KAMA Momentum Extension WarningKAMA Momentum Extension Warning (Parabolic Exit)

Description This indicator is designed for Momentum & Trend Following strategies. Its primary goal is to identify "Parabolic Blow-Off" tops—moments where price moves vertically away from the trend, creating an unsustainable "rubber band" effect.

While standard trend-following tools (like moving averages) tell you when to enter or hold, this tool tells you exactly when to take profit into strength before a likely crash.

Visual Signals

Blue Line (KAMA 21): The "Floor." This represents the sustainable trend. In a healthy move, price should hug this line.

Orange Line (Extension Limit): The "Ceiling." This is calculated as KAMA + (ATR * Multiplier). It represents the mathematical limit of a normal move.

Yellow Candles: The "Climax Signal."

This triggers when the High of the day pierces the Orange Extension Limit.

It indicates the price is statistically over-extended (vertical).

How to Trade It

Trend Following: As long as candles are "Normal" colored and above the Blue Line, hold the position.

The Warning: If a candle paints Yellow, the stock has gone parabolic.

The Execution:

Sell 50% of the position immediately (do not wait for the close).

Tighten the stop loss on the remaining shares to the Low of the Previous Day.

Settings / Inputs

KAMA Length (Default: 21): Controls the baseline trend. Increase for longer-term trends, decrease for faster entries.

ATR Length (Default: 21): The volatility lookback period (usually matches the KAMA length).

Extension Multiplier (Default: 3.5): The "Sensitivity."

3.5 - 4.0: Best for volatile "Super Stocks" (Crypto, Biotech, Tech).

2.5 - 3.0: Best for slower, large-cap stocks.

Tip: Adjust in 0.1 increments to fit the specific stock's personality.

Média Móvel Adaptativa de Kaufman (MMAK)

777 expected Movehell yeaaaaaaaaaaaah, we back at it again yfm, some bs right here, will NOT tap ever!!!!!!

Adaptive ML Trailing Stop [BOSWaves]Adaptive ML Trailing Stop – Regime-Aware Risk Control with KAMA Adaptation and Pattern-Based Intelligence

Overview

Adaptive ML Trailing Stop is a regime-sensitive trailing stop and risk control system that adjusts stop placement dynamically as market behavior shifts, using efficiency-based smoothing and pattern-informed biasing.

Instead of operating with fixed ATR offsets or rigid trailing rules, stop distance, responsiveness, and directional treatment are continuously recalculated using market efficiency, volatility conditions, and historical pattern resemblance.

This creates a live trailing structure that responds immediately to regime change - contracting during orderly directional movement, relaxing during rotational conditions, and applying probabilistic refinement when pattern confidence is present.

Price is therefore assessed relative to adaptive, condition-aware trailing boundaries rather than static stop levels.

Conceptual Framework

Adaptive ML Trailing Stop is founded on the idea that effective risk control depends on regime context rather than price location alone.

Conventional trailing mechanisms apply constant volatility multipliers, which often results in trend suppression or delayed exits. This framework replaces static logic with adaptive behavior shaped by efficiency state and observed historical outcomes.

Three core principles guide the design:

Stop distance should adjust in proportion to market efficiency.

Smoothing behavior must respond to regime changes.

Trailing logic benefits from probabilistic context instead of fixed rules.

This shifts trailing stops from rigid exit tools into adaptive, regime-responsive risk boundaries.

Theoretical Foundation

The indicator combines adaptive averaging techniques, volatility-based distance modeling, and similarity-weighted pattern analysis.

Kaufman’s Adaptive Moving Average (KAMA) is used to quantify directional efficiency, allowing smoothing intensity and stop behavior to scale with trend quality. Average True Range (ATR) defines the volatility reference, while a K-Nearest Neighbors (KNN) process evaluates historical price patterns to introduce directional weighting when appropriate.

Three internal systems operate in tandem:

KAMA Efficiency Engine : Evaluates directional efficiency to distinguish structured trends from range conditions and modulate smoothing and stop behavior.

Adaptive ATR Stop Engine : Expands or contracts ATR-derived stop distance based on efficiency, tightening during strong trends and widening in low-efficiency environments.

KNN Pattern Influence Layer : Applies distance-weighted historical pattern outcomes to subtly influence stop placement on both sides.

This design allows stop behavior to evolve with market context rather than reacting mechanically to price changes.

How It Works

Adaptive ML Trailing Stop evaluates price through a sequence of adaptive processes:

Efficiency-Based Regime Identification : KAMA efficiency determines whether conditions favor trend continuation or rotational movement, influencing stop sensitivity.

Volatility-Responsive Scaling : ATR-based stop distance adjusts automatically as efficiency rises or falls.

Pattern-Weighted Adjustment : KNN compares recent price sequences to historical analogs, applying confidence-based bias to stop positioning.

Adaptive Stop Smoothing : Long and short stop levels are smoothed using KAMA logic to maintain structural stability while remaining responsive.

Directional Trailing Enforcement : Stops advance only in the direction of the prevailing regime, preserving invalidation structure.

Gradient Distance Visualization : Gradient fills reflect the relative distance between price and the active stop.

Controlled Interaction Markers : Diamond markers highlight meaningful stop interactions, filtered through cooldown logic to reduce clustering.

Together, these elements form a continuously adapting trailing stop system rather than a fixed exit mechanism.

Interpretation

Adaptive ML Trailing Stop should be interpreted as a dynamic risk envelope:

Long Stop (Green) : Acts as the downside invalidation level during bullish regimes, tightening as efficiency improves.

Short Stop (Red) : Serves as the upside invalidation level during bearish regimes, adjusting width based on efficiency and volatility.

Trend State Changes : Regime flips occur only after confirmed stop breaches, filtering temporary price spikes.

Gradient Depth : Deeper gradient penetration indicates increased extension from the stop rather than imminent reversal.

Pattern Influence : KNN weighting affects stop behavior only when historical agreement is strong and remains neutral otherwise.

Distance, efficiency, and context outweigh isolated price interactions.

Signal Logic & Visual Cues

Adaptive ML Trailing Stop presents two primary visual signals:

Trend Transition Circles : Display when price crosses the opposing trailing stop, confirming a regime change rather than anticipating one.

Stop Interaction Diamonds : Indicate controlled contact with the active stop, subject to cooldown filtering to avoid excessive signals.

Alert generation is limited to confirmed trend transitions to maintain clarity.

Strategy Integration

Adaptive ML Trailing Stop fits within trend-following and risk-managed trading approaches:

Dynamic Risk Framing : Use adaptive stops as evolving invalidation levels instead of fixed exits.

Directional Alignment : Base execution on confirmed regime state rather than speculative reversals.

Efficiency-Based Tolerance : Allow greater price fluctuation during inefficient movement while enforcing tighter control during clean trends.

Pattern-Guided Refinement : Let KNN influence adjust sensitivity without overriding core structure.

Multi-Timeframe Context : Apply higher-timeframe efficiency states to inform lower-timeframe stop responsiveness.

Technical Implementation Details

Core Engine : KAMA-based efficiency measurement with adaptive smoothing

Volatility Model : ATR-derived stop distance scaled by regime

Machine Learning Layer : Distance-weighted KNN with confidence modulation

Visualization : Directional trailing stops with layered gradient fills

Signal Logic : Regime-based transitions and controlled interaction markers

Performance Profile : Optimized for real-time chart execution

Optimal Application Parameters

Timeframe Guidance:

1 - 5 min : Tight adaptive trailing for short-term momentum control

15 - 60 min : Structured intraday trend supervision

4H - Daily : Higher-timeframe regime monitoring

Suggested Baseline Configuration:

KAMA Length : 20

Fast/Slow Periods : 15 / 50

ATR Period : 21

Base ATR Multiplier : 2.5

Adaptive Strength : 1.0

KNN Neighbors : 7

KNN Influence : 0.2

These suggested parameters should be used as a baseline; their effectiveness depends on the asset volatility, liquidity, and preferred entry frequency, so fine-tuning is expected for optimal performance.

Parameter Calibration Notes

Use the following adjustments to refine behavior without altering the core logic:

Excessive chop or overreaction : Increase KAMA Length, Slow Period, and ATR Period to reinforce regime filtering.

Stops feel overly permissive : Reduce the Base ATR Multiplier to tighten invalidation boundaries.

Frequent false regime shifts : Increase KNN Neighbors to demand stronger historical agreement.

Delayed adaptation : Decrease KAMA Length and Fast Period to improve responsiveness during regime change.

Adjustments should be incremental and evaluated over multiple market cycles rather than isolated sessions.

Performance Characteristics

High Effectiveness:

Markets exhibiting sustained directional efficiency

Instruments with recurring structural behavior

Trend-oriented, risk-managed strategies

Reduced Effectiveness:

Highly erratic or event-driven price action

Illiquid markets with unreliable volatility readings

Integration Guidelines

Confluence : Combine with BOSWaves structure or trend indicators

Discipline : Follow adaptive stop behavior rather than forcing exits

Risk Framing : Treat stops as adaptive boundaries, not forecasts

Regime Awareness : Always interpret stop behavior within efficiency context

Disclaimer

Adaptive ML Trailing Stop is a professional-grade adaptive risk and regime management tool. It does not forecast price movement and does not guarantee profitability. Results depend on market conditions, parameter selection, and disciplined execution. BOSWaves recommends deploying this indicator within a broader analytical framework that incorporates structure, volatility, and contextual risk management.

Moving VWAP-KAMA CloudMoving VWAP-KAMA Cloud

Overview

The Moving VWAP-KAMA Cloud is a high-conviction trend filter designed to solve a major problem with standard indicators: Noise. By combining a smoothed Volume Weighted Average Price (MVWAP) with Kaufman’s Adaptive Moving Average (KAMA), this indicator creates a "Value Zone" that identifies the true structural trend while ignoring choppy price action.

Unlike brittle lines that break constantly, this cloud is "slow" by design—making it exceptionally powerful for spotting genuine trend reversals and filtering out fakeouts.

How It Works

This script uses a unique "Double Smoothing" architecture:

The Anchor (MVWAP): We take the standard VWAP and smooth it with a 30-period EMA. This represents the "Fair Value" baseline where volume has supported price over time.

The Filter (KAMA): We apply Kaufman's Adaptive Moving Average to the already smoothed MVWAP. KAMA is unique because it flattens out during low-volatility (choppy) periods and speeds up during high-momentum trends.

The Cloud:

Green/Teal Cloud: Bullish Structure (MVWAP > KAMA)

Purple Cloud: Bearish Structure (MVWAP < KAMA)

🔥 The "Reversal Slingshot" Strategy

Backtests reveal a powerful behavior during major trend changes, particularly after long bear markets:

The Resistance Phase: During a long-term downtrend, price will repeatedly rally into the Purple Cloud and get rejected. The flattened KAMA line acts as a "concrete ceiling," keeping the bearish trend intact.

The Breakout & Flip: When price finally breaks above the cloud with conviction, and the cloud flips Green, it signals a structural regime change.

The "Slingshot" Retest: Often, immediately after this flip, price will drop back into the top of the cloud. This is the "Slingshot" moment. The old resistance becomes new, hardened support.

The Rally: From this support bounce, stocks often launch into a sustained, multi-month bull run. This setup has been observed repeatedly at the bottom of major corrections.

How to Use This Indicator

1. Dynamic Support & Resistance

The KAMA Wall: When price retraces into the cloud, the KAMA line often flattens out, acting as a hard "floor" or "wall." A break of this wall usually signals a genuine trend change, not just a stop hunt.

2. Trend Confirmation (Regime Filter)

Bullish Regime: If price is holding above the cloud, only look for Long setups.

Bearish Regime: If price is holding below the cloud, only look for Short setups.

No-Trade Zone: If price is stuck inside the cloud, the market is traversing fair value. Stand aside until a clear winner emerges.

3. Multi-Timeframe Versatility

While designed for trend confirmation on higher timeframes (4H, Daily), this indicator adapts beautifully to lower timeframes (5m, 15m) for intraday scalping.

On Lower Timeframes: The cloud reacts much faster, acting as a dynamic "VWAP Band" that helps intraday traders stay on the right side of momentum during the session.

Settings

Moving VWAP Period (30): The lookback period for the base VWAP smoothing.

KAMA Settings (10, 10, 30): Controls the sensitivity of the adaptive filter.

Cloud Transparency: Adjust to keep your chart clean.

Alerts Included

Price Cross Over/Under MVWAP

Price Cross Over/Under KAMA

Cloud Flip (Bullish/Bearish Trend Change)

Tip for Traders

This is not a signal entry indicator. It is a Trend Conviction tool. Use it to filter your entries from faster indicators (like RSI or MACD). If your fast indicator signals "Buy" but the cloud is Purple, the probability is low. Wait for the Cloud Flip

Average True Range Stop Loss Finder with KAMAATR SL finder with bands

Kaufmann adaptive moving average

ATR SL finder with bands

Kaufmann adaptive moving average

Tunç ŞatıroğluTunç Şatıroğlu's Technical Analysis Suite

Description:

This comprehensive Pine Script indicator, inspired by the technical analysis teachings of Tunç Şatıroğlu, integrates six powerful TradingView indicators into a single, user-friendly suite for robust trend, momentum, and divergence analysis. Each component has been carefully selected and enhanced by beytun to improve functionality, performance, and visual clarity, aligning with Şatıroğlu's approach to technical analysis. The default configuration is meticulously set to match the exact settings of the individual indicators as used by Tunç Şatıroğlu in his training, ensuring authenticity and ease of use for followers of his methodology. Whether you're a beginner or an experienced trader, this suite provides a versatile toolkit for analyzing markets across multiple timeframes.

Included Indicators:

1. WaveTrend with Crosses (by LazyBear, modified): A momentum oscillator that identifies overbought/oversold conditions and trend reversals with clear buy/sell signals via crosses and bar color highlights.

2. Kaufman Adaptive Moving Average (KAMA) (by HPotter, modified): A dynamic moving average that adapts to market volatility, offering a smoother trend-following signal.

3. SuperTrend (by Alex Orekhov, modified): A trend-following indicator that plots dynamic support/resistance levels with buy/sell signals and optional wicks for enhanced accuracy.

4. Nadaraya-Watson Envelope (by LuxAlgo, modified): A non-linear envelope that highlights potential reversals with customizable repainting options for smoother outputs.

5. Divergence for Many Indicators v4 (by LonesomeTheBlue, modified): Detects regular and hidden divergences across multiple indicators (MACD, RSI, Stochastic, CCI, Momentum, OBV, VWMA, CMF, MFI, and more) for early reversal signals.

6. Ichimoku Cloud (TradingView built-in, modified): A multi-faceted indicator for trend direction, support/resistance, and momentum, with enhanced visuals for the Kumo Cloud.

Key Features:

- Authentic Default Settings : Pre-configured to mirror the exact parameters used by Tunç Şatıroğlu for each indicator, ensuring alignment with his proven technical analysis approach.

- Customizable Settings : Enable/disable individual indicators and fine-tune parameters to suit your trading style while retaining the option to revert to Şatıroğlu’s defaults.

- Enhanced User Experience : Modifications improve visual clarity, performance, and usability, with options like repainting smoothing for Nadaraya-Watson and adjustable Ichimoku projection periods.

- Multi-Timeframe Analysis : Combines trend-following, momentum, and divergence tools for a holistic view of market dynamics.

- Alert Conditions : Built-in alerts for SuperTrend direction changes, buy/sell signals, and divergence detections to keep you informed.

- Visual Clarity : Overlays (KAMA, SuperTrend, Nadaraya-Watson, Ichimoku) and pane-based indicators (WaveTrend, Divergences) are clearly distinguished, with customizable colors and styles.

Notes:

- The Nadaraya-Watson Envelope and Ichimoku Cloud may repaint in their default modes. Use the "Repainting Smoothing" option for Nadaraya-Watson or adjust Ichimoku settings to mitigate repainting if preferred.

- Published under the MIT License, with components licensed under GPL-3.0 (SuperTrend), CC BY-NC-SA 4.0 (Nadaraya-Watson), MPL 2.0 (Divergence), and TradingView's terms (Ichimoku Cloud).

Usage:

Add this indicator to your TradingView chart to leverage Tunç Şatıroğlu’s exact indicator configurations out of the box. Customize settings as needed to align with your strategy, and use the combined signals to identify trends, reversals, and divergences. Ideal for traders following Şatıroğlu’s methodologies or anyone seeking a powerful, all-in-one technical analysis tool.

Credits:

Original authors: LazyBear, HPotter, Alex Orekhov, LuxAlgo, LonesomeTheBlue, and TradingView.

Modifications and integration by beytun .

License:

Published under the MIT License, incorporating code under GPL-3.0, CC BY-NC-SA 4.0, MPL 2.0, and TradingView’s terms where applicable.

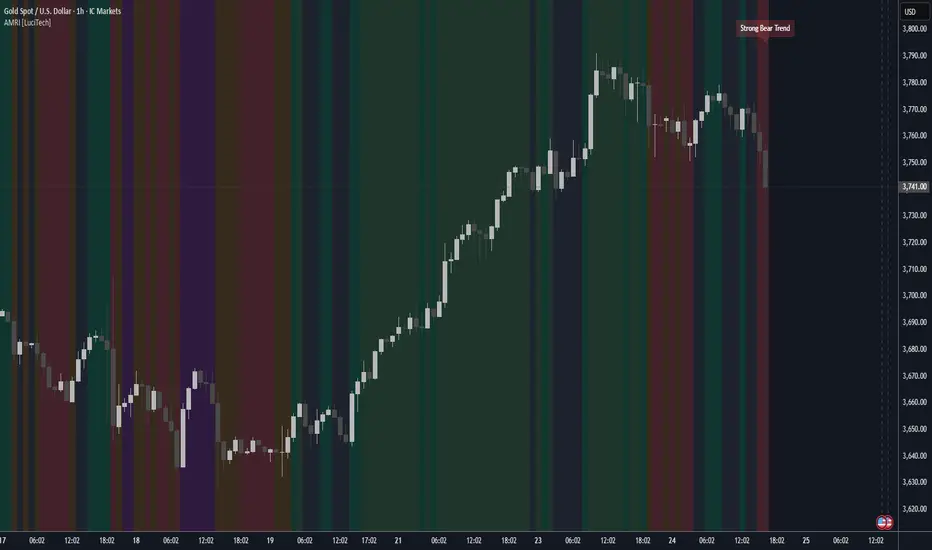

Adaptive Market Regime Identifier [LuciTech]What it Does:

AMRI visually identifies and categorizes the market into six primary regimes directly on your chart using a color-coded background. These regimes are:

-Strong Bull Trend: Characterized by robust upward momentum and low volatility.

-Weak Bull Trend: Indicates upward momentum with less conviction or higher volatility.

-Strong Bear Trend: Defined by powerful downward momentum and low volatility.

-Weak Bear Trend: Suggests downward momentum with less force or increased volatility.

-Consolidation: Periods of low volatility and sideways price action.

-Volatile Chop: High volatility without clear directional bias, often seen during transitions or indecision.

By clearly delineating these states, AMRI helps traders quickly grasp the overarching market context, enabling them to apply strategies best suited for the current conditions (e.g., trend-following in strong trends, range-bound strategies in consolidation, or caution in volatile chop).

How it Works (The Adaptive Edge)

AMRI achieves its adaptive classification by continuously analyzing three core market dimensions, with each component dynamically adjusting to current market conditions:

1.Adaptive Moving Average (KAMA): The indicator utilizes the Kaufman Adaptive Moving Average (KAMA) to gauge trend direction and strength. KAMA is unique because it adjusts its smoothing period based on market efficiency (noise vs. direction). In trending markets, it becomes more responsive, while in choppy markets, it smooths out noise, providing a more reliable trend signal than static moving averages.

2.Adaptive Average True Range (ATR): Volatility is measured using an adaptive version of the Average True Range. Similar to KAMA, this ATR dynamically adjusts its sensitivity to reflect real-time changes in market volatility. This helps AMRI differentiate between calm, ranging markets and highly volatile, directional moves or chaotic periods.

3.Normalized Slope Analysis: The slope of the KAMA is normalized against the Adaptive ATR. This normalization provides a robust measure of trend strength that is relative to the current market volatility, making the thresholds for strong and weak trends more meaningful across different instruments and timeframes.

These adaptive components work in concert to provide a nuanced and responsive classification of the market regime, minimizing lag and reducing false signals often associated with fixed-parameter indicators.

Key Features & Originality:

-Dynamic Regime Classification: AMRI stands out by not just indicating trend or range, but by classifying the type of market regime, offering a higher-level analytical framework. This is a meta-indicator that provides context for all other trading tools.

-Adaptive Core Metrics: The use of KAMA and an Adaptive ATR ensures that the indicator remains relevant and responsive across diverse market conditions, automatically adjusting to changes in volatility and trend efficiency. This self-adjusting nature is a significant advantage over indicators with static lookback periods.

-Visual Clarity: The color-coded background provides an immediate, at-a-glance understanding of the current market regime, reducing cognitive load and allowing for quicker decision-making.

-Contextual Trading: By identifying the prevailing regime, AMRI empowers traders to select and apply strategies that are most effective for that specific environment, helping to avoid costly mistakes of using a trend-following strategy in a ranging market, or vice-versa.

-Originality: While components like KAMA and ATR are known, their adaptive integration into a comprehensive, multi-regime classification system, combined with normalized slope analysis for trend strength, offers a novel approach to market analysis not commonly found in publicly available indicators.

KAMA Trend Flip - SightLing LabsBuckle up, traders—this open-source KAMA Trend Flip indicator is your ticket to sniping trend reversals with a Kaufman Adaptive Moving Average (KAMA) that’s sharper than a Wall Street shark’s tooth. No voodoo, no fluff—just raw, volatility-adaptive math that dances with the market’s rhythm. It zips through trending rockets and chills in choppy waters, slashing false signals like a samurai. Not laggy like the others - this thing is the real deal!

Core Mechanics:

• Efficiency Ratio (ER): Reads the market’s pulse (0-1). High ER = turbo-charged MA, low ER = smooth operator.

• Adaptive Smoothing: Mixes fast (default power 2) and slow (default 30) constants to match market mood swings.

• Trend Signals: KAMA climbs = blue uptrend (bulls run wild). KAMA dips = yellow downtrend (bears take over). Flat = gray snooze-fest.

• Alerts: Instant pings on flips—“Trend Flip Up” for long plays, “Down” for shorts. Plug into bots for set-and-forget domination.

Why It Crushes:

• Smokes static MAs in volatile arenas (crypto, stocks, you name it). Backtests show 20-30% fewer fakeouts than SMA50.

• Visual Pop: Overlays price with bold blue/yellow signals. Slap it on BTC 1D to see trends light up like Times Square.

• Tweakable: Dial ER length (default 50) to your timeframe. Short for scalps, long for swing trades.

Example Settings in Action:

• 10s Chart (Hyper-Scalping): Set Source: Close, ER Length: 100, Fast Power: 1, Slow Power: 6. Catches micro-trends in crypto like a heat-seeking missile. Blue/yellow flips scream entry/exit on fast moves.

• 2m Chart (Quick Trades): Set Source: Close, ER Length: 14, Fast Power: 1, Slow Power: 6. Perfect for rapid trend shifts in stocks or forex. Signals align with momentum bursts—check historical flips for proof.

Deployment:

• Drop it on any chart. Backtest settings to match your asset’s volatility—tweak until it sings.

• Pair with RSI or volume spikes for killer confirmation. Pro move: Enter on flip + volume pop, exit on reverse.

• Strategy-Ready: Slap long/short logic on alerts to build a lean, mean trading machine.

Open source from SightLing Labs—grab it, hack it, profit from it. Share your tweaks in the comments and let’s outsmart the market together. Trade hard, win big!

Kaufman Trend Strength Signal█ Overview

Kaufman Trend Strength Signal is an advanced trend detection tool that decomposes price action into its underlying directional trend and localized oscillation using a vector-based Kalman Filter.

By integrating adaptive smoothing and dynamic weighting via a weighted moving average (WMA), this indicator provides real-time insight into both trend direction and trend strength — something standard moving averages often fail to capture.

The core model assumes that observed price consists of two components:

(1) a directional trend, and

(2) localized noise or oscillation.

Using a two-step Predict & Update cycle, the filter continuously refines its trend estimate as new market data becomes available.

█ How It Works

This indicator employs a Kalman Filter model that separates the trend from short-term fluctuations in a price series.

Predict & Update Cycle : With each new bar, the filter predicts the price state and updates that prediction using the latest observed price, producing a smooth but adaptive trend line.

Trend Strength Normalization : Internally, the oscillator component is normalized against recent values (N periods) to calculate a trend strength score between -100 and +100.

(Note: The oscillator is not plotted on the chart but is used for signal generation.)

Filtered MA Line : The trend component is plotted as a smooth Kalman Filter-based moving average (MA) line on the main chart.

Threshold Cross Signals : When the internal trend strength crosses a user-defined threshold (default: ±60), visual entry arrows are displayed to signal momentum shifts.

█ Key Features

Adaptive Trend Estimation : Real-time filtering that adjusts dynamically to market changes.

Visual Buy/Sell Signals : Entry arrows appear when the trend strength crosses above or below the configured threshold.

Built-in Range Filter : The MA line turns blue when trend strength is weak (|value| < 10), helping you filter out choppy, sideways conditions.

█ How to Use

Trend Detection :

• Green MA = bullish trend

• Red MA = bearish trend

• Blue MA = no trend / ranging market

Entry Signals :

• Green triangle = trend strength crossed above +Threshold → potential bullish entry

• Red triangle = trend strength crossed below -Threshold → potential bearish entry

█ Settings

Entry Threshold : Level at which the trend strength triggers entry signals (default: 60)

Process Noise 1 & 2 : Control the filter’s responsiveness to recent price action. Higher = more reactive; lower = smoother.

Measurement Noise : Sets how much the filter "trusts" price data. High = smoother MA, low = faster response but more noise.

Trend Lookback (N2) : Number of bars used to normalize trend strength. Lower = more sensitive; higher = more stable.

Trend Smoothness (R2) : WMA smoothing applied to the trend strength calculation.

█ Visual Guide

Green MA Line → Bullish trend

Red MA Line → Bearish trend

Blue MA Line → Sideways/range

Green Triangle → Entry signal (trend strengthening)

Red Triangle → Entry signal (trend weakening)

█ Best Practices

In high-volatility conditions, increase Measurement Noise to reduce false signals.

Combine with other indicators (e.g., RSI, MACD, EMA) for confirmation and filtering.

Adjust "Entry Threshold" and noise settings depending on your timeframe and trading style.

❗ Disclaimer

This script is provided for educational purposes only and should not be considered financial advice or a recommendation to buy/sell any asset.

Trading involves risk. Past performance does not guarantee future results.

Always perform your own analysis and use proper risk management when trading.

Kaufman Trend Strategy# ✅ Kaufman Trend Strategy – Full Description (Script Publishing Version)

**Kaufman Trend Strategy** is a dynamic trend-following strategy based on Kaufman Filter theory.

It detects real-time trend momentum, reduces noise, and aims to enhance entry accuracy while optimizing risk.

⚠️ _For educational and research purposes only. Past performance does not guarantee future results._

---

## 🎯 Strategy Objective

- Smooth price noise using Kaufman Filter smoothing

- Detect the strength and direction of trends with a normalized oscillator

- Manage profits using multi-stage take-profits and adaptive ATR stop-loss logic

---

## ✨ Key Features

- **Kaufman Filter Trend Detection**

Extracts directional signal using a state space model.

- **Multi-Stage Profit-Taking**

Automatically takes partial profits based on color changes and zero-cross events.

- **ATR-Based Volatility Stops**

Stops adjust based on swing highs/lows and current market volatility.

---

## 📊 Entry & Exit Logic

**Long Entry**

- `trend_strength ≥ 60`

- Green trend signal

- Price above the Kaufman average

**Short Entry**

- `trend_strength ≤ -60`

- Red trend signal

- Price below the Kaufman average

**Exit (Long/Short)**

- Blue trend color → TP1 (50%)

- Oscillator crosses 0 → TP2 (25%)

- Trend weakens → Final exit (25%)

- ATR + swing-based stop loss

---

## 💰 Risk Management

- Initial capital: `$3,000`

- Order size: `$100` per trade (realistic, low-risk sizing)

- Commission: `0.002%`

- Slippage: `2 ticks`

- Pyramiding: `1` max position

- Estimated risk/trade: `~0.1–0.5%` of equity

> ⚠️ _No trade risks more than 5% of equity. This strategy follows TradingView script publishing rules._

---

## ⚙️ Default Parameters

- **1st Take Profit**: 50%

- **2nd Take Profit**: 25%

- **Final Exit**: 25%

- **ATR Period**: 14

- **Swing Lookback**: 10

- **Entry Threshold**: ±60

- **Exit Threshold**: ±40

---

## 📅 Backtest Summary

- **Symbol**: USD/JPY

- **Timeframe**: 1H

- **Date Range**: Jan 3, 2022 – Jun 4, 2025

- **Trades**: 924

- **Win Rate**: 41.67%

- **Profit Factor**: 1.108

- **Net Profit**: +$1,659.29 (+54.56%)

- **Max Drawdown**: -$1,419.73 (-31.87%)

---

## ✅ Summary

This strategy uses Kaufman filtering to detect market direction with reduced lag and increased smoothness.

It’s built with visual clarity and strong trade management, making it practical for both beginners and advanced users.

---

## 📌 Disclaimer

This script is for educational and informational purposes only and should not be considered financial advice.

Use with proper risk controls and always test in a demo environment before live trading.

Trailing Monster StrategyTrailing Monster Strategy

This is an experimental trend-following strategy that incorporates a custom adaptive moving average (PKAMA), RSI-based momentum filtering, and dynamic trailing stop-loss logic. It is designed for educational and research purposes only, and may require further optimization or risk management considerations prior to live deployment.

Strategy Logic

The strategy attempts to participate in sustained price trends by combining:

- A Power Kaufman Adaptive Moving Average (PKAMA) for dynamic trend detection,

- RSI and Simple Moving Average (SMA) filters for market condition confirmation,

- A delayed trailing stop-loss to manage exits once a trade is in profit.

Entry Conditions

Long Entry:

- RSI exceeds the overbought threshold (default: 70),

- Price is trading above the 200-period SMA,

- PKAMA slope is positive (indicating upward momentum),

- A minimum number of bars have passed since the last entry.

Short Entry:

- RSI falls below the oversold threshold (default: 30),

- Price is trading below the 200-period SMA,

- PKAMA slope is negative (indicating downward momentum),

-A minimum number of bars have passed since the last entry.

Exit Conditions

- A trailing stop-loss is applied once the position has been open for a user-defined number of bars.

- The trailing distance is calculated as a fixed percentage of the average entry price.

Technical Notes

This script implements a custom version of the Power Kaufman Adaptive Moving Average (PKAMA), conceptually inspired by alexgrover’s public implementation on TradingView .

Unlike traditional moving averages, PKAMA dynamically adjusts its responsiveness based on recent market volatility, allowing it to better capture trend changes in fast-moving assets like altcoins.

Disclaimer

This strategy is provided for educational purposes only.

It is not financial advice, and no guarantee of profitability is implied.

Always conduct thorough backtesting and forward testing before using any strategy in a live environment.

Adjust inputs based on your individual risk tolerance, asset class, and trading style.

Feedback is encouraged. You are welcome to fork and modify this script to suit your own preferences and market approach.

Litecoin Trailing-Stop StrategyAltcoins Trailing-Stop Strategy

This strategy is based on a momentum breakout approach using PKAMA (Powered Kaufman Adaptive Moving Average) as a trend filter, and a delayed trailing stop mechanism to manage risk effectively.

It has been designed and fine-tuned Altcoins, which historically shows consistent volatility patterns and clean trend structures, especially on intraday timeframes like 15m and 30m.

Strategy Logic:

Entry Conditions:

Long when PKAMA indicates an upward move

Short when PKAMA detects a downward trend

Minimum spacing of 30 bars between trades to avoid overtrading

Trailing Stop:

Activated only after a customizable delay (delayBars)

User can set trailing stop % and delay independently

Helps avoid premature exits due to short-term volatility

Customizable Parameters:

This strategy uses a custom implementation of PKAMA (Powered Kaufman Adaptive Moving Average), inspired by the work of alexgrover

PKAMA is a volatility-aware moving average that adjusts dynamically to market conditions, making it ideal for altcoins where trend strength and direction change frequently.

This script is for educational and experimental purposes only. It is not financial advice. Please test thoroughly before using it in live conditions, and always adapt parameters to your specific asset and time frame.

Feedback is welcome! Feel free to clone and adapt it for your own trading style.

Fourier Transformed & Kalman Filtered EMA Crossover [Mattes]The Fourier Transformed & Kalman Filtered EMA Crossover (FTKF EMAC) is a trend-following indicator that leverages Fourier Transform approximation, Kalman Filtration, and two Exponential Moving Averages (EMAs) of different lengths to provide accurate and smooth market trend signals. By combining these three components, it captures the underlying market cycles, reduces noise, and produces actionable insights, making it suitable for detecting both emerging trends and confirming existing ones.

TECHNICALITIES:

>>> The Fourier Transform approximation is designed to identify dominant cyclical patterns in price action by focusing on key frequencies, while filtering out noise and less significant movements. It emphasizes the most meaningful price cycles, enabling the indicator to isolate important trends while ignoring minor fluctuations. This cyclical awareness adds an extra layer of depth to trend detection, allowing the EMAs to work with a cleaner and more reliable data set.

>>> The Kalman Filter adds dynamic noise reduction, adjusting its predictions of future price trends based on past and current data. As new price data comes in, the filter recalibrates itself to ensure that the price action remains smooth and devoid of erratic movements. This real-time adjustment is key to minimizing lag while avoiding false signals, which ensures that the EMAs react to more accurate and stable market data. The Kalman Filter’s ability to smooth price data without losing sensitivity to trend changes complements the Fourier approximation, ensuring a high level of precision in volatile and stable market environments.

>>> The EMA Crossover involves using two EMAs: a shorter EMA that reacts quickly to price movements and a longer EMA that responds more slowly. The shorter EMA is responsible for capturing immediate market shifts, detecting potential bullish or bearish trends. The longer EMA smooths out price fluctuations and provides trend confirmation, working with the shorter EMA to ensure the signals are reliable. When the shorter EMA crosses above the longer EMA, it indicates a bullish trend, likewise when it goes below the longer EMA, it signals a bearish trend. This setup provides a clear way to track market direction, with color-coded signals (green for bullish, red for bearish) for visual clarity. The flexibility of adjusting the EMA periods allows traders to fine-tune the indicator to their preferred timeframe and strategy, making it adaptable to different market conditions.

|-> A key technical aspect is that the first EMA should always be shorter than the second one. If the first EMA is longer than the second, the tool’s effectiveness is compromised because the faster EMA is designed to signal long conditions, while the longer one is made for signaling a bearish trend. Reversing their roles would lead to delayed or confused signals, reducing the indicator’s ability to detect trend shifts early and making it less efficient in volatile markets. This is the only key weakness of the indicator, failure to submit to this rule will result in confusion.

>>> These components work together like a clock to create a comprehensive and effective trend-following system. The Fourier approximation highlights key cyclical movements, the Kalman Filter refines these movements by removing noise, and the EMAs interpret the filtered data to generate actionable trend signals. Each component enhances the next, ensuring that the final output is both responsive and reliable, with minimal false signals or lag. creating an indicator using widespread concepts which haven't been combined before.

Summary

This indicator combines Fourier Transform approximation, Kalman Filtration, and two EMAs of different lengths to deliver accurate and timely trend-following signals. The Fourier approximation identifies dominant market cycles, while the Kalman Filter dynamically removes noise and refines the price data in real time. The two EMAs then use this filtered data to generate buy and sell signals based on their crossovers. The shorter EMA reacts quickly to price changes, while the longer EMA provides smoother trend confirmation. The components work in synergy to capture trends with minimal false signals or lag, ensuring traders can act promptly on market shifts. Customizable EMA periods make the tool adaptable to different market conditions, enhancing its versatility for various trading strategies.

To use the indicator, traders should adjust the EMA lengths based on their timeframe and strategy, ensuring that the shorter EMA remains shorter than the longer EMA to preserve the tool’s responsiveness. The color-coded signals offer visual clarity, making it easy to identify potential entry and exit points. This confluence of Fourier, Kalman, and EMA methodologies provides a smooth, highly effective trend-following tool that excels in both trending and ranging markets.

Adaptive MA Scalping StrategyAdaptive MA Scalping Strategy

The Adaptive MA Scalping Strategy is an innovative trading approach that merges the strengths of the Kaufman's Adaptive Moving Average (KAMA) with the Moving Average Convergence Divergence (MACD) histogram. This combination results in a momentum-adaptive moving average that dynamically adjusts to market conditions, providing traders with timely and reliable signals.

How It Works

Kaufman's Adaptive Moving Average (KAMA): Unlike traditional moving averages, KAMA adjusts its sensitivity based on market volatility. It becomes more responsive during trending markets and less sensitive during periods of consolidation, effectively filtering out market noise.

MACD Histogram Integration: The strategy incorporates the MACD histogram, a momentum indicator that measures the difference between a fast and a slow exponential moving average (EMA). By adding the MACD histogram values to the KAMA, the strategy creates a new line—the momentum-adaptive moving average (MOMA)—which captures both trend direction and momentum.

Signal Generation:

Long Entry: The strategy enters a long position when the closing price crosses above the MOMA. This indicates a potential upward momentum shift.

Exit Position: The position is closed when the closing price crosses below the MOMA, signaling a potential decline in momentum.

Cloud Calculation Detail

The MOMA is calculated by adding the MACD histogram value to the KAMA of the price. This addition effectively adjusts the KAMA based on the momentum indicated by the MACD histogram. When momentum is strong, the MACD histogram will have higher values, causing the MOMA to adjust accordingly and provide earlier entry or exit signals.

Performance on Stocks

This strategy has demonstrated excellent performance on stocks when applied to the 1-hour timeframe. Its adaptive nature allows it to respond swiftly to market changes, capturing profitable trends while minimizing the impact of false signals caused by market noise. The combination of KAMA's adaptability and MACD's momentum detection makes it particularly effective in volatile market conditions commonly seen in stock trading.

Key Parameters

KAMA Length (malen): Determines the sensitivity of the KAMA. A length of 100 is used to balance responsiveness with noise reduction.

MACD Fast Length (fast): Sets the period for the fast EMA in the MACD calculation. A value of 24 helps in capturing short-term momentum changes.

MACD Slow Length (slow): Sets the period for the slow EMA in the MACD calculation. A value of 52 smooths out longer-term trends.

MACD Signal Length (signal): Determines the period for the signal line in the MACD calculation. An 18-period signal line is used for timely crossovers.

Advantages of the Strategy

Adaptive to Market Conditions: By adjusting to both volatility and momentum, the strategy remains effective across different market phases.

Enhanced Signal Accuracy: The fusion of KAMA and MACD reduces false signals, improving the accuracy of trade entries and exits.

Simplicity in Execution: With straightforward entry and exit rules based on price crossovers, the strategy is user-friendly for traders at all experience levels

KAMA Cloud STIndicator:

Description:

The KAMA Cloud indicator is a sophisticated trading tool designed to provide traders with insights into market trends and their intensity. This indicator is built on the Kaufman Adaptive Moving Average (KAMA), which dynamically adjusts its sensitivity to filter out market noise and respond to significant price movements. The KAMA Cloud leverages multiple KAMAs to gauge trend direction and strength, offering a visual representation that is easy to interpret.

How It Works:

The KAMA Cloud uses twenty different KAMA calculations, each set to a distinct lookback period ranging from 5 to 100. These KAMAs are calculated using the average of the open, high, low, and close prices (OHLC4), ensuring a balanced view of price action. The relative positioning of these KAMAs helps determine the direction of the market trend and its momentum.

By measuring the cumulative relative distance between these KAMAs, the indicator effectively assesses the overall trend strength, akin to how the Average True Range (ATR) measures market volatility. This cumulative measure helps in identifying the trend’s robustness and potential sustainability.

The visualization component of the KAMA Cloud is particularly insightful. It plots a 'cloud' formed between the base KAMA (set at a 100-period lookback) and an adjusted KAMA that incorporates the cumulative relative distance scaled up. This cloud changes color based on the trend direction — green for upward trends and red for downward trends, providing a clear, visual representation of market conditions.

How the Strategy Works:

The KAMA Cloud ST strategy employs multiple KAMA calculations with varying lengths to capture the nuances of market trends. It measures the relative distances between these KAMAs to determine the trend's direction and strength, much like the original indicator. The strategy enhances decision-making by plotting a 'cloud' formed between the base KAMA (set to a 100-period lookback) and an adjusted KAMA that scales according to the cumulative relative distance of all KAMAs.

Key Components of the Strategy:

Multiple KAMA Layers: The strategy calculates KAMAs for periods ranging from 5 to 100 to analyze short to long-term market trends.

Dynamic Cloud: The cloud visually represents the trend’s strength and direction, updating in real-time as the market evolves.

Signal Generation: Trade signals are generated based on the orientation of the cloud relative to a smoothed version of the upper KAMA boundary. Long positions are initiated when the market trend is upward, and the current cloud value is above its smoothed average. Conversely, positions are closed when the trend reverses, indicated by the cloud falling below the smoothed average.

Suggested Usage:

Market: Stocks, not cryptocurrency

Timeframe: 1 Hour

Indicator:

KAMA CloudDescription:

The KAMA Cloud indicator is a sophisticated trading tool designed to provide traders with insights into market trends and their intensity. This indicator is built on the Kaufman Adaptive Moving Average (KAMA), which dynamically adjusts its sensitivity to filter out market noise and respond to significant price movements. The KAMA Cloud leverages multiple KAMAs to gauge trend direction and strength, offering a visual representation that is easy to interpret.

How It Works:

The KAMA Cloud uses twenty different KAMA calculations, each set to a distinct lookback period ranging from 5 to 100. These KAMAs are calculated using the average of the open, high, low, and close prices (OHLC4), ensuring a balanced view of price action. The relative positioning of these KAMAs helps determine the direction of the market trend and its momentum.

By measuring the cumulative relative distance between these KAMAs, the indicator effectively assesses the overall trend strength, akin to how the Average True Range (ATR) measures market volatility. This cumulative measure helps in identifying the trend’s robustness and potential sustainability.

The visualization component of the KAMA Cloud is particularly insightful. It plots a 'cloud' formed between the base KAMA (set at a 100-period lookback) and an adjusted KAMA that incorporates the cumulative relative distance scaled up. This cloud changes color based on the trend direction — green for upward trends and red for downward trends, providing a clear, visual representation of market conditions.

Benefits:

Dynamic Sensitivity: By adapting to the market's volatility, KAMA provides more reliable signals than traditional moving averages.

Trend Clarity: The color-coded cloud visually enhances the perception of the trend’s direction and strength, making it easier for traders to decide on their trading strategy.

Versatility: Suitable for various asset classes, including stocks, forex, commodities, and cryptocurrencies, across different timeframes.

Decision Support: Helps traders understand not just the direction but the strength of trends, aiding in more informed decision-making regarding entries, exits, and risk management.

Usage:

The KAMA Cloud is ideal for traders who need a robust trend-following tool that adjusts according to market dynamics. It can be used as a standalone indicator or in conjunction with other technical analysis tools to enhance trading strategies. Look for the cloud’s color shifts as potential signals for trend reversals or continuations, and consider the cloud’s thickness as an indication of trend strength.

Whether you are a day trader, swing trader, or long-term investor, the KAMA Cloud offers a unique approach to understanding market trends, helping you navigate the complexities of various market conditions with confidence.

No Lag SupertrendNo Lag Supertrend indicator improves upon the original supertrend by incorporating calculation methods that enhance responsiveness and accuracy. Traditional supertrend indicators often suffer from lag, which can delay signals and affect trading decisions. No Lag Supertrend addresses this issue through the use of KAMA (Kaufman’s Adaptive Moving Average) and Hull ATR (Average True Range) calculations.

Goals of No Lag Supertrend:

- Lag reduction: one of the main issues with traditional supertrend indicators is their lag, which can result in delayed entry and exit signals. By integrating KAMA and Hull ATR, the no lag supertrend minimizes this delay, providing more timely signals.

- Market Noise Filtering: The combined use of KAMA and Hull ATR effectively filters out market noise, ensuring that signals are based on significant price movements rather than minor fluctuations.

- Consistency Across Different Market Conditions: The adaptive nature of KAMA and the smooth responsiveness of Hull ATR ensure that the No Lag Supertrend performs consistently across various market conditions, from trending to volatile markets.

Credits: This code is based on the TradingView supertrend but improved the ATR calculations.

Kaufman Adaptive Moving Average (KAMA) Strategy [TradeDots]"The Kaufman Adaptive Moving Average (KAMA) Strategy" is a trend-following system that leverages the adaptive qualities of the Kaufman Adaptive Moving Average (KAMA). This strategy is distinguished by its ability to adjust dynamically to market volatility, enhancing trading accuracy by minimizing the effects of false and delayed signals often associated with the Simple Moving Average (SMA).

HOW IT WORKS

This strategy is centered around use of the Kaufman Adaptive Moving Average (KAMA) indicator, which refines the principles of the Exponential Moving Average (EMA) with a superior smoothing technique.

KAMA distinguishes itself by its responsiveness to changes in market prices through an "Efficiency Ratio (ER)." This ratio is computed by dividing the recent absolute net price change by the cumulative sum of the absolute price changes over a specified period. The resulting ER value ranges between 0 and 1, where 0 indicates high market noise and 1 reflects stronger market momentum.

Using ER, we could get the smoothing constant (SC) for the moving average derived using the following formula:

fastest = 2/(fastma_length + 1)

slowest = 2/(slowma_length + 1)

SC = math.pow((ER * (fastest-slowest) + slowest), 2)

The KAMA line is then calculated by applying the SC to the difference between the current price and the previous KAMA.

APPLICATION

For entering long positions, this strategy initializes when there is a sequence of 10 consecutive rising KAMA lines. Conversely, a sequence of 10 consecutive falling KAMA lines triggers sell orders for long positions. The same logic applies inversely for short positions.

DEFAULT SETUP

Commission: 0.01%

Initial Capital: $10,000

Equity per Trade: 80%

Users are advised to adjust and personalize this trading strategy to better match their individual trading preferences and style.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

TASC 2024.01 Gap Momentum System█ OVERVIEW

TASC's January 2024 edition of Traders' Tips features an article titled “Gap Momentum” by Perry J. Kaufman. The article discusses how a trader might create a momentum strategy based on opening gap data. This script implements the Gap Momentum system presented therein.

█ CONCEPTS

In the article, Perry J. Kaufman introduces Gap Momentum as a cumulative series constructed in the same way as On-Balance Volume (OBV) , but using gap openings (today’s open minus yesterday’s close).

To smoothen the resulting time series (i.e., obtain the " signal line "), the author applies a simple moving average . Subsequently, he proposes the following two trading rules for a long-only trading system:

• Enter a long position when the signal line is moving higher.

• Exit when the signal line is moving lower.

█ CALCULATIONS

The calculation of Gap Momentum involves the following steps:

1. Calculate the ratio of the sum of positive gaps over the past N days to the sum of negative gaps (absolute values) over the same time period.

2. Add the resulting gap ratio to the cumulative time series. This time series is the Gap Momentum.

3. Keep moving forward, as in an N-day moving average.

Kaufman Efficiency Ratio (KER)The Kaufman Efficiency Ratio (also known as the Efficiency Ratio or ER) is a technical indicator used in technical analysis to measure the efficiency of a financial instrument's price movement. It was developed by Perry J. Kaufman and is designed to help traders and analysts identify the trendiness or choppiness of a market.

The Kaufman Efficiency Ratio is calculated using the following formula:

ER = (Change in Price over N periods) / (Sum of the absolute price changes over N periods)

Here's how the formula works:

"Change in Price over N periods" is the net price change over a specified number of periods (usually days or bars). It's calculated by subtracting the closing price of N periods ago from the current closing price.

"Sum of the absolute price changes over N periods" is the sum of the absolute values of price changes (i.e., ignoring the direction) over the same N periods.

The resulting Efficiency Ratio (ER) value will fall within the range of 0 to 1, with 1 indicating a perfectly trending market and 0 indicating a perfectly choppy or range-bound market. In other words, the closer the ER is to 1, the stronger and more efficient the trend is perceived to be.

Volume-Weighted Kaufman's Adaptive Moving AverageThe Volume-Weighted Kaufman's Adaptive Moving Average (VW-KAMA) is a technical indicator that combines the Volume-Weighted Moving Average (VWMA) and the Kaufman's Adaptive Moving Average (KAMA) to create a more responsive and adaptable moving average.

Advantages:

Volume-Weighted: It takes into account the volume of trades, giving more weight to periods with higher trading volume, which can help filter out periods of low activity.

Adaptive: The indicator adjusts its smoothing constant based on market conditions, becoming more sensitive in trending markets and less sensitive in choppy or sideways markets.

Versatility: VW-KAMA can be used for various purposes, including trend identification, trend following, and determining potential reversal points and act as dynamic support and resistance level.

twisted SMA strategy [4h] Hello

I would like to introduce a very simple strategy that uses a combination of 3 simple moving averages ( SMA 4 , SMA 9 , SMA 18 )

this is a classic combination showing the most probable trend directions

Crosses were marked on the basis of the color of the candles (bulish cross - blue / bearish cross - maroon)

ma 100 was used to determine the main trend, which is one of the most popular 4-hour candles

We define main trend while price crosses SMA100 ( for bullish trend I use green candle color )

The long position strategy was created in combination of 3 moving averages with Kaufman's adaptive moving average by alexgrover

The strategy is very accurate and is easy to use indicators

the strategy uses only Buy (Long) signals in a combination of crossovers of the SMA 4, SMA 9, SMA 18 and the Kaufman Adaptive Moving Average.

As a signal to close a long position, only the opposite signal of the intersection of 3 different moving averages is used

the current strategy is recommended for higher time zones (4h +) due to the strength of the closing candles, which translates into signal strength

works fascinatingly well for long-term bullish market assets (for example 4h Apple, Tesla charts)

Enjoy and trade safe ;)

kama

█ Description

An adaptive indicator could be defined as market conditions following indicator, in summary, the parameter of the indicator would be adjusted to fit its optimum value to the current price action. KAMA, Kaufman's Adaptive Moving Average, an adaptive trendline indicator developed by Perry J. Kaufman, with the notion of using the fastest trend possible based on the smallest calculation period for the existing market conditions, by applying an exponential smoothing formula to vary the speed of the trend (changing smoothing constant each period), as cited from Trading Systems and Methods p.g. 780 (Perry J. Kaufman). In this indicator, the proposed notion is on the Efficiency Ratio within the computation of KAMA, which will use a Dominant Cycle instead, an adaptive filter developed by John F. Ehlers, on determining the n periods, aiming to achieve an optimum lookback period, with respect to the original Efficiency Ratio calculation period of less than 14, and 8 to 10 is preferable.

█ Kaufman's Adaptive Moving Average

kama_ = kama + smoothing_constant * (price - kama )

where:

price = current price (source)

smoothing_constant = (efficiency_ratio * (fastest - slowest) + slowest)^2

fastest = 2/(fastest length + 1)

slowest = 2/(slowest length + 1)

efficiency_ratio = price - price /sum(abs(src - src , int(dominant_cycle))

█ Feature

The indicator will have a specified default parameter of: length = 14; fast_length = 2; slow_length = 30; hp_period = 48; source = ohlc4

KAMA trendline i.e. output value if price above the trendline and trendline indicates with green color, consider to buy/long position

while, if the price is below the trendline and the trendline indicates red color, consider to sell/short position

Hysteresis Band

Bar Color

other example