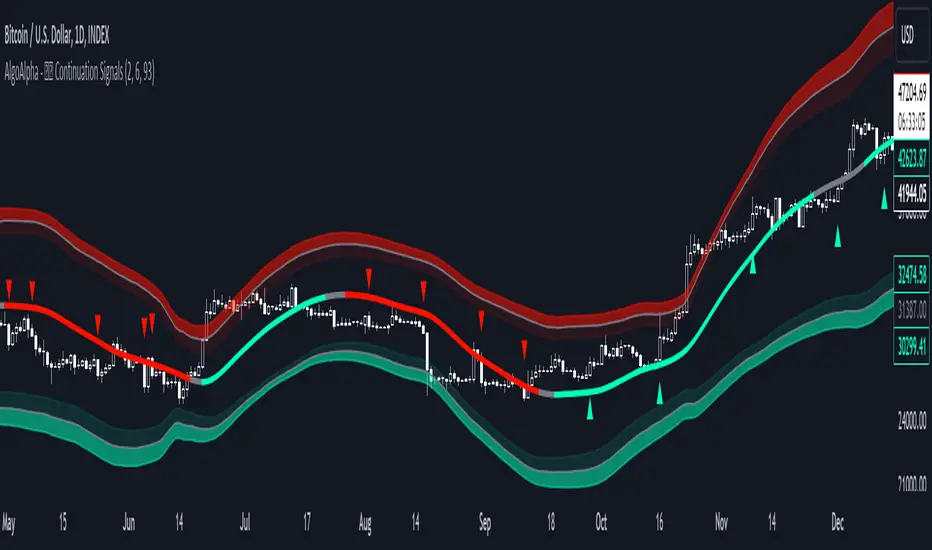

Trend Continuation Signals [AlgoAlpha]Introducing the Trend Continuation Signals by AlgoAlpha 🌟🚀

Elevate your trading game with this multipurpose indicator, designed to pinpoint trend continuation opportunities as well as highlight volatility and oversold/overbought conditions. Whether you're a trading novice or a seasoned market veteran, this tool offers intuitive visual cues to boost your decision-making and enhance your market analysis. Let's explore the key features, how to use it effectively, and delve into the operational mechanics that make this tool a game-changer in your trading arsenal:

Key Features:

🔥 Advanced Trend Detection : Leverages the Hull Moving Average (HMA) for superior trend tracking as compared to other MAs, offering unique insights into market momentum.

🌈 Volatility Bands : Implements adjustable bands around the trend line, which evolve with market conditions to highlight potential trading opportunities.

⚡ Trend Continuation Signals : Identifies bullish and bearish continuation signals, equipping you with actionable signals to exploit the prevailing market trend.

🎨 Intuitive Color Coding : Employs a vibrant color scheme to distinguish between uptrends, downtrends, and neutral phases, facilitating easy interpretation of the indicator's insights.

🛠 How to Use "Trend Continuation Signals ":

🔍 Setting Up : Incorporate the indicator onto your chart and customize the indicator to suite your preferences.

👀 Reading the Signals : Pay attention to the color-coded trend lines and volatility bands. Green indicates an uptrend, red signifies a downtrend, and gray denotes a neutral market condition.

📈 Identifying Entry Points : Look for bullish (▲) and bearish (▼) continuation icons below or above the price bars as signals for potential entry points for long or short positions, respectively.

🔄 Confirmation : Validate your trades with further analysis or other indicators. The Trend Continuation Signals are most effective when complemented by other technical analysis tools or fundamental insights.

📉 Risk Management : Implement stop-loss orders in line with your risk appetite and adjust them based on the volatility bands provided by the indicator to safeguard your investments.

How It Operates:

The essence of the indicator is captured through the hull moving averages for both the primary and secondary lines, set at periods of 93 and 50, respectively, to reflect market trends and pullbacks that trigger the continuation signals every time price recovers from a detected pullback.

Volatility is quantified through the standard deviation of the midline, magnified by a factor, establishing the upper and lower trend band boundaries.

Further volatility bands are plotted around the main volatility band, providing a granular view of market volatility and potential breakout or breakdown zones.

Market trend direction is determined by comparing the HMA line's current position to its previous value, enhanced by the secondary line to identify continuation patterns.

Embrace the power of the Trend Continuation Signals to enhance your trading strategy! It is important to note that all indicators are best used in confluence with other forms of analysis, happy trading! 📊💥

Meanreversion

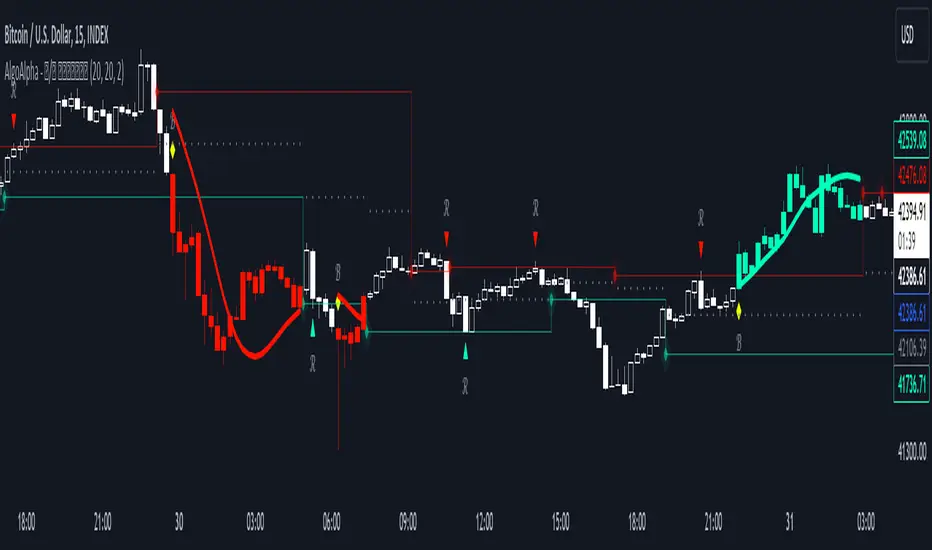

Reversal and Breakout Signals [AlgoAlpha]🚀🌟 Introducing the Reversal and Breakout Signals by AlgoAlpha 🌟🚀

This innovative tool is crafted to enhance your chart analysis by identifying potential reversal and breakout opportunities directly on your charts. It's designed with both novice and experienced traders in mind, providing intuitive visual cues for better decision-making. Let's dive into the key features and how it operates:

### Key Features:

🔶 Dynamic Period Settings: Customize the sensitivity of the indicator with user-defined periods for both the indicator and volume strength.

📊 Volume Threshold: Set a threshold to define what constitutes strong volume, enabling the identification of significant market movements.

💡 Trend Coloring: Option to color candles during trends, making it easier to visualize bullish and bearish market conditions.

🌈 Customizable Visuals: Choose your preferred colors for bullish, bearish, and breakout signals, personalizing the chart to your liking.

🚨 Advanced Alert System: Configure alerts for reversal and breakout signals, ensuring you never miss a potential trading opportunity.

### How to Use:

To maximize the effectiveness of the Reversal and Breakout Signals tool, follow these steps:

1. 🔧 Set Up Your Preferences:

- Adjust the Indicator Period and Volume Strength Period to match the timeframe of your trading strategy. This fine-tuning allows the indicator to better align with your specific market analysis needs.

- Define the Strong Volume Threshold to distinguish between ordinary and significant volume movements. This helps in identifying breakout or reversal signals with higher confidence.

2. 🎨 Customize Visuals:

- Choose colors for Bullish , Bearish , and Breakout Signals to visually differentiate between different types of market activities. This customization facilitates quicker decision-making while scanning charts.

3. 🔍 Reversal Signals:

- Bullish Reversal : Look for a triangle below the bar indicating a potential upward movement. It's identified when the price dips below the lower level but closes above it, suggesting a rejection of lower prices.

- Bearish Reversal : A triangle above the bar signals a potential downward movement. This occurs when the price spikes above the upper level but closes below, indicating a rejection of higher prices.

4. 📈 Trend and Breakout Signals:

- Diamonds represent breakout signals. A bullish breakout is marked below the bar when the price closes above the upper level, suggesting strong buying pressure. Conversely, a bearish breakout above the bar indicates strong selling pressure as the price closes below the lower level.

- The tool also features a Trend Tracker that highlights the current market trend using the Hull Moving Average (HMA). This can help you stay aligned with the overall market direction for your trades.

By integrating these steps into your trading strategy, the Reversal and Breakout Signals tool can provide actionable insights to help identify potential entry and exit points, enhancing your trading decisions with visual cues and alerts for market reversals and breakouts.

### How It Works:

The core logic revolves around calculating weighted moving averages of high and low prices over a user-defined period, identifying the highest and lowest points within this period to establish potential breakout or breakdown levels while reducing the amount of noise, hence the use of moving averages.

1. Weighted Moving Averages Calculation:

sh = ta.wma(high, len)

sl = ta.wma(low, len)

h = ta.highest(sh, len)

l = ta.lowest(sl, len)

2. Breakout and Reversal Detection:

The script then employs logic to detect bullish and bearish breakouts and reversals based on the closing price's position relative to these levels, combined with volume analysis to confirm the strength of the move.

if not (h < h or h > h )

hstore := h

if not (l < l or l > l )

lstore := l

bullishbreakout := (breakout or ((breakout or breakout or breakout or breakout ) and candledir == 1)) and strongvol and not (bullishbreakout or bullishbreakout or bullishbreakout )

bearishbreakout := (breakdown or ((breakdown or breakdown or breakdown or breakdown ) and candledir == -1)) and strongvol and not (bearishbreakout or bearishbreakout or bearishbreakout )

3. Visual Indicators and Alerts:

Visual cues such as triangle shapes for reversals and diamonds for breakouts, along with colored bars, make it easy to spot these opportunities. Additionally, alerts can be set up for these events, ensuring traders can react promptly to potential trading setups.

plotshape(bullishrej and not (state ==- 1) ? low * 0.9995 : na, " Bullish Reversal ", shape.triangleup, location.belowbar, color.new(green, 0), size = size.tiny, text = "𝓡", textcolor = color.gray)

plotshape(bearishrej and not (state == 1) ? high * 1.0005 : na, " Bearish Reversal ", shape.triangledown, location.abovebar, color.new(red, 0), size = size.tiny, text = "𝓡", textcolor = color.gray)

plotshape(bullishbreakout ? low * 0.999 : na, " Bullish Breakout ", shape.diamond, location.belowbar, color.new(yellow, 0), size = size.tiny, text = "𝓑", textcolor = color.gray)

plotshape(bearishbreakout ? high * 1.001 : na, " Bearish Breakout ", shape.diamond, location.abovebar, color.new(yellow, 0), size = size.tiny, text = "𝓑", textcolor = color.gray)

This script is a versatile tool designed to aid in the identification of key reversal and breakout points, helping traders to make informed decisions based on technical analysis. Its customization options allow for a tailored analysis experience, fitting the unique needs and strategies of each trader.

MVRV Z-Score [AlgoAlpha]Introducing the ∑ MVRV Z-Score by AlgoAlpha, a dynamic and sophisticated tool designed for traders seeking to gain an edge in INDEX:BTCUSD analysis. This script employs advanced statistical techniques on Bitcoin On-Chain data to offer a deeper understanding of market conditions, focusing on valuation extremes and momentum trends. Let's explore the features and functionalities that make this tool a valuable addition to your trading arsenal.

Key Features:

🔶 Adjustable Parameters: Customize the Z score lookback length, moving average lookback length, and choose from six moving average types, tailoring the analysis to your trading style.

🔶 Heiken Ashi Compatibility: Incorporate Heiken Ashi plots to visualize market trends, adding a layer of clarity to your technical analysis.

🔶 Divergence Alerts: Detect significant bullish and bearish divergences, allowing for timely identification of potential market reversals.

🔶 Configurable Alerts: Set alerts for overbought, oversold, and divergence conditions, ensuring you never miss an opportunity.

How to Use:

1. ➡️ Parameter Selection: Start by configuring the Z-Score and moving average settings according to your analysis needs. This includes selecting the lookback period and the type of moving average.

2. ➡️ Visualization Options: Choose to enable Heiken Ashi plots for an alternative view of the Z-Score, which can help in identifying trend directions more clearly.

3. ➡️ Monitor for Signals: Keep an eye out for divergence signals and overbought/oversold conditions as potential indicators for entering or exiting trades.

4. ➡️ Alert Setup: Configure alerts based on your selected parameters to receive notifications for important market movements and conditions.

How It Works:

The core of this tool is the Z-Score calculation, which assesses the standard deviation of the current market value from its mean, highlighting overvalued or undervalued market conditions. Here's a brief overview of the script's operational mechanics:

1. 📊 Calculating the Z-Score: The script first calculates the mean over a user-defined lookback period of the MVRV ratio, then it computes the Z-Score to identify deviations from the average.

meanValue = ta.sma(marketValue, zScoreLookback)

zScoreValue = (marketValue - meanValue) / ta.stdev(marketValue, zScoreLookback)

2. 📈 Applying a Moving Average: To smooth the Z-Score data and make trends more discernible, a moving average is applied. Users can choose from several types, such as SMA, EMA, or HMA, based on their preference.

3. 🔄 Heiken Ashi Visualization: For those opting for a more intuitive trend analysis, Heiken Ashi plots can be enabled, transforming the Z-Score data into candlestick charts that simplify trend identification.

4. 🔍 Identifying Divergences: The script is equipped to spot divergences between the market price action and the Z-Score, signaling potential bullish or bearish market reversals.

oscHigherLow = haClose > ta.valuewhen(findPivotLow, haClose , 1) and isInRange(findPivotLow )

priceLowerLow = low < ta.valuewhen(findPivotLow, low , 1)

bullishCondition = enablePlotBullish and priceLowerLow and oscHigherLow and findPivotLow

5. 🚨 Configurable Alerts: Lastly, the script allows for the setting of customizable alerts based on the Z-Score, moving averages, and identified divergences, enabling traders to react promptly to market changes.

The ∑ MVRV Z-Score by AlgoAlpha is an essential tool for traders looking to analyze and interpret market dynamics through a quantitatively rigorous lens. Whether you're focused on identifying market extremes or tracking trend momentum, this script offers the insights needed to support informed trading decisions. 🌟📊💡

SuperTrend Fisher [AlgoAlpha]🚀🌟 Introducing the "Super Fisher" by AlgoAlpha, a sophisticated and versatile tool crafted for the discerning trader. This innovative indicator merges the precision of the Fisher Transform with the adaptability of the SuperTrend methodology, offering a fresh perspective on market analysis. 📈🔍

Key Features:

🔶 Customizable Settings: Tailor the indicator to your trading style with adjustable inputs like "Fair-value Period" and "EMA Length". Choose your preferred "Up Color" and "Down Color" for a personalized visual experience.

🔶 Advanced Fisher Transform: At the heart of this tool is the Fisher Transform, an algorithm renowned for pinpointing potential price reversals by normalizing asset prices.

🔶 Integrated SuperTrend Functionality: This feature adds a layer of trend analysis, using the refined Fisher Transform values to generate dynamic, trend-following signals.

🔶 Enhanced Visualization: Clearly distinguishable bullish and bearish market phases, thanks to the color-coded plots of Fisher Transform and SuperTrend values.

🔶 Overbought/Oversold Levels: Visual plots and fills for these levels provide additional insights into market extremities.

🔶 Configurable Alerts: Stay informed with alerts for critical market movements like crossing the zero line or the SuperTrend.

Logic:

The "Super Fisher" operates on a sophisticated algorithm:

1. Fisher Transform Calculation: It starts by calculating the Detrended Price Oscillator (DPO) and its standard deviation. These values are then transformed using the Fisher Transform formula, which is subsequently smoothed with a Hull Moving Average.

2. SuperTrend Integration: The SuperTrend function employs the Fisher Transform values to create a dynamic trend-following tool. It calculates upper and lower bands and determines which one to use for market direction based on whether the fisher is above or below the bands, offering an insightful view of the price trend.

3. Overbought/Oversold Identification: The tool plots specific levels to indicate overbought and oversold conditions, aiding in the identification of potential reversal points.

Here's a closer look at the core calculations:

Calculates the Fisher Transform:

value = 0.0

value := round_(.66 * ((src - low_) / (high_ - low_) - .5) + .67 * nz(value ))

fish1 = 0.0

fish1 := .5 * math.log((1 + value) / (1 - value)) + .5 * nz(fish1 )

fish1 := ta.hma(fish1, l)

Calculates the SuperTrend:

supertrend(factor, atrPeriod, srcc) =>

src = srcc

atr = atrr(srcc, atrPeriod)

upperBand = src + factor * atr

lowerBand = src - factor * atr

prevLowerBand = nz(lowerBand )

prevUpperBand = nz(upperBand )

lowerBand := lowerBand > prevLowerBand or srcc < prevLowerBand ? lowerBand : prevLowerBand

upperBand := upperBand < prevUpperBand or srcc > prevUpperBand ? upperBand : prevUpperBand

int direction = na

float superTrend = na

prevSuperTrend = superTrend

if na(atr )

direction := 1

else if prevSuperTrend == prevUpperBand

direction := srcc > upperBand ? -1 : 1

else

direction := srcc < lowerBand ? 1 : -1

superTrend := direction == -1 ? lowerBand : upperBand

How to Use:

📊 To maximize the potential of the "Super Fisher", follow these steps:

1. Customize Settings: Adjust the inputs to match your trading preferences. This includes setting the periods for the Fisher Transform and SuperTrend, as well as choosing colors for better visualization.

2. Analyze the Market: Observe the Fisher Transform and SuperTrend plots to gauge market direction. Pay special attention to color changes, as they indicate shifts in market sentiment.

3. Identify Extremes: Use the overbought and oversold plots to understand potential reversal points.

4. Set Alerts: Utilize the alert functionality to stay informed about significant market movements, ensuring you never miss an opportunity.

🔥 In summary the "Super Fisher" is a comprehensive market analysis tool designed to enhance your trading insights and decision-making process. 📉🌟🚨

TanHef RanksTanHef Ranks: A numeric compass to market tops and bottoms.

█ Simple Explanation:

This indicator is designed to signal 'buy low and sell high' opportunities through numerical rankings, where larger numbers represent stronger signals. These numbered rankings are negative for potential ‘buy’ opportunities and positive for possible ‘sell’ moments.

█ Understanding Numerical Rankings:

The numerical rankings (from +18 to -18) identify and take advantage of market tendencies of prices reverting back to their historical average, also known as mean reversion. It operates on a simple principle: smaller values signal a potential for short-term mean reversion, while larger values suggest a probable shift in both short and long-term mean reversion. These values are derived from a careful analysis of both short and long-term mean reversions, providing traders with a nuanced understanding of market movements.

█ Analyzing Numeric Ranking Extremes:

The historical occurrences of numeric rankings are recorded into a table to help identify the previous extreme rankings (for example anything -10/+10 is considered extreme), which historically signal key turning points in market movements. The previously extreme rankings offer insights into potential end-of trend scenarios or trend reversals, thereby attempting to make high-probability trading decisions.

█ Risk Management Integration:

This indicator combined with disciplined risk management, offers a more secure trading approach. Applying a stop-loss near lows after entries on the oversold side (negative rankings) protects from large losses. Additionally, once prices reach overbought territories (positive rankings) applying a tight stop-loss helps to lock in profits while continuing exposure to the aggressive upwards momentum.

█ Calculation Methodology:

The indicator evaluates market momentum by analyzing upward and downward movements. It does this by referencing the 10 'length' input parameters, where 'length' refers to the number of price bars referenced. Each 'length' increases in value to analyze trends from short to long-term. A numerical rank is given when these trends align, with higher ranks requiring agreement across both short and longer-term lengths. This alignment across different time periods helps to ensure the indicator's signals are robust.

█ Indicator Stability (No Repainting):

When a price bar closes, its associated ranking is fixed and remains unchanged (some other indicators repaint, which means signals can change after a bar closes). While a price bar is open, its numeric ranking may increase in absolute value but never decrease towards zero, ensuring further stability. This stability and consistency is crucial for reliable back-testing and real-time analysis. Notably, in the highly improbable scenario where a ranking may exhibit both a positive and negative value simultaneously during extreme volatility, both the positive and negative numeric ranking is displayed.

█ Practical Application:

Pro Tip: Use at a minimum -4/+4 rank as potential basic buy/sell signals. Higher absolute numeric rankings are ideal as they indicate stronger reversal potential due to higher rankings identifying longer period reversals.

Entry Scenario: Refer to the chart below. The -9 ranking (3 occurrences in the table) indicates potential oversold conditions, suggesting a buy. Add a stop-loss near recent lows to protect against losses.

Exit Scenario: Refer to the chart below. The +7 ranking (6 occurrences in the table) indicates potential overbought conditions, suggesting a sell. Place a stop-loss to protect profits and remain exposed to further gains.

█ Indicator Settings:

Additional Timeframe: Allows users to include an extra timeframe's data in the analysis for more nuanced insights.

Lengths: Defines the periods over which the indicator calculates its rankings, affecting the sensitivity and time horizon of the signals.

Max Number Calculated: Sets the upper limit for the numerical rankings the indicator can output, tuning the extremity of the signals it identifies. (Reducing improves indicator load time)

Visual Styling (Current Timeframe): Customizes the appearance of the indicator's output on the chart for the selected timeframe, enhancing visibility and readability.

Table Settings: Adjusts the display properties of the table that lists numerical rankings, including its visibility, location, and size on the chart.

Indicator Display Type: Selects the mode in which the indicator presents its data, either overlaying the main chart or in a separate pane as an oscillator.

Alerts: Configures the conditions and frequency at which the indicator will trigger trading alerts, based on the numeric rankings and user-defined parameters.

█ How To Access:

You can see the Author's Instructions below to get access.

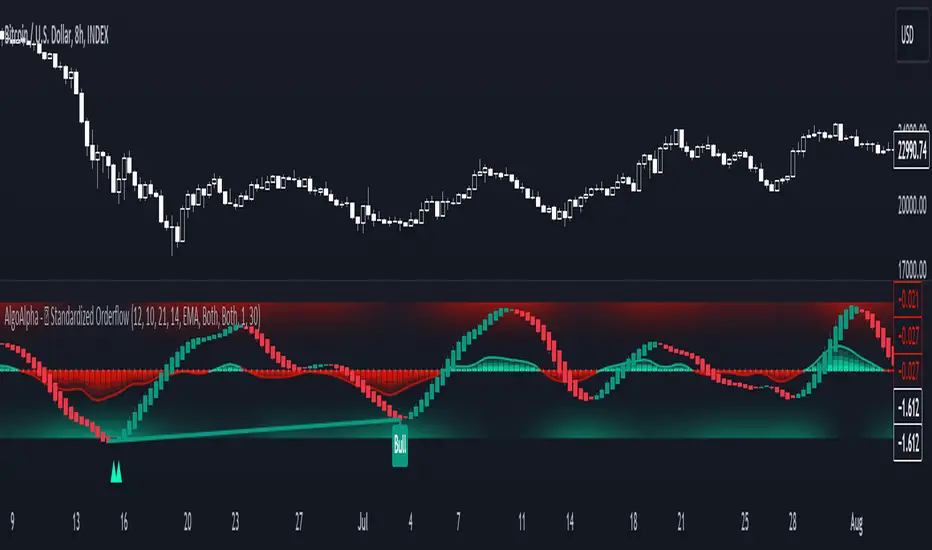

Standardized Orderflow [AlgoAlpha]Introducing the Standardized Orderflow indicator by AlgoAlpha. This innovative tool is designed to enhance your trading strategy by providing a detailed analysis of order flow and velocity. Perfect for traders who seek a deeper insight into market dynamics, it's packed with features that cater to various trading styles. 🚀📊

Key Features:

📈 Order Flow Analysis: At its core, the indicator analyzes order flow, distinguishing between bullish and bearish volume within a specified period. It uses a unique standard deviation calculation for normalization, offering a clear view of market sentiment.

🔄 Smoothing Options: Users can opt for a smoothed representation of order flow, using a Hull Moving Average (HMA) for a more refined analysis.

🌪️ Velocity Tracking: The indicator tracks the velocity of order flow changes, providing insights into the market's momentum.

🎨 Customizable Display: Tailor the display mode to focus on either order flow, order velocity, or both, depending on your analysis needs.

🔔 Alerts for Critical Events: Set up alerts for crucial market events like crossover/crossunder of the zero line and overbought/oversold conditions.

How to Use:

1. Setup: Easily configure the indicator to match your trading strategy with customizable input parameters such as order flow period, smoothing length, and moving average types.

2. Interpretation: Watch for bullish and bearish columns in the order flow chart, utilize the Heiken Ashi RSI candle calculation, and look our for reversal notations for additional market insights.

3. Alerts: Stay informed with real-time alerts for key market events.

Code Explanation:

- Order Flow Calculation:

The core of the indicator is the calculation of order flow, which is the sum of volumes for bullish or bearish price movements. This is followed by normalization using standard deviation.

orderFlow = math.sum(close > close ? volume : (close < close ? -volume : 0), orderFlowWindow)

orderFlow := useSmoothing ? ta.hma(orderFlow, smoothingLength) : orderFlow

stdDev = ta.stdev(orderFlow, 45) * 1

normalizedOrderFlow = orderFlow/(stdDev + stdDev)

- Velocity Calculation:

The velocity of order flow changes is calculated using moving averages, providing a dynamic view of market momentum.

velocityDiff = ma((normalizedOrderFlow - ma(normalizedOrderFlow, velocitySignalLength, maTypeInput)) * 10, velocityCalcLength, maTypeInput)

- Display Options:

Users can choose their preferred display mode, focusing on either order flow, order velocity, or both.

orderFlowDisplayCond = displayMode != "Order Velocity" ? display.all : display.none

wideDisplayCond = displayMode != "Order Flow" ? display.all : display.none

- Reversal Indicators and Divergences:

The indicator also includes plots for potential bullish and bearish reversals, as well as regular and hidden divergences, adding depth to your market analysis.

bullishReversalCond = reversalType == "Order Flow" ? ta.crossover(normalizedOrderFlow, -1.5) : (reversalType == "Order Velocity" ? ta.crossover(velocityDiff, -4) : (ta.crossover(velocityDiff, -4) or ta.crossover(normalizedOrderFlow, -1.5)) )

bearishReversalCond = reversalType == "Order Flow" ? ta.crossunder(normalizedOrderFlow, 1.5) : (reversalType == "Order Velocity" ? ta.crossunder(velocityDiff, 4) : (ta.crossunder(velocityDiff, 4) or ta.crossunder(normalizedOrderFlow, 1.5)) )

In summary, the Standardized Orderflow indicator by AlgoAlpha is a versatile tool for traders aiming to enhance their market analysis. Whether you're focused on short-term momentum or long-term trends, this indicator provides valuable insights into market dynamics. 🌟📉📈

Standardized Median Proximity [AlgoAlpha]Introducing the Standardized Median Proximity by AlgoAlpha 🚀📊 – a dynamic tool designed to enhance your trading strategy by analyzing price fluctuations relative to the median value. This indicator is built to provide clear visual cues on the price deviation from its median, allowing for a nuanced understanding of market trends and potential reversals.

🔍 Key Features:

1. 📈 Median Tracking: At the core of this indicator is the calculation of the median price over a specified lookback period. By evaluating the current price against this median, the indicator provides a sense of whether the price is trending above or below its recent median value.

medianValue = ta.median(priceSource, lookbackLength)

2. 🌡️ Normalization of Price Deviation: The deviation of the price from the median is normalized using standard deviation, ensuring that the indicator's readings are consistent and comparable across different time frames and instruments.

standardDeviation = ta.stdev(priceDeviation, 45)

normalizedValue = priceDeviation / (standardDeviation + standardDeviation)

3. 📌 Boundary Calculations: The indicator sets upper and lower boundaries based on the normalized values, helping to identify overbought and oversold conditions.

upperBoundary = ta.ema(positiveValues, lookbackLength) + ta.stdev(positiveValues, lookbackLength) * stdDevMultiplier

lowerBoundary = ta.ema(negativeValues, lookbackLength) - ta.stdev(negativeValues, lookbackLength) * stdDevMultiplier

4. 🎨 Visual Appeal and Clarity: With carefully chosen colors, the plots provide an intuitive and clear representation of market states. Rising trends are indicated in a shade of green, while falling trends are shown in red.

5. 🚨 Alert Conditions: Stay ahead of market movements with customizable alerts for trend shifts and impulse signals, enabling timely decisions.

alertcondition(ta.crossover(normalizedValue, 0), "Bullish Trend Shift", "Median Proximity Crossover Zero Line")

🔧 How to Use:

- 🎯 Set your preferred lookback lengths and standard deviation multipliers to tailor the indicator to your trading style.

- 💹 Utilize the boundary plots to understand potential overbought or oversold conditions.

- 📈 Analyze the color-coded column plots for quick insights into the market's direction relative to the median.

- ⏰ Set alerts to notify you of significant trend changes or conditions that match your trading criteria.

Basic Logic Explained:

- The indicator first calculates the median of the selected price source over your chosen lookback period. This median serves as a baseline for measuring price deviation.

- It then standardizes this deviation by dividing it by the standard deviation of the price deviation over a 45-period lookback, creating a normalized value.

- Upper and lower boundaries are computed using the exponential moving average (EMA) and standard deviation of these normalized values, adjusted by your selected multiplier.

- Finally, color-coded plots provide a visual representation of these calculations, offering at-a-glance insights into market conditions.

Remember, while this tool offers valuable insights, it's crucial to use it as part of a comprehensive trading strategy, complemented by other analysis and indicators. Happy trading!

🚀

Volume-Trend Sentiment (VTS) [AlgoAlpha]Introducing the Volume-Trend Sentiment by AlgoAlpha, a unique tool designed for traders who seek a deeper understanding of market sentiment through volume analysis. This innovative indicator offers a comprehensive view of market dynamics, blending volume trends with price action to provide an insightful perspective on market sentiment. 🚀📊

Key Features:

1. 🌟 Dual Trend Analysis: This indicator combines the concepts of price movement and volume, offering a multi-dimensional view of market sentiment. By analyzing the relationship between the closing and opening prices relative to volume, it provides a nuanced understanding of market dynamics.

2. 🎨 Customizable Settings: Flexibility is at the core of this indicator. Users can adjust various parameters such as the length of the volume trend, standard deviation, and SMA length, ensuring a tailored experience to match individual trading strategies.

3. 🌈 Visual Appeal: With options to display noise, the main plot, and background colors, the indicator is not only informative but also visually engaging. Users can choose their preferred colors for up and down movements, making the analysis more intuitive.

4. ⚠️ Alerts for Key Movements: Stay ahead of market changes with built-in alert conditions. These alerts notify traders when the Volume-Trend Sentiment crosses above or below the midline, signaling potential shifts in market momentum.

How It Works:

The core of the indicator is the calculation of the Volume-Trend Sentiment (VTS). It is computed by subtracting a double-smoothed Exponential Moving Average (EMA) of the price-volume ratio from a single EMA of the same ratio. This method highlights the trend in volume relative to price changes.

volumeTrend = ta.ema((close - open) / volume, volumeTrendLength) - ta.ema(ta.ema((close - open) / volume, volumeTrendLength), volumeTrendLength)

To manage volatility and noise in the volume trend, the indicator employs a standard deviation calculation and a Simple Moving Average (SMA). This smoothing process helps in identifying the true underlying trend by filtering out extreme fluctuations.

standardDeviation = ta.stdev(volumeTrend, standardDeviationLength) * 1

smoothedVolumeTrend = ta.sma(volumeTrend / (standardDeviation + standardDeviation), smaLength)

A unique feature is the dynamic background color, which changes based on the sentiment level. This visual cue instantly communicates the market's bullish or bearish sentiment, enhancing the decision-making process.

getColor(volumeTrendValue) =>

sentimentLevel = math.abs(volumeTrendValue * 10)

baseTransparency = 60 // Base transparency level

colorTransparency = math.max(90 - sentimentLevel * 5, baseTransparency)

volumeTrendValue > 0 ? color.new(upColor, colorTransparency) : color.new(downColor, colorTransparency)

bgcolor(showBackgroundColor ? getColor(smoothedVolumeTrend) : na)

In summary, the Volume-Trend Sentiment by AlgoAlpha is a comprehensive tool that enhances market analysis through a unique blend of volume and price trends. Whether you're a seasoned trader or just starting out, this indicator offers valuable insights into market sentiment and helps in making informed trading decisions. 📈📉🔍🌐

Median Proximity Percentile [AlgoAlpha]📊🚀 Introducing the "Median Proximity Percentile" by AlgoAlpha, a dynamic and sophisticated trading indicator designed to enhance your market analysis! This tool efficiently tracks median price proximity over a specified lookback period and finds it's percentile between 2 dynamic standard deviation bands, offering valuable insights for traders looking to make informed decisions.

🌟 Key Features:

Color-Coded Visuals: Easily interpret market trends with color-coded plots indicating bullish or bearish signals.

Flexibility: Customize the indicator with your preferred price source and lookback lengths to suit your trading strategy.

Advanced Alert System: Stay ahead with customizable alerts for key trend shifts and market conditions.

🔍 Deep Dive into the Code:

Choose your preferred price data source and define lookback lengths for median and EMA calculations. priceSource = input.source(close, "Source") and lookbackLength = input.int(21, minval = 1, title = "Lookback Length")

Calculate median value, price deviation, and normalized value to analyze market position relative to the median. medianValue = ta.median(priceSource, lookbackLength)

Determine upper and lower boundaries based on standard deviation and EMA. upperBoundary = ta.ema(positiveValues, lookbackLength) + ta.stdev(positiveValues, lookbackLength) * stdDevMultiplier

lowerBoundary = ta.ema(negativeValues, lookbackLength) - ta.stdev(negativeValues, lookbackLength) * stdDevMultiplier

Compute the percentile value to track market position within these boundaries. percentileValue = 100 * (normalizedValue - lowerBoundary)/(upperBoundary - lowerBoundary) - 50

Enhance your analysis with Hull Moving Average (HMA) for smoother trend identification. emaValue = ta.hma(percentileValue, emaLookbackLength)

Visualize trends with color-coded plots and characters for easy interpretation. plotColor = percentileValue > 0 ? colorUp : percentileValue < 0 ? colorDown : na

Set up advanced alerts to stay informed about significant market movements. // Alerts

alertcondition(ta.crossover(emaValue, 0), "Bullish Trend Shift", "Median Proximity Percentile Crossover Zero Line")

alertcondition(ta.crossunder(emaValue, 0), "Bearish Trend Shift", "Median Proximity Percentile Crossunder Zero Line")

alertcondition(ta.crossunder(emaValue,emaValue ) and emaValue > 90, "Bearish Reversal", "Median Proximity Percentile Bearish Reversal")

alertcondition(ta.crossunder(emaValue ,emaValue) and emaValue < -90, "Bullish Reversal", "Median Proximity Percentile Bullish Reversal")

🚨 Remember, the "Median Proximity Percentile " is a tool to aid your analysis. It’s essential to combine it with other analysis techniques and market understanding for best results. Happy trading! 📈📉

Momentum Bias Index [AlgoAlpha]Description:

The Momentum Bias Index by AlgoAlpha is designed to provide traders with a powerful tool for assessing market momentum bias. The indicator calculates the positive and negative bias of momentum to gauge which one is greater to determine the trend.

Key Features:

Comprehensive Momentum Analysis: The script aims to detect momentum-trend bias, typically when in an uptrend, the momentum oscillator will oscillate around the zero line but will have stronger positive values than negative values, similarly for a downtrend the momentum will have stronger negative values. This script aims to quantify this phenomenon.

Overlay Mode: Traders can choose to overlay the indicator on the price chart for a clear visual representation of market momentum.

Take-profit Signals: The indicator includes signals to lock in profits, they appear as labels in overlay mode and as crosses when overlay mode is off.

Impulse Boundary: The script includes an impulse boundary, the impulse boundary is a threshold to visualize significant spikes in momentum.

Standard Deviation Multiplier: Users can adjust the standard deviation multiplier to increase the noise tolerance of the impulse boundary.

Bias Length Control: Traders can customize the length for evaluating bias, enabling them to fine-tune the indicator according to their trading preferences. A higher length will give a longer-term bias in trend.

BTC Supply in Profits and Losses (BTCSPL) [AlgoAlpha]Description:

🚨The BTC Supply in Profits and Losses (BTCSPL) indicator, developed by AlgoAlpha, offers traders insights into the distribution of INDEX:BTCUSD addresses between profits and losses based on INDEX:BTCUSD on-chain data.

Features:

🔶Alpha Decay Adjustment: The indicator provides the option to adjust the data against Alpha Decay, this compensates for the reduction in clarity of the signal over time.

🔶Rolling Change Display: The indicator enables the display of the rolling change in the distribution of Bitcoin addresses between profits and losses, aiding in identifying shifts in market sentiment.

🔶BTCSPL Value Score: The indicator optionally displays a value score ranging from -1 to 1, traders can use this to carry out strategic dollar cost averaging and reverse dollar cost averaging based on the implied value of bitcoin.

🔶Reversal Signals: The indicator gives long-term reversal signals denoted as "▲" and "▼" for the price of bitcoin based on oversold and overbought conditions of the BTCSPL.

🔶Moving Average Visualization: Traders can choose to display a moving average line, allowing for better trend identification.

How to Use ☝️ (summary):

Alpha Decay Adjustment: Toggle this option to enable or disable Alpha Decay adjustment for a normalized representation of the data.

Moving Average: Toggle this option to show or hide the moving average line, helping traders identify trends.

Short-Term Trend: Enable this option to display the short-term trend based on the Aroon indicator.

Rolling Change: Choose this option to visualize the rolling change in the distribution between profits and losses.

BTCSPL Value Score: Activate this option to show the BTCSPL value score, ranging from -1 to 1, 1 implies that bitcoin is extremely cheap(buy) and -1 implies bitcoin is extremely expensive(sell).

Reversal Signals: Gives binary buy and sell signals for the long term

Volume Exhaustion [AlgoAlpha]Introducing the Volume Exhaustion by AlgoAlpha, is an innovative tool that aims to identify potential exhaustion or peaks in trading volume , which can be a key indicator for reversals or continuations in market trends 🔶.

Key Features:

Signal Plotting : A special feature is the plotting of 'Release' signals, marked by orange diamonds, indicating points where the exhaustion index crosses under its previous value and is above a certain boundary. This could signify critical market points 🚨.

Calculation Length Customization : Users can adjust the calculation and Signal lengths to suit their trading style, allowing for flexibility in analysis over different time periods. ☝️

len = input(50, "Calculation Length")

len2 = input(8, "Signal Length")

Visual Appeal : The script offers customizable colors (col for the indicator and col1 for the background) enhancing the visual clarity and user experience 💡.

col = input.color(color.white, "Indicator Color")

col1 = input.color(color.gray, "Background Color")

Advanced Volume Processing : At its core, the script utilizes a combination of Hull Moving Average (HMA) and Exponential Moving Average (EMA) applied to the volume data. This sophisticated approach helps in smoothing out the volume data and reducing lag.

sv = ta.hma(volume, len)

ssv = ta.hma(sv, len)

Volume Exhaustion Detection : The script calculates the difference between the volume and its smoothed version, normalizing this value to create an exhaustion index (fff). Positive values of this index suggest potential volume exhaustion.

f = sv-ssv

ff = (f) / (ta.ema(ta.highest(f, len) - ta.lowest(f, len), len)) * 100

fff = ff > 0 ? ff : 0

Boundary and Zero Line : The script includes a boundary line (boundary) and a zero line (zero), with the area between them filled for enhanced visual interpretation. This helps in assessing the relative position of the exhaustion index.

Customizable Background : The script colors the background of the chart for better readability and to distinguish the indicator’s area clearly.

Overall, Volume Exhaustion is designed for traders who focus on volume analysis. It provides a unique perspective on volume trends and potential exhaustion points, which can be crucial for making informed trading decisions. This script is a valuable addition for traders looking to enhance their trading experience with advanced volume analysis tools.

Simple Neural Network Transformed RSI [QuantraSystems]Simple Neural Network Transformed RSI

Introduction

The Simple Neural Network Transformed RSI (ɴɴᴛ ʀsɪ) stands out as a formidable tool for traders who specialize in lower timeframe trading.

It is an innovative enhancement of the traditional RSI readings with simple neural network smoothing techniques.

This unique blend results in fairly accurate signals, tailored for swift market movements. The ɴɴᴛ ʀsɪ is particularly resistant to the usual market noise found in lower timeframes, ensuring a clearer view of short-term trends.

Furthermore, its diverse range of visualization options adds versatility, making it a valuable tool for traders seeking to capitalize on short-duration market dynamics.

Legend

In the Image you can see the BTCUSD 1D Chart with the ɴɴᴛ ʀsɪ in Trend Following Mode to display the current trend. This is visualized with the barcoloring.

Its Overbought and Oversold zones start at 50% and end at 100% of the selected Standard Deviation (default σ = 2), which can indicate extremely rare situations which can lead to either a softening momentum in the trend or even a mean reversion situation.

Here you can also see the original Indicator line and the Heikin Ashi transformed Indicator bars - more on that now.

Notes

Quantra Standard Value Contents:

To draw out all the information from the indicator calculation we have added a Heikin-Ashi (HA) Candle Visualization.

This HA transformation smoothens out the indicator values and gives a more informative look into Momentum and Trend of the Indicator itself.

This allows early entries and exits by observing the HA transformed Indicator values.

To diversify, different visualization options are available, either a classic line, HA transformed or Hybrid, which contains both of the previous.

To make Quantra's Indicators as useful and versatile as possible we have created options

to change the barcoloring and thus the derived signal from the indicator based on different modes.

Option to choose different Modes:

Trend Following (Indicator above mid line counts as uptrend, below is downtrend)

Extremities (Everything going beyond the Deviation Bands in a Mean Reversion manner is highlighted)

Candles (Color of HA candles as barcolor)

Reversion (HA ONLY) (Reversion Signals via the triangles if HA candles change state outside of the Deviation Bands)

- Reversion Signals are indicated by the triangles in the Heikin-Ashi or Hybrid visualization when the HA Candles revert

from downwards to upwards or the other way around OUTSIDE of the SD Bands.

Depending on the Indicator they signal OB/OS areas and can either work as high probability entries and exits for Mean Reversion trades or

indicate Momentum slow downs and potential ranges.

Please use another indicator to confirm this.

Case Study

To effectively utilize the NNT-RSI, traders should know their style and familiarize themselves with the available options.

As stated above, you have multiple modes available that you can combine as you need and see fit.

In the given example mostly only the mode was used in an isolated fashion.

Trend Following:

Purely relied on State Change - Midline crossover

Could be combined with Momentum or Reversion analysis for better entries/exits.

Extremities:

Ideal entry/exit is in the accordingly colored OS/OB Area, the Reversion signaled the latest possible entry/exit.

HA Candles:

Specifically applicable for strong trends. Powerful and fast tool.

Can whip if used as sole condition.

Reversions:

Shows the single entry and exit bars which have a positive expected value outcome.

Can also be used as confirmation or as last signal.

Please note that we always advise to find more confluence by additional indicators.

Traders are encouraged to test and determine the most suitable settings for their specific trading strategies and timeframes.

In the showcased trades the default settings were used.

Methodology

The Simple Neural Network Transformed RSI uses a simple neural network logic to process RSI values, smoothing them for more accurate trend analysis.

This is achieved through a linear combination of RSI values over a specified input length, weighted evenly to produce a neural network output.

// Simple neural network logic (linear combination with weighted aggregation)

var float inputs = array.new_float(nnLength, na)

for i = 0 to nnLength - 1

array.set(inputs, i, rsi1 )

nnOutput = 0.0

for i = 0 to nnLength - 1

nnOutput := nnOutput + array.get(inputs, i) * (1 / nnLength)

nnOutput

This output is then compared against a standard or dynamic mean line to generate trend following signals.

Mean = ta.sma(nnOutput, sdLook)

cross = useMean? 50 : Mean

The indicator also incorporates Heikin Ashi candlestick calculations to provide additional insights into market dynamics, such as trend strength and potential reversals.

// Calculate Heikin Ashi representation

ha = ha(

na(nnOutput ) ? nnOutput : nnOutput ,

math.max(nnOutput, nnOutput ),

math.min(nnOutput, nnOutput ),

nnOutput)

Standard deviation bands are used to create dynamic overbought and oversold zones, further enhancing the tool's analytical capabilities.

// Calculate Dynamic OB/OS Zones

stdv_bands(_src, _length, _mult) =>

float basis = ta.sma(_src, _length)

float dev = _mult * ta.stdev(_src, _length)

= stdv_bands(nnOutput, sdLook,sdMult/2)

= stdv_bands(nnOutput, sdLook, sdMult)

The Standard Deviation bands take defined parameters from the user, in this case sigma of ideally between 2 to 3,

to help the indicator detect extremely improbable conditions and thus take an inversely probable signal from it to forward to the user.

The parameter settings and also the visualizations allow for ample customizations by the trader.

For questions or recommendations, please feel free to seek contact in the comments.

Triple Confirmation Kernel Regression Overlay [QuantraSystems]Kernel Regression Oscillator - Overlay

Introduction

The Kernel Regression Oscillator (ᏦᏒᎧ) represents an advanced tool for traders looking to capitalize on market trends.

This Indicator is valuable in identifying and confirming trend directions, as well as probabilistic and dynamic oversold and overbought zones.

It achieves this through a unique composite approach using three distinct Kernel Regressions combined in an Oscillator.

The additional Chart Overlay Indicator adds confidence to the signal.

Which is this Indicator.

This methodology helps the trader to significantly reduce false signals and offers a more reliable indication of market movements than more widely used indicators can.

Legend

The upper section is the Overlay. It features the Signal Wave to display the current trend.

Its Overbought and Oversold zones start at 50% and end at 100% of the selected Standard Deviation (default σ = 3), which can indicate extremely rare situations which can lead to either a softening momentum in the trend or even a mean reversion situation.

The lower one is the Base Chart.

The Indicator is linked here

It features the Kernel Regression Oscillator to display a composite of three distinct regressions, also displaying current trend.

Its Overbought and Oversold zones start at 50% and end at 100% of the selected Standard Deviation (default σ = 2), which can indicate extremely rare situations.

Case Study

To effectively utilize the ᏦᏒᎧ, traders should use both the additional Overlay and the Base

Chart at the same time. Then focus on capturing the confluence in signals, for example:

If the 𝓢𝓲𝓰𝓷𝓪𝓵 𝓦𝓪𝓿𝓮 on the Overlay and the ᏦᏒᎧ on the Base Chart both reside near the extreme of an Oversold zone the probability is higher than normal that momentum in trend may soften or the token may even experience a reversion soon.

If a bar is characterized by an Oversold Shading in both the Overlay and the Base Chart, then the probability is very high to experience a reversion soon.

In this case the trader may want to look for appropriate entries into a long position, as displayed here.

If a bar is characterized by an Overbought Shading in either Overlay or Base Chart, then the probability is high for momentum weakening or a mean reversion.

In this case the trade may have taken profit and closed his long position, as displayed here.

Please note that we always advise to find more confluence by additional indicators.

Recommended Settings

Swing Trading (1D chart)

Overlay

Bandwith: 45

Width: 2

SD Lookback: 150

SD Multiplier: 2

Base Chart

Bandwith: 45

SD Lookback: 150

SD Multiplier: 2

Fast-paced, Scalping (4min chart)

Overlay

Bandwith: 75

Width: 2

SD Lookback: 150

SD Multiplier: 3

Base Chart

Bandwith: 45

SD Lookback: 150

SD Multiplier: 2

Notes

The Kernel Regression Oscillator on the Base Chart is also sensitive to divergences if that is something you are keen on using.

For maximum confluence, it is recommended to use the indicator both as a chart overlay and in its Base Chart.

Please pay attention to shaded areas with Standard Deviation settings of 2 or 3 at their outer borders, and consider action only with high confidence when both parts of the indicator align on the same signal.

This tool shows its best performance on timeframes lower than 4 hours.

Traders are encouraged to test and determine the most suitable settings for their specific trading strategies and timeframes.

The trend following functionality is indicated through the "𝓢𝓲𝓰𝓷𝓪𝓵 𝓦𝓪𝓿𝓮" Line, with optional "Up" and "Down" arrows to denote trend directions only (toggle “Show Trend Signals”).

Methodology

The Kernel Regression Oscillator takes three distinct kernel regression functions,

used at similar weight, in order to calculate a balanced and smooth composite of the regressions. Part of it are:

The Epanechnikov Kernel Regression: Known for its efficiency in smoothing data by assigning less weight to data points further away from the target point than closer data points, effectively reducing variance.

The Wave Kernel Regression: Similarly assigning weight to the data points based on distance, it captures repetitive and thus wave-like patterns within the data to smoothen out and reduce the effect of underlying cyclical trends.

The Logistic Kernel Regression: This uses the logistic function in order to assign weights by probability distribution on the distance between data points and target points. It thus avoids both bias and variance to a certain level.

kernel(source, bandwidth, kernel_type) =>

switch kernel_type

"Epanechnikov" => math.abs(source) <= 1 ? 0.75 * (1 - math.pow(source, 2)) : 0.0

"Logistic" => 1/math.exp(source + 2 + math.exp(-source))

"Wave" => math.abs(source) <= 1 ? (1 - math.abs(source)) * math.cos(math.pi * source) : 0.

kernelRegression(src, bandwidth, kernel_type) =>

sumWeightedY = 0.

sumKernels = 0.

for i = 0 to bandwidth - 1

base = i*i/math.pow(bandwidth, 2)

kernel = kernel(base, 1, kernel_type)

sumWeightedY += kernel * src

sumKernels += kernel

(src - sumWeightedY/sumKernels)/src

// Triple Confirmations

Ep = kernelRegression(source, bandwidth, 'Epanechnikov' )

Lo = kernelRegression(source, bandwidth, 'Logistic' )

Wa = kernelRegression(source, bandwidth, 'Wave' )

By combining these regressions in an unbiased average, we follow our principle of achieving confluence for a signal or a decision, by stacking several edges to increase the probability that we are correct.

// Average

AV = math.avg(Ep, Lo, Wa)

The Standard Deviation bands take defined parameters from the user, in this case sigma of ideally between 2 to 3,

to help the indicator detect extremely improbable conditions and thus take an inversely probable signal from it to forward to the user.

The parameter settings and also the visualizations allow for ample customizations by the trader. The indicator comes with default and recommended settings.

For questions or recommendations, please feel free to seek contact in the comments.

Triple Confirmation Kernel Regression Base [QuantraSystems]Kernel Regression Oscillator - BASE

Introduction

The Kernel Regression Oscillator (ᏦᏒᎧ) represents an advanced tool for traders looking to capitalize on market trends.

This Indicator is valuable in identifying and confirming trend directions, as well as probabilistic and dynamic oversold and overbought zones.

It achieves this through a unique composite approach using three distinct Kernel Regressions combined in an Oscillator. The additional Chart Overlay Indicator adds confidence to the signal.

This methodology helps the trader to significantly reduce false signals and offers a more reliable indication of market movements than more widely used indicators can.

Legend

The upper section is the Overlay. It features the Signal Wave to display the current trend.

Its Overbought and Oversold zones start at 50% and end at 100% of the selected Standard Deviation (default σ = 3), which can indicate extremely rare situations which can lead to either a softening momentum in the trend or even a mean reversion situation.

The lower one is the Base Chart - This Indicator.

It features the Kernel Regression Oscillator to display a composite of three distinct regressions, also displaying current trend.

Its Overbought and Oversold zones start at 50% and end at 100% of the selected Standard Deviation (default σ = 2), which can indicate extremely rare situations.

Case Study

To effectively utilize the ᏦᏒᎧ, traders should use both the additional Overlay and the Base

Chart at the same time. Then focus on capturing the confluence in signals, for example:

If the 𝓢𝓲𝓰𝓷𝓪𝓵 𝓦𝓪𝓿𝓮 on the Overlay and the ᏦᏒᎧ on the Base Chart both reside near the extreme of an Oversold zone the probability is higher than normal that momentum in trend may soften or the token may even experience a reversion soon.

If a bar is characterized by an Oversold Shading in both the Overlay and the Base Chart, then the probability is very high to experience a reversion soon.

In this case the trader may want to look for appropriate entries into a long position, as displayed here.

If a bar is characterized by an Overbought Shading in either Overlay or Base Chart, then the probability is high for momentum weakening or a mean reversion.

In this case the trade may have taken profit and closed his long position, as displayed here.

Please note that we always advise to find more confluence by additional indicators.

Recommended Settings

Swing Trading (1D chart)

Overlay

Bandwith: 45

Width: 2

SD Lookback: 150

SD Multiplier: 2

Base Chart

Bandwith: 45

SD Lookback: 150

SD Multiplier: 2

Fast-paced, Scalping (4min chart)

Overlay

Bandwith: 75

Width: 2

SD Lookback: 150

SD Multiplier: 3

Base Chart

Bandwith: 45

SD Lookback: 150

SD Multiplier: 2

Notes

The Kernel Regression Oscillator on the Base Chart is also sensitive to divergences if that is something you are keen on using.

For maximum confluence, it is recommended to use the indicator both as a chart overlay and in its Base Chart.

Please pay attention to shaded areas with Standard Deviation settings of 2 or 3 at their outer borders, and consider action only with high confidence when both parts of the indicator align on the same signal.

This tool shows its best performance on timeframes lower than 4 hours.

Traders are encouraged to test and determine the most suitable settings for their specific trading strategies and timeframes.

The trend following functionality is indicated through the "𝓢𝓲𝓰𝓷𝓪𝓵 𝓦𝓪𝓿𝓮" Line, with optional "Up" and "Down" arrows to denote trend directions only (toggle “Show Trend Signals”).

Methodology

The Kernel Regression Oscillator takes three distinct kernel regression functions,

used at similar weight, in order to calculate a balanced and smooth composite of the regressions. Part of it are:

The Epanechnikov Kernel Regression: Known for its efficiency in smoothing data by assigning less weight to data points further away from the target point than closer data points, effectively reducing variance.

The Wave Kernel Regression: Similarly assigning weight to the data points based on distance, it captures repetitive and thus wave-like patterns within the data to smoothen out and reduce the effect of underlying cyclical trends.

The Logistic Kernel Regression: This uses the logistic function in order to assign weights by probability distribution on the distance between data points and target points. It thus avoids both bias and variance to a certain level.

kernel(source, bandwidth, kernel_type) =>

switch kernel_type

"Epanechnikov" => math.abs(source) <= 1 ? 0.75 * (1 - math.pow(source, 2)) : 0.0

"Logistic" => 1/math.exp(source + 2 + math.exp(-source))

"Wave" => math.abs(source) <= 1 ? (1 - math.abs(source)) * math.cos(math.pi * source) : 0.

kernelRegression(src, bandwidth, kernel_type) =>

sumWeightedY = 0.

sumKernels = 0.

for i = 0 to bandwidth - 1

base = i*i/math.pow(bandwidth, 2)

kernel = kernel(base, 1, kernel_type)

sumWeightedY += kernel * src

sumKernels += kernel

(src - sumWeightedY/sumKernels)/src

// Triple Confirmations

Ep = kernelRegression(source, bandwidth, 'Epanechnikov' )

Lo = kernelRegression(source, bandwidth, 'Logistic' )

Wa = kernelRegression(source, bandwidth, 'Wave' )

By combining these regressions in an unbiased average, we follow our principle of achieving confluence for a signal or a decision, by stacking several edges to increase the probability that we are correct.

// Average

AV = math.avg(Ep, Lo, Wa)

The Standard Deviation bands take defined parameters from the user, in this case sigma of ideally between 2 to 3,

to help the indicator detect extremely improbable conditions and thus take an inversely probable signal from it to forward to the user.

The parameter settings and also the visualizations allow for ample customizations by the trader. The indicator comes with default and recommended settings.

For questions or recommendations, please feel free to seek contact in the comments.

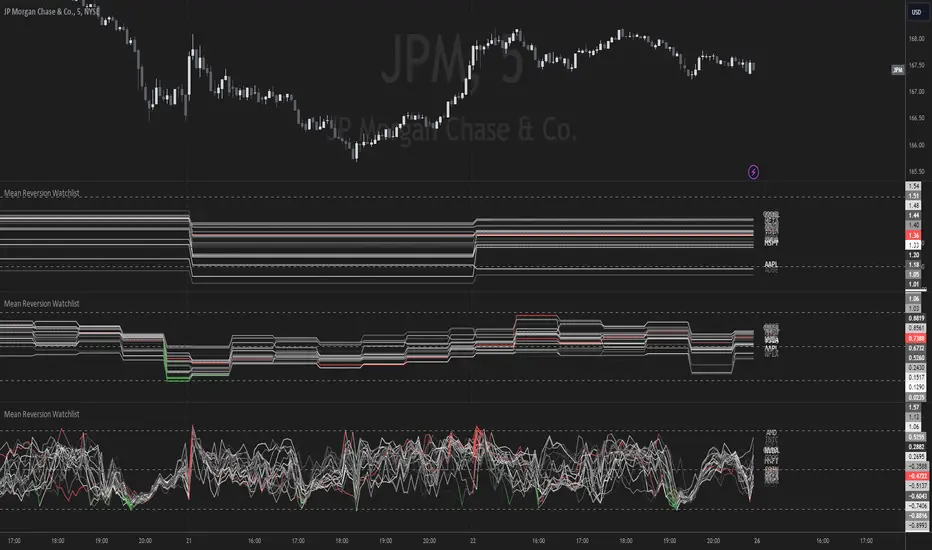

Mean Reversion Watchlist [Z score]Hi Traders !

What is the Z score:

The Z score measures a values variability factor from the mean, this value is denoted by z and is interpreted as the number of standard deviations from the mean.

The Z score is often applied to the normal distribution to “standardize” the values; this makes comparison of normally distributed random variables with different units possible.

This popular reversal based indicator makes an assumption that the sample distribution (in this case the sample of price values) is normal, this allows for the interpretation that values with an extremely high or low percentile or “Z” value will likely be reversal zones.

This is because in the population data (the true distribution) which is known, anomaly values are very rare, therefore if price were to take a z score factor of 3 this would mean that price lies 3 standard deviations from the mean in the positive direction and is in the ≈99% percentile of all values. We would take this as a sign of a negative reversal as it is very unlikely to observe a consecutive equal to or more extreme than this percentile or Z value.

The z score normalization equation is given by

In Pine Script the Z score can be computed very easily using the below code.

// Z score custom function

Zscore(source, lookback) =>

sma = ta.sma(source, lookback)

stdev = ta.stdev(source, lookback, true)

zscore = (source - sma) / stdev

zscore

The Indicator:

This indicator plots the Z score for up to 20 different assets ( Note the maximum is 40 however the utility of 40 plots in one indicator is not much, there is a diminishing marginal return of the number of plots ).

Z score threshold levels can also be specified, the interpretation is the same as stated above.

The timeframe can also be fixed, by toggling the “Time frame lock” user input under the “TIME FRAME LOCK” user input group ( Note this indicator does not repain t).

Alpha Schaff [AlgoAlpha]Description:

The Alpha Schaff indicator is a proprietary technical analysis tool that incorporates a modified version of the Schaff Trend Cycle (STC) to generate trading signals. The indicator is designed to identify potential overbought and oversold conditions in the market. It utilizes a combination of exponential moving averages (EMAs) and price volatility to generate trading signals. The plot of the indicator is derived from the opening price adjusted by a factor that depends on the Alpha Schaff value. A color scheme is used to indicate whether the current value is higher or lower than the previous value.

What is Alpha Schaff?:

Alpha Schaff is a technical indicator used in trading to identify potential trend reversals and confirm the strength of a current trend. It combines multiple moving averages and oscillators to generate buy and sell signals. Traders use Alpha Schaff to make informed decisions about entering or exiting positions based on its indications of trend momentum and market conditions.

Calculation:

The Alpha Schaff indicator calculates the difference between fast and slow EMAs based on the specified input lengths. It then measures the highest and lowest values of the difference over a defined sensitivity period. The indicator normalizes these values to a percentage scale to provide insights into the current market conditions.

How to use it?:

Monitor the color of the indicator line. A change in color indicates a potential trend reversal. For example, a switch from white to a purple color suggests a possible bullish trend, while a switch from a purple color to white indicates a potential bearish trend. Points of reversal can also be indicated by distinctive arrows pointing upwards or downward as well as visualized in bullish/bearish colors. The Distance between the indicator plot and the source can be interpreted as a measurement of price volatility. The script includes alert conditions that trigger when specific criteria are met. These alerts can notify users of potential buying or selling opportunities based on the indicator's signals.

Utility:

The Alpha Schaff is a trend-following indicator suitable for traders operating in trending markets. It offers clear and precise signals that provide valuable insights into bullish or bearish price movements. Additionally, this indicator stands out by incorporating distinctive arrows, indicating potential retracement points and allowing traders to anticipate mean reversion.

Originality:

The Alpha Schaff indicator, developed by AlgoAlpha introduces a proprietary modification to the Schaff Trend Cycle (STC) by incorporating multiple moving averages and oscillators. While the concept of the Schaff Trend Cycle exists, the specific implementation and combination of elements in the Alpha vSchaff indicator are unique to this tool. The inclusion of color schemes, arrow indicators, and volatility measurements sets it apart from other technical analysis indicators. Traders can benefit from its originality by utilizing its distinctive features to make more informed trading decisions in trending markets.

Amazing Oscillator (AO) [Algoalpha]Description:

Introducing the Amazing Oscillator indicator by Algoalpha, a versatile tool designed to help traders identify potential trend shifts and market turning points. This indicator combines the power of the Awesome Oscillator (AO) and the Relative Strength Index (RSI) to create a new indicator that provides valuable insights into market momentum and potential trade opportunities.

Key Features:

Customizable Parameters: The indicator allows you to customize the period of the RSI calculations to fine-tune the indicator's responsiveness.

Visual Clarity: The indicator uses user-defined colors to visually represent upward and downward movements. You can select your preferred colors for both bullish and bearish signals, making it easy to spot potential trade setups.

AO and RSI Integration: The script combines the AO and RSI indicators to provide a comprehensive view of market conditions. The RSI is applied to the AO, which results in a standardized as well as a less noisy version of the Awesome Oscillator. This makes the indicator capable of pointing out overbought or oversold conditions as well as giving fewer false signals

Signal Plots: The indicator plots key levels on the chart, including the RSI threshold(Shifted down by 50) at 30 and -30. These levels are often used by traders to identify potential trend reversal points.

Signal Alerts: For added convenience, the indicator includes "x" markers to signal potential buy (green "x") and sell (red "x") opportunities based on RSI crossovers with the -30 and 30 levels. These alerts can help traders quickly identify potential entry and exit points.

Hurst ALMA Channels With Signals [UAlgo]

In the pursuit of identifying potential market pivots, a single measurement of Average True Range (ATR), may not provide sufficient information on its own, lacking directional insights. However, by employing a Moving Average (MA), specifically the Arnaud Legoux MA with Hurst C. calculation applied, a potential trading range can be visualized, taking recent volatility into account.

The underlying assumption is that if volatility remains relatively stable and the price extends beyond this ATR-derived range, there is a high probability of a reversion to the mean. At this point, it is postulated that available buying or selling pressure is depleted, prompting a pivot back to the mean.

To enhance the analysis, multiple MAs of different lengths are plotted. While individual MAs alone may not convey substantial information, observing reversions to the mean between MAs of varying lengths becomes insightful. Shorter MAs may oscillate above or below longer MAs, returning to the mean and creating crossover patterns.

The key innovation lies in combining these two concepts. By utilizing three different length MAs with corresponding ATR lengths, a dynamic system is established. The smallest band fluctuates within the medium band, and the medium band oscillates within the large band, creating approximate short, medium, and long trading ranges relative to the MAs.

For instance, in a theoretical scenario, when the smallest band reaches the upper limit of the medium band, and simultaneously, the medium band reaches the upper limit of the large band, and the price surpasses all of them, there is a heightened probability of a market reversal.

It's important to emphasize that these observations are based on historical volatility patterns and are subject to adjustments based on specific market conditions and the chosen instrument.

The developed indicator generates three distinct signal types, each providing valuable insights into potential market pivots without disclosing specific parameters:

Large Triangles : Representing a high-probability pivot, this signal occurs when the price surpasses all bands, either at the top or bottom. It suggests an extreme point where a pivot is likely.

Medium Triangles : Indicating a notable market event, this signal emerges when the price exceeds both the small and medium bands but falls short of surpassing the large band. Additionally, the small band must have exceeded the medium band. This configuration points to a significant market move with a potential for reversion.

Small Triangles : This signal is observed when the price surpasses both the small and medium bands, yet does not breach the large band. Notably, the small band should not have exceeded the medium band. This signal type suggests a distinctive market condition where a pivot may be imminent.

These triangle signals are designed to identify key points in the market where historical patterns indicate a likelihood of reversion or significant price movement. It is crucial to note that the interpretation of these signals should be adapted to specific market conditions and instruments.

Good luck to you all !

Trend Flow Profile [AlgoAlpha]Description:

The "Trend Flow Profile" indicator is a powerful tool designed to analyze and interpret the underlying trends and reversals in a financial market. It combines the concepts of Order Flow and Rate of Change (ROC) to provide valuable insights into market dynamics, momentum, and potential trade opportunities. By integrating these two components, the indicator offers a comprehensive view of market sentiment and price movements, facilitating informed trading decisions.

Rationale:

The combination of Order Flow and ROC in the "Trend Flow Profile" indicator stems from the recognition that both factors play critical roles in understanding market behavior. Order Flow represents the net buying or selling pressure in the market, while ROC measures the rate at which prices change. By merging these elements, the indicator captures the interplay between market participants' actions and the momentum of price movements, enabling traders to identify trends, spot reversals, and gauge the strength of price acceleration or deceleration.

Calculation:

The Order Flow component is computed by summing the volume when prices move up and subtracting the volume when prices move down. This cumulative measure reflects the overall order imbalance in the market, providing insights into the dominant buying or selling pressure.

The ROC component calculates the percentage change in price over a given period. It compares the current price to a previous price and expresses the change as a percentage. This measurement indicates the velocity and direction of price movement, allowing traders to assess the market's momentum.

How to Use It?

The "Trend Flow Profile" indicator offers valuable information to traders for making informed trading decisions. It enables the identification of underlying trends and potential reversals, providing a comprehensive view of market sentiment and momentum. Here are some key ways to utilize the indicator:

Spotting Trends: The indicator helps identify the prevailing market trend, whether bullish or bearish. A consistent positive (green) histogram indicates a strong uptrend, while a consistent negative (red) histogram suggests a robust downtrend.

Reversal Signals: Reversal patterns can be identified when the histogram changes color, transitioning from positive to negative (or vice versa). These reversals can signify potential turning points in the market, highlighting opportunities for counter-trend trades.

Momentum Assessment: By observing the width and intensity of the histogram, traders can assess the acceleration or deceleration of price momentum. A wider histogram suggests strong momentum, while a narrower histogram indicates a potential slowdown.

Utility:

The "Trend Flow Profile" indicator serves as a valuable tool for traders, providing several benefits. Traders can easily identify the prevailing market trend, enabling them to align their trading strategies with the dominant direction of the market. The indicator also helps spot potential reversals, allowing traders to anticipate market turning points and capture counter-trend opportunities. Additionally, the green and red histogram colors provide visual cues to determine the optimal duration of a long or short position. Following the green histogram signals when in a long position and the red histogram signals when in a short position can assist traders in managing their trades effectively. Moreover, the width and intensity of the histogram offer insights into the acceleration or deceleration of momentum. Traders can gauge the strength of price movements and adjust their trading strategies accordingly. By leveraging the "Trend Flow Profile" indicator, traders gain a comprehensive understanding of market dynamics, which enhances their decision-making and improves their overall trading outcomes.

Bollinger Bands Percentile + Stdev Channels (BBPct) [AlgoAlpha]Description:

The "Bollinger Bands Percentile (BBPct) + STD Channels" mean reversion indicator, developed by AlgoApha, is a technical analysis tool designed to analyze price positions using Bollinger Bands and Standard Deviation Channels (STDC). The combination of these two indicators reinforces a stronger reversal signal. BBPct calculates the percentile rank of the price's standard deviation relative to a specified lookback period. Standard deviation channels operate by utilizing a moving average as the central line, with upper and lower lines equidistant from the average based on the market's volatility, helping to identify potential price boundaries and deviations.

How it Works:

The BBPct indicator utilizes Bollinger Bands, which consist of a moving average (basis) and upper and lower bands based on a specified standard deviation multiplier. By default, it uses a 20-period moving average and a standard deviation multiplier of 2. The upper band is calculated by adding the basis to the standard deviation multiplied by the multiplier, while the lower band is calculated by subtracting the same value. The BBPct indicator calculates the position of the current price between the lower and upper Bollinger Bands as a percentile value. It determines this position by comparing the price's distance from the lower band to the overall range between the upper and lower bands. A value of 0 indicates that the price is at the lower band, while a value of 100 indicates that the price is at the upper band. The indicator also includes an optional Bollinger Band standard deviation percentage (%Stdev) histogram, representing the deviation of the current price from the moving average as a percentage of the price itself.

Standard deviation channels, also known as volatility channels, aid in identifying potential buying and selling opportunities while minimizing unfavorable trades. These channels are constructed by two lines that run parallel to a moving average. The separation between these lines is determined by the market's volatility, represented by standard deviation. By designating upper and lower channel lines, the channels demarcate the borders between typical and atypical price movements. Consequently, when the market's price falls below the lower channel line, it suggests undervaluation, whereas prices surpassing the upper channel line indicate overvaluation.

Signals

The chart displays potential reversal points through the use of red and green arrows. A red arrow indicates a potential bearish retracement, signaling a possible downward movement, while a green arrow represents a potential pullback to the positive, suggesting a potential upward movement. These signals are generated only when both the BBPct (Bollinger Bands Percentage) and the STDC (Standard Deviation Channel) indicators align with bullish or bearish conditions. Consequently, traders might consider opening long positions when the green arrow appears and short positions when the red arrow is plotted.

Usage:

This indicator can be utilized by traders and investors to effectively identify pullbacks, reversals, and mean regression, thereby enhancing their trading opportunities. Notably, extreme values of the BBPct, such as below -5 or above 105, indicate oversold or overbought conditions, respectively. Moreover, the presence of extreme STDC zones occurs when prices fall below the lower channel line or cross above the upper channel line. Traders can leverage this information as a mean reversion tool by identifying instances of peak overbought and oversold values. These distinctive characteristics facilitate the identification of potential entry and exit points, thus augmenting trading decisions and enhancing market analysis.

The indicator's parameters, such as the length of the moving average, the data source, and the standard deviation multiplier, can be customized to align with individual trading strategies and preferences.

Originality:

The BBPct + STDC indicator, developed by AlgoAlpha, is an original implementation that combines the calculation of Bollinger Bands, percentile ranking, the %Stdev histogram and the STDC. While it shares some similarities with the Bollinger Bands %B indicator, the BBPct indicator introduces additional elements and customization options tailored to AlgoAlpha's methodology. The script is released under the Mozilla Public License 2.0, granting users the freedom to utilize and modify it while adhering to the license terms.

Fourier Smoothed Volume Zone Oscillator (FSVZO) [AlgoAlpha]Description