KAMA Strategy - Kaufman's Adaptive Moving AverageThis strategy combines Kaufman's Adaptive Moving Average for entry with optional KAMA, PSAR, and Trailing ATR stops for exits.

Kaufman's Adaptive Moving Average is, in my opinion, a gem among the plethora of indicators. It is underrated considering it offers a solution that intuitively makes a lot of sense. When I first read about it, it was a real 'aha!' moment. Look at the top, pink line. Notice how during trending times it follows the trend quickly and closely, but during choppy, non-trending periods, the KAMA stays absolutely flat? Interesting! To trade with it, we simply follow the direction the KAMA is pointing. Is it up? Go long. Is it down? Go short. Is it flat? Hold on.

How does it manage to quickly follow real trends like a fast EMA but ignore choppy conditions that would whipsaw a fast EMA back and forth? It analyses whether recent price moves are significant relative to recent noise and then adapts the length of the EMA window accordingly. If price movement is big compared to the recent noise, the EMA window gets smaller. If price movement is relatively small or average compared to the recent noise, the EMA window gets bigger. In practice it means:

The KAMA would be flat if a 20 point upwards move occurred during a period that has had, on average, regular 20 point moves BUT

the KAMA would point up if a 20 point move occurred during a period that has, on average, had moves of only around 5 points.

In other words, it's a slow EMA during choppy flat / quiet flat periods, and a fast EMA as soon as significant volatility occurs. Perfect!

-----

The Strategy

The strategy is more than just a KAMA indicator. It contains:

KAMA exit (optional)

ATR trailing stop loss exit (optional)

PSAR stop loss exit (optional)

KAMA filter for entry and exits

All features are adjustable in the strategy settings

The Technical Details:

Check out the strategy's 'Inputs' panel. The buy and sell signals are based on the 'KAMA 1' there.

KAMA 1: Length -- 14 is the default. This is the length of the window the KAMA looks back over. In this instance, it c

KAMA 1: Fast KAMA Length -- 2 is the default. This is the tightest the EMA length is allowed to get. It will tend towards this length when volatility is high.

KAMA 1: Slow KAMA Length -- 20 is the default. This is the biggest the EMA length is allowed to get. It will tend towards this length when volatility is low.

KAMA Filter

The strategy buys when the KAMA begins to point up and sells when the KAMA points down. Generally, the KAMA is very good at filtering out the noise itself - it will go flat during noisy/choppy periods. But to add another layer of safety, its author, Perry Kaufman, proposed a KAMA filter. It works by taking the standard deviation of returns over the length of the the 'KAMA 1: Length' I mentioned above and multiplying it by an 'Entry Filter' (1 by default) and 'Exit Filter' (0.5 by default). The entry condition to go long is that the KAMA is pointing up and and it moved up more than 1 x St. Dev. of Returns. The exit condition is when the KAMA is pointing down and it moved down by more than 0.5 x St. Dev. of Returns.

Thanks

Thanks to ChuckBanger, cheatcountry, millerrh, and racer8 for parts of the code. I was able to build upon their good work.

-----

I hope this strategy is helpful to you.

Do you have any thoughts, ideas, or questions? Let me know in the comments or send me a message! I'd be glad to help you out.

If you need an indicator or strategy to be built or customised for you, let me know! I'll be glad to help and it'll probably be cheaper than you think!

Média Móvel Adaptativa de Kaufman (MMAK)

[A618] Liquidity Levels Based OBV SR with KAMAWe all know OBV plays a very important role in figuring out price volume divergences and it can help anyone analyse the directivity force of the market and has a very good tradeoff if applied correctly

In this Experiment i have derived liquidity levels for OBV using volume jumps inside the market

A volume jump is classified as:

Good Volume Jump = 1.618 times the Average Volume (WMA or 2pole ButterWorth's Filter of Volume)

Great Volume Jump = 2 times the Average Volume (WMA or 2pole ButterWorth's Filter of Volume)

Extreme Volume Jump = 3 times the Average Volume (WMA or 2pole ButterWorth's Filter of Volume)

So the horizontal levels which you see on the indicator (colored in red/ blue / gray lines) are the derived Liquidity Levels for OBV in the Market, these are the levels where OBV is most likely to perform a movement or come back

Also I have applied KAMA indicator on top of OBV for better Directive guidance, as of my experiments KAMA seems to be most stable and consistence of all the other moving averages,

KAMA's Length inculde:

KAMA - 8

KAMA - 34

KAMA - 200

Hope this Script help you guys!

Thanks to Tradingview for providing such an awesome platform

##Note for Credits ::

The Ehlers 2 pole butterworth Filter function is derived from @cheatcountry script ()

MA+MA+ is a multi time frame moving average indicator with more than a dozen different moving averages (like KAMA, VAMA, JMA, HMA and much more).

More moving averages will be added on every update, hence Follow me to get notified.

MA+ Supports automatic (AUTO in settings) time frame multiplier. For example, if you set 'Auto Resolution Multiplier' to 6, and your base chart is 5 minutes, the moving averages will plot at 5 * 6 = 30 minutes.

You can still use 'User Defined' to use your own time frame without using the multiplier.

Use higher time frame than the base chart time frame to avoid repainting.

Default multiplier for higher time frame is 2.

Supports Signals 1 (rising MA) or -1 (falling MA) to attach to another indicator.

Bars are not colored by default.

Just for this great community, You can request in the comments other moving averages that do not exists in MA+.

Tobacco ChannelThese bands use KAMA for the basis, build Keltner Channels that you might expect high probability reversals to occur from.

I named it Tobacco Channel because I found its idea in Cuban's Reversion Bands — Indicator by cubantobacco.

KINSKI Flexible Multi MA (EMA, SMA, RMA, WMA, VWMA, KAMA, HMA)This Multi Moving Average (MA) indicator is more flexible than any other indicator of this type offered so far. You can define up to 10 different Moving Average (MA) lines based on different calculation variants.

The following MA types can be configured.

- EMA: Exponentially Moving Average

- SMA: Small Moving Average

- RMA: Rolling Moving Average

- WMA: Weighted Moving Average

- VWMA: Volume Weighted Moving Average

- KAMA: Kaufman's Adaptive Moving Average

- HMA: Hull Moving Average

Which settings can be made?

- Selection for calculation formula ("Calculation Source"). The default value is "close".

- for each MA line the "Length" and the "Type" can be defined

- furthermore you can make layout adjustments via the "Style" menu

3MA'S + KAMA Trend (20EMA,50MA,200MA + KAMA Trend)This indicator, combines the traditional FOREX moving averages (20EMA, 50ma, 200ma) into a single indicator with

an adaptive moving average (AMA) taken from a user defined timeframe to show trend direction (by default, it plots

the daily 10/2/34 KAMA overlayed on any timeframe chart.

An AMA moves slowly when markets are sideways but swiftly during periods of volatility as a result it reacts much fast than

traditional options for moving average trends.

If the price is above the KAMA, trend is up. Below the KAMA, trend is down.

Moving Average Compendium===========

Moving Average Compendium (16 MA Types)

===========

A selection of the most popular, widely used, interesting and most powerful Moving Averages we can think of. We've compiled 16 MA's into this script, and allowed full access to the source code so you can use what you need, as you need it.

-----------

From very simple moving averages using built-in functions, all the way through to Fractal Adaptive Averages, we've tried to cover as much as we can think of! BUT, if you would like to make a suggestion or recommendation to be added to this compendium of MA's please let us know! Together we can get a complete list of many dozens of types of Moving Average.

Full List (so far)

---

SMA - Simple Moving Average

EMA - Exponential Moving Average

WMA - Weighted Moving Average

VWMA - Volume Weighted Moving Average

DEMA - Double Exponential Moving Average

TEMA - Triple Exponential Moving Average

SMMA - Smoothed Moving Average

HMA - Hull Moving Average

ZLEMA - Zero-Lag Exponential Moving Average

KAMA - Kaufman Adaptive Moving Average

JMA - Jurik Moving Average

SWMA - Sine-Weighted Moving Average

TriMA - Triangular Moving Average

MedMA - Moving Median Average

GeoMA - Geometric Mean Moving Average

FRAMA - Fractal Adaptive Moving Average

Line color changes from green (upward) to red (downward) - some of the MA types will "linger" without moving up or down and when they are in this state they should appear gray in color.

Thanks to all involved -

Good Luck and Happy Trading!

RSI based on Kaufman’s Adaptive Moving Average This is RSI based on Kaufman’s Adaptive Moving Average.

Drawing line flatter than normal RSI.

In My sense, it can easier find Divergence than normal RSI.

I use William Delbert Gann's short cycle of "multiples of 7" for the default setting.

Or, you can choose and customize a setting from my preset.

Moving Average Adaptive QThe Moving Average Adaptive Q (MAAQ) was authored by Perry Kaufman in the Stocks and Commodities Magazine 06/1995

This is similar to his Kaufman Adaptive Moving Average with a few changes. This is a pretty close moving average which I like quite a bit. Try it and let me know what you think.

Send me a message and let me know what other indicators you would like to see!

Slow Heiken Ashi and Exponential Moving average Strategy 2.2Strategy using Slow Heiken Ashi by Glaz and Exponential moving averages. Looking for someone to help me turn the strategy into non-reoccuring alerts as I am having trouble doing so.

Kaufman Adaptive Moving Average Ribbon [ChuckBanger]Kaufman Adaptive Moving Average is one of the best moving averages in my opinion. So I made a ribbon script out of it. Good luck traders :)

Kaufman Adaptive Least Squares Moving AverageIntroduction

It is possible to use a wide variety of filters for the estimation of a least squares moving average, one of the them being the Kaufman adaptive moving average (KAMA) which adapt to the market trend strength, by using KAMA in an lsma we therefore allow for an adaptive low lag filter which might provide a smarter way to remove noise while preserving reactivity.

The Indicator

The lsma aim to minimize the sum of the squared residuals, paired with KAMA we obtain a great adaptive solution for smoothing while conserving reactivity. Length control the period of the efficiency ratio used in KAMA, higher values of length allow for overall smoother results. The pre-filtering option allow for even smoother results by using KAMA as input instead of the raw price.

The proposed indicator without pre-filtering in green, a simple moving average in orange, and a lsma with all of them length = 200. The proposed filter allow for fast and precise crosses with the moving average while eliminating major whipsaws.

Same setup with the pre-filtering option, the result are overall smoother.

Conclusion

The provided code allow for the implementation of any filter instead of KAMA, try using your own filters. Thanks for reading :)

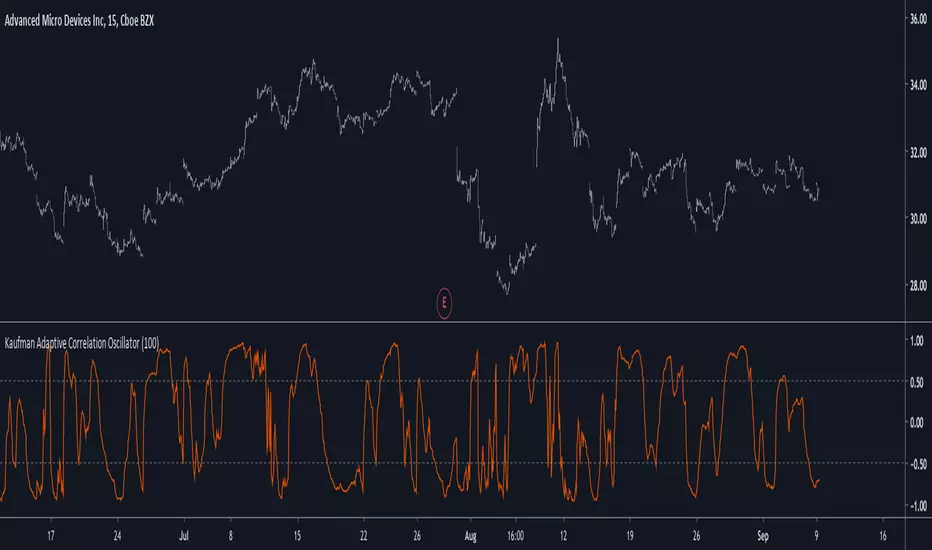

Kaufman Adaptive Correlation OscillatorIntroduction

The correlation oscillator is a technical indicator that measure the linear relationship between the market closing price and a simple increasing line, the indicator is in a (-1,1) range and rise when price is up-trending and fall when price is down-trending. Another characteristic of the indicator is its inherent smoothing which provide a noise free (to some extent) oscillator.

Such indicator use simple moving averages as well as estimates of the standard deviation for its calculation, but we can easily make it adaptive, this is why i propose this new technical indicator that create an adaptive correlation oscillator based on the Kaufman adaptive moving average.

The Indicator

The length parameter control the period window of the moving average, larger periods return smoother results while having a low kurtosis, which mean that values will remain around 1 or -1 a longer period of time. Pre-filtering apply a Kaufman adaptive moving average to the input, which allow for a smoother output.

No pre-filtering in orange, pre-filtering in yellow, period = 100 for both oscillators.

If you are not aware of the Kaufman adaptive moving average, such moving average return more reactive results when price is trending and smoother results when price is ranging, this also apply for the proposed indicator.

Conclusion

Classical correlation coefficients could use this approach, therefore the linear relationships between any variables could be measured. The fact that the indicator is adaptive add a certain potential, however such combination make the indicator have the drawback of kama + the correlation oscillator, which might appear at certain points.

Thanks for reading !

Adaptive ChannelThis indicator uses KAMA to adjust the length of a channel according to volatility.

A set up is generated when a candle closes below/above the mid point line; this is indicated via the background color.

Buy/sell on the break of the high/low of the signal candle.

Use the channel top/bottom as a stop (or a close above/below the mid pint line)

Powered Kaufman Adaptive Moving AverageIntroduction

The ability the Kaufman adaptive moving average (KAMA) has to be flat during ranging markets and close to the price during trending markets is what make this moving average one of the most useful in technical analysis. KAMA is calculated by using exponential averaging using the efficiency ratio (ER) as smoothing variable where 1 > ER > 0 . An increasing efficiency ratio indicate a trending market. Based on one of my latest indicator (see Kaufman Adaptive Bands) i propose this modified KAMA that allow to emphasis the abilities of KAMA by powering the efficiency ratio. I also added a new option that allow for even more adaptivity.

The Indicator

The indicator is a simple KAMA of period length that use a powered ER with exponent factor .

When factor = 1 the indicator is a simple KAMA, however when factor > 1 there can be more emphasis on the flattening effect of KAMA.

You can also restrain this effect by using 1 > factor > 0

Note that when the exponent is lower than 1 and greater than 0 you are basically applying a nth square root to the value, for example pow(2,0.5) = sqrt(2) because 1/0.5 = 2, in our case :

pow(ER,factor > 1) < ER and pow(ER,1 > factor > 0) > ER

Self Powered P-KAMA

When the self powered option is checked you are basically powering ER with the reciprocal of ER as exponent, however factor does no longer change anything. This can give interesting results since the exponent depend on the market trend strength.

In orange the self powered KAMA of period length = 50 and in blue a basic powered KAMA with a factor of 3 and a period of length = 50.

Conclusion

Applying basic math to indicators is always fun and easy to do, if you have adaptive moving averages using exponential averaging try powering your smoothing variable in order to see interesting results. I hope you like this indicator. Thanks for reading !

Kaufman Adaptive BandsIntroduction

Bands are quite efficient in technical analysis, they can provide support and resistance levels, provide breakouts points, trailing stop loss/take profits positions and can show the current market volatility to the user. Most of the time bands are made from a central tendency estimator like a moving average plus/minus a volatility indicator. Therefore bands can be made out of pretty much everything thus allowing for any kind of flavors.

So i propose a band indicator made from a Kaufman adaptive moving average using an estimate of the standard deviation.

Construction

The Kaufman moving average is an exponential averager using the efficiency ratio as smoothing variable, length control the period of kama and in order to provide more smoothness a power parameter has been introduced, higher values of power will return smoother results.

The volatility indicator is made from a biased estimation of the standard deviation by using the square root of the mean of the square minus the square of the mean method, except that we use kama instead of a mean.

The bands are made by adding/subtracting this volatility indicator with kama.

How To Use

The ability of the indicator to adapt to the current market state is what makes him a great tool for avoiding major exposition during ranging market, therefore the indicator will have a greater motion during trending market, or more simply the bands will move during trending markets while staying "flat" during ranging ones. Therefore the indicator might be more suited to breakouts, even if some cases will return what where turning points, this is particularly true during ranging markets.

Of course the efficiency ratio is not an "unbiased" trend metric indicator, it can consider high volatility markets as trending markets. Its one of his downsides.

High values of power will create smoother bands.

When using a low power parameter use an higher mult. In general using a low power value will make the bands move more freely as well as making them closer to each others.

Conclusion

At least the indicator is really nice to the eyes when using high power values, its ability to adapt to the market is a great addition to other more classical bands indicators, i also introduced a volatility estimator based on kama, some might have used the following estimation : kama(abs(price - kama)) which would have created a slower result. A trailing stop might be made from it if i see request about such addition.

If you are curious here are some more images of the indicator performing on different markets. Thanks for reading !

Koby's 3 average MACD indicatorThis MACD is averaging 3 different MACD; KAMA MACD, ZLEMA MACD, and normal MACD.

Can find easier MACD's divergence and convergence than normal MACD.

And more smoothly drawing than ZLEMA MACD (KZ_MACD) which is I've made before.

Koby's ZLEMA MACD and KAMA signalUsing zero lag ema for MACD line, and using KAMA for MACD's signal line.

Test version.

This has MACD and signal cross alert, and 0 line alert.

Bryant Adaptive Moving Average@ChartArt got my attention to this idea.

This type of moving average was originally developed by Michael R. Bryant (Adaptrade Software newsletter, April 2014). Mr. Bryant suggested a new approach, so called Variable Efficiency Ratio (VER), to obtain adaptive behaviour for the moving average. This approach is based on Perry Kaufman' idea with Efficiency Ratio (ER) which was used by Mr. Kaufman to create KAMA.

As result Mr. Bryant got a moving average with adaptive lookback period. This moving average has 3 parameters:

Initial lookback

Trend Parameter

Maximum lookback

The 2nd parameter, Trend Parameter can take any positive or negative value and determines whether the lookback length will increase or decrease with increasing ER.

Changing Trend Parameter we can obtain KAMA' behaviour

To learn more see www.adaptrade.com

Kaufman Adaptive Moving AverageKaufman Adaptive Moving Average script.

This indicator was originally developed by Perry J. Kaufman (`Smarter Trading: Improving Performance in Changing Markets`, 1995).

colorsi just put it for for who ever want it.. it has some issue of repaint . put on 1 day frame in hlc box ,so it can solve the issue to some extent. based on Marco code with some modification

i hope someone will be able to fix the code and make it better :)

MA Study: Different Types and More [NeoButane]A study of moving averages that utilizes different tricks I've learned to optimize them. Included is Bollinger Bands, Guppy (GMMA) and Super Guppy.

The method used to make it MtF should be more precise and smoother than regular MtF methods that use the security function. For intraday timeframes, each number represents each hour, with 24 equal to 1 day. For daily, 3 is 3 day, for weekly, 4 is the 4 weekly, etc. If you're on a higher timeframe than the one selected, the length will not change.

Log-space is used to make calculations work on many cryptos. The rules for color changing Guppy is changed to make it not as choppy on MAs other than EMA. Note that length does not affect SWMA and VWAP and source does not affect VWAP.

A short summary of each moving average can be found here: medium.com

List of included MAs:

ALMA: Arnaud Legoux

Double EMA

EMA: Exponential

Hull MA

KAMA: Kaufman Adaptive

Linear Regression Curve

LSMA: Least Squares

SMA: Simple

SMMA/RMA: Smoothed/Running

SWMA: Symm. Weighted

TMA: Triangular

Triple EMA

VWMA: Volume Weighted

WMA: Weighted

ZLEMA: Zero Lag

VWAP: Vol Weighted Average

Welles Wilder MA