Asset Correlation Matrix [PEARSON|BETA|R2]The Market Dilemma: The Liquidity Trap and The Illusion of Diversification

One of the most expensive mistakes in modern trading is the assumption that holding different asset classes—such as Technology Stocks, Crypto, and Commodities—automatically provides safety. In stable economic times, this may be true. However, in environments defined by high liquidity stress or macroeconomic shocks, the correlations between these seemingly distinct assets tend to converge mathematically to 1.0. This phenomenon is known in quantitative finance as "Systemic Coupling." When this occurs, technical analysis on individual charts loses its predictive power because the asset is no longer trading on its own idiosyncratic fundamentals (e.g., earnings or user growth) but is merely acting as a high-beta proxy for global liquidity flows. This toolkit solves this problem by providing an institutional-grade framework to quantify exactly how much "independence" your assets truly possess at any given moment. It objectively separates a "Stock Picker's Market," where individual analysis works, from a "Macro Regime," where only the broader trend matters.

Scientific Foundation: Why Logarithmic Returns Matter

Standard retail indicators often calculate correlation based on simple percentage price changes. This approach is mathematically flawed over longer timeframes due to the compounding effect. This algorithm is grounded in Modern Portfolio Theory (MPT) and utilizes Logarithmic Returns (continuously compounded returns). As established in academic literature by Hudson & Gregoriou (2015), log returns provide time-additivity and numerical stability. This ensures that the statistical relationship measured over a rolling 60-day window is accurate and not distorted by volatility spikes, providing a professional basis for risk modeling.

The Three Pillars of Analysis: Understanding the Metrics

To fully understand market behavior, one must look at the relationship between an asset and a benchmark from three distinct mathematical angles. This indicator allows you to switch between these institutional metrics:

1. Pearson Correlation (Directional Alignment):

This is the classic measure of linear dependence, ranging from -1.0 to +1.0. Its primary value lies in identifying Regime Changes . When the correlation is high (above 0.8), the asset has lost its autonomy and is "locked" with the benchmark. When the correlation drops or turns negative, the asset is "decoupled." This mode is essential for hedging strategies. If you are long Bitcoin and short the Nasdaq to hedge, but their correlation drops to zero, your hedge has mathematically evaporated. This mode warns you of such structural breaks.

2. Beta Sensitivity (Volatility Adjusted Risk):

While Correlation asks "Are they moving together?", Beta asks "How violently are they moving together?". Beta adjusts the correlation by the relative volatility of the asset versus the benchmark. A Beta of 1.5 implies that for every 1% move in the S&P 500, the asset is statistically likely to move 1.5%. This is the single most important metric for Position Sizing . In high-beta regimes, you must reduce position size to maintain constant risk. This mode visualizes when an asset transitions from being a "Defensive Haven" (Beta < 1.0) to a "High Risk Vehicle" (Beta > 1.0).

3. Explained Variance / R-Squared (The Truth Serum):

This is the most advanced metric in the toolkit, rarely found in retail indicators. R-Squared ranges from 0% to 100% and answers the question of causality: "How much of the asset's price movement is purely explained by the movement of the benchmark?" If R2 is 85%, it mathematically proves that 85% of the price action is external noise driven by the market, and only 15% is driven by the asset's own news or chart pattern. Institutional traders use this to filter trades: They seek Low R-Squared environments for alpha generation (breakouts) and avoid High R-Squared environments where they would simply be trading the index with higher fees.

The Theory of "Invisible Gravity" and Macro Benchmarking

While comparing assets to the S&P 500 is standard, the theoretical value of this matrix expands significantly when utilizing Macro Benchmarks like US Treasury Yields (US10Y). According to Discounted Cash Flow (DCF) theory, the value of long-duration assets (like Tech Stocks or Crypto) is inversely related to the risk-free rate. By setting the benchmark to yields, this indicator makes this theoretical concept visible. A strong Negative Correlation confirms that asset appreciation is being driven by "cheap money" (falling yields). However, a sudden flip to Positive Correlation against yields signals a profound shift in market mechanics, often indicating that inflation fears are being replaced by growth fears or monetary debasement. This visualizes the "Denominator Effect" in real-time.

Visualizing Market Breadth and Internal Health

Beyond individual lines, the "Breadth Mode" aggregates the data into a histogram to diagnose the health of a trend. A healthy rally is supported by broad participation, meaning high correlation across risk assets. A dangerous, exhausted rally is characterized by Divergence : Price makes a new high, but the Correlation Breadth (the number of assets participating in the move) collapses. This is often the earliest warning signal of a liquidity withdrawal before a reversal occurs.

References

Markowitz, H. (1952). Portfolio Selection. The Journal of Finance.

Sharpe, W. F. (1964). Capital Asset Prices: A Theory of Market Equilibrium.

Hudson, R., & Gregoriou, A. (2015). Calculating and Comparing Security Returns: Logarithmic vs Simple Returns.

Disclaimer: This indicator is for educational purposes only. Past performance is not indicative of future results.

Diversification

Assets Correlation by GDM📊 Correlation Matrix Table between Two Assets

This indicator calculates and displays the rolling correlation between the asset on your chart and a second asset of your choice. The correlation is computed based on log returns over a user-defined lookback period. A live summary table appears in the bottom left corner, providing a real-time snapshot of the current correlation and its context.

How it works:

Comparison Asset:

Select any symbol to compare with the chart asset (e.g., compare BTCUSD to ETHUSD).

Lookback Period:

Choose the rolling window (in bars) used to calculate the Pearson correlation coefficient.

Dynamic Table:

A table in the lower left corner summarizes:

Main asset symbol

Comparison symbol

Analysis period (bars)

Current correlation value (rounded to 2 decimals)

Correlation strength & direction (Strong, Moderate, Weak | Positive/Negative)

Visual Plot:

The indicator plots the correlation value over time so you can observe changes and trends.

Table Positioning:

Table location can be adjusted from settings (bottom left/right, top left/right).

How to use:

Risk Management & Diversification:

Quickly assess if two assets move together (positive correlation), in opposite directions (negative correlation), or independently.

Pairs Trading:

Identify opportunities when correlation diverges from historical norms.

Portfolio Construction:

Avoid overexposure to highly correlated assets, or use negative correlation for hedging.

Limitations & Tips:

Correlation values are based on historical returns and may change during periods of market stress or volatility.

Use multiple lookback periods (short, medium, long) for a more robust view.

Correlation does not imply causation—always complement with additional analysis.

Script Features:

User-selectable comparison asset and lookback window.

Real-time correlation calculation.

Clean summary table with correlation stats.

Optional alert logic and correlation plot for more advanced usage.

If you find this indicator useful, please leave a like and let me know your suggestions for improvements!

Correlation MA – 15 Assets + Average (Optional)This indicator calculates the moving average of the correlation coefficient between your charted asset and up to 15 user-selected symbols. It helps identify uncorrelated or inversely correlated assets for diversification, pair trading, or hedging.

Features:

✅ Compare your current chart against up to 15 assets

✅ Toggle assets on/off individually

✅ Custom correlation and MA lengths

✅ Real-time average correlation line across enabled assets

✅ Horizontal lines at +1, 0, and -1 for easy visual reference

Ideal for:

Portfolio diversification analysis

Finding low-correlation stocks

Mean-reversion & pair trading setups

Crypto, equities, ETFs

To use: set the benchmark chart (e.g. TSLA), choose up to 15 assets, and adjust settings as needed. Look for assets with correlation near 0 or negative values for uncorrelated performance.

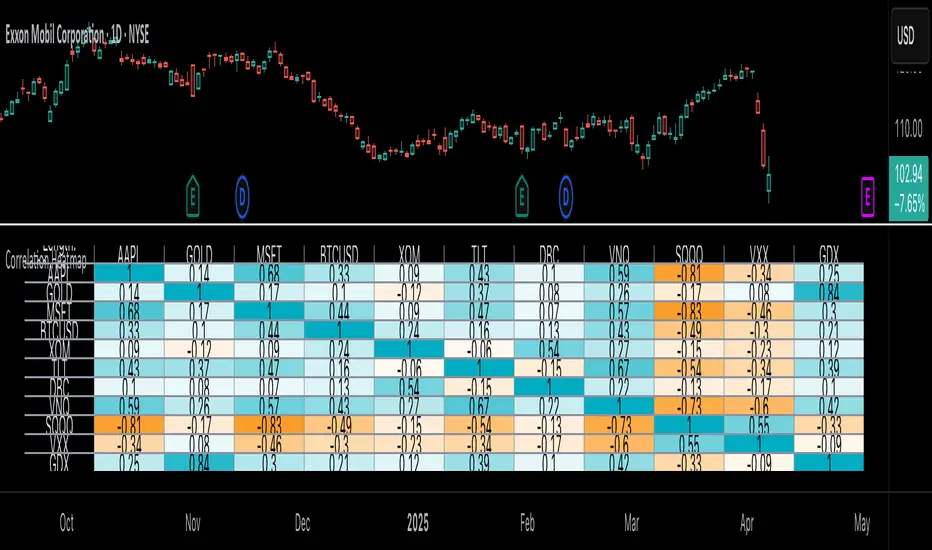

Correlation Heatmap█ OVERVIEW

This indicator creates a correlation matrix for a user-specified list of symbols based on their time-aligned weekly or monthly price returns. It calculates the Pearson correlation coefficient for each possible symbol pair, and it displays the results in a symmetric table with heatmap-colored cells. This format provides an intuitive view of the linear relationships between various symbols' price movements over a specific time range.

█ CONCEPTS

Correlation

Correlation typically refers to an observable statistical relationship between two datasets. In a financial time series context, it usually represents the extent to which sampled values from a pair of datasets, such as two series of price returns, vary jointly over time. More specifically, in this context, correlation describes the strength and direction of the relationship between the samples from both series.

If two separate time series tend to rise and fall together proportionally, they might be highly correlated. Likewise, if the series often vary in opposite directions, they might have a strong anticorrelation . If the two series do not exhibit a clear relationship, they might be uncorrelated .

Traders frequently analyze asset correlations to help optimize portfolios, assess market behaviors, identify potential risks, and support trading decisions. For instance, correlation often plays a key role in diversification . When two instruments exhibit a strong correlation in their returns, it might indicate that buying or selling both carries elevated unsystematic risk . Therefore, traders often aim to create balanced portfolios of relatively uncorrelated or anticorrelated assets to help promote investment diversity and potentially offset some of the risks.

When using correlation analysis to support investment decisions, it is crucial to understand the following caveats:

• Correlation does not imply causation . Two assets might vary jointly over an analyzed range, resulting in high correlation or anticorrelation in their returns, but that does not indicate that either instrument directly influences the other. Joint variability between assets might occur because of shared sensitivities to external factors, such as interest rates or global sentiment, or it might be entirely coincidental. In other words, correlation does not provide sufficient information to identify cause-and-effect relationships.

• Correlation does not predict the future relationship between two assets. It only reflects the estimated strength and direction of the relationship between the current analyzed samples. Financial time series are ever-changing. A strong trend between two assets can weaken or reverse in the future.

Correlation coefficient

A correlation coefficient is a numeric measure of correlation. Several coefficients exist, each quantifying different types of relationships between two datasets. The most common and widely known measure is the Pearson product-moment correlation coefficient , also known as the Pearson correlation coefficient or Pearson's r . Usually, when the term "correlation coefficient" is used without context, it refers to this correlation measure.

The Pearson correlation coefficient quantifies the strength and direction of the linear relationship between two variables. In other words, it indicates how consistently variables' values move together or in opposite directions in a proportional, linear manner. Its formula is as follows:

𝑟(𝑥, 𝑦) = cov(𝑥, 𝑦) / (𝜎𝑥 * 𝜎𝑦)

Where:

• 𝑥 is the first variable, and 𝑦 is the second variable.

• cov(𝑥, 𝑦) is the covariance between 𝑥 and 𝑦.

• 𝜎𝑥 is the standard deviation of 𝑥.

• 𝜎𝑦 is the standard deviation of 𝑦.

In essence, the correlation coefficient measures the covariance between two variables, normalized by the product of their standard deviations. The coefficient's value ranges from -1 to 1, allowing a more straightforward interpretation of the relationship between two datasets than what covariance alone provides:

• A value of 1 indicates a perfect positive correlation over the analyzed sample. As one variable's value changes, the other variable's value changes proportionally in the same direction .

• A value of -1 indicates a perfect negative correlation (anticorrelation). As one variable's value increases, the other variable's value decreases proportionally.

• A value of 0 indicates no linear relationship between the variables over the analyzed sample.

Aligning returns across instruments

In a financial time series, each data point (i.e., bar) in a sample represents information collected in periodic intervals. For instance, on a "1D" chart, bars form at specific times as successive days elapse.

However, the times of the data points for a symbol's standard dataset depend on its active sessions , and sessions vary across instrument types. For example, the daily session for NYSE stocks is 09:30 - 16:00 UTC-4/-5 on weekdays, Forex instruments have 24-hour sessions that span from 17:00 UTC-4/-5 on one weekday to 17:00 on the next, and new daily sessions for cryptocurrencies start at 00:00 UTC every day because crypto markets are consistently open.

Therefore, comparing the standard datasets for different asset types to identify correlations presents a challenge. If two symbols' datasets have bars that form at unaligned times, their correlation coefficient does not accurately describe their relationship. When calculating correlations between the returns for two assets, both datasets must maintain consistent time alignment in their values and cover identical ranges for meaningful results.

To address the issue of time alignment across instruments, this indicator requests confirmed weekly or monthly data from spread tickers constructed from the chart's ticker and another specified ticker. The datasets for spreads are derived from lower-timeframe data to ensure the values from all symbols come from aligned points in time, allowing a fair comparison between different instrument types. Additionally, each spread ticker ID includes necessary modifiers, such as extended hours and adjustments.

In this indicator, we use the following process to retrieve time-aligned returns for correlation calculations:

1. Request the current and previous prices from a spread representing the sum of the chart symbol and another symbol ( "chartSymbol + anotherSymbol" ).

2. Request the prices from another spread representing the difference between the two symbols ( "chartSymbol - anotherSymbol" ).

3. Calculate half of the difference between the values from both spreads ( 0.5 * (requestedSum - requestedDifference) ). The results represent the symbol's prices at times aligned with the sample points on the current chart.

4. Calculate the arithmetic return of the retrieved prices: (currentPrice - previousPrice) / previousPrice

5. Repeat steps 1-4 for each symbol requiring analysis.

It's crucial to note that because this process retrieves prices for a symbol at times consistent with periodic points on the current chart, the values can represent prices from before or after the closing time of the symbol's usual session.

Additionally, note that the maximum number of weeks or months in the correlation calculations depends on the chart's range and the largest time range common to all the requested symbols. To maximize the amount of data available for the calculations, we recommend setting the chart to use a daily or higher timeframe and specifying a chart symbol that covers a sufficient time range for your needs.

█ FEATURES

This indicator analyzes the correlations between several pairs of user-specified symbols to provide a structured, intuitive view of the relationships in their returns. Below are the indicator's key features:

Requesting a list of securities

The "Symbol list" text box in the indicator's "Settings/Inputs" tab accepts a comma-separated list of symbols or ticker identifiers with optional spaces (e.g., "XOM, MSFT, BITSTAMP:BTCUSD"). The indicator dynamically requests returns for each symbol in the list, then calculates the correlation between each pair of return series for its heatmap display.

Each item in the list must represent a valid symbol or ticker ID. If the list includes an invalid symbol, the script raises a runtime error.

To specify a broker/exchange for a symbol, include its name as a prefix with a colon in the "EXCHANGE:SYMBOL" format. If a symbol in the list does not specify an exchange prefix, the indicator selects the most commonly used exchange when requesting the data.

Note that the number of symbols allowed in the list depends on the user's plan. Users with non-professional plans can compare up to 20 symbols with this indicator, and users with professional plans can compare up to 32 symbols.

Timeframe and data length selection

The "Returns timeframe" input specifies whether the indicator uses weekly or monthly returns in its calculations. By default, its value is "1M", meaning the indicator analyzes monthly returns. Note that this script requires a chart timeframe lower than or equal to "1M". If the chart uses a higher timeframe, it causes a runtime error.

To customize the length of the data used in the correlation calculations, use the "Max periods" input. When enabled, the indicator limits the calculation window to the number of periods specified in the input field. Otherwise, it uses the chart's time range as the limit. The top-left corner of the table shows the number of confirmed weeks or months used in the calculations.

It's important to note that the number of confirmed periods in the correlation calculations is limited to the largest time range common to all the requested datasets, because a meaningful correlation matrix requires analyzing each symbol's returns under the same market conditions. Therefore, the correlation matrix can show different results for the same symbol pair if another listed symbol restricts the aligned data to a shorter time range.

Heatmap display

This indicator displays the correlations for each symbol pair in a heatmap-styled table representing a symmetric correlation matrix. Each row and column corresponds to a specific symbol, and the cells at their intersections correspond to symbol pairs . For example, the cell at the "AAPL" row and "MSFT" column shows the weekly or monthly correlation between those two symbols' returns. Likewise, the cell at the "MSFT" row and "AAPL" column shows the same value.

Note that the main diagonal cells in the display, where the row and column refer to the same symbol, all show a value of 1 because any series of non-na data is always perfectly correlated with itself.

The background of each correlation cell uses a gradient color based on the correlation value. By default, the gradient uses blue hues for positive correlation, orange hues for negative correlation, and white for no correlation. The intensity of each blue or orange hue corresponds to the strength of the measured correlation or anticorrelation. Users can customize the gradient's base colors using the inputs in the "Color gradient" section of the "Settings/Inputs" tab.

█ FOR Pine Script® CODERS

• This script uses the `getArrayFromString()` function from our ValueAtTime library to process the input list of symbols. The function splits the "string" value by its commas, then constructs an array of non-empty strings without leading or trailing whitespaces. Additionally, it uses the str.upper() function to convert each symbol's characters to uppercase.

• The script's `getAlignedReturns()` function requests time-aligned prices with two request.security() calls that use spread tickers based on the chart's symbol and another symbol. Then, it calculates the arithmetic return using the `changePercent()` function from the ta library. The `collectReturns()` function uses `getAlignedReturns()` within a loop and stores the data from each call within a matrix . The script calls the `arrayCorrelation()` function on pairs of rows from the returned matrix to calculate the correlation values.

• For consistency, the `getAlignedReturns()` function includes extended hours and dividend adjustment modifiers in its data requests. Additionally, it includes other settings inherited from the chart's context, such as "settlement-as-close" preferences.

• A Pine script can execute up to 40 or 64 unique `request.*()` function calls, depending on the user's plan. The maximum number of symbols this script compares is half the plan's limit, because `getAlignedReturns()` uses two request.security() calls.

• This script can use the request.security() function within a loop because all scripts in Pine v6 enable dynamic requests by default. Refer to the Dynamic requests section of the Other timeframes and data page to learn more about this feature, and see our v6 migration guide to learn what's new in Pine v6.

• The script's table uses two distinct color.from_gradient() calls in a switch structure to determine the cell colors for positive and negative correlation values. One call calculates the color for values from -1 to 0 based on the first and second input colors, and the other calculates the colors for values from 0 to 1 based on the second and third input colors.

Look first. Then leap.

Uptrick: Portfolio Allocation DiversificationIntro

The Uptrick: Portfolio Allocation Diversification script is designed to help traders and investors manage multiple assets simultaneously. It generates signals based on various trading systems, allocates capital using different diversification methods, and displays real-time metrics and performance tables on the chart. The indicator compares active trading strategies with a separate long-term holding (HODL) simulation, allowing you to see how a systematic trading approach stacks up against a simple buy-and-hold strategy.

------------------------------------------------------------------------

Trading System Selection

1. No signals (none)

In this mode, the script does not produce bullish or bearish indicators; every asset stays in a neutral stance. This setup is useful if you prefer to observe how capital might be distributed based solely on the chosen diversification method, with no influence from directional signals.

2. rsi – neutral

This mode uses an index-based measure of whether an asset appears overbought or oversold. It generates a bearish signal if market conditions point to overbought territory, and a bullish signal if they indicate oversold territory. If neither extreme surfaces, it remains neutral. Some traders apply this in sideways or range-bound conditions, where overbought and oversold levels often hint at possible turning points. It does not specifically account for divergence patterns.

3. rsi – long only

In this setting, the system watches for instances where momentum readings strengthen even if the asset’s price is still under pressure or setting new lows. It also considers oversold levels as potential signals for a bullish setup. When such conditions emerge, the script flags a possible move to the upside, ignoring indications that might otherwise suggest a bearish trend. This approach is generally favored by those who want to concentrate exclusively on identifying price recoveries.

4. rsi – short only

Here, the script focuses on spotting signs of deteriorating momentum while an asset’s price remains relatively high or attempts further gains. It also checks whether the market is drifting into overbought territory, suggesting a potential decline. Under such conditions, it issues a bearish signal. It provides no bullish alerts, making it particularly suitable for traders who look to take advantage of overvalued scenarios or protect themselves against sudden downward moves.

5. Deviation from fair value

Under this system, the script judges how far the current price may have strayed from what is considered typical, taking into account normal fluctuations. If the asset appears to be trading at an unusually low level compared to that reference, it is flagged as bullish. If it seems abnormally high, a bearish signal is issued. This can be applied in various market environments to seek opportunities that arise from perceived mispricing.

6. Percentile channel valuation

In this mode, the script determines where an asset's price stands within a historical distribution, highlighting whether it has reached unusually high or low territory compared to its recent past. When the price reaches what is deemed an extreme reading, it may indicate that a reversal is more likely. This approach is often used by traders who watch for statistical outliers and potential reversion to a more typical trading range.

7. ATH valuation

This technique involves comparing an asset's current price with its previously recorded peak values. The script then interprets whether the price is positioned so far below the all-time high that it looks discounted, or so close to that high that it could be overextended. Such perspective is favored by market participants who want to see if an asset still has ample room to climb before matching historic extremes, or if it is nearing a possible ceiling.

8. Z-score system

Here, the script measures how far above or below a standard reference average an asset's price may be, translated into standardized units. Substantial negative readings can suggest a price that might be unusually weak, prompting a bullish indication, while large positive readings could signal overextension and lead to a bearish call. This method is useful for traders watching for abrupt deviations from a norm that often invite a reversion to more balanced levels.

RSI Divergence Period

This input is particularly relevant for the RSI - Long Only and RSI - Short Only modes. The period determines how many bars in the past you compare RSI values to detect any divergences.

------------------------------------------------------------------------

Diversification Method

Once the script has determined a bullish, bearish, or neutral stance for each asset, it then calculates how to distribute capital among all included assets. The diversification method sets the weighting logic.

1. None

Gives each asset an equal weight. For example, if you have five included assets, each might get 20 percent. This is a simple baseline.

2. Risk-Adjusted Expected Return Using Volatility Clustering

Emphasizes each asset’s average returns relative to its observed risk or volatility tendencies. Assets that exhibit good risk-adjusted returns combined with moderate or lower volatility may receive higher weights than more volatile or less appealing assets. This helps steer capital toward assets that have historically provided a better ratio of return to risk.

3. Relative Strength

Allocates more capital to assets that show stronger price strength compared to a reference (for example, price above a long-term moving average plus a higher RSI). Assets in clear uptrends may be given higher allocations.

4. Trend-Following Indicators

Examines trend-based signals, like positive momentum measurements or upward-trending strength indicators, to assign more weight to assets demonstrating strong directional moves. This suits those who prefer to latch onto trending markets.

5. Volatility-Adjusted Momentum

Looks for assets that have strong price momentum but relatively subdued volatility. The script tends to reward assets that are trending well yet are not too volatile, aiming for stable upward performance rather than massive swings.

6. Correlation-Based Risk Parity

Attempts to weight assets in such a way that the overall portfolio risk is more balanced. Although it is not an advanced correlation matrix approach in a strict sense, it conceptually scales each asset’s weight so no single outlier heavily dominates.

7. Omega Ratio Maximization

Gives preference to assets with higher omega ratios. This ratio can be interpreted as the probability-weighted gains versus losses. Assets with a favorable skew are given more capital.

8. Liquidity-Weighted Valuation

Considers each asset’s average trading liquidity, such as the combination of volume and price. More liquid assets typically receive a higher allocation because they can be entered or exited with lower slippage. If the trading system signals bullishness, that can further boost the allocation, and if it signals bearishness, the allocation might be set to zero or reduced drastically.

9. Drawdown-Controlled Allocation (DCA)

Examines each asset’s maximum drawdown over a recent window. Assets experiencing lighter drawdowns (thus indicating somewhat less downside volatility) receive higher allocations, aiming for a smoother overall equity curve.

------------------------------------------------------------------------

Portfolio and Allocation Settings

Portfolio Value

Defines how much total capital is available for the strategy-based investment portion. For example, if set to 10,000, then each asset’s monetary allocation is determined by the percentage weighting times 10,000.

Use Fixed Allocation

When enabled, the script calculates the initial allocation percentages after 50 bars of data have passed. It then locks those percentages for the remainder of the backtest or real-time session. This feature allows traders to test a static weighting scenario to see how it differs from recalculating weights at each bar.

------------------------------------------------------------------------

HODL Simulator

The script has a separate simulation that accumulates positions in an asset whenever it appears to be recovering from an undervalued state. This parallel tracking is intended to contrast a simple buy-and-hold approach with the more adaptive allocation methods used elsewhere in the script.

HODL Buy Quantity

Each time an asset transitions from an undervalued state to a recovery phase, the simulator executes a purchase of a predefined quantity. For example, if set to 0.5 units, the system will accumulate this amount whenever conditions indicate a shift away from undervaluation.

HODL Buy Threshold

This parameter determines the level at which the simulation identifies an asset as transitioning out of an undervalued state. When the asset moves above this threshold after previously being classified as undervalued, a buy order is triggered. Over time, the performance of these accumulated positions is tracked, allowing for a comparison between this passive accumulation method and the more dynamic allocation strategy.

------------------------------------------------------------------------

Asset Table and Display Settings

The script displays data in multiple tables directly on your chart. You can toggle these tables on or off and position them in various corners of your TradingView screen.

Asset Info Table Position

This table provides key details for each included asset, displaying:

Symbol – Identifies the trading pair being monitored. This helps users keep track of which assets are included in the portfolio allocation process.

Current Trading Signal – Indicates whether the asset is in a bullish, bearish, or neutral state based on the selected trading system. This assists in quickly identifying which assets are showing potential trade opportunities.

Volatility Approximation – Represents the asset’s historical price fluctuations. Higher volatility suggests greater price swings, which can impact risk management and position sizing.

Liquidity Estimate – Reflects the asset’s market liquidity, often based on trading volume and price activity. More liquid assets tend to have lower transaction costs and reduced slippage, making them more favorable for active strategies.

Risk-Adjusted Return Value – Measures the asset’s returns relative to its risk level. This helps in determining whether an asset is generating efficient returns for the level of volatility it experiences, which is useful when making allocation decisions.

2. Strategy Allocation Table Position

Displays how your selected diversification method converts each asset into an allocation percentage. It also shows how much capital is being invested per asset, the cumulative return, standard performance metrics (for example, Sharpe ratio), and the separate HODL return percentage.

Symbol – Displays the asset being analyzed, ensuring clarity in allocation distribution.

Allocation Percentage – Represents the proportion of total capital assigned to each asset. This value is determined by the selected diversification method and helps traders understand how funds are distributed within the portfolio.

Investment Amount – Converts the allocation percentage into a dollar value based on the total portfolio size. This shows the exact amount being invested in each asset.

Cumulative Return – Tracks the total return of each asset over time, reflecting how well it has performed since the strategy began.

Sharpe Ratio – Evaluates the asset’s return in relation to its risk by comparing excess returns to volatility. A higher Sharpe ratio suggests a more favorable risk-adjusted performance.

Sortino Ratio – Similar to the Sharpe ratio, but focuses only on downside risk, making it more relevant for traders who prioritize minimizing losses.

Omega Ratio – Compares the probability of achieving gains versus losses, helping to assess whether an asset provides an attractive risk-reward balance.

Maximum Drawdown – Measures the largest percentage decline from an asset’s peak value to its lowest point. This metric helps traders understand the worst-case loss scenario.

HODL Return Percentage – Displays the hypothetical return if the asset had been bought and held instead of traded actively, offering a direct comparison between passive accumulation and the active strategy.

3. Profit Table

If the Profit Table is activated, it provides a summary of the actual dollar-based gains or losses for each asset and calculates the overall profit of the system. This table includes separate columns for profit excluding HODL and the combined total when HODL gains are included. As seen in the image below, this allows users to compare the performance of the active strategy against a passive buy-and-hold approach. The HODL profit percentage is derived from the Portfolio Value input, ensuring a clear comparison of accumulated returns.

4. Best Performing Asset Table

Focuses on the single highest-returning or highest-profit asset at that moment. It highlights the symbol, the asset’s cumulative returns, risk metrics, and other relevant stats. This helps identify which asset is currently outperforming the rest.

5. Most Profitable Asset

A simpler table that underscores the asset producing the highest absolute dollar profit across the portfolio.

------------------------------------------------------------------------

Multi Asset Selection

You can include up to ten different assets (such as BTCUSDT, ETHUSDT, ADAUSDT, and so on) in this script. Each asset has two inputs: one to enable or disable its inclusion, and another to select its trading pair symbol. Once you enable an asset, the script requests the relevant market data from TradingView.

------------------------------------------------------------------------

Uniqness and Features

1. Multiple Data Fetches

Each asset is pulled from the chart’s timeframe, along with various metrics such as RSI, volatility approximations, and trend indicators.

2. Various Risk and Performance Metrics

The script internally keeps track of different measures, like Sharpe ratio (a measure of average return adjusted for risk), Sortino ratio (which focuses on downside volatility), Omega ratio, and maximum drawdown. These metrics feed into the strategy allocation table, helping you quickly assess the risk-and-return profile of each asset.

3. Real-Time Tables

Instead of having to set up complex spreadsheets or external dashboards, the script updates all tables on every new bar. The color schemes in these tables are designed to draw attention to bullish or bearish signals, positive or negative returns, and so forth.

4. HODL Comparison

You can visually compare the active strategy’s results to a separate continuous buy-on-dips accumulation strategy. This allows for insight into whether your dynamic approach truly beats a simpler, more patient method.

5. Locking Allocations

The Use Fixed Allocation input is convenient for those who want to see how holding a fixed distribution of capital performs over time. It helps in distinguishing between constant rebalancing vs a fixed, set-and-forget style.

------------------------------------------------------------------------

How to use

1. Add the Script to Your Chart

Once added, open the settings panel to configure your asset list, choose a trading system, and select the diversification approach.

2. Select Assets

Pick up to ten symbols to monitor. Disable any you do not want included. Each included asset is then handled for signals, diversification, and performance metrics.

3. Choose Trading System

Decide if you prefer RSI-based signals, a fair-value approach, or a percentile-based method, among others. The script will then flag assets as bullish, bearish, or neutral according to that selection.

4. Pick a Diversification Method

For example, you might choose Trend-Following Indicators if you believe momentum stocks or cryptocurrencies will continue their trends. Or you could use the Omega Ratio approach if you want to reward assets that have had a favorable upside probability.

5. Set Portfolio Value and HODL Parameters

Enter how much capital you want to allocate in total (for the dynamic strategy) and adjust HODL buy quantities and thresholds as desired. (HODL Profit % is calculated from the Portfolio Value)

6. Inspect the Tables

On the chart, the script can display multiple tables showing your allocations, returns, risk metrics, and which assets are leading or lagging. Monitor these to make decisions about capital distribution or see how the strategy evolves.

------------------------------------------------------------------------

Additional Remarks

This script aims to simplify multi-asset portfolio management in a single tool. It emphasizes user-friendliness by color-coding the data in tables, so you do not need extra spreadsheets. The script is also flexible in letting you lock allocations or compare dynamic updates.

Always remember that no script can guarantee profitable outcomes. Real markets involve unpredictability, and real trading includes fees, slippage, and liquidity constraints not fully accounted for here. The script uses real-time and historical data for demonstration and educational purposes, providing a testing environment for various systematic strategies.

Performance Considerations

Due to the complexity of this script, users may experience longer loading times, especially when handling multiple assets or using advanced allocation methods. In some cases, calculations may time out if too many settings are adjusted simultaneously. If this occurs, removing and reapplying the indicator to the chart can help reset the process. Additionally, it is recommended to configure inputs gradually instead of adjusting all parameters at once, as excessive changes can extend the script’s loading duration beyond TradingView’s processing limits.

------------------------------------------------------------------------

Originality

This script stands out by integrating multiple asset management techniques within a single indicator, eliminating the need for multiple scripts or external portfolio tools. Unlike traditional single-asset strategies, it simultaneously evaluates multiple assets, applies systematic allocation logic, and tracks risk-adjusted performance in real time. The script is designed to function within TradingView’s script limitations while still allowing for complex portfolio simulations, making it an efficient tool for traders managing diverse holdings. Additionally, its combination of systematic trading signals with allocation-based diversification provides a structured approach to balancing exposure across different market conditions. The dynamic interplay between adaptive trading strategies and passive accumulation further differentiates it from conventional strategy indicators that focus solely on directional signals without considering capital allocation.

Conclusion

Uptrick: Portfolio Allocation Diversification pulls multiple assets into one efficient workflow, where each asset’s signal, volatility, and performance is measured, then assigned a share of capital according to your selected diversification method. The script accommodates both dynamic rebalancing and a locked allocation style, plus an ongoing HODL simulation for passive accumulation comparison. It neatly visualizes the entire process through on-chart tables that are updated every bar.

Traders and investors looking for ways to manage multiple assets under one unified framework can explore the different modules within this script to find what suits their style. Users can quickly switch among trading systems, vary the allocation approach, or review side-by-side performance metrics to see which method aligns best with their risk tolerance and market perspective.

Lead-Lag Market Detector [CryptoSea]The Lead-Lag Market Detector is an advanced tool designed to help traders identify leading and lagging assets within a chosen market. This indicator leverages correlation analysis to rank assets based on their influence, making it ideal for traders seeking to optimise their portfolio or spot key market trends.

Key Features

Dynamic Asset Ranking: Utilises real-time correlation calculations to rank assets by their influence on the market, helping traders identify market leaders and laggers.

Customisable Parameters: Includes adjustable lookback periods and correlation thresholds to adapt the analysis to different market conditions and trading styles.

Comprehensive Asset Coverage: Supports up to 30 assets, offering broad market insights across cryptocurrencies, stocks, or other markets.

Gradient-Enhanced Table Display: Presents results in a colour-coded table, where assets are ranked dynamically with influence scores, aiding in quick visual analysis.

In the example below, the ranking highlights how assets tend to move in groups. For instance, BTCUSDT, ETHUSDT, BNBUSDT, SOLUSDT, and LTCUSDT are highly correlated and moving together as a group. Similarly, another group of correlated assets includes XRPUSDT, FILUSDT, APEUSDT, XTZUSDT, THETAUSDT, and CAKEUSDT. This grouping of assets provides valuable insights for traders to diversify or spread exposure.

If you believe one asset in a group is likely to perform well, you can spread your exposure into other correlated assets within the same group to capitalise on their collective movement. Additionally, assets like AVAXUSDT and ZECUSDT, which appear less correlated or uncorrelated with the rest, may offer opportunities to act as potential hedges in your trading strategy.

How it Works

Correlation-Based Scoring: Calculates pairwise correlations between assets over a user-defined lookback period, identifying assets with high influence scores as market leaders.

Customisable Thresholds: Allows traders to define a correlation threshold, ensuring the analysis focuses only on significant relationships between assets.

Dynamic Score Calculation: Scores are updated dynamically based on the timeframe and input settings, providing real-time insights into market behaviour.

Colour-Enhanced Results: The table display uses gradients to visually distinguish between leading and lagging assets, simplifying data interpretation.

Application

Portfolio Optimisation: Identifies influential assets to help traders allocate their portfolio effectively and reduce exposure to lagging assets.

Market Trend Identification: Highlights leading assets that may signal broader market trends, aiding in strategic decision-making.

Customised Trading Strategies: Adapts to various trading styles through extensive input settings, ensuring the analysis meets the specific needs of each trader.

The Lead-Lag Market Detector by is an essential tool for traders aiming to uncover market leaders and laggers, navigate complex market dynamics, and optimise their trading strategies with precision and insight.

Oster's Investment Plan (OIP)Oster's Investment Plan (OIP) is a versatile and powerful tool designed to help traders and investors create and evaluate their long-term investment strategies . Unlike many conventional investment tools, OIP emphasizes customization, allowing users to design personalized savings plans and compare the performance of their portfolios against chosen benchmarks. Whether you're setting up a new investment plan or analyzing an existing one, OIP provides comprehensive insights into your portfolio's growth and performance.

Tailored Investment Planning:

OIP enables users to create customized savings plans with up to five assets from any available on TradingView. This feature offers unparalleled flexibility in asset selection, allowing investors to diversify their portfolios across various markets and asset classes. With OIP , users can freely determine the weighting of each asset, ensuring the portfolio aligns with their individual investment strategies and risk preferences .

Comprehensive Fee and Cost Analysis:

One of OIPs standout features is its ability to factor in nearly all cost components associated with investing. This includes annual deposit fees, fees on savings rates, tax deductions on dividend payouts, potential savings rate dynamics, and the Total Expense Ratio (TER) of funds. By considering these costs, OIP provides a realistic and accurate projection of your portfolio's growth, helping you identify the most cost-effective broker or investment platform .

Benchmark Comparison:

OIP allows users to select any benchmark to compare their portfolio's performance. This feature enables investors to gauge their portfolio's returns against broader market indices or specific sector benchmarks, providing valuable insights into the effectiveness of their investment strategy. The ability to choose and change benchmarks ensures that OIP remains relevant and adaptable to different investment goals and market conditions.

Reinvestment of Dividends:

For investors who prefer to reinvest their dividends, OIP can incorporate annual dividend reinvestments into the portfolio's growth curve . This feature accounts for the compounding effect of reinvested dividends, offering a more accurate representation of potential portfolio performance over time.

Use Cases:

Creating a Personalized Savings Plan:

With OIP , users can design a personalized savings plan tailored to their financial goals and investment horizon. By selecting up to five assets and determining their weightings, investors can create a diversified portfolio that suits their risk tolerance and investment preferences. OIP then calculates the potential growth of the portfolio, factoring in all relevant costs and fees, to provide a clear picture of the expected returns.

Evaluating Broker Fees:

For those who have already established a long-term investment plan, OIP can be used to compare the costs associated with different brokerage platforms . By inputting the fee structures of various brokers, investors can identify the most cost-effective option, ensuring that they maximize their returns by minimizing fees and expenses.

Sophisticated Calculation Methodology:

OIP employs a robust calculation methodology to derive its insights. It takes into account the initial investment, recurring deposits, fees, taxes, and the performance of the selected assets. The tool adjusts for annual deposit fees, dynamic savings rates, and the reinvestment of dividends, providing a detailed and nuanced evaluation of the portfolio's performance.

Interpretation:

OIP plots the total equity of the savings plan and the chosen benchmark , allowing users to visually compare the performance of their portfolio against the benchmark. The tool also displays the total invested amount , helping investors track their contributions and returns over time. Dynamic color coding enhances visual clarity, with the savings plan and benchmark differentiated by distinct colors for easy interpretation.

Conclusion:

Oster's Investment Plan (OIP) represents a significant advancement in investment planning and portfolio analysis. By offering customizable parameters, comprehensive fee considerations, and benchmark comparisons, OIP equips investors with a powerful tool for creating and evaluating their investment strategies. Whether you're a seasoned investor or new to the market, OIP provides invaluable insights that can inform and enrich your investment journey.

By integrating these features, OIP stands out as a sophisticated and user-friendly tool for managing and optimizing investment portfolios. Its emphasis on customization, detailed cost analysis, and flexible benchmarking makes it an essential resource for any investor looking to maximize their returns and achieve their financial goals.

GDP BreakdownProvides an easy way for viewing the sub sections that make up a country's total GDP. Not all countries provide data for each subsector (Agriculture, Construction, Manufacturing, Mining, Public Administration, Services, Utilities). Only countries that provide complete data are able to be selected in the settings. If I've missed any please let me know in the comment section so they can be added. This is much easier than having to individually selecting each ticker for each country when looking to compare how diversified an economy is.

Diversified Investment EMA Cross Strategy SimulatorThis simulating indicator proves that even if you use a simple strategy, you can reduce your risk by diversifying your investments.

The strategy itself is simple.(only long)

Buy when 50 days EMA crosses over 200 days EMA.

Sell when 50 days EMA crosses under 200 days EMA.

Or, stop loss when the asset falls by 2% (eg).

Using this simple strategy on an asset is just a test of your luck.

However, this capital change graph shows that risk can be reduced by diversifying investment into eight assets rather than one asset.

Options

Total Assets Capital Change represents the sum of capital changes for 8 assets. The gray line is the initial capital.

Each Asset Capital Change represents all eight asset capital changes. In this case, the gray line is displayed as the initial capital divided by 8.

The rest of the options show a graph of capital change for each asset, showing when buys and sells occurred.

And set the start date, initial capital, stop loss %, and commission.

And select the 8 assets you want to invest in and you are ready to go. To effectively reduce risk, uncoupled assets would be better if possible.

The table in the lower right shows the selected asset and color.

Please enjoy the simulation.

Coefficient of Variation - EMA and SMA StDevYet another way to try and measure volatility. An alternative to using ATR is Standard Deviation, it can be used to measure volatility or what is also known as risk. SD measures how dispersed or far away the data is from the mean. It's commonly seen in risk management formulas or portfolio diversification formulas. The problem however is that the numbers that ATR and SD give off from one equity might not be relative to others or its own past. For example, SPY can give a large number despite not being as volatile as other equities while others being compared to can have smaller volatility numbers and still be more volatile looking.

A solution I thought of is to use percentages that are relatable to different equities. I found out another name for this idea comes from statistics and is known as coefficient of variation, also known as relative standard deviation. This helps see the volatility as a percentage and not just a number that only relates to what is being seen at the moment. I put in a border line on the zero level to see where zero is at but also to edit in case there is such a thing as a percentage number that can be too high or too low for volatility to be looked at if needed. The average and standard deviation formulas can use either simple moving average or exponential moving average.

Portfolio ManagerMeet our all-new Portfolio Manager

The idea of such a tool was the lack of anything like that out there. Recently I've seen that the culture most common around the newcomers to trading has become extraordinarily scalping-like and much leaned on high-risk operations.

Fundamental cornerstones of math and statistics that are keys to lasting networth growth have been wholly forgotten.

One of the most efficient and simple ways that I tell my friends to make money without getting too technical is diversification.

It's merely math; I suggest reading about the Modern Portfolio Theory, based on the work about diversification of uncorrelated assets by Markowitz(Nobel-winner because of that).

Translating it to mere humans, the more assets you have, the more uncorrelated they are(as in their pattern of moves are nothing alike), the fewer risks of losing money in a given time you have.

So by following such stats, it's clear to say that's always important to trade on different fronts.

To quantify and qualify who diversified you are and how much risk you're taking, we decided to create a pretty handy tool.

Let's get the samba going:

C-Index is the individual correlation score of that asset compared to the given portfolio correlation average.

C-Score is the final correlation score of your portfolio.

Below that, we got the performance tracker, whatever timeframe you're benchmarking your portfolio, it will show there. I like to back-test for one year.

And last but not least, we have a proprietary risk exposure gauge, so we run a few math tricks, and we calculate how was the maximum of your investment that was exposed through-out the time range we set in. So let's say we have a 10% risk exposure over 365 days. It means that over one year at maximum we could have lost 10% of our investment.

If you're not familiar with correlation:

-> +100 score = Fully Correlated(Similar Behaviors)

-> 0 Score = Totally Uncorrelated(Different Behaviors)

-> -100 score = Inversely Correlated(Opposite Behaviors)

So any asset that averages between -20 and 20 is very little correlated to its comparison. Therefore, their pattern of behavior tend to be independent

By comparing the change and the risk exposure, you can assess your risk/reward ratio - golden information.

Not only that, but we also added several markets so you can easily benchmark your portfolio(up to 9 custom assets) to a diversified gamma of markets in the world.

We diversified each benchmark portfolio within its available industries for maximum risk mitigation.

You can change your benchmark range, nine custom assets, labels preferences, and nine benchmark portfolios, including NIKKEI, NASDAQ, IBOV , ASX , DAX , CRYPTO, FOREX, FTSE , SHANGHAI.

If you liked what you see take a look at our signare to get access to our scripts!