Por que indicadores baseados em sessão ocasionalmente estendem as sessões diárias nos futuros dos EUA?

Alguns indicadores no TradingView realizam cálculos em um período específico (sessão) e são reiniciados no final de cada período. Por exemplo, os indicadores Perfil de Volume da Sessão e Session Time Price Opportunity acumulam os dados dentro de uma sessão de negociação diária (um dia de negociação, desde a abertura até o fechamento do mercado) para produzir uma análise da sessão, que é reiniciada assim que uma nova sessão diária começa. Outros indicadores, como Pontos de Pivô Padrão, Preço Médio Ponderado por Volume e Time Price Opportunity periódico, permitem que os usuários definam um período customizado de dias, semanas ou meses para que o indicador analise, partindo de uma sessão de 1 dia ou maior.

Ocasionalmente, esses indicadores podem estender as sessões diárias em gráficos intradiários para incluir várias sessões de negociação intradiária em uma “sessão diária” estendida. Por exemplo, na captura de tela abaixo, o indicador Perfil de Volume da Sessão estende uma sessão diária que começa em 19 de janeiro até 21 de janeiro, mesmo havendo uma interrupção da sessão em 20 de janeiro. Esse comportamento não é um erro do indicador, mas sim um ajuste intencional feito pela bolsa de valores que define o cronograma das sessões de negociação do instrumento.

Por que isso acontece?

Primeiro, é importante distinguir entre sessão de negociação, dia de negociação e dia do calendário. Por exemplo, para símbolos com sessões overnight, a sessão “diária” de negociação abrange dois dias do calendário e começa no dia do calendário anterior ao seu dia de negociação associado. Portanto, uma sessão diária para o símbolo "ES1!" que pertence a um dia de negociação “Segunda-feira” começa no Domingo às 17:00 CT (Horário Central) e termina na Segunda-feira às 16:00 CT.

Indicadores baseados em sessão reiniciam seus cálculos uma vez por dia de negociação, o que muitas vezes pode corresponder a uma vez por dia do calendário, dado o tempo gráfico diário. No entanto, ocasionalmente, uma bolsa pode alterar o comprimento da sessão diária de um instrumento, reduzindo-a ou estendendo-a, o que pode variar o número de dia do calendário dentro da sessão. Consequentemente, os indicadores baseados em sessão podem não reiniciar seus cálculos diariamente, apesar do progresso dos dias do calendário.

Para futuros negociados nos EUA do grupo CME (bolsas CBOT, CME, NYMEX e COMEX), as bolsas seguem os feriados federais dos EUA, encurtando as sessões de negociação nesses dias. O grupo CME lista seus horários de negociação durante feriados anuais aqui, detalhando as diferentes alterações de sessão para cada feriado e commodity. Frequentemente, as bolsas combinam as sessões encurtadas em um único dia de negociação estendido, o que resulta em uma única sessão “diária” que pode incluir negociações intradiárias de até três dia do calendário.

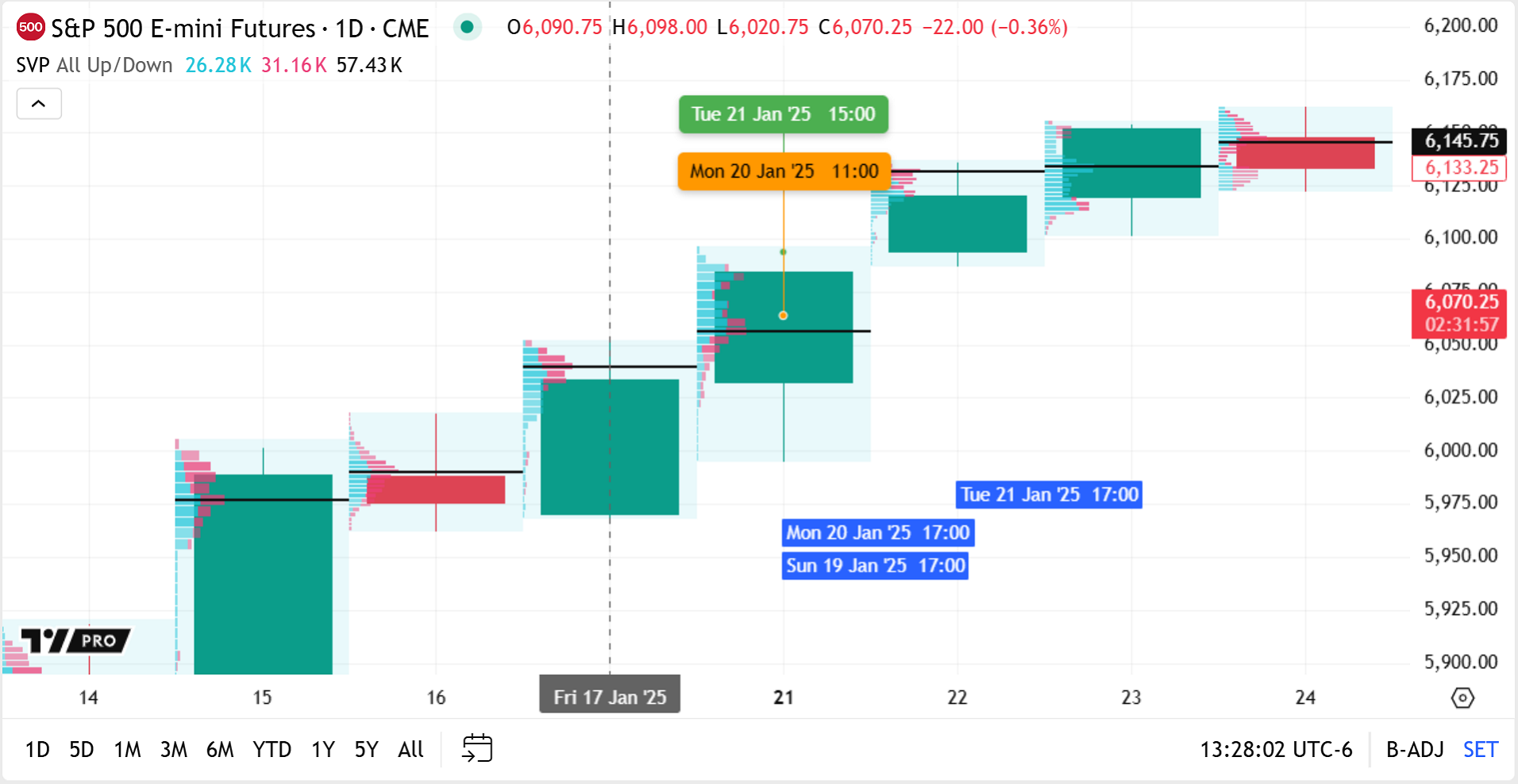

Por exemplo, o calendário de feriados do grupo CME mostra que a bolsa observa o Dia de Martin Luther King Jr. com horários de negociação encurtados na segunda-feira, 20 de janeiro de 2025. Para futuros de ações, a bolsa anunciou que as negociações intradiárias do domingo, 19 de janeiro, às 17:00 CT, até Terça-feira, 21 de janeiro, às 16:00 CT, pertencerão a uma sessão de negociação estendida para Terça-feira:

Nós podemos ver a sessão de feriado modificada ao adicionarmos o indicador Perfil de Volume da Sessão no gráfico intradiário do símbolo "ES1!". A sessão de negociação de Segunda-feira (normalmente de Domingo 17:00–Segunda 16:00 CT) agora é encurtada para o feriado, terminando às 11:00 CT, e é combinada com a sessão de negociação de Terça-feira (Segunda 17:00–Terça 16:00 CT) como uma única sessão “diária” estendida. Embora o indicador pareça, à primeira vista, não reiniciar a sessão aqui, ele, de fato, representa corretamente as datas de sessão de negociação definidas pela bolsa:

Nós também podemos verificar que as sessões definidas pelo indicador coincidem com os dados diários provenientes da bolsa ao observamos o gráfico diário do símbolo. A barra diária de Sexta-feira, 17 de Janeiro (a sessão anterior ao Domingo) é seguida imediatamente pela barra diária de Terça-feira, 21 de janeiro, que cobre toda a atividade intradiária de preços do Domingo até Terça-feira (veja que nossos rótulos intradiários aparecem todos nesta vela):

Levando em conta a distinção entre dias de negociação e dias do calendário, fica mais fácil perceber que, quando um indicador baseado em sessão combina vários dias do calendário em uma única sessão diária de negociação, por exemplo, em um feriado dos EUA, isso não se trata de um erro no indicador. Pelo contrário, é um ajuste intencional da bolsa que atribui as datas de negociação para seus dados “diários”. Nossos indicadores baseados em sessão simplesmente fornecem os dados da sessão diária conforme fornecidos pelas bolsas.

Uma observação adicional é que uma sessão de negociação encurtada geralmente possui um volume de negociação significativamente menor do que uma sessão diária típica, então usar a sessão incompleta como uma “sessão diária” separada distorceria de forma imprecisa as tendências de volume diárias interpretadas. Em vez disso, ter uma sessão estendida mantém o volume da sessão dentro de uma faixa diária típica.

Se os usuários tiverem acesso ao código-fonte de um indicador baseado em sessão, eles podem usar um tempo gráfico de "1440" no script para expressar uma sessão fixa de 24 horas (1440 minutos) em vez de usar uma sessão "diária" de 1D. O tempo gráfico "1440" constrói suas sessões com base nos dados intradiários do instrumento, em vez de depender das sessões diárias definidas pela bolsa. Portanto, ele divide os dados em intervalos fixos, independentemente das alterações de sessão da bolsa, reiniciando a cada dia do calendário.