Moving Average Adaptive QThe Moving Average Adaptive Q (MAAQ) was authored by Perry Kaufman in the Stocks and Commodities Magazine 06/1995

This is similar to his Kaufman Adaptive Moving Average with a few changes. This is a pretty close moving average which I like quite a bit. Try it and let me know what you think.

Send me a message and let me know what other indicators you would like to see!

Média Móvel Adaptativa (MMA)

Minkowski Distance Factor Adaptive Period MACDHi, this script comes from the idea that Ricardo Santos' Minkovski Distance Function is transferred to the period as a factor.

Minkowski distance is used as a percentage factor with the help of Relative Strength Index function.

Minkowski Distance Function Script :

And thus an adaptive MACD was created.

This script can give much better results in more optimized larger periods.

I leave the decision to determine the periods and weights.

I used the weights of 9,12,26 and periods created with multiplied by factor.

Regards.

Deviation Scaled Moving Average [ChuckBanger]This is a deviation scaled moving average original designed by John Ehlers. It is a new adaptive moving average that has the ability to rapidly adapt to volatility in price movement with minimal lag. Because it is so smooth and adapts to the volatility of the market it is by far a really great tool for spotting trend changes

MTF IQ IFM Moving AverageMTF ready adaptive MA using Ehler's IQ IFM ( In Phase - Quadrature Instantaneous Frequency Measurement ).

Ehler's formula is a method of quantitatively measuring the length of a market cycle. In this case it is used to calculate the "optimal" adaptive EMA.

Theoretically the length generated by Ehler's formula could be used in many indicators and it's been placed within it's own function so you should be able to simply copy/paste it. HOWEVER pine will not accept series variables for the length input used in built-in functions. You will have to manually code (or find) a version of your indicator that doesn't use the pine built in.

Options :

type : optionally add volume weighting

range : historical range used in IQ IFM

cycle length mult : method to create faster/slower MAs. eg 0.5 is half the length of a cycle and a faster EMA ie EMA10 vs EMA20

low sat fix : some cryptocurrencies with low satoshi values cause an issue with the calculation, if you get no/nonsensical lines, enable this. Shouldn't affect other instruments, but can be disabled just in case.

MTF options: run the calculation on an alternative timeframe

--------------------------------------

If you find it useful please consider a tip/donation :

BTC - 3BMEXEDyWJ58eXUEALYPadbn1wwWKmf6sA

MAMA FAMA KAMA.. chameleon 🎵

Uses Kaufmann's Efficiency Ratio to generate adaptive inputs for Ehler's MAMA/FAMA. Alphas from the Hilbert transform are then used in place for the KAMA calculation.

Original MAMA/FAMA by everget : link

--------------------------------------

If you find it useful please consider a tip/donation :

BTC - 3BMEXEDyWJ58eXUEALYPadbn1wwWKmf6sA

EQma - Adaptive Smoothing Based On Optimal Markets DetectionIntroduction

"You don’t put sunscreen when there is no sun, you don’t use an umbrella when there is no rain, you don’t use a kite when there is no wind, so why would you use a trend following strategy when there is no trend ?"

This is how i start my 4th paper "A New Technical Indicator For Optimal Markets Detection" where i present two new technical indicators. We talked about the first one, running equity, which aim to detect the best moment to enter trades, based on this new metric i made an adaptive moving average.

You can see the full paper here figshare.com

The Indicator

The moving average is based on exponential averaging and use a smoothing variable alpha based on the running equity metric, in order to calculate alpha the running equity is divided by the optimal equity which show the best returns possible for the conditions used. Basically the indicator work as follow :

When the running equity is close to the optimal equity it means that the price need no/little filtering since it does not contain information that need to be filtered, therefore alpha is high, however when the running equity is far from the optimal equity this mean that the price posses malign information that need to be removed.

This is why the indicator will be closer to the price when length is high :

See the full paper for an explanation on how this work.

I added various options for the indicator, one will reduce the lag by squaring alpha, thus giving for length = 14 :

The efficient option will make use of recursion to provide a more efficient indicator :

In green the efficient version, note how this option can allow a better fit with the price.

Conclusion

This is an indicator but at its core its rather a framework, if you have read the paper you'll see that the conditions are just 1 and -1 that changes with time, basically its like making a strategy with :

Condition = if buy then 1 else if sell then -1 else Precedent value of condition.

So those two indicators allow to give useful and usable information about your strategy. I hope it can be of use for anyone here, if so don't hesitate to send me what you made using the proposed indicator (and with all my indicators in general). If you are writing a paper and you think this indicator could fit in your work then let me know so i can be aware of it :)

Thanks for reading !

Acknowledgement

My papers are quite ridiculous but they still manage to get some views, some researchers don't even reach those number in so little time which is quite unfortunate but also really motivating for me, so thanks to those who take time to read them and give me some feedback :)

Kaufman Adaptive Correlation OscillatorIntroduction

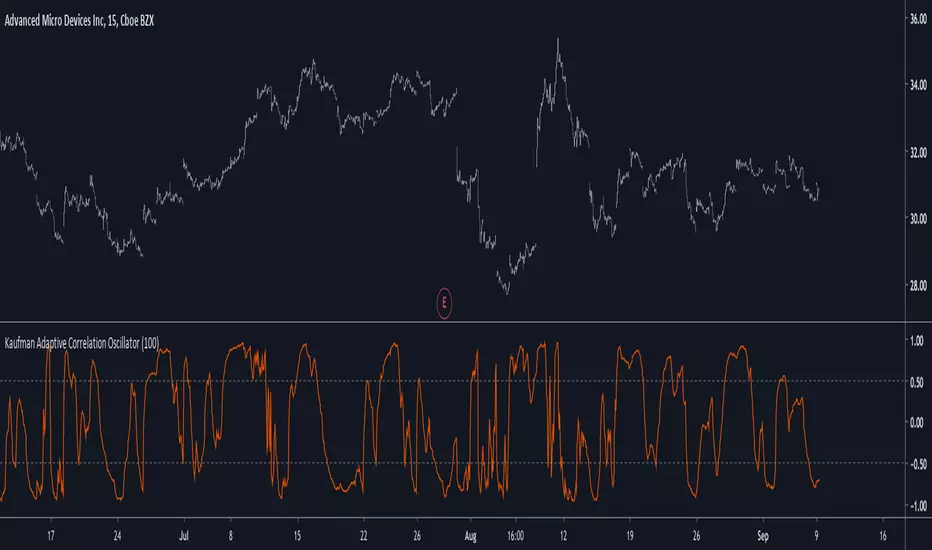

The correlation oscillator is a technical indicator that measure the linear relationship between the market closing price and a simple increasing line, the indicator is in a (-1,1) range and rise when price is up-trending and fall when price is down-trending. Another characteristic of the indicator is its inherent smoothing which provide a noise free (to some extent) oscillator.

Such indicator use simple moving averages as well as estimates of the standard deviation for its calculation, but we can easily make it adaptive, this is why i propose this new technical indicator that create an adaptive correlation oscillator based on the Kaufman adaptive moving average.

The Indicator

The length parameter control the period window of the moving average, larger periods return smoother results while having a low kurtosis, which mean that values will remain around 1 or -1 a longer period of time. Pre-filtering apply a Kaufman adaptive moving average to the input, which allow for a smoother output.

No pre-filtering in orange, pre-filtering in yellow, period = 100 for both oscillators.

If you are not aware of the Kaufman adaptive moving average, such moving average return more reactive results when price is trending and smoother results when price is ranging, this also apply for the proposed indicator.

Conclusion

Classical correlation coefficients could use this approach, therefore the linear relationships between any variables could be measured. The fact that the indicator is adaptive add a certain potential, however such combination make the indicator have the drawback of kama + the correlation oscillator, which might appear at certain points.

Thanks for reading !

[CS] AMA Strategy - Channel Break-Out"There are various ways to detect trends with moving averages. The moving average is a rolling filter and uptrends are detected when either the price is above the moving average or when the moving average’s slope is positive.

Given that an SMA can be well approximated by a constant-α AMA, it makes a lot of sense to adopt the AMA as the principal representative of this family of indicators. Not only it is potentially flexible in the definition of its effective lookback but it is also recursive. The ability to compute indicators recursively is a very big positive in latency-sensitive applications like high-frequency trading and market-making. From the definition of the AMA, it is easy to derive that AMA > 0 if P(i) > AMA(i-1). This means that the position of the price relative to an AMA dictates its slope and provides a way to determine whether the market is in an uptrend or a downtrend."

You can find this and other very efficient strategies from the same author here:

www.amazon.com

In the following repository you can find this system implemented in lisp:

github.com

To formalize, define the upside and downside deviations as the same sensitivity moving averages of relative price appreciations and depreciations

from one observation to another:

D+(0) = 0 D+(t) = α(t − 1)max((P(t) − P(t − 1))/P(t − 1)) , 0) + (1 − α(t − 1))D+(t − 1)

D−(0) = 0 D−(t) = −α(t − 1)min((P(t) − P(t − 1))/P(t − 1)) , 0)+ (1 − α(t − 1))D−(t − 1)

The AMA is computed by

AMA(0) = P(0) AMA(t) = α(t − 1)P(t) + (1 − α(t − 1))AMA(t − 1)

And the channels

H(t) = (1 + βH(t − 1))AMA(t) L(t) = (1 − βL(t − 1))AMA(t)

For a scale constant β, the upper and lower channels are defined to be

βH(t) = β D− βL(t) = β D+

The signal-to-noise ratio calculations are state dependent:

SNR(t) = ((P(t) − AMA(t − 1))/AMA(t − 1)) / β D−(t) IfP(t) > H(t)

SNR(t) = −((P(t) − AMA(t − 1))/AMA(t − 1)) / β D−(t) IfP(t) < L(t)

SNR(t) = 0 otherwise.

Finally the overall sensitivity α(t) is determined via the following func-

tion of SNR(t):

α(t) = αmin + (αmax − αmin) ∗ Arctan(γ SNR(t))

Note: I added a moving average to α(t) that could add some lag. You can optimize the indicator by eventually removing it from the computation.

Dynamically Adjustable Moving AverageIntroduction

The Dynamically Adjustable Moving Average (AMA) is an adaptive moving average proposed by Jacinta Chan Phooi M’ng (1) originally provided to forecast Asian Tiger's futures markets. AMA adjust to market condition in order to avoid whipsaw trades as well as entering the trending market earlier. This moving average showed better results than classical methods (SMA20, EMA20, MAC, MACD, KAMA, OptSMA) using a classical crossover/under strategy in Asian Tiger's futures from 2014 to 2015.

Dynamically Adjustable Moving Average

AMA adjust to market condition using a non-exponential method, which in itself is not common, AMA is described as follow :

1/v * sum(close,v)

where v = σ/√σ

σ is the price standard deviation.

v is defined as the Efficacy Ratio (not be confounded with the Efficiency Ratio) . As you can see v determine the moving average period, you could resume the formula in pine with sma(close,v) but in pine its not possible to use the function sma with variables for length, however you can derive sma using cumulation.

sma ≈ d/length where d = c - c_length and c = cum(close)

So a moving average can be expressed as the difference of the cumulated price by the cumulated price length period back, this difference is then divided by length. The length period of the indicator should be short since rounded version of v tend to become less variables thus providing less adaptive results.

AMA in Forex Market

In 2014/2015 Major Forex currencies where more persistent than Asian Tiger's Futures (2) , also most traded currency pairs tend to have a strong long-term positive autocorrelation so AMA could have in theory provided good results if we only focus on the long term dependency. AMA has been tested with ASEAN-5 Currencies (3) and still showed good results, however forex is still a tricky market, also there is zero proof that switching to a long term moving average during ranging market avoid whipsaw trades (if you have a paper who prove it please pm me) .

Conclusion

An interesting indicator, however the idea behind it is far from being optimal, so far most adaptive methods tend to focus more in adapting themselves to market complexity than volatility. An interesting approach would have been to determine the validity of a signal by checking the efficacy ratio at time t . Backtesting could be a good way to see if the indicator is still performing well.

References

(1) J.C.P. M’ng, Dynamically adjustable moving average (AMA’) technical

analysis indicator to forecast Asian Tigers’ futures markets, Physica A (2018),

doi.org

(2) www.researchgate.net

(3) www.ncbi.nlm.nih.gov

Bryant Adaptive Moving Average@ChartArt got my attention to this idea.

This type of moving average was originally developed by Michael R. Bryant (Adaptrade Software newsletter, April 2014). Mr. Bryant suggested a new approach, so called Variable Efficiency Ratio (VER), to obtain adaptive behaviour for the moving average. This approach is based on Perry Kaufman' idea with Efficiency Ratio (ER) which was used by Mr. Kaufman to create KAMA.

As result Mr. Bryant got a moving average with adaptive lookback period. This moving average has 3 parameters:

Initial lookback

Trend Parameter

Maximum lookback

The 2nd parameter, Trend Parameter can take any positive or negative value and determines whether the lookback length will increase or decrease with increasing ER.

Changing Trend Parameter we can obtain KAMA' behaviour

To learn more see www.adaptrade.com

Jurik Moving AverageThis indicator was originally developed by Mark Jurik.

NOTE: If Mr. Jurik ask me to remove this indicator from public access then I will do it.

Adaptive Least SquaresAn adaptive filtering technique allowing permanent re-evaluation of the filter parameters according to price volatility. The construction of this filter is based on the formula of moving ordinary least squares or lsma , the period parameter is estimated by dividing the true range with its highest. The filter will react faster during high volatility periods and slower during low volatility ones.

High smooth parameter will create smoother results, values inferior to 3 are recommended.

You can easily replace the parameter estimation method as long as the one used fluctuate in a range of , for example you can use the efficiency ratio

ER = abs(change(close,length))/sum(abs(change(close)),length)

Or the Fractal Dimension Index , in fact any values will work as long as they are rescaled (stoch(value,value,value,length)/100)

For any suggestions/questions feel free to send me a message :)

Kaufman Adaptive Moving AverageKaufman Adaptive Moving Average script.

This indicator was originally developed by Perry J. Kaufman (`Smarter Trading: Improving Performance in Changing Markets`, 1995).

Ehlers MESA Adaptive Moving Averages (MAMA & FAMA)Ehlers MESA Adaptive Moving Averages (MAMA & FAMA) script.

These indicators was originally developed by John F. Ehlers (Stocks & Commodities V. 19:10: MESA Adaptive Moving Averages).

Ehlers Deviation-Scaled Moving Average (DSMA)Ehlers Deviation-Scaled Moving Average indicator script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 36:8: The Deviation-Scaled Moving Average).

Ahrens Moving AverageAhrens Moving Average indicator script.

This indicator was originally developed by Richard D. Ahrens (Stocks & Commodities V.31:11 (26-30): Build A Better Moving Average).

Index Adaptive Keltner Channels [DW]This study is an experiment in adaptive filtering. The process in this study was inspired by KAMA and ZLEMA filtering techniques.

First, data is given an optional modification for lag reduction.

Then, an adaptive filter of your choice is calculated. There are 6 different adaptive filters to choose from in this study:

-Commodity Channel Index Adaptive Moving Average (CCIAMA)

-Relative Strength Index Adaptive Moving Average (RSIAMA)

-%R Adaptive Moving Average (%RAMA)

-Klinger Volume Oscillator Adaptive Moving Average (KVOAMA)

-Money Flow Index Adaptive Moving Average (MFIAMA)

-Correlation Coefficient Adaptive Moving Average (CCAMA)

Next, ATR is calculated using the specified adaptive filter.

A set of ranges is calculated by multiplying ATR by the square root of the sampling period, then dividing it by 2 and 4.

And Finally, the ranges are added to and subtracted from the adaptive filter to generate the channels.

Custom bar colors are included. The formula for the color scheme is based on filter direction and price.

Adaptive Laguerre FilterAdaptive Laguerre Filter indicator script.

The Adaptive Laguerre Filter was originally developed and described by John Ehlers in his paper `Time Warp – Without Space Travel`.

Thanks to @apozdnyakov for the sorting solution.

Adaptive Moving AverageAdaptive Moving Average indicator script. This indicator was originally developed by Vitali Apirine (Stocks & Commodities V.36:5: Adaptive Moving Averages).

Variable Index Dynamic Average (VIDYA)Variable Index Dynamic Average indicator script based on the original version by Tushar Chande.