OPEN-SOURCE SCRIPT

Atualizado Robust Weighting Oscillator

Introduction

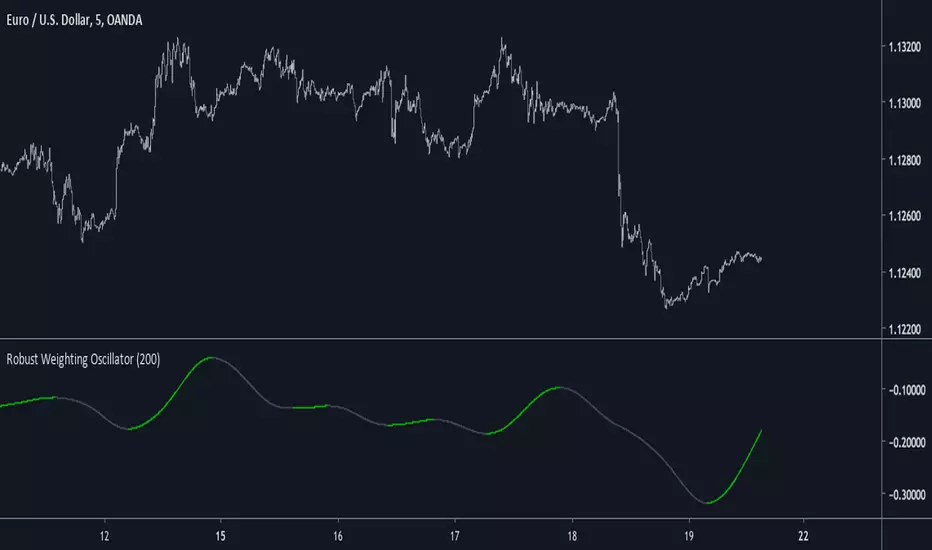

A simple oscillator using a modified lowess architecture, good in term of smoothness and reactivity.

Lowess Regression

Lowess or local regression is a non-parametric (can be used with data not fitting a normal distribution) smoothing method. This method fit a curve to the data using least squares.

In order to have a lowess regression one must use tricube kernel for the weightings w, the weightings are determined using a k-nearest-neighbor model.

lowess is then calculated like so :

Σ(wG(y-a-bx)^2)

Our indicator use G, a ,b and remove the square as well as replacing x by y

Conclusion

The oscillator is simple and nothing revolutionary but its still interesting to have new indicators.

Lowess would be a great method to be made on pinescript, i have an estimate but its not that good. Some codes use a simple line equation in order to estimate a lowess smoother, i can describe it as ax + b where a is a smooth oscillator, b some kind of filter defined by lp + bp with lp a smooth low pass filter and bp a bandpass filter, x is a variable dependent of the smoothing span.

A simple oscillator using a modified lowess architecture, good in term of smoothness and reactivity.

Lowess Regression

Lowess or local regression is a non-parametric (can be used with data not fitting a normal distribution) smoothing method. This method fit a curve to the data using least squares.

In order to have a lowess regression one must use tricube kernel for the weightings w, the weightings are determined using a k-nearest-neighbor model.

lowess is then calculated like so :

Σ(wG(y-a-bx)^2)

Our indicator use G, a ,b and remove the square as well as replacing x by y

Conclusion

The oscillator is simple and nothing revolutionary but its still interesting to have new indicators.

Lowess would be a great method to be made on pinescript, i have an estimate but its not that good. Some codes use a simple line equation in order to estimate a lowess smoother, i can describe it as ax + b where a is a smooth oscillator, b some kind of filter defined by lp + bp with lp a smooth low pass filter and bp a bandpass filter, x is a variable dependent of the smoothing span.

Notas de Lançamento

Added G in a separate calculation mode, thanks to @ aaahopper for pointing it out. Changed color for downside movements.Script de código aberto

Em verdadeiro espírito do TradingView, o criador deste script o tornou de código aberto, para que os traders possam revisar e verificar sua funcionalidade. Parabéns ao autor! Embora você possa usá-lo gratuitamente, lembre-se de que a republicação do código está sujeita às nossas Regras da Casa.

Check out the indicators we are making at luxalgo: tradingview.com/u/LuxAlgo/

"My heart is so loud that I can't hear the fireworks"

"My heart is so loud that I can't hear the fireworks"

Aviso legal

As informações e publicações não se destinam a ser, e não constituem, conselhos ou recomendações financeiras, de investimento, comerciais ou de outro tipo fornecidos ou endossados pela TradingView. Leia mais nos Termos de Uso.

Script de código aberto

Em verdadeiro espírito do TradingView, o criador deste script o tornou de código aberto, para que os traders possam revisar e verificar sua funcionalidade. Parabéns ao autor! Embora você possa usá-lo gratuitamente, lembre-se de que a republicação do código está sujeita às nossas Regras da Casa.

Check out the indicators we are making at luxalgo: tradingview.com/u/LuxAlgo/

"My heart is so loud that I can't hear the fireworks"

"My heart is so loud that I can't hear the fireworks"

Aviso legal

As informações e publicações não se destinam a ser, e não constituem, conselhos ou recomendações financeiras, de investimento, comerciais ou de outro tipo fornecidos ou endossados pela TradingView. Leia mais nos Termos de Uso.