Smart Money Dynamics Blocks - Pearson MatrixSmart Money Dynamics Blocks — Pearson Matrix

A structural fusion of Prime Number Theory, Pearson Correlation, and Cumulative Delta Geometry.

1. Mathematical Foundation

This indicator is built on the intersection of Prime Number Theory and the Pearson correlation coefficient, creating a structural framework that quantifies how price and time evolve together.

Prime numbers — unique, indivisible, and irregular — are used here as nonlinear time intervals. Each prime length (2, 3, 5, 7, 11…97) represents a regression horizon where correlation is measured between price and time. The result is a multi-scale correlation lattice — a geometric matrix that captures hidden directional strength and temporal bias beyond traditional moving averages.

2. The Pearson Matrix Logic

For every prime interval p, the indicator calculates the linear correlation:

r_p = corr(price, bar_index, p)

Each r_p reflects how closely price and time move together across a prime-defined window. All r_p values are then averaged to create avgR, a single adaptive coefficient summarizing overall structural coherence.

- When avgR > 0.8 → strong positive correlation (labeled R+).

- When avgR < -0.8 → strong negative correlation (labeled R−).

This approach gives a mathematically grounded definition of trend — one that isn’t based on pattern recognition, but on measurable correlation strength.

3. Sequential Prime Slope and Median Pivot

Using the ordered sequence of 25 prime intervals, the model computes sequential slopes between adjacent primes. These slopes represent the rate of change of structure between two prime scales. A robust median aggregator smooths the slopes, producing a clean, stable directional vector.

The system anchors this slope to the 41-bar pivot — the median of the first 25 primes — serving as the geometric midpoint of the prime lattice. The resulting yellow line on the chart is not an ordinary regression line; it’s a dynamic prime-slope function, adapting continuously with correlation feedback.

4. Regression-Style Parallel Bands

Around this prime-slope line, the indicator constructs parallel bands using standard deviation envelopes — conceptually similar to a regression channel but recalculated through the prime–Pearson matrix.

These bands adjust dynamically to:

- Volatility, via standard deviation of residuals.

- Correlation strength, via avgR sign weighting.

Together, they visualize statistical deviation geometry, making it easier to observe symmetry, expansion, and contraction phases of price structure.

5. Volume and Cumulative Delta Peaks

Below the geometric layer, the indicator incorporates a custom lower-timeframe volume feed — by default using 15-second data (custom_tf_input_volume = “15S”). This allows precise delta computation between up-volume and down-volume even on higher timeframe charts.

From this feed, the indicator accumulates delta over a configurable period (default: 100 bars). When cumulative delta reaches a local maximum or minimum, peak and trough markers appear, showing the precise bar where buying or selling pressure statistically peaked.

This combination of geometry and order flow reveals the intersection of market structure and energy — where liquidity pressure expresses itself through mathematical form.

6. Chart Interpretation

The primary chart view represents the live execution of the indicator. It displays the relationship between structural correlation and volume behavior in real time.

Orange “R+” and blue “R−” labels indicate regions of strong positive or negative Pearson correlation across the prime matrix. The yellow median prime-slope line serves as the structural backbone of the indicator, while green and red parallel bands act as dynamic regression boundaries derived from the underlying correlation strength. Peaks and troughs in cumulative delta — displayed as numerical annotations — mark statistically significant shifts in buying and selling pressure.

The secondary visualization (Prime Regression Concept) expands on this by illustrating how regression behavior evolves across prime intervals. Each colored regression fan corresponds to a prime number window (2, 3, 5, 7, …, 97), demonstrating how multiple regression lines would appear if drawn independently. The indicator integrates these into one unified geometric model — eliminating the need to plot tens of regression lines manually. It’s a conceptual tool to help visualize the internal logic: the synthesis of many small-scale regressions into a single coherent structure.

7. Interpretive Insight

This model is not a prediction tool; it’s an instrument of mathematical observation. By translating price dynamics into a prime-structured correlation space, it reveals how coherence unfolds through time — not as a forecast, but as a measurable evolution of structure.

It unifies three analytical domains:

- Prime distribution — defines a nonlinear temporal architecture.

- Pearson correlation — quantifies statistical cohesion.

- Cumulative delta — expresses behavioral imbalance in order flow.

The synthesis creates a geometric analysis of liquidity and time — where structure meets energy, and where the invisible rhythm of market flow becomes measurable.

8. Contribution & Feedback

Share your observations in the comments:

- The time gap and alternation between R+ and R− clusters.

- How different timeframes change delta sensitivity or reveal compression/expansion.

- Prime intervals/clusters that tend to sit near turning points or liquidity shifts.

- How avgR behaves across assets or regimes (trending, ranging, high-vol).

- Notable interactions with the parallel bands (touches, breaks, mean-revert).

Your field notes help others read the model more effectively and compare contexts.

Summary

- Primes define the structure.

- Pearson quantifies coherence.

- Slope median stabilizes geometry.

- Regression bands visualize deviation.

- Cumulative delta locates imbalance.

Together, they construct a framework where mathematics meets market behavior.

G-channel

Squeeze Momentum Regression Clouds [SciQua]╭──────────────────────────────────────────────╮

☁️ Squeeze Momentum Regression Clouds

╰──────────────────────────────────────────────╯

🔍 Overview

The Squeeze Momentum Regression Clouds (SMRC) indicator is a powerful visual tool for identifying price compression , trend strength , and slope momentum using multiple layers of linear regression Clouds. Designed to extend the classic squeeze framework, this indicator captures the behavior of price through dynamic slope detection, percentile-based spread analytics, and an optional UI for trend inspection — across up to four customizable regression Clouds .

────────────────────────────────────────────────────────────

╭────────────────╮

⚙️ Core Features

╰────────────────╯

Up to 4 Regression Clouds – Each Cloud is created from a top and bottom linear regression line over a configurable lookback window.

Slope Detection Engine – Identifies whether each band is rising, falling, or flat based on slope-to-ATR thresholds.

Spread Compression Heatmap – Highlights compressed zones using yellow intensity, derived from historical spread analysis.

Composite Trend Scoring – Aggregates directional signals from each Cloud using your chosen weighting model.

Color-Coded Candles – Optional candle coloring reflects the real-time composite score.

UI Table – A toggleable info table shows slopes, compression levels, percentile ranks, and direction scores for each Cloud.

Gradient Cloud Styling – Apply gradient coloring from Cloud 1 to Cloud 4 for visual slope intensity.

Weight Aggregation Options – Use equal weighting, inverse-length weighting, or max pooling across Clouds to determine composite trend strength.

────────────────────────────────────────────────────────────

╭──────────────────────────────────────────╮

🧪 How to Use the Indicator

1. Understand Trend Bias with Cloud Colors

╰──────────────────────────────────────────╯

Each Cloud changes color based on its current slope:

Green indicates a rising trend.

Red indicates a falling trend.

Gray indicates a flat slope — often seen during chop or transitions.

Cloud 1 typically reflects short-term structure, while Cloud 4 represents long-term directional bias. Watch for multi-Cloud alignment — when all Clouds are green or red, the trend is strong. Divergence among Clouds often signals a potential shift.

────────────────────────────────────────────────────────────

╭───────────────────────────────────────────────╮

2. Use Compression Heat to Anticipate Breakouts

╰───────────────────────────────────────────────╯

The space between each Cloud’s top and bottom regression lines is measured, normalized, and analyzed over time. When this spread tightens relative to its history, the script highlights the band with a yellow compression glow .

This visual cue helps identify squeeze zones before volatility expands. If you see compression paired with a changing slope color (e.g., gray to green), this may indicate an impending breakout.

────────────────────────────────────────────────────────────

╭─────────────────────────────────╮

3. Leverage the Optional Table UI

╰─────────────────────────────────╯

The indicator includes a dynamic, floating table that displays real-time metrics per Cloud. These include:

Slope direction and value , with historical Min/Max reference.

Top and Bottom percentile ranks , showing how price sits within the Cloud range.

Current spread width , compared to its historical norms.

Composite score , which blends trend, slope, and compression for that Cloud.

You can customize the table’s position, theme, transparency, and whether to show a combined summary score in the header.

────────────────────────────────────────────────────────────

╭─────────────────────────────────────────────╮

4. Analyze Candle Color for Composite Signals

╰─────────────────────────────────────────────╯

When enabled, the indicator colors candles based on a weighted composite score. This score factors in:

The signed slope of each Cloud (up, down, or flat)

The percentile pressure from the top and bottom bands

The degree of spread compression

Expect green candles in bullish trend phases, red candles during bearish regimes, and gray candles in mixed or low-conviction zones.

Candle coloring provides a visual shorthand for market conditions , useful for intraday scanning or historical backtesting.

────────────────────────────────────────────────────────────

╭────────────────────────╮

🧰 Configuration Guidance

╰────────────────────────╯

To tailor the indicator to your strategy:

Use Cloud lengths like 21, 34, 55, and 89 for a balanced multi-timeframe view.

Adjust the slope threshold (default 0.05) to control how sensitive the trend coloring is.

Set the spread floor (e.g., 0.15) to tune when compression is detected and visualized.

Choose your weighting style : Inverse Length (favor faster bands), Equal, or Max Pooling (most aggressive).

Set composite weights to emphasize trend slope, percentile bias, or compression—depending on your market edge.

────────────────────────────────────────────────────────────

╭────────────────╮

✅ Best Practices

╰────────────────╯

Use aligned Cloud colors across all bands to confirm trend conviction.

Combine slope direction with compression glow for early breakout entry setups.

In choppy markets, watch for Clouds 1 and 2 turning flat while Clouds 3 and 4 remain directional — a sign of potential trend exhaustion or consolidation.

Keep the table enabled during backtesting to manually evaluate how each Cloud behaved during price turns and consolidations.

────────────────────────────────────────────────────────────

╭───────────────────────╮

📌 License & Usage Terms

╰───────────────────────╯

This script is provided under the Creative Commons Attribution-NonCommercial 4.0 International License .

✅ You are allowed to:

Use this script for personal or educational purposes

Study, learn, and adapt it for your own non-commercial strategies

❌ You are not allowed to:

Resell or redistribute the script without permission

Use it inside any paid product or service

Republish without giving clear attribution to the original author

For commercial licensing , private customization, or collaborations, please contact Joshua Danford directly.

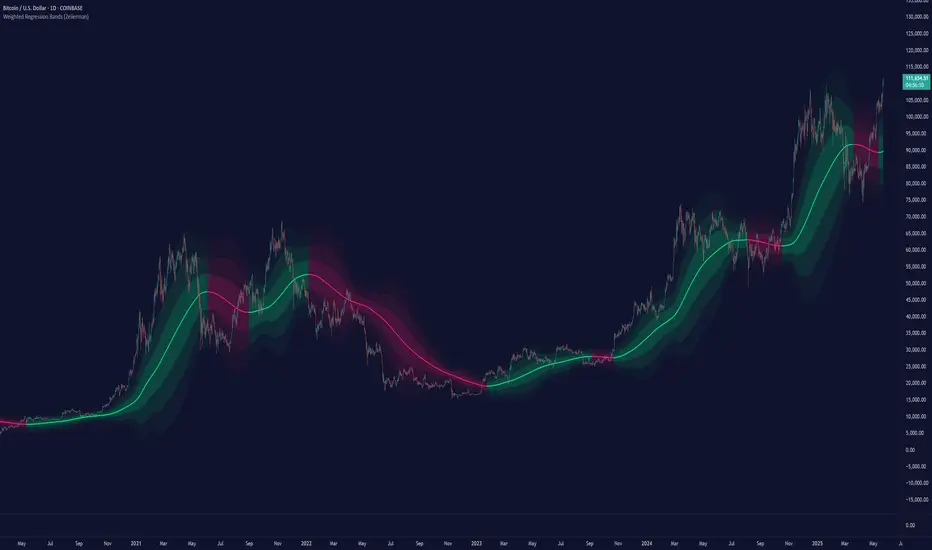

Weighted Regression Bands (Zeiierman)█ Overview

Weighted Regression Bands is a precision-engineered trend and volatility tool designed to adapt to the real market structure instead of reacting to price noise.

This indicator analyzes Weighted High/Low medians and applies user-selectable smoothing methods — including Kalman Filtering, ALMA, and custom Linear Regression — to generate a Fair Value line. Around this, it constructs dynamic standard deviation bands that adapt in real-time to market volatility.

The result is a visually clean and structurally intelligent trend framework suitable for breakout traders, mean reversion strategies, and trend-driven analysis.

█ How It Works

⚪ Structural High/Low Analysis

At the heart of this indicator is a custom high/low weighting system. Instead of using just the raw high or low values, it calculates a midline = (high + low) / 2, then applies one of three weighting methods to determine which price zones matter most.

Users can select the method using the “Weighted HL Method” setting:

Simple

Selects the single most dominant median (highest or lowest) in the lookback window. Ideal for fast, reactive signals.

Advanced

Ranks each bar based on a composite score: median × range × recency. This method highlights structurally meaningful bars that had both volatility and recency. A built-in Kalman filter is applied for extra stability.

Smooth

Blends multiple bars into a single weighted average using smoothed decay and range. This provides the softest and most stable structural response.

⚪ Smoothing Methods (ALMA / Linear Regression)

ALMA provides responsive, low-lag smoothing for fast trend reading.

Linear Regression projects the Fair Value forward, ideal for trend modeling.

⚪ Kalman Smoothing Filter

Before trend calculations, the indicator applies an optional Kalman-style smoothing filter. This helps:

Reduce choppy false shifts in trend,

Retain signal clarity during volatile periods,

Provide stability for long-term setups.

⚪ Deviation Bands (Dynamic Volatility Envelopes)

The indicator builds ±1, ±2, and ±3 standard deviation bands around the fair value line:

Calculated from the standard deviation of price,

Bands expand and contract based on recent volatility,

Visualizes potential overbought/oversold or trending conditions.

█ How to Use

⚪ Trend Trading & Filtering

Use the Fair Value line to identify the dominant direction.

Only trade in the direction of the slope for higher probability setups.

⚪ Volatility-Based Entries

Watch for price reaching outer bands (+2σ, +3σ) for possible exhaustion.

Mean reversion entries become higher quality when far from Fair Value.

█ Settings

Length – Lookback for Weighted HL and trend smoothing

Deviation Multiplier – Controls how wide the bands are from the fair value line

Method – Choose between ALMA or Linear Regression smoothing

Smoothing – Strength of Kalman Filter (1 = none, <1 = stronger smoothing)

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Moving Volume-Weighted Avg Price, % Channel, BBsThis script includes:

- Moving Volume-Weighted Average Price line.

- User-defined % band above and below, very useful for "breakout" signals, and mentally adjusting to the magnitude of price swings when viewing an automatic scale on the price axis.

- Volume-Weighted Bollinger Bands, which are more sensitive to volume.

More detail:

- This is like TV's basic VWAP in concept, except the major flaw in that is that it has reset periods that you can't override, and the volume is cumulative until the next hard reset. The 'reset' is OK for securities trading, that resets every day anyway. But not for crypto - and not if/when securities trading goes 24/7. Also, the denominator accumulating over the entire period is also *not* OK, because then what is shown means something different as the day progresses - which kind of makes it useless. In other words, it starts out very sensitive to volume, and gets progressively more numb to it as they day progresses, and starts flattening out.

- This fixes both problems, by using a user-definable moving window for the average. Essentially combining SMA with volume-weighting.

- You may also find an invaluable trading aid, in the % bands above and below.

- What can optionally be shown is standard deviation bands, aka Bollinger bands. The advantage over regular BB is that it's volume-weighted. Since it is already calculated on a moving average, the period for the standard deviation has been shortened by default, and the magnitude increased, to better approximate regular Bollinger Bands - but it's still more responsive to volume.

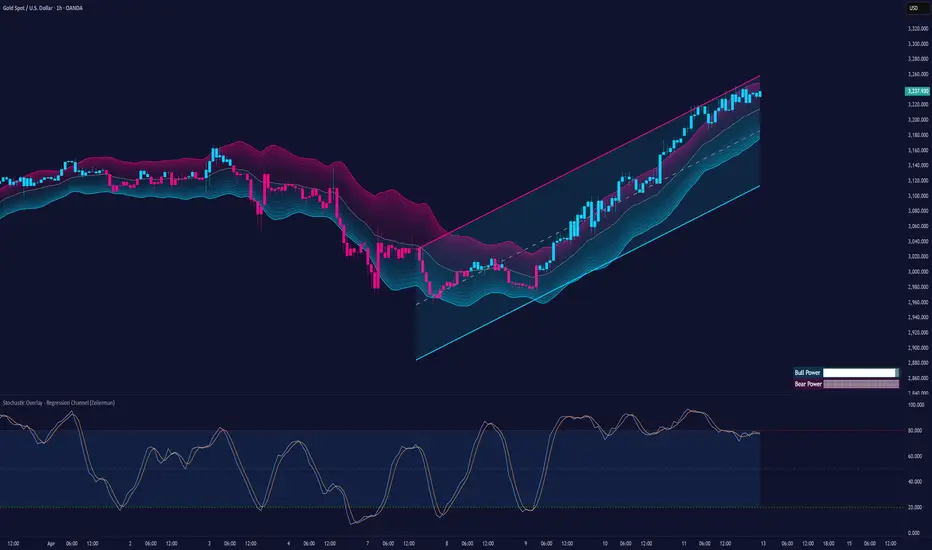

Stochastic Overlay - Regression Channel (Zeiierman)█ Overview

The Stochastic Overlay – Regression Channel (Zeiierman) is a next-generation visualization tool that transforms the traditional Stochastic Oscillator into a dynamic price-based overlay.

Instead of leaving momentum trapped in a lower subwindow, this indicator projects the Stochastic oscialltor directly onto price itself — allowing traders to visually interpret momentum, overbought/oversold conditions, and market strength without ever taking their eyes off price action.

⚪ In simple terms:

▸ The Bands = The Stochastic Oscillator — but on price.

▸ The Midline = Stochastic 50 level

▸ Upper Band = Stochastic Overbought Threshold

▸ Lower Band = Stochastic Oversold Threshold

When the price moves above the midline → it’s the same as the oscillator moving above 50

When the price breaks above the upper band → it’s the same as Stochastic entering overbought.

When the price reaches the lower band →, think of it like Stochastic being oversold.

This makes market conditions visually intuitive. You’re literally watching the oscillator live on the price chart.

█ How It Works

The indicator layers 3 distinct technical elements into one clean view:

⚪ Stochastic Momentum Engine

Tracks overbought/oversold conditions and directional strength using:

%K Line → Momentum of price

%D Line → Smoothing filter of %K

Overbought/Oversold Bands → Highlight potential reversal zones

⚪ Volatility Adaptive Bands

Dynamic bands plotted above and below price using:

ATR * Stochastic Scaling → Creates wider bands during volatile periods & tighter bands in calm conditions

Basis → Moving average centerline (EMA, SMA, WMA, HMA, RMA selectable)

This means:

→ In strong trends: Bands expand

→ In consolidations: Bands contract

⚪ Regression Channel

Projects trend direction with different models:

Logarithmic → Captures non-linear growth (perfect for crypto or exponential stocks)

Linear → Classic regression fit

Adaptive → Dynamically adjusts sensitivity

Leading → Projects trend further ahead (aggressive mode)

Channels include:

Midline → Fair value trend

Upper/Lower Bounds → Deviation-based support/resistance

⚪ Heatmap - Bull & Bear Power Strength

Visual heatmeter showing:

% dominance of bulls vs bears (based on close > or < Band Basis)

Automatic normalization regardless of timeframe

Table display on-chart for quick visual insight

Dynamic highlighting when extreme levels are reached

⚪ Trend Candlestick Coloring

Bars auto-color based on trend filter:

Above Basis → Bullish Color

Below Basis → Bearish Color

█ How to Use

⚪ Trend Trading

→ Use Band direction + Regression Channel to identify trend alignment

→ Longs favored when price holds above the Basis

→ Shorts favored when price stays below the Basis

→ Use the Bull & Bear heatmap to asses if the bulls or the bears are in control.

⚪ Mean Reversion

→ Look for price to interact with Upper or Lower Band extremes

→ Stochastic reaching OB/OS zones further supports reversals

⚪ Momentum Confirmation

→ Crossovers between %K and %D can confirm continuation or divergence signals

→ Especially powerful when happening at band boundaries

⚪ Strength Heatmap

→ Quickly visualize current buyer vs seller control

→ Sharp spikes in Bull Power = Aggressive buying

→ Sharp spikes in Bear Power = Heavy selling pressure

█ Why It Useful

This is not a typical Stochastic or regression tool. The tool is designed for traders who want to:

React dynamically to price volatility

Map momentum into volatility context

Use adaptive regression channels across trend styles

Visualize bull vs bear power in real-time

Follow trends with built-in reversal logic

█ Settings

Stochastic Settings

Stochastic Length → Period of calculation. Higher = smoother, Lower = faster signals.

%K Smoothing → Smooths the Stochastic line itself.

%D Smoothing → Smooths the moving average of %K for slower signals.

Stochastic Band

Band Length → Length of the Moving Average Basis.

Volatility Multiplier → Controls band width via ATR scaling.

Band Type → Choose MA type (EMA, SMA, WMA, HMA, RMA).

Regression Channel

Regression Type → Logarithmic / Linear / Adaptive / Leading.

Regression Length → Number of bars for regression calculation.

Heatmap Settings

Heatmap Length → Number of bars to calculate bull/bear dominance.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Log Regression Oscillator Channel [BigBeluga]

This unique overlay tool blends logarithmic trend analysis with dynamic oscillator behavior. It projects RSI, MFI, or Stochastic lines directly into a log regression channel on the price chart — offering an intuitive way to detect overbought/oversold momentum within the broader price structure.

🔵Key Features:

Logarithmic Regression Channel:

➣ Draws a trend-based channel using logarithmic regression, adapting to price growth curvature over time.

➣ Features upper, lower, and optional midline boundaries to visualize trend flow and range extremes.

Oscillator Overlay (RSI / MFI / Stochastic):

➣ Projects your chosen oscillator inside the channel using dynamic polylines.

➣ Allows switching between RSI, Money Flow Index, or Stochastic for versatile momentum insight.

Threshold-Based Scaling:

➣ The top and bottom of the channel represent traditional oscillator thresholds (e.g., RSI 70/30).

➣ Users can modify the scale in settings to customize what "overbought" or "oversold" means visually.

Signal Line Integration:

➣ Adds a yellow moving average (signal line) for smoother confirmation of oscillator turns.

➣ Helps identify divergence, momentum shifts, and fakeouts with better clarity.

Live Oscillator Readout:

➣ Displays the real-time oscillator value at the right edge of the chart.

➣ Ensures traders stay aware of current momentum levels without switching panels.

🔵Usage:

Momentum Context:

➣ When the oscillator touches the upper regression band, it may signal local overbought pressure.

➣ Touching the lower band may indicate oversold conditions within the current log trend.

Divergence Detection:

➣ Use the oscillator’s behavior relative to the channel slope to spot divergence from price.

➣ For example, RSI rising inside a falling channel can flag early trend shifts.

Trend-Sensitive Entries:

➣ Combine oscillator signals with log channel direction to filter trades in trend alignment.

➣ Signal line crossovers inside the channel act as early warning for momentum turns.

The Log Regression Oscillator Channel transforms how traders view classic momentum tools. By embedding oscillators into a logarithmic trend structure, it offers unmatched clarity on momentum positioning relative to price expansion. Ideal for swing traders, mean-reverters, or trend followers looking to sharpen entries and exits with style.

Logarithmic Regression Channel-Trend [BigBeluga]

This indicator utilizes logarithmic regression to track price trends and identify overbought and oversold conditions within a trend. It provides traders with a dynamic channel based on logarithmic regression, offering insights into trend strength and potential reversal zones.

🔵Key Features:

Logarithmic Regression Trend Tracking: Uses log regression to model price trends and determine trend direction dynamically.

f_log_regression(src, length) =>

float sumX = 0.0

float sumY = 0.0

float sumXSqr = 0.0

float sumXY = 0.0

for i = 0 to length - 1

val = math.log(src )

per = i + 1.0

sumX += per

sumY += val

sumXSqr += per * per

sumXY += val * per

slope = (length * sumXY - sumX * sumY) / (length * sumXSqr - sumX * sumX)

average = sumY / length

intercept = average - slope * sumX / length + slope

Regression-Based Channel: Plots a log regression channel around the price to highlight overbought and oversold conditions.

Adaptive Trend Colors: The color of the regression trend adjusts dynamically based on price movement.

Trend Shift Signals: Marks trend reversals when the log regression line cross the log regression line 3 bars back.

Dashboard for Key Insights: Displays:

- The regression slope (multiplied by 100 for better scale).

- The direction of the regression channel.

- The trend status of the logarithmic regression band.

🔵Usage:

Trend Identification: Observe the regression slope and channel direction to determine bullish or bearish trends.

Overbought/Oversold Conditions: Use the channel boundaries to spot potential reversal zones when price deviates significantly.

Breakout & Continuation Signals: Price breaking outside the channel may indicate strong trend continuation or exhaustion.

Confirmation with Other Indicators: Combine with volume or momentum indicators to strengthen trend confirmation.

Customizable Display: Users can modify the lookback period, channel width, midline visibility, and color preferences.

Logarithmic Regression Channel-Trend is an essential tool for traders who want a dynamic, regression-based approach to market trends while monitoring potential price extremes.

Machine Learning Regression Trend [LuxAlgo]The Machine Learning Regression Trend tool uses random sample consensus (RANSAC) to fit and extrapolate a linear model by discarding potential outliers, resulting in a more robust fit.

🔶 USAGE

The proposed tool can be used like a regular linear regression, providing support/resistance as well as forecasting an estimated underlying trend.

Using RANSAC allows filtering out outliers from the input data of our final fit, by outliers we are referring to values deviating from the underlying trend whose influence on a fitted model is undesired. For financial prices and under the assumptions of segmented linear trends, these outliers can be caused by volatile moves and/or periodic variations within an underlying trend.

Adjusting the "Allowed Error" numerical setting will determine how sensitive the model is to outliers, with higher values returning a more sensitive model. The blue margin displayed shows the allowed error area.

The number of outliers in the calculation window (represented by red dots) can also be indicative of the amount of noise added to an underlying linear trend in the price, with more outliers suggesting more noise.

Compared to a regular linear regression which does not discriminate against any point in the calculation window, we see that the model using RANSAC is more conservative, giving more importance to detecting a higher number of inliners.

🔶 DETAILS

RANSAC is a general approach to fitting more robust models in the presence of outliers in a dataset and as such does not limit itself to a linear regression model.

This iterative approach can be summarized as follow for the case of our script:

Step 1: Obtain a subset of our dataset by randomly selecting 2 unique samples

Step 2: Fit a linear regression to our subset

Step 3: Get the error between the value within our dataset and the fitted model at time t , if the absolute error is lower than our tolerance threshold then that value is an inlier

Step 4: If the amount of detected inliers is greater than a user-set amount save the model

Repeat steps 1 to 4 until the set number of iterations is reached and use the model that maximizes the number of inliers

🔶 SETTINGS

Length: Calculation window of the linear regression.

Width: Linear regression channel width.

Source: Input data for the linear regression calculation.

🔹 RANSAC

Minimum Inliers: Minimum number of inliers required to return an appropriate model.

Allowed Error: Determine the tolerance threshold used to detect potential inliers. "Auto" will automatically determine the tolerance threshold and will allow the user to multiply it through the numerical input setting at the side. "Fixed" will use the user-set value as the tolerance threshold.

Maximum Iterations Steps: Maximum number of allowed iterations.

Nadaraya-Watson: Envelope (Non-Repainting)Due to popular request, this is an envelope implementation of my non-repainting Nadaraya-Watson indicator using the Rational Quadratic Kernel. For more information on this implementation, please refer to the original indicator located here:

What is an Envelope?

In technical analysis, an "envelope" typically refers to a pair of upper and lower bounds that surrounds price action to help characterize extreme overbought and oversold conditions. Envelopes are often derived from a simple moving average (SMA) and are placed at a predefined distance above and below the SMA from which they were generated. However, envelopes do not necessarily need to be derived from a moving average; they can be derived from any estimator, including a kernel estimator such as Nadaraya-Watson.

How to use this indicator?

Overall, this indicator offers a high degree of flexibility, and the location of the envelope's bands can be adjusted by (1) tweaking the parameters for the Rational Quadratic Kernel and (2) adjusting the lookback window for the custom ATR calculation. In a trending market, it is often helpful to use the Nadaraya-Watson estimate line as a floating SR and/or reversal zone. In a ranging market, it is often more convenient to use the two Upper Bands and two Lower Bands as reversal zones.

How are the Upper and Lower bounds calculated?

In this indicator, the Rational Quadratic (RQ) Kernel estimates the price value at each bar in a user-defined lookback window. From this estimation, the upper and lower bounds of the envelope are calculated based on a custom ATR calculated from the kernel estimations for the high, low, and close series, respectively. These calculations are then scaled against a user-defined multiplier, which can be used to further customize the Upper and Lower bounds for a given chart.

How to use Kernel Estimations like this for other indicators?

Kernel Functions are highly underrated, and when calibrated correctly, they have the potential to provide more value than any mundane moving average. For those interested in using non-repainting Kernel Estimations for technical analysis, I have written a Kernel Functions library that makes it easy to access various well-known kernel functions quickly. The Rational Quadratic Kernel is used in this implementation, but one can conveniently swap out other kernels from the library by modifying only a single line of code. For more details and usage examples, please refer to the Kernel Functions library located here:

Pivot Parallel Channel by [livetrend]This script draws parallel channels using pivot points for trend analysis.

Script draws maximum 4 parallel channels if suitable up or down trend already exists on the chart according to chosen Pivot Length and Multiplier.

You can change Multiplier to draw Higher Time Frame Channels.

Good luck!

Regression Channel Trend DetectionThis is a regression channel that uses ichimoku to determine trend. The sensitivity is customizable. The centerline will change color according to the trend detected by ichimoku, and each line can act as support/resistance. The bands of the channel also change colors according to how far price is getting away from them. If you notice in this example, the lower band is turning orange when the price is getting too far away from it, suggesting that it may have risen too fast and too soon. This is still in testing so feel free to comment with any suggestions or fixes.

TF Segmented Polynomial Regression [LuxAlgo]This indicator displays polynomial regression channels fitted using data within a user selected time interval.

The model is fitted using the same method described in our previous script:

Settings

Degree: Degree of the fitted polynomial

Width: Multiplicative factor of the model RMSE. Controls the width of the polynomial regression's channels

Timeframe: Fits the polynomial regression using data within the selected timeframe interval

Show fit for new bars: If selected, will fit the regression model for newly generated bars, else the previous fitted value is displayed.

Src: Input source

Usage

Segmented (or piecewise) models yield multiple fits by first partitioning the data into multiple intervals from specific partitioning conditions. In this script this partitioning condition is for a user selected timeframe to change.

Segmented models can be particularly pertinent for market prices, which often describes a series of local trends.

Segmented polynomial regressions can describe the nature of underlying trends in the price from their fit, such as if an underlying trend is more linear (trending) or constant (ranging), and if a trend is monotonic.

The above chart shows a monthly partitioning on SPX 15m, using a polynomial regression of degree 3. Channel extremities allows highlighting local tops/bottoms.

For real time applications users can choose to fit a current model to incoming price data using the Show fit for new bars settings.

Details

The script does not make use of line.new to display the segmented linear regressions, which allows showing a higher number of historical fits. Each channel extremity as well as the model fit is displayed from the plot function, as such user can more easily set alerts on them.

It is important to note that achieving this requires accessing future price data, as such this script is subject to lookahead bias, historical results differ from the results one could have obtained in real-time.

Linear Regression ChannelsThese channels are generated from the current values of the linear regression channel indicator, the standard deviation is calculated based off of the RSI . This indicator gives an idea of when the linear regression model predicts a change in direction.

You are able to change the length of the linear regression model, as well as the size of the zone. A negative zone size will make the zone stretch away from the center, and a positive zone size will make it stretch towards the centerline.

Infiten's Regressive Trend Channel An experiment using Pinescript's candle plotting feature. This indicator performs a linear regression on the lows, highs, and moving average, and plots them all in the form of a candlestick. If the close is below the prediction, the candlestick is red, if the close is above the regression, the candlestick is green. Effective and aesthetic way to analyze trends.

Linear Regression Channel - Auto Volume BasedBased on oryginal TV indicator BUT with a little twist. ;)

I really like the regression channel - but the problem is that the length needs to be always manually adjusted.

In this script I try to solve this issue.

This is modified version on TV indicator - Linear Regression Channel.

The main difference is that now you don't get static length - it is automatically adjuested to the recent price action (determined by highest volume in last 300 bars).

Linear Regression Relative Strength[image/x/iZvwDWEY/

Relative Strength indicator comparing the current symbol to SPY (or any other benchmark). It may help to pick the right assets to complement the portfolio build around core ETFs such as SPY.

The general idea is to show if the current symbol outperforms or underperforms the benchmark (SPY by default) when bought some certain time ago. Relative performance is displayed as percent and is calculated for three different time ranges - short (1 mo by default), mid (1 quarter), and long (half a year). To smooth the volatility, the script uses linear regression to estimate the trend and takes the start and the end points of the linear regression line to compute the relative strength.

It is important to remember that the script shows the gain relative to SPY (or other selected benchmark), not the asset's gain. Therefore, it may indicate that the asset is profitable, but it still may lose value if SPY is in downtrend.

Therefore, it is crucial to check other indicators before making a decision. In the example above, standard linear regression for one quarter is used to indicate the direction of the trend.

Support Resistance ChannelsHello All,

For Long time I was planning to make Support/Resistance Channels script, finally I had time and here it is.

How this script works?

- it finds and keeps Pivot Points

- when it found a new Pivot Point it clears older S/R channels then;

- for each pivot point it searches all pivot points in its own channel with dynamic width

- while creating the S/R channel it calculates its strength

- then sorts all S/R channels by strength

- it shows the strongest S/R channels, before doing this it checks old location in the list and adjust them for better visibility

- if any S/R channel was broken on last move then it gives alert and put shape below/above the candle

- The colors of the S/R channels are adjusted automatically

You can set/change following settings:

- Pivot Period

- Source : High/Low or Close/Open can be used

- Maximum Channel Width %: this is the maximum channel width rate, this is calculated using Highest/Lowest levels in last 300 bars

- Number of S/R to show : this is the number of Strongest S/R to show

- Loopback Period: While calculating S/R levels it checks Pivot Points in LoopBack Period

- Show S/R on last # Bars: To see S/R levels only on last N bars

- Start Date: the script starts calculating Pivot Point from this date, the reason I put this option is for visuality. Explained below

- You can set colors/transparency

- and You can enable/disable shapes for broken S/R levels

Examples:

You can change colors as you wish:

here " Show S/R on last # Bars " set 100:

Sometimes visuality may corrupt because of old S/R levels, to solve it you need to set "Start Date" in the options to start the script in visual part (last 292 bars)

here in first screenshot it doesn't look good (shrink), then on second screenshot I set the "Start Date" it looks better, if you change time frame don't forget to set it again :)

Enjoy!

Moving Regression Prediction BandsIntroducing the Moving Regression Prediction Bands indicator.

Here I aimed to combine the principles of traditional band indicators (such as Bollinger Bands), regression channel and outlier detection methods. Its upper and lower bands define an interval in which the current price was expected to fall with a prescribed probability, as predicted by the previous-step result of the local polynomial regression (for the original Moving Regression script, see link below).

Algorithm

1. At every time step, the script performs local polynomial regression of the sample data within the lookback window specified by the Length input parameter.

2. The fitted polynomial is used to construct the Moving Regression time series as well as to extrapolate data, that is, to predict the next data point ( MRPrediction ).

3. The accuracy of local interpolation is estimated by means of the root-mean-square error ( RMSE ), that is, the deviation between the fitted polynomial and the observed values.

4. The MRPrediction and RMSE values calculated for the previous bar are then used to build the upper and lower bands , which I define as follows:

Upper Band = MRPrediction_prev + Multiplier *( RMSE_prev )

Lower Band = MRPrediction_prev - Multiplier *( RMSE_prev )

Here the Multiplier is a user-defined parameter that should be interpreted as a quantile in the standard normal distribution (the default value of 2.0 roughly corresponds to the 95% prediction interval).

To visualize the central line , the script offers the following options:

Previous-Period MR Prediction: MRPrediction_prev time series from the above equation.

MR: Conventional Moving Regression time series.

Ribbon: “Previous-Period MR Prediction” and “MR” curves plotted together and colored according to their relative value (green if MR > Previous MR Prediction; red otherwise).

Usage

My original idea was to use the band breakouts as potential trading signals. For example, the price crossing above the upper band is a bullish signal , being a potential sign that price is gaining momentum and is out of a previously predicted trend. The exit signal could be the crossing under the lower band or under the central line.

However, be aware that it is an experimental indicator, so you might fin some better strategies.

Feel free to play around!

GAURs Polynomial Regression ChannelsThanks to The Sweet Lord , here is the Gaur's Polynomial Regression Channel.

Its a Polynomial Regression Channel but applied a little differently. Wont go into technical details much. Overview of options is as follows-

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Channel Options

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

1. Degree of Polynomial: 1/2/3

Default = 3

Defines the degree of polynomials - 1,2,3. Note here, degree 1 will not be a straight line since its applied differently.

Try different degrees for different fits and market conditions.

2. Channel Length:

Default 30 (candles)

You can go beyond 100 or 200 candle lengths but smaller is the usual preference of Poly-Reg-channel traders. It all depends on market conditions and your style of trading. Do your research. I am usually comfortable with a range of 20-50 (in crypto markets).

3. Basis of Channel height/boundries: ATR/Manual

Default: ATR

ATR provides a dynamically adjusted entry/exit bounds of the channels. As ATR changes, the channel bounds also changes its height. It can also be fixed manually. Manual heights wont change automatically.

4. Basis of Y-Value: open/close/ sma / ema / wma /hilow

Default: close

Y- value is the y value of the (x,y) coordinates used while calculating the regression coefficients. Dont worry about it, its nothing serious.

5. Apply channel smoothning using sma?: Yes/No

Default: Yes

Without smoothning, the channel does not "look" good.

6. Shaded Area Height Percentage:

Its the extra margin for the channel. Its in percentage of the total height (defined 3 above) of channels. The shaded area provides an extra allowance for your entries or exits beyond the ATR or manual heights.

7. Plot RSI?: Yes/No

Default: Yes

Plots RSI (orange line in between the channel - its different from the dotted center line) considering the downbound of channels as 0 (oversold) and upbound of channels as 100 (overbought)

8. Plot 200 sma?: Yes/No

Default: Yes

It plots a 200 period fast (green) and 225 period slow (red) sma . I usually use two MAs. Its visually very easy to understand.

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Sample Strategy

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

You can develop your own strategy with the channels. But following is just one of the ways you can trade.

Best Application: Ranging markets. But can be happily used in volatile conditions, with a little experience.

1. SMA: -- (this condition is optional really)

If green (200) is above red (225) go only long. If red is above green go only short. Defines long term trend of the market.

2. Channel slope: -- (this stuff needs practice/experience)

Depending on the channel slope, like if its tending to go up or down, you can choose to take only short or long trades. It defines short term momentum of the market.

3. ATR based heights:

Since its ATR based, the channel height are our natural entry and exit points.

Long:

When price touches lower shaded area, consider possible long entry. Exit on price entering the upper shaded area.

Short:

Enter on upper bound shaded area, exit on lower.

4. RSI:

For additional conformations. Again note, the RSI considers the lower bound of channel as 0 and upper as 100. But since, the channel moves up and down, the RSI will also move not only as RSI but also with the channel. Meaning, say if the RSI is valued at 50, then it will be near the center of the channel but since the center changes as time and price changes, the RSI valued at 50 at different times will not be at the same horizontal level respect to the graph, although it will be at the same level (center) respect to the channel.

5. PRC Channel Percentage label:

This label is at the lower side a bit ahead of the current candle. Provides you info on what is the channel percentage. This is especially helpful in crypto markets to gauge your possible percentage profit where profits can be much higher than forex or other instruments. It can also helps you select a suitable market/instrument if the channels are based on ATR.

6. Extra indicators:

I usually use stochastic along with this setup for extra conformations.

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Donate

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Use freely and donate generously if you find value. Your help will really help.

I had earlier provided BTC addresses for donations but it seems to violate TV House rules.

Hope they make TV coins redeemable in future.

- Pranav Joshi

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Extra Info

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

// © cpranavjoshi

// special thanks to the "Trading View" people for providing this great platform for free

// ------------------------

// MATH

// ------------------------

// special thanks to an article on the web that provided layman friendly explanation of the maths

// unfortunately i wont be able to provide the link to that article owing to TV restrictions, though i sincerely would have liked to credit the author.

// Google search this phrase, and you should be able to get it in one of the first results - "polynomialregression Mathematics of Polynomial Regression"

// my regression math calculation is a further resolution upon the generalized matrix formula given in the that article.

// the generalized matrix looks scary but in fact its much simpler than one may assume

// the summation sign things are just float numbers that can be easily found out

// so we get a matrix with number of equations equal to the number of unknowns.

// e.g. if its a 3rd degree poly, it has 4 unknowns (c0,c1,c2,c3) with 4 equations as in the generalized matrix

// it can be resolved by simple algebra

// Note: the results have been verified with excel using same input data points.

// pine was difficult for me so i coded it in python first to verify

// ------------------------

// WHY

// ------------------------

// this script was coded because Pranav badly needed Polynomial channels (had used them in mt4 earlier)

// and at the time of this coding, i could not find any readily available script in the trading view public library ( tnx public)

// the complex math was probably the hurdle

// i m not good in maths, but by the Will of the Lord, i could resolve the issue with simple algebra and logic

// ------------------------

// PINE

// ------------------------

// i am just an average (even poor probably) programmer and pine script is not my language

// this is a humble attempt to write my first pine with whatever i could do quickly

// experts - feel free to develop if needed. have used some workarounds in drawings/plottings. rectify them if possible

//

//

// - Pranav Joshi

Regression Channel [DW]This is an experimental study which calculates a linear regression channel over a specified period or interval using custom moving average types for its calculations.

Linear regression is a linear approach to modeling the relationship between a dependent variable and one or more independent variables.

In linear regression, the relationships are modeled using linear predictor functions whose unknown model parameters are estimated from the data.

The regression channel in this study is modeled using the least squares approach with four base average types to choose from:

-> Arnaud Legoux Moving Average (ALMA)

-> Exponential Moving Average (EMA)

-> Simple Moving Average (SMA)

-> Volume Weighted Moving Average (VWMA)

When using VWMA, if no volume is present, the calculation will automatically switch to tick volume, making it compatible with any cryptocurrency, stock, currency pair, or index you want to analyze.

There are two window types for calculation in this script as well:

-> Continuous, which generates a regression model over a fixed number of bars continuously.

-> Interval, which generates a regression model that only moves its starting point when a new interval starts. The number of bars for calculation cumulatively increases until the end of the interval.

The channel is generated by calculating standard deviation multiplied by the channel width coefficient, adding it to and subtracting it from the regression line, then dividing it into quartiles.

To observe the path of the regression, I've included a tracer line, which follows the current point of the regression line. This is also referred to as a Least Squares Moving Average (LSMA).

For added predictive capability, there is an option to extend the channel lines into the future.

A custom bar color scheme based on channel direction and price proximity to the current regression value is included.

I don't necessarily recommend using this tool as a standalone, but rather as a supplement to your analysis systems.

Regression analysis is far from an exact science. However, with the right combination of tools and strategies in place, it can greatly enhance your analysis and trading.

Kozlod - Channel Break Out AlertsStudy version with alerts of standard "Channel Break Out Strategy".

LinearRegressionChannelBreakoutMy first idea about the linear regression channel... It is free and available for everybody.