucial for optimizing the indicator's performance.

Main Settings

Source: This is the data series on which the indicator is applied, typically the closing price (close). You can select other price data like open, high, low, or a custom series to base the envelope calculations.

History: This setting determines how much historical data the indicator should consider when calculating the envelopes. A value of 0 will make the indicator process all available data, while a higher value restricts it to the most recent n bars. This can be useful for reducing the computational load or focusing the analysis on recent market behavior.

Iterations: This parameter controls the number of iterations used in the envelope generation algorithm. More iterations will typically result in a smoother envelope, but can also increase computation time. The optimal number of iterations depends on the desired balance between smoothness and responsiveness.

Kernel Style: The smoothing kernel used in the Kernel Density Estimator (KDE). Available options include Sinc, Gaussian, Epanechnikov, Logistic, and Triangular. Each kernel has different properties, affecting how the smoothing is applied. For example, Gaussian provides a smooth, bell-shaped curve, while Epanechnikov is more efficient computationally with a parabolic shape.

Envelope Style: This setting determines whether the envelope should be Static or Dynamic. The Static mode applies a fixed period for the envelope, while the Dynamic mode automatically adjusts the period based on the fundamental frequency of the price data. Dynamic mode is typically more responsive to changing market conditions.

High Q: This option controls the quality factor (Q) of the high-pass filter. Enabling this will increase the Q factor, leading to a sharper cutoff and more precise isolation of high-frequency components, which can help in better identifying significant price peaks.

Symmetric: This setting allows you to choose between symmetric and asymmetric envelopes. Symmetric envelopes maintain an equal distance from the central price line on both sides, while asymmetric envelopes can adjust differently above and below the price line, which might better capture market conditions where upside and downside volatility are not equal.

Smooth Envelopes: When enabled, this setting applies additional smoothing to the envelopes. While this can reduce noise and make the envelopes more visually appealing, it may also decrease their responsiveness to sudden market changes.

Dynamic Settings

Extra Detrend: This setting toggles an additional high-pass filter that can be applied when using a long filter period. The purpose is to further detrend the data, ensuring that the envelope focuses solely on the most recent price oscillations.

Filter Period Multiplier: This multiplier adjusts the period of the high-pass filter dynamically based on the detected fundamental frequency. Increasing this multiplier will lengthen the period, making the filter less sensitive to short-term price fluctuations.

Filter Period (Min) and Filter Period (Max): These settings define the minimum and maximum bounds for the high-pass filter period. They ensure that the filter period stays within a reasonable range, preventing it from becoming too short (and overly sensitive) or too long (and too sluggish).

Envelope Period Multiplier: Similar to the filter period multiplier, this adjusts the period for the envelope generation. It scales the period dynamically to match the detected price cycles, allowing for more precise envelope adjustments.

Envelope Period (Min) and Envelope Period (Max): These settings establish the minimum and maximum bounds for the envelope period, ensuring the envelopes remain adaptive without becoming too reactive or too slow.

Static Settings

Filter Period: In static mode, this setting determines the fixed period for the high-pass filter. A shorter period will make the filter more responsive to price changes, while a longer period will smooth out more of the price data.

Envelope Period: This setting specifies the fixed period used for generating the envelopes in static mode. It directly influences how tightly or loosely the envelopes follow the price action.

TAE Smoothing: This controls the degree of smoothing applied during the TAE process in static mode. Higher smoothing values result in more gradual envelope curves, which can be useful in reducing noise but may also delay the envelope’s response to rapid price movements.

Visual Settings

Top Band Color: This setting allows you to choose the color for the upper band of the envelope. This band represents the resistance level in the price action.

Bottom Band Color: Similar to the top band color, this setting controls the color of the lower band, which represents the support level.

Center Line Color: This is the color of the central price line, often referred to as the carrier. It represents the detrended price around which the envelopes are constructed.

Line Width: This determines the thickness of the plotted lines for the top band, bottom band, and center line. Thicker lines can make the envelopes more visible, especially when overlaid on price data.

Fill Alpha: This controls the transparency level of the shaded area between the top and bottom bands. A lower alpha value will make the fill more transparent, while a higher value will make it more opaque, helping to highlight the envelope more clearly.

The envelopes generated by the True Envelopes indicator are designed to provide a more precise and responsive representation of price action compared to traditional methods like Bollinger Bands or Keltner Channels. The core idea behind this indicator is to create a price envelope that smoothly interpolates the significant peaks in price action, offering a more accurate depiction of support and resistance levels.

One of the critical aspects of this approach is the use of a high-pass filtered signal to identify these peaks. The high-pass filter serves as an effective method of detrending the price data, isolating the rapid fluctuations in price that are often lost in standard trend-following indicators. By filtering out the lower frequency components (i.e., the trend), the high-pass filter reveals the underlying oscillations in the price, which correspond to significant peaks and troughs. These oscillations are crucial for accurately constructing the envelope, as they represent the most responsive elements of the price movement.

The algorithm works by first applying the high-pass filter to the source price data, effectively detrending the series and isolating the high-frequency price changes. This filtered signal is then used to estimate the fundamental frequency of the price movement, which is essential for dynamically adjusting the envelope to current market conditions. By focusing on the peaks identified in the high-pass filtered signal, the algorithm generates an envelope that is both smooth and adaptive, closely following the most significant price changes without overfitting to transient noise.

Compared to traditional envelopes and bands, such as Bollinger Bands and Keltner Channels, the True Envelopes indicator offers several advantages. Bollinger Bands, which are based on standard deviations, and Keltner Channels, which use the average true range (ATR), both tend to react to price volatility but do not necessarily follow the peaks and troughs of the price with precision. As a result, these traditional methods can sometimes lag behind or fail to capture sudden shifts in price momentum, leading to either false signals or missed opportunities.

In contrast, the True Envelopes indicator, by using a high-pass filtered signal and a dynamic period estimation, adapts more quickly to changes in price behavior. The envelopes generated by this method are less prone to the lag that often affects standard deviation or ATR-based bands, and they provide a more accurate representation of the price's immediate oscillations. This can result in better predictive power and more reliable identification of support and resistance levels, making the True Envelopes indicator a valuable tool for traders looking for a more responsive and precise approach to market analysis.

In conclusion, the True Envelopes indicator is a powerful tool that blends advanced theoretical concepts with practical implementation, offering traders a precise and responsive way to analyze price dynamics. By adapting the True Amplitude Envelope (TAE) method through the use of a Kernel Density Estimator (KDE) and high-pass filtering, this indicator effectively captures the most significant price movements, providing a more accurate depiction of support and resistance levels compared to traditional methods like Bollinger Bands and Keltner Channels. The flexible settings allow for extensive customization, ensuring the indicator can be tailored to suit various trading strategies and market conditions.

Monest Value Indicator (MVI)

Description

The Monest Value Indicator (MVI) is a modern oscillator designed to address common issues in traditional oscillators like RSI or MACD. Unlike classical oscillators, the MVI dynamically adjusts to relative price movements and market volatility, providing a transparent and reliable valuation for short-term trading decisions.

This indicator normalizes price data around a consensus line and accounts for market volatility using the Average True Range (ATR). It highlights overbought and oversold conditions, offering a unique perspective for traders.

Key Features

Dynamic Overbought/Oversold Levels : Highlights significant price extremes for better entry and exit signals. Volatility Normalization : Adapts to market conditions, ensuring consistent readings across various assets. Consensus-Based Valuation : Uses a moving average of the midrange price for baseline calculations. No Lag or Stickiness : Reacts promptly to price movements without getting stuck in extreme zones.

How It Works

Consensus Line :

Calculated as a 5-day moving average of the midrange:

Consensus = SMA((High + Low) / 2, 5) .

Offset OHLC Data :

All prices are adjusted relative to the consensus line:

Offset Price = Price - Consensus .

Volatility Normalization :

Adjusted prices are normalized using a 5-day ATR divided by 5:

Normalized Price = Offset Price / (ATR / 5) .

MVI Calculation :

The normalized closing price is plotted as the MVI.

Overbought/Oversold Levels :

Default levels are set at +8 (overbought) and -8 (oversold).

How to Use

Identifying Overbought/Oversold Conditions :

When the MVI crosses above +8 , the asset is overbought, signaling a potential reversal or pullback.

When the MVI drops below -8 , the asset is oversold, indicating a potential bounce or upward move.

Trend Confirmation :

Use the MVI to confirm trends by observing sustained movements above or below zero.

Combine with other trend indicators (e.g., Moving Averages) for robust analysis.

Alerts :

Set alerts for when the MVI crosses overbought or oversold levels to stay informed about potential trading opportunities.

Inputs

ATR Length : Default is 5. Adjust to modify the sensitivity of volatility normalization. Consensus Length : Default is 5. Change to tweak the baseline calculation.

Example

Overbought Signal : MVI exceeds +8 , indicating the asset may reverse from an overvalued position. Oversold Signal : MVI drops below -8 , suggesting the asset may recover from an undervalued state. Flat Market : MVI hovers near zero, indicating price consolidation.

Dynamic Score PSAR [QuantAlgo]Dynamic Score PSAR 📈🧬

The Dynamic Score PSAR by QuantAlgo introduces an innovative approach to trend detection by utilizing a dynamic trend scoring technique in combination with the Parabolic SAR. This method goes beyond traditional trend-following indicators by evaluating market momentum through a scoring system that analyzes price behavior over a customizable window. By dynamically adjusting to evolving market conditions, this indicator provides clearer, more adaptive trend signals that help traders and investors anticipate market reversals and capitalize on momentum shifts with greater precision.

💫 Conceptual Foundation and Innovation

At the core of the Dynamic Score PSAR is the dynamic trend score system, which assesses price movements by comparing normalized PSAR values across a range of historical data points. This dynamic trend scoring technique offers a unique, probabilistic approach to trend analysis by evaluating how the current market compares to past price movements. Unlike traditional PSAR indicators that rely on static parameters, this scoring mechanism allows the indicator to adjust in real time to market fluctuations, offering traders and investors a more responsive and insightful view of trends. This innovation makes the Dynamic Score PSAR particularly effective in detecting shifts in momentum and potential reversals, even in volatile or complex market environments.

✨ Technical Composition and Calculation

The Dynamic Score PSAR is composed of several advanced components designed to provide a higher probability of detecting accurate trend shifts. The key innovation lies in the dynamic trend scoring technique, which iterates over historical PSAR values and evaluates price momentum through a dynamic scoring system. By comparing the current normalized PSAR value with previous data points over a user-defined window, the system generates a score that reflects the strength and direction of the trend. This allows for a more refined and responsive detection of trends compared to static, traditional indicators.

To enhance clarity, the PSAR values are normalized against an Exponential Moving Average (EMA), providing a standardized framework for comparison. This normalization ensures that the indicator adapts dynamically to market conditions, making it more effective in volatile markets. The smoothing process reduces noise, helping traders and investors focus on significant trend signals.

Additionally, users can adjust the length of the data window and the sensitivity thresholds for detecting uptrends and downtrends, providing flexibility for different trading and investing environments.

📈 Features and Practical Applications

Customizable Window Length: Adjust the window length to control the indicator’s sensitivity to recent price movements. This provides flexibility for short-term or long-term trend analysis.

Uptrend/Downtrend Thresholds: Set customizable thresholds for identifying uptrends and downtrends. These thresholds define when trend signals are triggered, offering adaptability to different market conditions.

Bar Coloring and Gradient Visualization: Visual cues, including color-coded bars and gradient fills, make it easier to interpret market trends and identify key moments for potential trend reversals.

Momentum Confirmation: The dynamic trend scoring system evaluates price action over time, providing a probabilistic measure of market momentum to confirm the strength and direction of a trend.

⚡️ How to Use

✅ Add the Indicator: Add the Dynamic Score PSAR to your favourites, then to your chart and adjust the PSAR settings, window length, and trend thresholds to match your preferences. Customize the sensitivity to price movements by tweaking the window length and thresholds for different market conditions.

👀 Monitor Trend Shifts: Watch for trend changes as the normalized PSAR values cross key thresholds, and use the dynamic score to confirm the strength and direction of trends. Bar coloring and background fills visually highlight key moments for trend shifts, making it easier to spot reversals.

🔔 Set Alerts: Configure alerts for significant trend crossovers and reversals, ensuring you can act on market movements promptly, even when you’re not actively monitoring the charts.

🌟 Summary and Usage Tips

The Dynamic Score PSAR by QuantAlgo is a powerful tool that combines traditional trend-following techniques with the flexibility of a dynamic trend scoring system. This innovative approach provides clearer, more adaptive trend signals, reducing the risk of false entries and exits while helping traders and investors capture significant market moves. The ability to adjust the indicator’s sensitivity and thresholds makes it versatile across different trading and investing environments, whether you’re focused on short-term pivots or long-term trend reversals. To maximize its effectiveness, fine-tune the sensitivity settings based on current market conditions and use the visual cues to confirm trend shifts.

RSI (Kernel Optimized) | Flux Charts💎 GENERAL OVERVIEW

Introducing our new KDE Optimized RSI Indicator! This indicator adds a new aspect to the well-known RSI indicator, with the help of the KDE (Kernel Density Estimation) algorithm, estimates the probability of a candlestick will be a pivot or not. For more information about the process, please check the "HOW DOES IT WORK ?" section.

Features of the new KDE Optimized RSI Indicator :

A New Approach To Pivot Detection

Customizable KDE Algorithm

Realtime RSI & KDE Dashboard

Alerts For Possible Pivots

Customizable Visuals

❓ HOW TO INTERPRET THE KDE %

The KDE % is a critical metric that reflects how closely the current RSI aligns with the KDE (Kernel Density Estimation) array. In simple terms, it represents the likelihood that the current candlestick is forming a pivot point based on historical data patterns. a low percentage suggests a lower probability of the current candlestick being a pivot point. In these cases, price action is less likely to reverse, and existing trends may continue. At moderate levels, the possibility of a pivot increases, indicating potential trend shifts or consolidations.Traders should start monitoring closely for confirmation signals. An even higher KDE % suggests a strong likelihood that the current candlestick could form a pivot point, which could lead to a reversal or significant price movement. These points often align with overbought or oversold conditions in traditional RSI analysis, making them key moments for potential trade entry or exit.

📌 HOW DOES IT WORK ?

The RSI (Relative Strength Index) is a widely used oscillator among traders. It outputs a value between 0 - 100 and gives a glimpse about the current momentum of the price action. This indicator then calculates the RSI for each candlesticks, and saves them into an array if the candlestick is a pivot. The low & high pivot RSIs' are inserted into two different arrays. Then the a KDE array is calculated for both of the low & high pivot RSI arrays. Explaining the KDE might be too much for this write-up, but for a brief explanation, here are the steps :

1. Define the necessary options for the KDE function. These are : Bandwidth & Nº Steps, Array Range (Array Max - Array Min)

2. After that, create a density range array. The array has (steps * 2 - 1) elements and they are calculated by (arrMin + i * stepCount), i being the index.

3. Then, define a kernel function. This indicator has 3 different kernel distribution modes : Uniform, Gaussian and Sigmoid

4. Then, define a temporary value for the current element of KDE array.

5. For each element E in the pivot RSI array, add "kernel(densityRange.get(i) - E, 1.0 / bandwidth)" to the temporary value.

6. Add 1.0 / arrSize * to the KDE array.

Then the prefix sum array of the KDE array is calculated. For each candlestick, the index closest to it's RSI value in the KDE array is found using binary search. Then for the low pivot KDE calculation, the sum of KDE values from found index to max index is calculated. For the high pivot KDE, the sum of 0 to found index is used. Then if high or low KDE value is greater than the activation threshold determined in the settings, a bearish or bullish arrow is plotted after bar confirmation respectively. The arrows are drawn as long as the KDE value of current candlestick is greater than the threshold. When the KDE value is out of the threshold, a less transparent arrow is drawn, indicating a possible pivot point.

🚩 UNIQUENESS

This indicator combines RSI & KDE Algorithm to get a foresight of possible pivot points. Pivot points are important entry, confirmation and exit points for traders. But to their nature, they can be only detected after more candlesticks are rendered after them. The purpose of this indicator is to alert the traders of possible pivot points using KDE algorithm right away when they are confirmed. The indicator also has a dashboard for realtime view of the current RSI & Bullish or Bearish KDE value. You can fully customize the KDE algorithm and set up alerts for pivot detection.

⚙️ SETTINGS

1. RSI Settings

RSI Length -> The amount of bars taken into account for RSI calculation.

Source -> The source value for RSI calculation.

2. Pivots

Pivot Lengths -> Pivot lengths for both high & low pivots. For example, if this value is set to 21; 21 bars before AND 21 bars after a candlestick must be higher for a candlestick to be a low pivot.

3. KDE

Activation Threshold -> This setting determines the amount of arrows shown. Higher options will result in more arrows being rendered.

Kernel -> The kernel function as explained in the upper section.

Bandwidth -> The bandwidth variable as explained in the upper section. The smoothness of the KDE function is tied to this setting.

Nº Bins -> The Nº Steps variable as explained in the upper section. It determines the precision of the KDE algorithm.

Inverse Fisher Oscillator [BigBeluga]The Inverse Fisher Oscillator is a powerful tool for identifying market trends and potential reversal points by applying the Inverse Fisher Transform to normalized price data. This indicator plots multiple smoothed oscillators, each color-coded to signify their relation to dynamic volatility bands. Additionally, the Butterworth filter is incorporated to further refine trend signals. The Inverse Fisher Oscillator offers traders a visually appealing and insightful approach to trend analysis and market direction detection.

🔵 KEY FEATURES

● Inverse Fisher Oscillator Visualization

Multiple Oscillators : The indicator calculates and plots six different Inverse Fisher Oscillators, each smoothed at increasing levels to provide a layered view of price momentum.

Color-Coded Signals : The oscillator lines are color-coded based on their relation to the volatility bands—green for bullish momentum, red for bearish momentum, and yellow for neutral movements.

● Butterworth Filter Integration

Filtering : The Butterworth filter is applied to mid-line Bands to reduce noise, allowing for clearer trend detection.

// Calculate constants for the Butterworth filter

float piPrd = math.pi / mid_len

float g = math.sqrt(2)

float a1 = math.exp(-g * piPrd)

float b1 = 2 * a1 * math.cos(g * piPrd)

float coef2 = b1

float coef3 = -a1 * a1

float coef1 = (1 - b1 + a1 * a1) / 4

// Source data for the Butterworth filter

float source = ifish // The first inverse Fisher Oscillator is used as the source

// Previous source and butter filter values

var float butter = na // Initialize the 'butter' variable

// Handle null values using the nz function

float prevB1 = nz(butter , source) // Use 'source' as a fallback if butter is null

float prevB2 = nz(butter , source) // Use 'source' as a fallback if butter is null

// Calculate the Butterworth filter value

butter := coef1 * (source + (2 * source ) + source ) + (coef2 * prevB1) + (coef3 * prevB2)

● Numbered Signal Marks

Signal Markers : The indicator plots numbered signals on the chart when an oscillator crosses above the upper volatility band or below the lower volatility band.

Numbered Lines : Numbers correspond to the different oscillators (1-6), helping traders easily identify which smoothing level generated the signal.

Visual Cues : The signals are color-coded—green for bullish crossovers and red for bearish crossunders—providing clear visual cues for trend accumulation phases.

Mid-Line Option : Traders can choose between plotting the Butterworth filter as a dynamic mid-line or simply displaying it as part of the bands.

Volatility Bands : Dynamic volatility bands provide additional context for interpreting the strength and sustainability of trends.

● Dashboard Display

Real-Time Market Trend Overview : The dashboard in the bottom-right corner of the chart displays the market trend based on the Inverse Fisher Oscillator for six different smoothing levels, providing a clear visual summary of market direction.

Direction Symbols : Directional symbols (up, down, or neutral) are displayed in the dashboard, color-coded to represent bullish, bearish, or neutral momentum.

Current Price Display : The dashboard also shows the current price and highlights whether it is above or below the opening price.

🔵 HOW TO USE

● Identifying Trend Reversals

Bullish Reversals : When the oscillators short period lines start to cross above the upper volatility band (green), it indicates potential bullish momentum.

Bearish Reversals : When the oscillator crosses below the lower volatility band (red), it signals potential bearish momentum.

Neutral Signals : When the oscillator remains within the bands (yellow), it suggests that the market is in a neutral or consolidating state. Traders may choose to wait for a clearer trend signal.

● Using the Dashboard for Trend Overview

Market Trend Summary : The dashboard provides a quick overview of market direction across six different smoothing levels. Green arrows indicate bullish momentum, red arrows indicate bearish momentum, and wavy lines suggest neutrality.

Price Context : The dashboard also displays the current price, helping traders quickly assess whether the price is moving in the expected direction relative to their trend analysis.

● Volatility Band Interpretation

Volatility-Based Signals : Pay attention to how the oscillators interact with the volatility bands. Strong trends will often result in oscillators staying above or below the bands, while weaker trends or consolidations will see oscillators hovering within the bands.

🔵 CUSTOMIZATION

Length and Smoothing : Adjust the length and smoothing parameters to fit different market conditions and timeframes.

Bands Multiplier : Customize the multiplier for the volatility bands to make them more or less sensitive to price changes.

Mid-Line Type : Choose whether to display the Butterworth filter as a mid-line or incorporate it into the volatility bands.

Signal Markers : Toggle on or off the number markers for signal crossovers, making it easier to identify key entry and exit points.

🔵 CONCLUSION

The Inverse Fisher Oscillator combines the power of the Inverse Fisher Transform and the Butterworth filter to provide a sophisticated approach to trend and reversal detection. By leveraging volatility-based analysis and visually intuitive signals, this indicator helps traders spot potential entry and exit points with greater clarity. The customizable dashboard display adds further value, offering a real-time summary of market conditions to enhance decision-making. Use this tool in conjunction with other technical analysis methods to develop a well-rounded trading strategy.

GannLSVZO Indicator [Algo Alert]The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Gann Laplace Smoothed Volume Zone Oscillator GannLSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the upgraded Discrete Fourier Transform, the Laplace Stieltjes Transform. Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Laplace with Gann Swing Entries and Exits (orange X) and with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

ORIGINALITY & USFULLNESS:

Personal combination of Gann swings and Laplace Stieltjes Transform of a price which results in less noise Volume Zone Oscillator.

The Laplace Stieltjes Transform is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

The Gann swings and the Gan swing strategy is developed by meomeo105, this Gann high and low algorithm forms the basis of the EMA modification.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 and Strategy closes all it's positions when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Laplace Stieltjes Transform approximation of a close price are taken from aprox library.

Key Features:

You can tailor the Indicator/Strategy to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Laplace Stieltjes Transform (FLT) and the innovative Double Discrete Fourier Transform (DTF32) soothed price series to suit your analytical needs.

Use dynamic calculation of Laplace coefficient or the static one. You may modify those inputs and Strategy entries with Gann swings.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame. I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

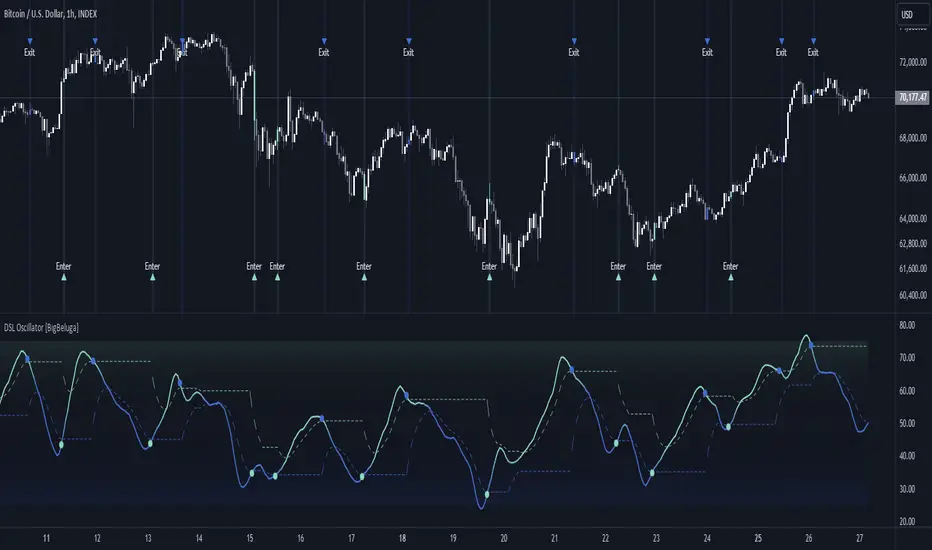

DSL Oscillator [BigBeluga]DSL Oscillator BigBeluga

The DSL (Discontinued Signal Lines) Oscillator is an advanced technical analysis tool that combines elements of the Relative Strength Index (RSI), Discontinued Signal Lines, and Zero-Lag Exponential Moving Average (ZLEMA). This versatile indicator is designed to help traders identify trend direction, momentum, and potential reversal points in the market.

What are Discontinued Signal Lines (DSL)?

Discontinued Signal Lines are an extension of the traditional signal line concept used in many indicators. While a standard signal line compares an indicator's value to its smoothed (slightly lagging) state, DSL takes this idea further by using multiple adaptive lines that respond to the indicator's current value. This approach provides a more nuanced view of the indicator's state and momentum, making it easier to determine trends and desired states of the indicator.

🔵 KEY FEATURES

● Discontinued Signal Lines (DSL)

Uses multiple adaptive lines that respond to the indicator's value

Provides a more nuanced view of the indicator's state and momentum

Helps determine trends and desired states of the indicator more effectively

Available in "Fast" and "Slow" modes for different responsiveness

Acts as dynamic support and resistance levels for the oscillator

● DSL Oscillator

Based on a combination of RSI and Discontinued Signal Lines

// Discontinued Signal Lines

dsl_lines(src, length)=>

UP = 0.

DN = 0.

UP := (src > ta.sma(src, length)) ? nz(UP ) + dsl_mode / length * (src - nz(UP )) : nz(UP )

DN := (src < ta.sma(src, length)) ? nz(DN ) + dsl_mode / length * (src - nz(DN )) : nz(DN )

Smoothed using Zero-Lag Exponential Moving Average for reduced lag

// Zero-Lag Exponential Moving Average function

zlema(src, length) =>

lag = math.floor((length - 1) / 2)

ema_data = 2 * src - src

ema2 = ta.ema(ema_data, length)

ema2

Oscillates between 0 and 100

Color-coded for easy interpretation of market conditions

● Signal Generation

Generates buy signals when the oscillator crosses above the lower DSL line below 50

Generates sell signals when the oscillator crosses below the upper DSL line above 50

Signals are visualized on both the oscillator and the main chart

● Visual Cues

Background color changes on signal occurrences for easy identification

Candles on the main chart are colored based on the latest signal

Oscillator line color changes based on its position relative to the DSL lines

🔵 HOW TO USE

● Trend Identification

Use the color and position of the DSL Oscillator relative to its Discontinued Signal Lines to determine the overall market trend

● Entry Signals

Look for buy signals (green circles) when the oscillator crosses above the lower DSL line

Look for sell signals (blue circles) when the oscillator crosses below the upper DSL line

Confirm signals with the triangles on the main chart and background color changes

● Exit Signals

Consider exiting long positions on exit signals and short positions on Entery signals

Watch for the oscillator crossing back between the DSL lines as a potential early exit signal

● Momentum Analysis

Strong momentum is indicated when the oscillator moves rapidly towards extremes and away from the DSL lines

Weakening momentum can be spotted when the oscillator struggles to reach new highs or lows, or starts converging with the DSL lines

The space between the DSL lines can indicate potential momentum strength - wider gaps suggest stronger trends

● Confirmation

Use the DSL lines as dynamic support/resistance levels for the oscillator

Look for convergence between oscillator signals and price action on the main chart

Combine signals with other technical indicators or chart patterns for stronger confirmation

🔵 CUSTOMIZATION

The DSL Oscillator offers several customization options:

Adjust the main calculation length for the DSL lines

Choose between "Fast" and "Slow" modes for the DSL lines calculation

By fine-tuning these settings, traders can adapt the DSL Oscillator to various market conditions and personal trading strategies.

The DSL Oscillator provides a multi-faceted approach to market analysis, combining trend identification, momentum assessment, and signal generation in one comprehensive tool. Its dynamic nature and visual cues make it suitable for both novice and experienced traders across various timeframes and markets. The integration of RSI, Discontinued Signal Lines, and ZLEMA offers traders a sophisticated yet intuitive tool to inform their trading decisions.

The use of Discontinued Signal Lines sets this oscillator apart from traditional indicators by providing a more adaptive and nuanced view of market conditions. This can potentially lead to more accurate trend identification and signal generation, especially in markets with varying volatility.

Traders can use the DSL Oscillator to identify trends, spot potential reversals, and gauge market momentum. The combination of the oscillator, dynamic signal lines, and clear visual signals provides a holistic view of market conditions. As with all technical indicators, it's recommended to use the DSL Oscillator in conjunction with other forms of analysis and within the context of a well-defined trading strategy.

S&P Short-Range Oscillator**SHOULD BE USED ON THE S&P 500 ONLY**

The S&P Short-Range Oscillator (SRO), inspired by the principles of Jim Cramer's oscillator, is a technical analysis tool designed to help traders identify potential buy and sell signals in the stock market, specifically for the S&P 500 index. The SRO combines several market indicators to provide a normalized measure of market sentiment, assisting traders in making informed decisions.

The SRO utilizes two simple moving averages (SMAs) of different lengths: a 5-day SMA and a 10-day SMA. It also incorporates the daily price change and market breadth (the net change of closing prices). The 5-day and 10-day SMAs are calculated based on the closing prices. The daily price change is determined by subtracting the opening price from the closing price. Market breadth is calculated as the difference between the current closing price and the previous closing price.

The raw value of the oscillator, referred to as SRO Raw, is the sum of the daily price change, the 5-day SMA, the 10-day SMA, and the market breadth. This raw value is then normalized using its mean and standard deviation over a 20-day period, ensuring that the oscillator is centered and maintains a consistent scale. Finally, the normalized value is scaled to fit within the range of -15 to 15.

When interpreting the SRO, a value below -5 indicates that the market is potentially oversold, suggesting it might be a good time to start buying stocks as the market could be poised for a rebound. Conversely, a value above 5 suggests that the market is potentially overbought. In this situation, it may be prudent to hold on to existing positions or consider selling if you have substantial gains.

The SRO is visually represented as a blue line on a chart, making it easy to track its movements. Red and green horizontal lines mark the overbought (5) and oversold (-5) levels, respectively. Additionally, the background color changes to light red when the oscillator is overbought and light green when it is oversold, providing a clear visual cue.

By incorporating the S&P Short-Range Oscillator into your trading strategy, you can gain valuable insights into market conditions and make more informed decisions about when to buy, sell, or hold your stocks. However, always consider other market factors and perform your own analysis before making any trading decisions.

The S&P Short-Range Oscillator is a powerful tool for traders looking to gain insights into market sentiment. It provides clear buy and sell signals through its combination of multiple indicators and normalization process. However, traders should be aware of its lagging nature and potential complexity, and use it in conjunction with other analysis methods for the best results.

Disclaimer

The S&P Short-Range Oscillator is for informational purposes only and should not be considered financial advice. Trading involves risk, and you should conduct your own research or consult a financial advisor before making investment decisions. The author is not responsible for any losses incurred from using this indicator. Use at your own risk.

ATH/ATL Tracker [LuxAlgo]The ATH/ATL Tracker effectively displays changes made between new All-Time Highs (ATH)/All-Time Lows (ATL) and their previous respective values, over the entire history of available data.

The indicator shows a histogram of the change between a new ATH/ATL and its respective preceding ATH/ATL. A tooltip showing the price made during a new ATH/ATL alongside its date is included.

🔶 USAGE

By tracking the change between new ATHs/ATLs and older ATHs/ATLs, traders can gain insight into market sentiment, breadth, and rotation.

If many stocks are consistently setting new ATHs and the number of new ATHs is increasing relative to old ATHs, it could indicate broad market participation in a rally. If only a few stocks are reaching new ATHs or the number is declining, it might signal that the market's upward momentum is decreasing.

A significant increase in new ATHs suggests optimism and willingness among investors to buy at higher prices, which could be considered a positive sentiment. On the other hand, a decrease or lack of new ATHs might indicate caution or pessimism.