BTC Future Gamma-Weighted Momentum Model (BGMM)The BTC Future Gamma-Weighted Momentum Model (BGMM) is a quantitative trading strategy that utilizes the Gamma-weighted average price (GWAP) in conjunction with a momentum-based approach to predict price movements in the Bitcoin futures market. The model combines the concept of weighted price movements with trend identification, where the Gamma factor amplifies the weight assigned to recent prices. It leverages the idea that historical price trends and weighting mechanisms can be utilized to forecast future price behavior.

Theoretical Background:

1. Momentum in Financial Markets:

Momentum is a well-established concept in financial market theory, referring to the tendency of assets to continue moving in the same direction after initiating a trend. Any observed market return over a given time period is likely to continue in the same direction, a phenomenon known as the “momentum effect.” Deviations from a mean or trend provide potential trading opportunities, particularly in highly volatile assets like Bitcoin.

Numerous empirical studies have demonstrated that momentum strategies, based on price movements, especially those correlating long-term and short-term trends, can yield significant returns (Jegadeesh & Titman, 1993). Given Bitcoin’s volatile nature, it is an ideal candidate for momentum-based strategies.

2. Gamma-Weighted Price Strategies:

Gamma weighting is an advanced method of applying weights to price data, where past price movements are weighted by a Gamma factor. This weighting allows for the reinforcement or reduction of the influence of historical prices based on an exponential function. The Gamma factor (ranging from 0.5 to 1.5) controls how much emphasis is placed on recent data: a value closer to 1 applies an even weighting across periods, while a value closer to 0 diminishes the influence of past prices.

Gamma-based models are used in financial analysis and modeling to enhance a model’s adaptability to changing market dynamics. This weighting mechanism is particularly advantageous in volatile markets such as Bitcoin futures, as it facilitates quick adaptation to changing market conditions (Black-Scholes, 1973).

Strategy Mechanism:

The BTC Future Gamma-Weighted Momentum Model (BGMM) utilizes an adaptive weighting strategy, where the Bitcoin futures prices are weighted according to the Gamma factor to calculate the Gamma-Weighted Average Price (GWAP). The GWAP is derived as a weighted average of prices over a specific number of periods, with more weight assigned to recent periods. The calculated GWAP serves as a reference value, and trading decisions are based on whether the current market price is above or below this level.

1. Long Position Conditions:

A long position is initiated when the Bitcoin price is above the GWAP and a positive price movement is observed over the last three periods. This indicates that an upward trend is in place, and the market is likely to continue in the direction of the momentum.

2. Short Position Conditions:

A short position is initiated when the Bitcoin price is below the GWAP and a negative price movement is observed over the last three periods. This suggests that a downtrend is occurring, and a continuation of the negative price movement is expected.

Backtesting and Application to Bitcoin Futures:

The model has been tested exclusively on the Bitcoin futures market due to Bitcoin’s high volatility and strong trend behavior. These characteristics make the market particularly suitable for momentum strategies, as strong upward or downward movements are often followed by persistent trends that can be captured by a momentum-based approach.

Backtests of the BGMM on the Bitcoin futures market indicate that the model achieves above-average returns during periods of strong momentum, especially when the Gamma factor is optimized to suit the specific dynamics of the Bitcoin market. The high volatility of Bitcoin, combined with adaptive weighting, allows the model to respond quickly to price changes and maximize trading opportunities.

Scientific Citations and Sources:

• Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65–91.

• Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637–654.

• Fama, E. F., & French, K. R. (1992). The Cross-Section of Expected Stock Returns. The Journal of Finance, 47(2), 427–465.

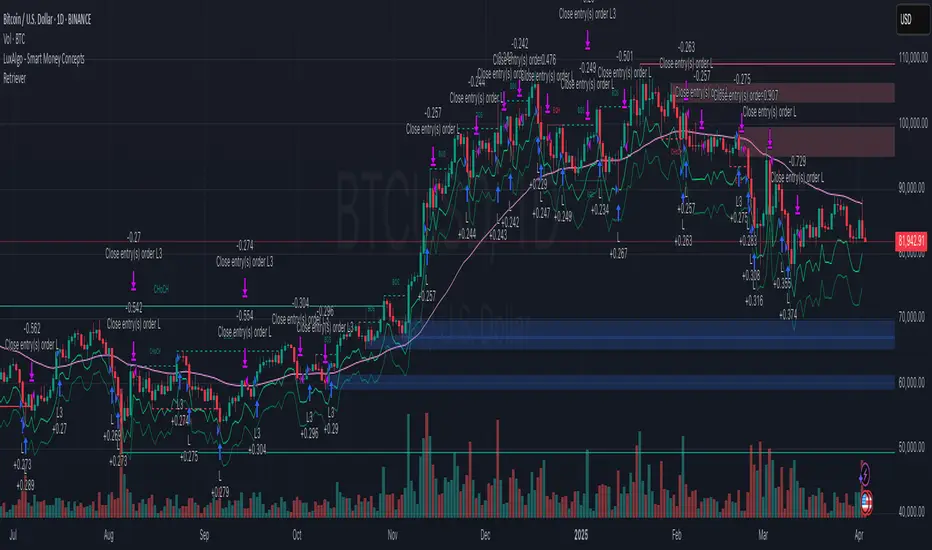

Médias Móveis

The RetrieverThis Pine Script strategy, named "The Retriever" aims to capitalize on price dips based on the size of the candlestick body. It uses a moving average of the body size to identify potential long entry points. Here's a breakdown:

Body Size Calculation: It calculates the absolute difference between the close and open prices (body) to determine the candlestick body size.

Entry Signals:

long: A long entry signal is generated when the close price is significantly higher than the moving average of the body size (ta.sma(body, 100)) multiplied by a factor (mult). Thanks to this principle we are entering just bigger dips but just in case it is sudden movement, typically dip during bulish trend.

longExtra: A second, more aggressive long entry signal is generated when the close price is even further above the moving average (multiplied by mult * 2). This signal is very rare and it is helping to decrease entry point in case huge market dips which can occor just few times per year.

Quantity Calculation: The order quantity (qty) is dynamically calculated based on the current equity and the price range between minRange and maxRange. It aims to adjust the quantity inversely to the price range, possibly increasing the quantity when the price range is smaller. It is actually very smart in several ways:

it is making bigger trades when market price is low (closer to manually defined minRange) and vice versa making smaller trades when market is close to maxRange

trade size is calculated based on current equity so it allows to use compound interest effect

as there is no SL in this strategy trade size is calculated to be max around 50-60% drawdown based on backtested results so it can survive 80-90% market drawdowns (entry point is after huge dip)

Exit Conditions: All open positions are closed when either of these conditions is met:

The last candle is green (close is lower than open). There is also minProfit param defined which is set to 0 so it means that our position has to be in profit. So we are never closing in loss. We have to differentiate here between order and position. Order can be in loss but overal position has to be always in profit.

John Bob-Trading-BotDeveloped by Ayebale John Bob with the help of his bestie, this innovative strategy combines advanced Smart Money Concepts with practical risk management tools to help traders identify and capitalize on key market moves.

Key Features:

Smart Money Concepts & Fair Value Gaps (FVG):

The strategy monitors price action for fair value gaps, which are visualized as extremely faint horizontal lines on the chart. These FVGs signal potential areas where institutional traders might have entered or exited positions.

Dynamic Entry Signals:

Buy signals are triggered when the price crosses above the 50-bar lowest low or when a bullish FVG is detected. Conversely, sell signals are generated when the price falls below the 50-bar highest high or a bearish FVG is identified. Each signal is visually marked on the chart with clear buy (green) and sell (red) labels.

Multi-Level Order Execution:

Once an entry signal occurs, the strategy places five separate orders, each with its own take-profit (TP) level. The TP levels are calculated dynamically using the Average True Range (ATR) and a set of predefined multipliers. This allows traders to scale out of positions as the market moves favorably.

Dynamic Risk Management:

A stop-loss is automatically set at a distance determined by the ATR, ensuring that risk is managed in accordance with current market volatility.

Real-Time Trade Information Table:

In the bottom-right corner of the chart, a trade information table displays essential details about the current trade:

Side: Displays "BUY NOW" (with a dark green background) for long entries or "SELL NOW" (with a dark red background) for short entries.

Entry Price & Stop-Loss: Shows the entry price (highlighted in green) and the corresponding stop-loss level (highlighted in red).

Take-Profit Levels: Lists the five TP levels, each of which turns green once the market price reaches that target.

Timer: A live timer in minutes counts from the moment the current trade trigger started, helping traders track the duration of their active trades.

Visual Progress Bar:

A histogram-style progress bar is plotted on the chart, visually representing the percentage gain (or loss) relative to the entry price.

This strategy was meticulously designed to incorporate both technical analysis and smart risk management, offering a robust trading solution that adapts to changing market conditions. Whether you're a seasoned trader or just starting out, the AyebaleJohnBob Trading Bot equips you with the tools and visual cues needed to make well-informed trading decisions. Enjoy a seamless blend of strategy and style—crafted with passion by Ayebale John Bob and his bestie!

BuyTheDips Trade on Trend and Fixed TP/SL

This strategy is designed to trade in the direction of the trend using exponential moving average (EMA) crossovers as signals while employing fixed percentages for take profit (TP) and stop loss (SL) to manage risk and reward. It is suitable for both scalping and swing trading on any timeframe, with its default settings optimized for short-term price movements.

How It Works

EMA Crossovers:

The strategy uses two EMAs: a fast EMA (shorter period) and a slow EMA (longer period).

A buy signal is triggered when the fast EMA crosses above the slow EMA, indicating a potential bullish trend.

A sell signal is triggered when the fast EMA crosses below the slow EMA, signaling a bearish trend.

Trend Filtering:

To improve signal reliability, the strategy only takes trades in the direction of the overall trend:

Long trades are executed only when the fast EMA is above the slow EMA (bullish trend).

Short trades are executed only when the fast EMA is below the slow EMA (bearish trend).

This filtering ensures trades are aligned with the prevailing market direction, reducing false signals.

Risk Management (Fixed TP/SL):

The strategy uses fixed percentages for take profit and stop loss:

Take Profit: A percentage above the entry price for long trades (or below for short trades).

Stop Loss: A percentage below the entry price for long trades (or above for short trades).

These percentages can be customized to balance risk and reward according to your trading style.

For example:

If the take profit is set to 2% and the stop loss to 1%, the strategy operates with a 2:1 risk-reward ratio. BINANCE:BTCUSDT

Mean Reversion Pro Strategy [tradeviZion]Mean Reversion Pro Strategy : User Guide

A mean reversion trading strategy for daily timeframe trading.

Introduction

Mean Reversion Pro Strategy is a technical trading system that operates on the daily timeframe. The strategy uses a dual Simple Moving Average (SMA) system combined with price range analysis to identify potential trading opportunities. It can be used on major indices and other markets with sufficient liquidity.

The strategy includes:

Trading System

Fast SMA for entry/exit points (5, 10, 15, 20 periods)

Slow SMA for trend reference (100, 200 periods)

Price range analysis (20% threshold)

Position management rules

Visual Elements

Gradient color indicators

Three themes (Dark/Light/Custom)

ATR-based visuals

Signal zones

Status Table

Current position information

Basic performance metrics

Strategy parameters

Optional messages

📊 Strategy Settings

Main Settings

Trading Mode

Options: Long Only, Short Only, Both

Default: Long Only

Position Size: 10% of equity

Starting Capital: $20,000

Moving Averages

Fast SMA: 5, 10, 15, or 20 periods

Slow SMA: 100 or 200 periods

Default: Fast=5, Slow=100

🎯 Entry and Exit Rules

Long Entry Conditions

All conditions must be met:

Price below Fast SMA

Price below 20% of current bar's range

Price above Slow SMA

No existing position

Short Entry Conditions

All conditions must be met:

Price above Fast SMA

Price above 80% of current bar's range

Price below Slow SMA

No existing position

Exit Rules

Long Positions

Exit when price crosses above Fast SMA

No fixed take-profit levels

No stop-loss (mean reversion approach)

Short Positions

Exit when price crosses below Fast SMA

No fixed take-profit levels

No stop-loss (mean reversion approach)

💼 Risk Management

Position Sizing

Default: 10% of equity per trade

Initial capital: $20,000

Commission: 0.01%

Slippage: 2 points

Maximum one position at a time

Risk Control

Use daily timeframe only

Avoid trading during major news events

Consider market conditions

Monitor overall exposure

📊 Performance Dashboard

The strategy includes a comprehensive status table displaying:

Strategy Parameters

Current SMA settings

Trading direction

Fast/Slow SMA ratio

Current Status

Active position (Flat/Long/Short)

Current price with color coding

Position status indicators

Performance Metrics

Net Profit (USD and %)

Win Rate with color grading

Profit Factor with thresholds

Maximum Drawdown percentage

Average Trade value

📱 Alert Settings

Entry Alerts

Long Entry (Buy Signal)

Short Entry (Sell Signal)

Exit Alerts

Long Exit (Take Profit)

Short Exit (Take Profit)

Alert Message Format

Strategy name

Signal type and direction

Current price

Fast SMA value

Slow SMA value

💡 Usage Tips

Consider starting with Long Only mode

Begin with default settings

Keep track of your trades

Review results regularly

Adjust settings as needed

Follow your trading plan

⚠️ Disclaimer

This strategy is for educational and informational purposes only. It is not financial advice. Always:

Conduct your own research

Test thoroughly before live trading

Use proper risk management

Consider your trading goals

Monitor market conditions

Never risk more than you can afford to lose

📋 Release Notes

14 January 2025

Added New Fast & Slow SMA Options:

Fibonacci-based periods: 8, 13, 21, 144, 233, 377

Additional period: 50

Complete Fast SMA options now: 5, 8, 10, 13, 15, 20, 21, 34, 50

Complete Slow SMA options now: 100, 144, 200, 233, 377

Bug Fixes:

Fixed Maximum Drawdown calculation in the performance table

Now using strategy.max_drawdown_percent for accurate DD reporting

Previous version showed incorrect DD values

Performance metrics now accurately reflect trading results

Performance Note:

Strategy tested with Fast/Slow SMA 13/377

Test conducted with 10% equity risk allocation

Daily Timeframe

For Beginners - How to Modify SMA Levels:

Find this line in the code:

fastLength = input.int(title="Fast SMA Length", defval=5, options= )

To add a new Fast SMA period: Add the number to the options list, e.g.,

To remove a Fast SMA period: Remove the number from the options list

For Slow SMA, find:

slowLength = input.int(title="Slow SMA Length", defval=100, options= )

Modify the options list the same way

⚠️ Note: Keep the periods that make sense for your trading timeframe

💡 Tip: Test any new combinations thoroughly before live trading

"Trade with Discipline, Manage Risk, Stay Consistent" - tradeviZion

Optimized Engulfing StrategyOptimized Engulfing Strategy

The Optimized Engulfing Strategy is a trend-following system designed to capitalize on bullish and bearish engulfing patterns in the market. It uses a combination of price action, trend direction, and volatility-based risk management to execute high-probability trades.

Key Components:

Bullish Engulfing Pattern:

A bullish engulfing candle is identified when:

The current candle closes above its open (bullish).

The previous candle closes below its open (bearish).

The current candle's close is higher than the previous candle's open.

The current candle's open is lower than the previous candle's close.

This pattern signals potential bullish momentum.

Bearish Engulfing Pattern:

A bearish engulfing candle is identified when:

The current candle closes below its open (bearish).

The previous candle closes above its open (bullish).

The current candle's close is lower than the previous candle's open.

The current candle's open is higher than the previous candle's close.

This pattern signals potential bearish momentum.

Trend Confirmation:

Trades are only taken in the direction of the trend:

Buy: When the 50-period SMA (simple moving average) is above the 200-period SMA, indicating an uptrend.

Sell: When the 50-period SMA is below the 200-period SMA, indicating a downtrend.

Risk Management:

Stop Loss: Placed below the low of the engulfing candle (for buys) or above the high (for sells), with an additional buffer based on the ATR (Average True Range) multiplied by a user-defined factor (default: 1.5).

Take Profit: Calculated using a fixed risk-to-reward ratio (default: 1:2), ensuring a potential reward that is double the risk.

Session Filtering:

Trades can be limited to specific trading hours using a customizable session filter (default: 24 hours).

Trade Execution:

Separate logic is implemented for buy and sell trades, allowing independent toggling of long or short positions via user inputs.

Visualization:

Bullish and bearish engulfing candles are highlighted on the chart for clarity.

The ATR value is displayed in the top-right corner of the chart for reference.

How It Works:

Identify a bullish or bearish engulfing pattern.

Confirm the direction of the trend using the 50 SMA and 200 SMA.

Ensure the market is within the allowed session filter (e.g., London or New York sessions).

Enter a trade if all conditions are met:

Long trades for bullish engulfing patterns in an uptrend.

Short trades for bearish engulfing patterns in a downtrend.

Manage the trade using a stop loss and take profit based on ATR and the risk-reward ratio.

FON60DK by leventsahThe strategy generates buy and sell signals using the Tillson T3 and TOTT (Twin Optimized Trend Tracker) indicators. Additionally, the Williams %R indicator is used to filter the signals. Below is an explanation of the main components of the code:

1. Input Parameters:

Tillson T3 and TOTT parameters: Separate parameters are defined for both buy (AL) and sell (SAT) conditions. These parameters control the sensitivity and behavior of the indicators.

Williams %R period: The period for the Williams %R indicator is set to determine overbought and oversold levels.

2. Tillson T3 Calculation:

The Tillson T3 indicator is a smoothed moving average that uses an exponential moving average (EMA) with additional smoothing. The formula calculates a weighted average of multiple EMAs to produce a smoother line.

The t3 function computes the Tillson T3 value based on the close price and the input parameters.

3. TOTT Calculation (Twin Optimized Trend Tracker):

The TOTT indicator is a trend-following tool that adjusts its sensitivity based on market conditions. It uses a combination of price action and a volatility coefficient to determine trend direction.

The Var_Func function calculates the TOTT value, which is then used to derive the OTT (Optimized Trend Tracker) levels for both buy and sell conditions.

4. Williams %R Calculation:

Williams %R is a momentum oscillator that measures overbought and oversold levels. It is calculated using the highest high and lowest low over a specified period.

5. Buy and Sell Conditions:

Buy Condition: A buy signal is generated when the Tillson T3 value crosses above the TOTT upper band (OTTup) and the Williams %R is above -20 (indicating an oversold condition).

Sell Condition: A sell signal is generated when the Tillson T3 value crosses below the TOTT lower band (OTTdnS) and the Williams %R is above -70 (used to close long positions).

6. Strategy Execution:

The strategy.entry function is used to open a long position when the buy condition is met.

The strategy.close function is used to close the long position when the sell condition is met.

7. Visualization:

The bars on the chart are colored green when a long position is open.

The Tillson T3, TOTT upper band (OTTup), and TOTT lower band (OTTdn) are plotted on the chart for both buy and sell conditions.

8. Plots:

The Tillson T3 values for buy and sell conditions are plotted in blue.

The TOTT upper and lower bands are plotted in green and red, respectively, for both buy and sell conditions.

Summary:

This strategy combines trend-following indicators (Tillson T3 and TOTT) with a momentum oscillator (Williams %R) to generate buy and sell signals. The use of separate parameters for buy and sell conditions allows for fine-tuning the strategy based on market behavior. The visual elements, such as colored bars and plotted indicators, help traders quickly identify signals and trends on the chart.

Hull Suite by MRS**Hull Suite by MRS Strategy Indicator**

The Hull Suite by MRS Strategy is a technical analysis tool designed to provide insights into market trends using variations of the Hull Moving Average (HMA). This strategy aims to help traders identify optimal entry points for both long and short positions by utilizing multiple types of Hull-based indicators.

### Key Features:

1. **Hull Moving Average Variations**: The indicator offers three different Hull Moving Average variants:

- **HMA (Hull Moving Average)**: A fast-moving average that minimizes lag and reacts quickly to price changes.

- **EHMA (Enhanced Hull Moving Average)**: A smoother version of HMA with reduced noise, offering a clearer view of market trends.

- **THMA (Triple Hull Moving Average)**: A more complex Hull average that aims to provide a stronger confirmation of trend direction.

2. **Customizable Parameters**:

- **Source Selection**: Allows traders to choose the source for calculation (e.g., closing prices).

- **Length**: A configurable parameter to adjust the period over which the moving average is calculated (e.g., 55-period for swing entries).

- **Trend Coloring**: Users can enable automatic color-coding of the Hull moving average to reflect whether the market is in an uptrend (green) or downtrend (red).

- **Candle Color**: Option to color candles based on Hull's trend, further improving the visual clarity of trend direction.

3. **Entry and Exit Signals**:

- **Buy Signal**: Generated when the Hull moving average crosses above its historical value, indicating a potential upward price movement.

- **Sell Signal**: Triggered when the Hull moving average crosses below its historical value, signaling a potential downward price movement.

- The strategy can be customized to work with long, short, or both directions, making it adaptable for various market conditions.

4. **Visual Representation**:

- **Hull Bands**: The indicator can plot the Hull moving average as bands, with customizable transparency to suit individual preferences.

- **Band Filler**: The area between the two Hull moving averages is filled, making it easier to identify trends at a glance.

5. **Backtesting and Strategy Execution**: This strategy can be tested on historical data with adjustable backtest start and stop dates, providing traders with a better understanding of its performance before live trading.

### Purpose:

The Hull Suite by MRS Strategy is designed to assist traders in determining the optimal time to enter and exit the market based on robust Hull moving averages. With its flexibility, it can be used for trend-following, swing trading, or other strategic applications.

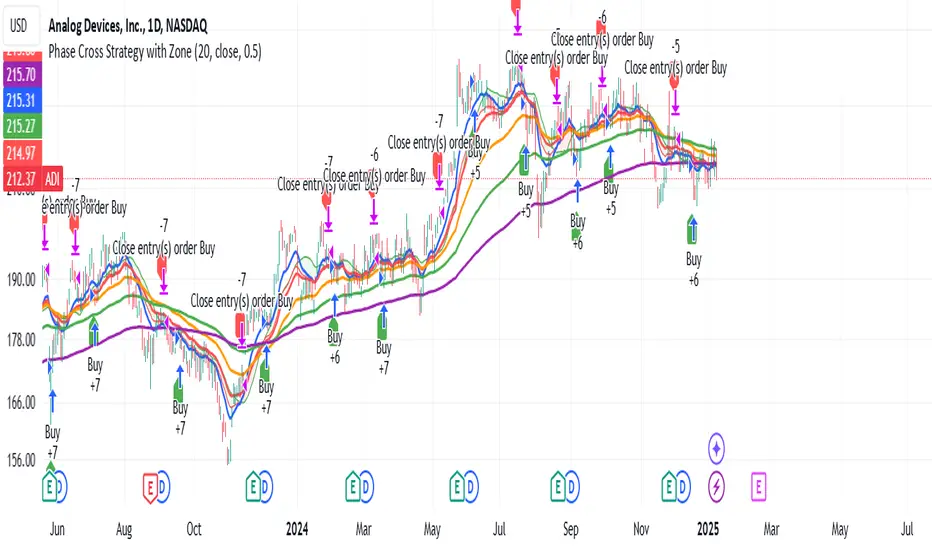

Phase Cross Strategy with Zone### Introduction to the Strategy

Welcome to the **Phase Cross Strategy with Zone and EMA Analysis**. This strategy is designed to help traders identify potential buy and sell opportunities based on the crossover of smoothed oscillators (referred to as "phases") and exponential moving averages (EMAs). By combining these two methods, the strategy offers a versatile tool for both trend-following and short-term trading setups.

### Key Features

1. **Phase Cross Signals**:

- The strategy uses two smoothed oscillators:

- **Leading Phase**: A simple moving average (SMA) with an upward offset.

- **Lagging Phase**: An exponential moving average (EMA) with a downward offset.

- Buy and sell signals are generated when these phases cross over or under each other, visually represented on the chart with green (buy) and red (sell) labels.

2. **Phase Zone Visualization**:

- The area between the two phases is filled with a green or red zone, indicating bullish or bearish conditions:

- Green zone: Leading phase is above the lagging phase (potential uptrend).

- Red zone: Leading phase is below the lagging phase (potential downtrend).

3. **EMA Analysis**:

- Includes five commonly used EMAs (13, 26, 50, 100, and 200) for additional trend analysis.

- Crossovers of the EMA 13 and EMA 26 act as secondary buy/sell signals to confirm or enhance the phase-based signals.

4. **Customizable Parameters**:

- You can adjust the smoothing length, source (price data), and offset to fine-tune the strategy for your preferred trading style.

### What to Pay Attention To

1. **Phases and Zones**:

- Use the green/red phase zone as an overall trend guide.

- Avoid taking trades when the phases are too close or choppy, as it may indicate a ranging market.

2. **EMA Trends**:

- Align your trades with the longer-term trend shown by the EMAs. For example:

- In an uptrend (price above EMA 50 or EMA 200), prioritize buy signals.

- In a downtrend (price below EMA 50 or EMA 200), prioritize sell signals.

3. **Signal Confirmation**:

- Consider combining phase cross signals with EMA crossovers for higher-confidence trades.

- Look for confluence between the phase signals and EMA trends.

4. **Risk Management**:

- Always set stop-loss and take-profit levels to manage risk.

- Use the phase and EMA zones to estimate potential support/resistance areas for exits.

5. **Whipsaws and False Signals**:

- Be cautious in low-volatility or sideways markets, as the strategy may generate false signals.

- Use additional indicators or filters to avoid entering trades during unclear market conditions.

### How to Use

1. Add the strategy to your chart in TradingView.

2. Adjust the input settings (e.g., smoothing length, offsets) to suit your trading preferences.

3. Enable the strategy tester to evaluate its performance on historical data.

4. Combine the signals with your own analysis and risk management plan for best results.

This strategy is a versatile tool, but like any trading method, it requires proper understanding and discretion. Always backtest thoroughly and trade with discipline. Let me know if you need further assistance or adjustments to the strategy!

EMA Crossover Strategy with Take Profit and Candle HighlightingStrategy Overview:

This strategy is based on the Exponential Moving Averages (EMA), specifically the EMA 20 and EMA 50. It takes advantage of EMA crossovers to identify potential trend reversals and uses multiple take-profit levels and a stop-loss for risk management.

Key Components:

EMA Crossover Signals:

Buy Signal (Uptrend): A buy signal is generated when the EMA 20 crosses above the EMA 50, signaling the start of a potential uptrend.

Sell Signal (Downtrend): A sell signal is generated when the EMA 20 crosses below the EMA 50, signaling the start of a potential downtrend.

Take Profit Levels:

Once a buy or sell signal is triggered, the strategy calculates multiple take-profit levels based on the range of the previous candle. The user can define multipliers for each take-profit level.

Take Profit 1 (TP1): 50% of the previous candle's range above or below the entry price.

Take Profit 2 (TP2): 100% of the previous candle's range above or below the entry price.

Take Profit 3 (TP3): 150% of the previous candle's range above or below the entry price.

Take Profit 4 (TP4): 200% of the previous candle's range above or below the entry price.

These levels are adjusted dynamically based on the previous candle's high and low, so they adapt to changing market conditions.

Stop Loss:

A stop-loss is set to manage risk. The default stop-loss is 3% from the entry price, but this can be adjusted in the settings. The stop-loss is triggered if the price moves against the position by this amount.

Trend Direction Highlighting:

The strategy highlights the bars (candles) with colors:

Green bars indicate an uptrend (when EMA 20 crosses above EMA 50).

Red bars indicate a downtrend (when EMA 20 crosses below EMA 50).

These visual cues help users easily identify the market direction.

Strategy Entries and Exits:

Entries: The strategy enters a long (buy) position when the EMA 20 crosses above the EMA 50 and a short (sell) position when the EMA 20 crosses below the EMA 50.

Exits: The strategy exits the positions at any of the defined take-profit levels or the stop-loss. Multiple exit levels provide opportunities to take profit progressively as the price moves in the favorable direction.

Entry and Exit Conditions in Detail:

Buy Entry Condition (Uptrend):

A buy position is opened when EMA 20 crosses above EMA 50, signaling the start of an uptrend.

The strategy calculates take-profit levels above the entry price based on the previous bar's range (high-low) and the multipliers for TP1, TP2, TP3, and TP4.

Sell Entry Condition (Downtrend):

A sell position is opened when EMA 20 crosses below EMA 50, signaling the start of a downtrend.

The strategy calculates take-profit levels below the entry price, similarly based on the previous bar's range.

Exit Conditions:

Take Profit: The strategy attempts to exit the position at one of the take-profit levels (TP1, TP2, TP3, or TP4). If the price reaches any of these levels, the position is closed.

Stop Loss: The strategy also has a stop-loss set at a default value (3% below the entry for long trades, and 3% above for short trades). The stop-loss helps to protect the position from significant losses.

Backtesting and Performance Metrics:

The strategy can be backtested using TradingView's Strategy Tester. The results will show how the strategy would have performed historically, including key metrics like:

Net Profit

Max Drawdown

Win Rate

Profit Factor

Average Trade Duration

These performance metrics can help users assess the strategy's effectiveness over historical periods and optimize the input parameters (e.g., multipliers, stop-loss level).

Customization:

The strategy allows for the adjustment of several key input values via the settings panel:

Take Profit Multipliers: Users can customize the multipliers for each take-profit level (TP1, TP2, TP3, TP4).

Stop Loss Percentage: The user can also adjust the stop-loss percentage to a custom value.

EMA Periods: The default periods for the EMA 50 and EMA 20 are fixed, but they can be adjusted for different market conditions.

Pros of the Strategy:

EMA Crossover Strategy: A classic and well-known strategy used by traders to identify the start of new trends.

Multiple Take Profit Levels: By taking profits progressively at different levels, the strategy locks in gains as the price moves in favor of the position.

Clear Trend Identification: The use of green and red bars makes it visually easier to follow the market's direction.

Risk Management: The stop-loss and take-profit features help to manage risk and optimize profit-taking.

Cons of the Strategy:

Lagging Indicators: The strategy relies on EMAs, which are lagging indicators. This means that the strategy might enter trades after the trend has already started, leading to missed opportunities or less-than-ideal entry prices.

No Confirmation Indicators: The strategy purely depends on the crossover of two EMAs and does not use other confirming indicators (e.g., RSI, MACD), which might lead to false signals in volatile markets.

How to Use in Real-Time Trading:

Use for Backtesting: Initially, use this strategy in backtest mode to understand how it would have performed historically with your preferred settings.

Paper Trading: Once comfortable, you can use paper trading to test the strategy in real-time market conditions without risking real money.

Live Trading: After testing and optimizing the strategy, you can consider using it for live trading with proper risk management in place (e.g., starting with a small position size and adjusting parameters as needed).

Summary:

This strategy is designed to identify trend reversals using EMA crossovers, with customizable take-profit levels and a stop-loss to manage risk. It's well-suited for traders looking for a systematic way to enter and exit trades based on clear market signals, while also providing flexibility to adjust for different risk profiles and trading styles.

Enhanced Gold Scalping Strategy (Backtest with Time Filter)Enhanced Gold Scalping Strategy (Backtest with Time Filter)

This script is a scalping strategy designed specifically for trading gold on lower timeframes, incorporating popular technical indicators and a session filter for optimal performance. The strategy aims to achieve consistency by combining trend-following and volatility-based conditions.

Key Features:

Indicators Used:

Exponential Moving Average (EMA): Filters trades based on the trend direction using a 50-period EMA.

Relative Strength Index (RSI): Ensures trades are taken in favorable momentum conditions (above 30 for longs and below 70 for shorts).

MACD Crossover: Identifies potential trade entries based on MACD line crossing above/below the signal line.

Average True Range (ATR): Used to dynamically calculate Stop Loss and Take Profit levels and ensure trades occur in high-volatility conditions.

Risk-Reward Optimization:

The strategy uses a customizable Risk-Reward Ratio (default is 2:1) for setting Stop Loss (SL) and Take Profit (TP) levels, ensuring that winning trades outweigh losses.

Volatility Filter:

Trades are only executed when the current ATR exceeds the 14-period ATR moving average by a defined threshold, filtering out low-volatility periods.

Session Filter:

The strategy only trades during active market hours (8:00 AM to 8:00 PM Amsterdam Time) on weekdays. This ensures trades align with periods of high liquidity and market activity.

Dynamic Entry and Exit Levels:

SL and TP levels are plotted dynamically on the chart to provide a clear visual of potential risk and reward for each trade.

Buy and Sell Signals:

Visual markers (green triangles for buy, red triangles for sell) on the chart to highlight entry points for better trade visibility.

How It Works:

Long Conditions:

MACD crossover (MACD line above the signal line).

RSI above 30.

Price is above the 50-period EMA.

ATR-based volatility condition is met.

Trade must occur within the defined session hours.

Short Conditions:

MACD crossunder (MACD line below the signal line).

RSI below 70.

Price is below the 50-period EMA.

ATR-based volatility condition is met.

Trade must occur within the defined session hours.

The strategy calculates dynamic SL and TP levels based on the ATR, ensuring flexibility to market conditions.

Customization Options:

EMA length, RSI length, and MACD parameters.

Risk-Reward Ratio for SL/TP calculations.

Volatility threshold for filtering trades.

Session start and end times for active trading hours.

Recommended Use:

Best suited for scalping gold on lower timeframes (15-min charts).

Disclaimer:

This strategy is intended for educational and backtesting purposes. Past performance is not indicative of future results. Use appropriate risk management and test thoroughly before applying to live trading.

EMA SHIFT & PARALLEL [n_dot]BINANCE:ETHUSDT.P

This strategy was developed for CRYPTO FUTURES, (the settings for ETHUSDT.P) . I aimed for the strategy to function in a live environment, so I focused on making its operation realistic:

When determining the position, only 80% (adjustable) of the available cash is invested to reduce the risk of position liquidation.

I account for a 0.05% commission, typical on the futures market, for each entry and exit.

Concept:

I modified a simple, well-known method: the crossover of two exponential moving averages (FAST, SLOW) generates the entry and exit signals.

I enhanced the base idea as follows:

For the fast EMA, I incorporated a multiplier (offset) to filter out market noise and focus only on strong signals.

I use different EMAs for long and short entry points; both have their own FAST and SLOW EMAs and their own offset. For longs, the FAST EMA is adjusted downward (<1), while for shorts, it is adjusted upward (>1). Consequently, the signal is generated when the modified FAST EMA crosses the SLOW EMA.

Risk Management:

The position includes the following components:

Separate stop-losses for long and short positions.

Separate trailers for long and short positions.

The strategy operates so that the entry point is determined by the EMA crossover, while the exit is governed only by the Stop Loss or Trailer. Optionally, it can be set to close the position at the EMA recrossing ("Close at Signal").

Trailer Operation:

An entry percentage and offset are defined. The trailer activates when the price surpasses the entry price, calculated automatically by the system.

The trailer closes the position when the price drops by the offset percentage from the highest reached price.

Example for trailer:

Purchase Price = 100

Trailer Enter = 5% → Activation Price = 105 (triggers trailer if market price crosses it).

Trailer Offset = 2%

If the price rises to 110, the exit price becomes 107.8.

If the price goes to 120, the exit price becomes 117.6.

If the price falls below 117.6, the trailer closes the position.

Settings:

Source: Determines the market price reference.

End Close: Closes positions at the end of the simulation to avoid "shadow positions" and provide an objective result.

Lot proportional to free cash (%): Only a portion of free cash is invested to meet margin requirements.

Plot Short, Plot Long: Simplifies displayed information by toggling indicator lines on/off.

Long Position (toggleable):

EMA Fast ws: Window size for FAST EMA.

EMA Slow ws: Window size for SLOW EMA.

EMA Fast down shift: Adjustment factor for FAST EMA.

Stop Loss long (%): Percent drop to close the position.

Trailer enter (%): Percent above the purchase price to activate the trailer.

Trailer offset (%): Percent drop to close the position.

Short Position (toggleable):

EMA Fast ws: Window size for FAST EMA.

EMA Slow ws: Window size for SLOW EMA.

EMA Fast up shift: Adjustment factor for FAST EMA.

Stop Loss short (%): Percent rise to close the position.

Trailer enter (%): Percent below the purchase price to activate the trailer.

Trailer offset (%): Percent rise to close the position.

Operational Framework:

If in a long position and a short EMA crossover occurs, the strategy closes the long and opens a short (flip).

If in a short position and a long EMA crossover occurs, the strategy closes the short and opens a long (flip).

A position can close in three ways:

Stop Loss

Trailer

Signal Recrossing

If none are active, the position remains open until the end of the simulation.

Observations:

Shifts significantly deviating from 1 increase overfitting risk. Recommended ranges: 0.96–0.99 (long) and 1.01–1.05 (short).

The strategy's advantage lies in risk management, crucial in leveraged futures markets. It operates with relatively low DrawDown.

Recommendations:

Bullish Market: Higher entry threshold (e.g., 6%) and larger offset (e.g., 3%).

Volatile/Sideways Market: Tighter parameters (e.g., 3%, 1%).

The method is stable, and minor parameter adjustments do not significantly impact results, helping assess overfitting: if small changes lead to drastic differences, the strategy is over-optimized.

EMA Settings: Adjust FAST and SLOW EMAs based on the asset's volatility and cyclicality.

On the crypto market, especially in the Futures market, short time periods (1–15 minutes) often show significant noise, making patterns/repetitions hard to identify. I recommend setting the interval to at least 1 hour.

I hope this contributes to your success!

Custom Dual EMA Crossover Strategy with Configurable LogicThis strategy is designed to assist traders in identifying and capitalizing on bullish market trends through a systematic and data-driven approach. It incorporates detailed trend analysis, volatility filtering, and percentage-based thresholds to provide actionable insights and high-confidence trade setups. It leverages the Exponential Moving Average and combines it with custom logic to detect volatility, maximum allowed price movements over last bars and trend confirmation.

Key Features:

- Buy orders follow several conditions, including but not limited to:

a. EMA Crossover: specifically designed to capture immediate market shifts rather than medium- or long-term trends, ensuring responsiveness to rapidly changing conditions but requiring additional confirmations to avoid false signals (see below).

b. Thresholds in Price Changes: Ensures recent price fluctuations remain within specific thresholds, allowing trades to be entered at optimal times and avoiding delayed or unsustainable short-term bullish trends.

c. Adequate Market Volatility: Requires sufficient market activity to avoid false signals stemming from low volatility conditions.

d. Bullish Medium-Term Trend: Validates a bullish medium-term trend using an EMA crossover to avoid trading during bearish market conditions and minimize risk.

- Leverages Take profit and Stop loss levels

- Implements an optional mechanism to automatically close trades after a predefined number of bars, supporting disciplined trade management.

The script does not rely on any public scripts or indicators. Apart the EMA, all the underlying logic, including the volatility thresholds and filtering mechanisms, has been custom developed to ensure originality and precision. The strategy's conditions are all configurable by the user in the TradingView pop-up, allowing it to adapt to different assets and timeframes. For example, users can set the EMA lengths to align with long-term trends for cryptocurrencies or adjust volatility thresholds to account for the specific price movement behavior of stocks or forex pairs.

---

Recommendations:

- Identify a crypto asset with potential

- Before live trading, rigorously backtest your strategy on the chosen asset and interval over a period of at least one year*, analyzing results, refining parameters' value and eventually changing timeframe and / or asset.

- Refine your approach until you achieve consistent profitability with a high win rate. Balance the two — a high win rate is great, but only if your profits outweigh your losses in the long term.

- Once successful, remain disciplined and adhere to the parameters that yield the best results. Set up TradingView alerts to trigger real-time actions via your preferred trading bot. Alerts can be set up on the Indicator, which mirrors the strategy's logic and enables users to execute real-time actions effectively. I will provide you access to the Indicator, as well as the Strategy.

* Alternatively, you can apply the strategy to a shorter period for tactical use. While this approach may increase short-term opportunities (e.g. strong bullish short term movements), it also comes with heightened risks.

Use Cases:

- Suitable for traders focusing on bullish or range-bound markets.

- Ideal for short to medium-term trading horizons.

Access and Configuration Support:

This is an invite-only script. For access, please reach out directly for subscription details. I also provide guidance on configuring the strategy with real-world examples to optimize its use for various assets, intervals and timeframes.

---

Disclaimer:

This script is a tool to support trading decisions and does not guarantee profitability. Past performance does not indicate future results. Trading carries inherent risks; always trade responsibly and manage risk accordingly.

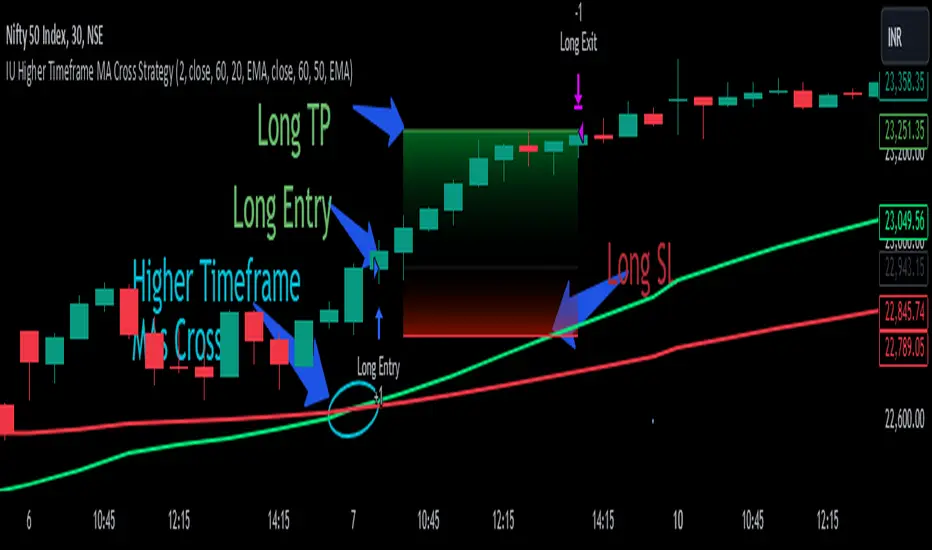

IU Higher Timeframe MA Cross StrategyIU Higher Timeframe MA Cross Strategy

The IU Higher Timeframe MA Cross Strategy is a versatile trading tool designed to identify trend by utilizing two customizable moving averages (MAs) across different timeframes and types. This strategy includes detailed entry and exit rules with fully configurable inputs, offering flexibility to suit various trading styles.

Key Features:

- Two moving averages (MA1 and MA2) with customizable types, lengths, sources, and timeframes.

- Both long and short trade setups based on MA crossovers.

- Integrated risk management with adjustable stop-loss and take-profit levels based on a user-defined risk-to-reward (RTR) ratio.

- Clear visualization of MAs, entry points, stop-loss, and take-profit zones.

Inputs:

1. Risk-to-Reward Ratio (RTR):

- Defines the take-profit level in relation to the stop-loss distance. Default is 2.

2. MA1 Settings:

- Source: Select the data source for calculating MA1 (e.g., close, open, high, low). Default is close.

- Timeframe: Specify the timeframe for MA1 calculation. Default is 60 (60-minute chart).

- Length: Set the lookback period for MA1 calculation. Default is 20.

- Type: Choose the type of moving average (options: SMA, EMA, SMMA, WMA, VWMA). Default is EMA.

- Smooth: Option to enable or disable smoothing of MA1 to merge gaps. Default is true.

3. MA2 Settings:

- Source: Select the data source for calculating MA2 (e.g., close, open, high, low). Default is close.

- Timeframe: Specify the timeframe for MA2 calculation. Default is 60 (60-minute chart).

- Length: Set the lookback period for MA2 calculation. Default is 50.

- Type: Choose the type of moving average (options: SMA, EMA, SMMA, WMA, VWMA). Default is EMA.

- Smooth: Option to enable or disable smoothing of MA2 to merge gaps. Default is true.

Entry Rules:

- Long Entry:

- Triggered when MA1 crosses above MA2 (crossover).

- Entry is confirmed only when the bar is closed and no existing position is active.

- Short Entry:

- Triggered when MA1 crosses below MA2 (crossunder).

- Entry is confirmed only when the bar is closed and no existing position is active.

Exit Rules:

- Stop-Loss:

- For long positions: Set at the low of the bar preceding the entry.

- For short positions: Set at the high of the bar preceding the entry.

- Take-Profit:

- For long positions: Calculated as (Entry Price - Stop-Loss) * RTR + Entry Price.

- For short positions: Calculated as Entry Price - (Stop-Loss - Entry Price) * RTR.

Visualization:

- Plots MA1 and MA2 on the chart with distinct colors for easy identification.

- Highlights stop-loss and take-profit levels using shaded zones for clear visual representation.

- Displays the entry level for active positions.

This strategy provides a robust framework for traders to identify and act on trend reversals while maintaining strict risk management. The flexibility of its inputs allows for seamless customization to adapt to various market conditions and trading preferences.

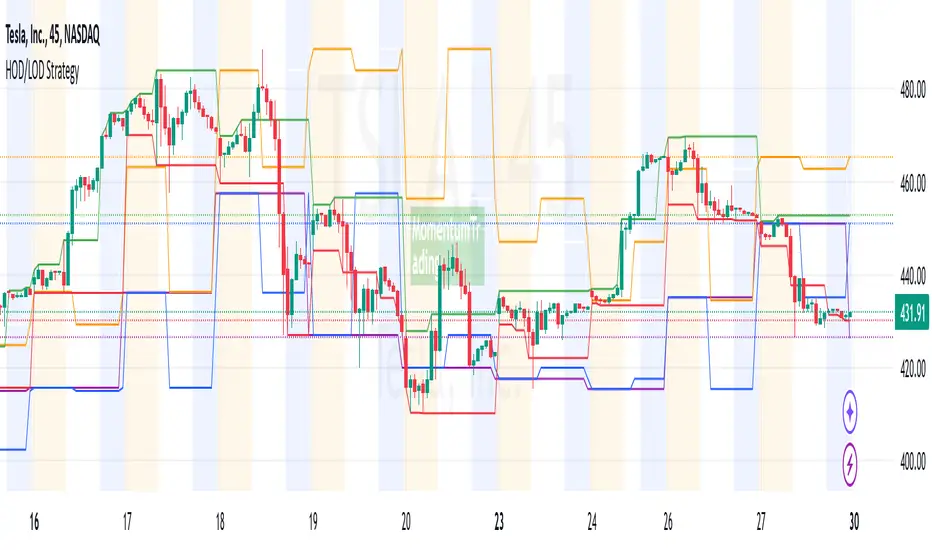

HOD/LOD/PMH/PML/PDH/PDL Strategy by @tradingbauhaus This script is a trading strategy @tradingbauhaus designed to trade based on key price levels, such as the High of Day (HOD), Low of Day (LOD), Premarket High (PMH), Premarket Low (PML), Previous Day High (PDH), and Previous Day Low (PDL). Below, I’ll explain in detail what the script does:

Core Functionality of the Script:

Calculates Key Price Levels:

HOD (High of Day): The highest price of the current day.

LOD (Low of Day): The lowest price of the current day.

PMH (Premarket High): The highest price during the premarket session (before the market opens).

PML (Premarket Low): The lowest price during the premarket session.

PDH (Previous Day High): The highest price of the previous day.

PDL (Previous Day Low): The lowest price of the previous day.

Draws Horizontal Lines on the Chart:

Plots horizontal lines on the chart for each key level (HOD, LOD, PMH, PML, PDH, PDL) with specific colors for easy visual identification.

Defines Entry and Exit Rules:

Long Entry (Buy): If the price crosses above the PMH (Premarket High) or the PDH (Previous Day High).

Short Entry (Sell): If the price crosses below the PML (Premarket Low) or the PDL (Previous Day Low).

Long Exit: If the price reaches the HOD (High of Day) during a long position.

Short Exit: If the price reaches the LOD (Low of Day) during a short position.

How the Script Works Step by Step:

Calculates Key Levels:

Uses the request.security function to fetch the HOD and LOD of the current day, as well as the highs and lows of the previous day (PDH and PDL).

Calculates the PMH and PML during the premarket session (before 9:30 AM).

Plots Levels on the Chart:

Uses the plot function to draw horizontal lines on the chart representing the key levels (HOD, LOD, PMH, PML, PDH, PDL).

Each level has a specific color for easy identification:

HOD: White.

LOD: Purple.

PDH: Orange.

PDL: Blue.

PMH: Green.

PML: Red.

Defines Trading Rules:

Uses conditions with ta.crossover and ta.crossunder to detect when the price crosses key levels.

Long Entry: If the price crosses above the PMH or PDH, a long position (buy) is opened.

Short Entry: If the price crosses below the PML or PDL, a short position (sell) is opened.

Long Exit: If the price reaches the HOD during a long position, the position is closed.

Short Exit: If the price reaches the LOD during a short position, the position is closed.

Executes Orders Automatically:

Uses the strategy.entry and strategy.close functions to open and close positions automatically based on the defined rules.

Advantages of This Strategy:

Based on Key Levels: Uses important price levels that often act as support and resistance.

Easy to Visualize: Horizontal lines on the chart make it easy to identify levels.

Automated: Entries and exits are executed automatically based on the defined rules.

Limitations of This Strategy:

Dependent on Volatility: Works best in markets with significant price movements.

False Crosses: There may be false crosses that generate incorrect signals.

No Advanced Risk Management: Does not include dynamic stop-loss or take-profit mechanisms.

How to Improve the Strategy:

Add Stop-Loss and Take-Profit: To limit losses and lock in profits.

Filter Signals with Indicators: Use RSI, MACD, or other indicators to confirm signals.

Optimize Levels: Adjust key levels based on the asset’s behavior.

In summary, this script is a trading strategy that operates based on key price levels, such as HOD, LOD, PMH, PML, PDH, and PDL. It is useful for traders who want to trade based on significant support and resistance levels.

EMA RSI Trend Reversal Ver.1Overview:

The EMA RSI Trend Reversal indicator combines the power of two well-known technical indicators—Exponential Moving Averages (EMAs) and the Relative Strength Index (RSI)—to identify potential trend reversal points in the market. The strategy looks for key crossovers between the fast and slow EMAs, and uses the RSI to confirm the strength of the trend. This combination helps to avoid false signals during sideways market conditions.

How It Works:

Buy Signal:

The Fast EMA (9) crosses above the Slow EMA (21), indicating a potential shift from a downtrend to an uptrend.

The RSI is above 50, confirming strong bullish momentum.

Visual Signal: A green arrow below the price bar and a Buy label are plotted on the chart.

Sell Signal:

The Fast EMA (9) crosses below the Slow EMA (21), indicating a potential shift from an uptrend to a downtrend.

The RSI is below 50, confirming weak or bearish momentum.

Visual Signal: A red arrow above the price bar and a Sell label are plotted on the chart.

Key Features:

EMA Crossovers: The Fast EMA crossing above the Slow EMA signals potential buying opportunities, while the Fast EMA crossing below the Slow EMA signals potential selling opportunities.

RSI Confirmation: The RSI helps confirm trend strength—values above 50 indicate bullish momentum, while values below 50 indicate bearish momentum.

Visual Cues: The strategy uses green arrows and red arrows along with Buy and Sell labels for clear visual signals of when to enter or exit trades.

Signal Interpretation:

Green Arrow / Buy Label: The Fast EMA (9) has crossed above the Slow EMA (21), and the RSI is above 50. This is a signal to buy or enter a long position.

Red Arrow / Sell Label: The Fast EMA (9) has crossed below the Slow EMA (21), and the RSI is below 50. This is a signal to sell or exit the long position.

Strategy Settings:

Fast EMA Length: Set to 9 (this determines how sensitive the fast EMA is to recent price movements).

Slow EMA Length: Set to 21 (this smooths out price movements to identify the broader trend).

RSI Length: Set to 14 (default setting to track momentum strength).

RSI Level: Set to 50 (used to confirm the strength of the trend—above 50 for buy signals, below 50 for sell signals).

Risk Management (Optional):

Use take profit and stop loss based on your preferred risk-to-reward ratio. For example, you can set a 2:1 risk-to-reward ratio (2x take profit for every 1x stop loss).

Backtesting and Optimization:

Backtest the strategy on TradingView by opening the Strategy Tester tab. This will allow you to see how the strategy would have performed on historical data.

Optimization: Adjust the EMA lengths, RSI period, and risk-to-reward settings based on your asset and time frame.

Limitations:

False Signals in Sideways Markets: Like any trend-following strategy, this indicator may generate false signals during periods of low volatility or sideways movement.

Not Suitable for All Market Conditions: This indicator performs best in trending markets. It may underperform in choppy or range-bound markets.

Strategy Example:

XRP/USD Example:

If you're trading XRP/USD and the Fast EMA (9) crosses above the Slow EMA (21), while the RSI is above 50, the indicator will signal a Buy.

Conversely, if the Fast EMA (9) crosses below the Slow EMA (21), and the RSI is below 50, the indicator will signal a Sell.

Bitcoin (BTC/USD):

On the BTC/USD chart, when the indicator shows a green arrow and a Buy label, it’s signaling a potential long entry. Similarly, a red arrow and Sell label indicate a short entry or exit from a previous long position.

Summary:

The EMA RSI Trend Reversal Indicator helps traders identify potential trend reversals with clear buy and sell signals based on the EMA crossovers and RSI confirmations. By using green arrows and red arrows, along with Buy and Sell labels, this strategy offers easy-to-understand visual signals for entering and exiting trades. Combine this with effective risk management and backtesting to optimize your trading performance.

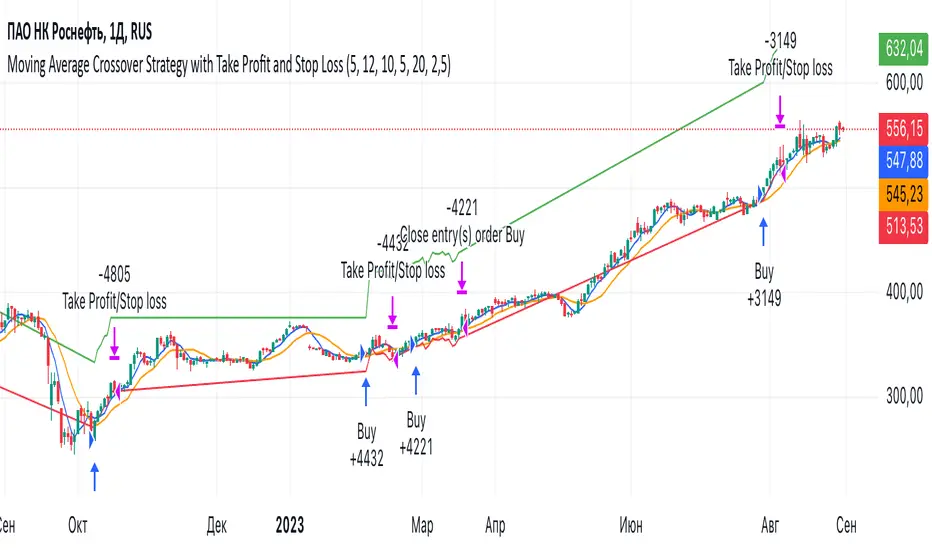

Moving Average Crossover Strategy with Take Profit and Stop LossThe Moving Average Crossover Strategy is a popular trading technique that utilizes two moving averages (MAs) of different periods to identify potential buy and sell signals. By incorporating take profit and stop loss levels, traders can effectively manage their risk while maximizing potential returns. Here’s a detailed explanation of how this strategy works:

Overview of the Moving Average Crossover Strategy

Moving Averages:

A short-term moving average (e.g., 50-day MA) reacts more quickly to price changes, while a long-term moving average (e.g., 200-day MA) smooths out price fluctuations over a longer period.

The strategy generates trading signals based on the crossover of these two averages:

Buy Signal: When the short-term MA crosses above the long-term MA (often referred to as a "Golden Cross").

Sell Signal: When the short-term MA crosses below the long-term MA (known as a "Death Cross").

Implementing Take Profit and Stop Loss

1. Setting Take Profit Levels

Definition: A take profit order automatically closes a trade when it reaches a specified profit level.

Strategy:

Determine a realistic profit target based on historical price action, support and resistance levels, or a fixed risk-reward ratio (e.g., 2:1).

For instance, if you enter a buy position at $100, you might set a take profit at $110 if you anticipate that level will act as resistance.

2. Setting Stop Loss Levels

Definition: A stop loss order limits potential losses by closing a trade when the price reaches a specified level.

Strategy:

Place the stop loss just below the most recent swing low for buy orders or above the recent swing high for sell orders.

Alternatively, you can use a percentage-based method (e.g., 2-3% below the entry point) to define your stop loss.

For example, if you enter a buy position at $100 with a stop loss set at $95, your maximum loss would be limited to $5 per share.

Example of Using Moving Average Crossover with Take Profit and Stop Loss

Entry Signal:

You observe that the 50-day MA crosses above the 200-day MA at $100. You enter a buy position.

Setting Take Profit and Stop Loss:

You analyze historical price levels and set your take profit at $110.

You place your stop loss at $95 based on recent swing lows.

Trade Management:

If the price rises to $110, your take profit order is executed, securing your profit.

If the price falls to $95, your stop loss is triggered, limiting your losses.

Relative StrengthThis strategy employs a custom "strength" function to assess the relative strength of a user-defined source (e.g., closing price, moving average) compared to its historical performance over various timeframes (8, 34, 20, 50, and 200 periods). The strength is calculated as a percentage change from an Exponential Moving Average (EMA) for shorter timeframes and a Simple Moving Average (SMA) for longer timeframes. Weights are then assigned to each timeframe based on a logarithmic scale, and a weighted average strength is computed.

Key Features:

Strength Calculation:

Calculates the relative strength of the source using EMAs and SMAs over various timeframes.

Assigns weights to each timeframe based on a logarithmic scale, emphasizing shorter timeframes.

Calculates a weighted average strength for a comprehensive view.

Visualizations:

Plots the calculated strength as a line, colored green for positive strength and red for negative strength.

Fills the background area below the line with green for positive strength and red for negative strength, enhancing visualization.

Comparative Analysis:

Optionally displays the strength of Bitcoin (BTC), Ethereum (ETH), S&P 500, Nasdaq, and Dow Jones Industrial Average (DJI) for comparison with the main source strength.

Backtesting:

Allows users to specify a start and end time for backtesting the strategy's performance.

Trading Signals:

Generates buy signals when the strength turns positive from negative and vice versa for sell signals.

Entry and exit are conditional on the backtesting time range.

Basic buy and sell signal plots are commented out (can be uncommented for visual representation).

Risk Management:

Closes all open positions and cancels pending orders outside the backtesting time range.

Disclaimer:

Backtesting results do not guarantee future performance. This strategy is for educational purposes only and should be thoroughly tested and refined before risking capital.

Additional Notes:

- The strategy uses a custom "strength" function that can be further customized to explore different timeframes and weighting schemes.

- Consider incorporating additional technical indicators or filters to refine the entry and exit signals.

- Backtesting with different parameters and market conditions is crucial for evaluating the strategy's robustness.

Three Moving Averages Strategythis is three moving averages strategy is good for day time frame best for swing trading , probability vary for 60 to 80 to increase the probability add other indictors . you can rsi or macd.

Bitcoin Exponential Profit Strategy### Strategy Description:

The **Bitcoin Trading Strategy** is an **Exponential Moving Average (EMA) crossover strategy** designed to identify bullish trends for Bitcoin.

1. **Indicators**:

- **Fast EMA (default 9 periods)**: Represents the short-term trend.

- **Slow EMA (default 21 periods)**: Represents the longer-term trend.

2. **Entry Condition**:

- A **bullish crossover** occurs when the Fast EMA crosses above the Slow EMA.

- The strategy enters a **long position** with a user-defined order size (default 0.01 BTC).

3. **Exit Conditions**:

- **Take Profit**: Closes the position when the profit target is reached (default $100).

- **Stop Loss**: Closes the position when the price drops below the stop loss level (default $50).

- **Bearish Crossunder**: Closes the position when the Fast EMA crosses below the Slow EMA.

4. **Visual Signals**:

- **BUY signals**: Displayed when a bullish crossover occurs.

- **SELL signals**: Displayed when a bearish crossunder occurs.

This strategy is optimized for trend-following behavior, ensuring positions are aligned with upward-moving trends while managing risk through clear stop-loss and take-profit levels.

Swing High/Low Pivots Strategy [LV]The Swing High/Low Pivots Strategy was developed as a counter-momentum trading tool.

The strategy is suitable for any market and the default values used in the input settings menu are set for Bitcoin (best on 15min). These values, expressed in minimum ticks (or pips if symbol is Forex) make this tool perfectly adaptable to every symbol and/or timeframe.

Check tooltips in the settings menu for more details about every user input.

STRTEGY ENTRY & EXIT MECHANISMS:

Trades Entry based on the detection of swing highs and lows for short and long entries respectively, validated by:

- Limit orders placed after each new pivot level confirmation

- Moving averages trend filter (if enabled)

- No active trade currently open

Trades Exit when the price reaches take-profit or stop-loss level as defined in the settings menu. A double entry/second take-profit level can be enabled for partial exits, with dynamic stop-loss adjustment for the remaining position.

Enhanced Trade Precision:

By limiting entries to confirmed swing high (HH, LH) or swing low (HL, LL) pivot points, the strategy ensures that trades occur at levels of significant price reversals. This precision reduces the likelihood of entering trades in the midst of a trend or during uncertain price action.

Risk Management Optimization:

The strategy incorporates clearly defined stop-loss (SL) and take-profit (TP) levels derived from the pivot points. This structured approach minimizes potential losses while locking in profits, which is critical for consistent performance in volatile markets.

Trend Filtering for Better Entry:

The use of a configurable moving average filter adds a layer of trend validation. This prevents entering trades against the dominant market trend, increasing the probability of success for each trade.

Avoidance of Noise:

The lookback period (length parameter) confirms pivots only after a set number of bars, effectively filtering out market noise and ensuring that entries are based on reliable, well-defined price movements.

Adaptability Across Markets:

The strategy is versatile and can be applied across different markets (Forex, stocks, crypto) due to its dynamic use of ticks and pips converters. It adapts seamlessly to varying price scales and asset types.

Dual Quantity Entries:

The original and optionnal double-entry mechanism allows traders to capture both short-term and extended profits by scaling out of positions. This adaptive approach caters to varying risk appetites and market conditions.

Clear Visualization:

The plotted pivot points, entry limits, SL, and TP levels provide visual clarity, making it easy for traders to track the strategy's behavior and make informed decisions.

Automated Execution with Alerts:

Integrated alerts for both entries and exits ensure timely actions without the need for constant market monitoring, enhancing efficiency. Configurable alert messages are suitable for API use.

Any feedback, comments, or suggestions for improvement are always welcome.

Hope you enjoy!

IU EMA Channel StrategyIU EMA Channel Strategy

Overview:

The IU EMA Channel Strategy is a simple yet effective trend-following strategy that uses two Exponential Moving Averages (EMAs) based on the high and low prices. It provides clear entry and exit signals by identifying price crossovers relative to the EMAs while incorporating a built-in Risk-to-Reward Ratio (RTR) for effective risk management.

Inputs ( Settings ):

- RTR (Risk-to-Reward Ratio): Define the ratio for risk-to-reward (default = 2).

- EMA Length: Adjust the length of the EMA channels (default = 100).

How the Strategy Works

1. EMA Channels:

- High-based EMA: EMA calculated on the high price.

- Low-based EMA: EMA calculated on the low price.

The area between these two EMAs creates a "channel" that visually highlights potential support and resistance zones.

2. Entry Rules:

- Long Entry: When the price closes above the high-based EMA (crossover).

- Short Entry: When the price closes below the low-based EMA (crossunder).

These entries ensure trades are taken in the direction of momentum.

3. Stop Loss (SL) and Take Profit (TP):

- Stop Loss:

- For long positions, the SL is set at the previous bar's low.

- For short positions, the SL is set at the previous bar's high.

- Take Profit:

- TP is automatically calculated using the Risk-to-Reward Ratio (RTR) you define.

- Example: If RTR = 2, the TP will be 2x the risk distance.

4. Exit Rules:

- Positions are closed at either the stop loss or the take profit level.

- The strategy manages exits automatically to enforce disciplined risk management.

Visual Features

1. EMA Channels:

- The high and low EMAs are dynamically color-coded:

- Green: Price is above the EMA (bullish condition).

- Red: Price is below the EMA (bearish condition).

- The area between the EMAs is shaded for better visual clarity.

2. Stop Loss and Take Profit Zones:

- SL and TP levels are plotted for both long and short positions.

- Zones are filled with:

- Red: Stop Loss area.

- Green: Take Profit area.

Be sure to manage your risk and position size properly.

DAILY Supertrend + EMA Crossover with RSI FilterThis strategy is a technical trading approach that combines multiple indicators—Supertrend, Exponential Moving Averages (EMAs), and the Relative Strength Index (RSI)—to identify and manage trades.

Core Components:

1. Exponential Moving Averages (EMAs):

Two EMAs, one with a shorter period (fast) and one with a longer period (slow), are calculated. The idea is to spot when the faster EMA crosses above or below the slower EMA. A fast EMA crossing above the slow EMA often suggests upward momentum, while crossing below suggests downward momentum.

2. Supertrend Indicator:

The Supertrend uses Average True Range (ATR) to establish dynamic support and resistance lines. These lines shift above or below price depending on the prevailing trend. When price is above the Supertrend line, the trend is considered bullish; when below, it’s considered bearish. This helps ensure that the strategy trades only in the direction of the overall trend rather than against it.

3. RSI Filter:

The RSI measures momentum. It helps avoid buying into markets that are already overbought or selling into markets that are oversold. For example, when going long (buying), the strategy only proceeds if the RSI is not too high, and when going short (selling), it only proceeds if the RSI is not too low. This filter is meant to improve the quality of the trades by reducing the chance of entering right before a reversal.

4. Time Filters:

The strategy only triggers entries during user-specified date and time ranges. This is useful if one wants to limit trading activity to certain trading sessions or periods with higher market liquidity.

5. Risk Management via ATR-based Stops and Targets:

Both stop loss and take profit levels are set as multiples of the ATR. ATR measures volatility, so when volatility is higher, both stops and profit targets adjust to give the trade more breathing room. Conversely, when volatility is low, stops and targets tighten. This dynamic approach helps maintain consistent risk management regardless of market conditions.

Overall Logic Flow:

- First, the market conditions are analyzed through EMAs, Supertrend, and RSI.

- When a buy (long) condition is met—meaning the fast EMA crosses above the slow EMA, the trend is bullish according to Supertrend, and RSI is below the specified “overbought” threshold—the strategy initiates or adds to a long position.

- Similarly, when a sell (short) condition is met—meaning the fast EMA crosses below the slow EMA, the trend is bearish, and RSI is above the specified “oversold” threshold—it initiates or adds to a short position.

- Each position is protected by an automatically calculated stop loss and a take profit level based on ATR multiples.

Intended Result:

By blending trend detection, momentum filtering, and volatility-adjusted risk management, the strategy aims to capture moves in the primary trend direction while avoiding entries at excessively stretched prices. Allowing multiple entries can potentially amplify gains in strong trends but also increases exposure, which traders should consider in their risk management approach.

In essence, this strategy tries to ride established trends as indicated by the Supertrend and EMAs, filter out poor-quality entries using RSI, and dynamically manage trade risk through ATR-based stops and targets.