MACD + RSI + EMA + BB + ATR Day Trading StrategyEntry Conditions and Signals

The strategy implements a multi-layered filtering approach to entry conditions, requiring alignment across technical indicators, timeframes, and market conditions .

Long Entry Requirements

Trend Filter: Fast EMA (9) must be above Slow EMA (21), price must be above Fast EMA, and higher timeframe must confirm uptrend

MACD Signal: MACD line crosses above signal line, indicating increasing bullish momentum

RSI Condition: RSI below 70 (not overbought) but above 40 (showing momentum)

Volume & Volatility: Current volume exceeds 1.2x 20-period average and ATR shows sufficient market movement

Time Filter: Trading occurs during optimal hours (9:30-11:30 AM ET) when market volatility is typically highest

Exit Strategies

The strategy employs multiple exit mechanisms to adapt to changing market conditions and protect profits :

Stop Loss Management

Initial Stop: Placed at 2.0x ATR from entry price, adapting to current market volatility

Trailing Stop: 1.5x ATR trailing stop that moves up (for longs) or down (for shorts) as price moves favorably

Time-Based Exits: All positions closed by end of trading day (4:00 PM ET) to avoid overnight risk

Best Practices for Implementation

Settings

Chart Setup: 5-minute timeframe for execution with 15-minute chart for trend confirmation

Session Times: Focus on 9:30-11:30 AM ET trading for highest volatility and opportunity

Pesquisar nos scripts por "momentum"

Trend Surge with Pullback FilterTrend Surge with Pullback Filter

Overview

Trend Surge with Pullback Filter is a price action-based strategy designed to enter strong trends not at the breakout, but at the first controlled pullback after a surge. It filters out noise by requiring momentum confirmation and low volatility conditions, aiming for better entry prices and reduced risk exposure.

How It Works

A strong upward trend is identified when the Rate of Change (ROC) exceeds a defined percentage (e.g., 2%).

Instead of jumping into the trend immediately, the strategy waits for a pullback: the price must drop at least 1% below its recent high (over the past 3 candles).

A low volatility environment is also required for entry — measured using ATR being below its 20-period average multiplied by a safety factor.

If all three conditions are met (trend + pullback + quiet volatility), the system enters a long position.

The trade is managed using a dynamic ATR-based stop-loss and a take-profit at 2x ATR.

An automatic exit occurs after 30 bars if neither SL nor TP is hit.

Key Features

- Momentum-triggered trend detection via ROC

- Smart pullback filter avoids overbought entries

- Volatility-based filter to eliminate noise and choppy conditions

- Dynamic risk-reward ratio with ATR-driven exit logic

- Time-limited exposure using bar-based exit

Parameter Explanation

ROC Length (10): Looks for short-term price surges

ROC Threshold (2.0%): Trend is considered valid if price increased more than 2%

Pullback Lookback (3): Checks last 3 candles for price retracement

Minimum Pullback % (1.0%): Entry only if price pulled back at least 1%

ATR Length (14): Measures current volatility

Low Volatility Multiplier (1.2): ATR must be below this multiple of its 20-period average

Risk-Reward (2.0): Target is set at 2x the stop-loss distance

Max Bars (30): Trade is closed automatically after 30 bars

Originality Statement

This strategy doesn’t enter at the trend start, unlike many momentum bots. Instead, it waits for the first market hesitation — a minor pullback under low volatility — before entering. This logic mimics how real traders often wait for a better entry after a breakout, avoiding emotional overbought buys. The combined use of ROC, dynamic pullback detection, and ATR-based environment filters makes it both practical and original for real-world trading.

Disclaimer

This strategy is intended for educational and research purposes. Backtest thoroughly and understand the logic before using with real capital.

SOXL Trend Surge v3.0.2 – Profit-Only RunnerSOXL Trend Surge v3.0.2 – Profit-Only Runner

This is a trend-following strategy built for leveraged ETFs like SOXL, designed to ride high-momentum waves with minimal interference. Unlike most short-term scalping scripts, this model allows trades to develop over multiple days to even several months, capitalizing on the full power of extended directional moves — all without using a stop-loss.

🔍 How It Works

Entry Logic:

Price is above the 200 EMA (long-term trend confirmation)

Supertrend is bullish (momentum confirmation)

ATR is rising (volatility expansion)

Volume is above its 20-bar average (liquidity filter)

Price is outside a small buffer zone from the 200 EMA (to avoid whipsaws)

Trades are restricted to market hours only (9 AM to 2 PM EST)

Cooldown of 15 bars after each exit to prevent overtrading

Exit Strategy:

Takes partial profit at +2× ATR if held for at least 2 bars

Rides the remaining position with a trailing stop at 1.5× ATR

No hard stop-loss — giving space for volatile pullbacks

⚙️ Strategy Settings

Initial Capital: $500

Risk per Trade: 100% of equity (fully allocated per entry)

Commission: 0.1%

Slippage: 1 tick

Recalculate after order is filled

Fill orders on bar close

Timeframe Optimized For: 45-minute chart

These parameters simulate an aggressive, high-volatility trading model meant for forward-testing compounding potential under realistic trading costs.

✅ What Makes This Unique

No stop-loss = fewer premature exits

Partial profit-taking helps lock in early wins

Trailing logic gives room to ride large multi-week moves

Uses strict filters (volume, ATR, EMA bias) to enter only during high-probability windows

Ideal for leveraged ETF swing or position traders looking to hold longer than the typical intraday or 2–3 day strategies

⚠️ Important Note

This is a high-risk, high-reward strategy meant for educational and testing purposes. Without a stop-loss, trades can experience deep drawdowns that may take weeks or even months to recover. Always test thoroughly and adjust position sizing to suit your risk tolerance. Past results do not guarantee future returns. Backtest range: May 8, 2020 – May 23, 2025

SpeedBullish Strategy Confirm V6.2SpeedBullish Strategy Confirm V6.2

SpeedBullish V6.2 is an advanced price-action + indicator-based strategy designed to confirm trend strength and signal entries with high precision. This version builds on the W/M pattern structure and adds dynamic filtering with EMA, MACD Histogram, RSI, ATR, and Volume.

✅ Signal Conditions

🔹 Buy Signal:

Price above EMA10 or EMA15

MACD Histogram crosses above 0

RSI > 50

(Optional) Higher low via Pivot Low

(Optional) ATR > ATR SMA * Multiplier

(Optional) Volume > SMA * Multiplier

🔻 Sell Signal:

Price below EMA10 or EMA15

MACD Histogram crosses below 0

RSI < 50

(Optional) Lower high via Pivot High

(Optional) Confirmed high volatility and volume

⚙️ Strategy Features

MACD Histogram for momentum shift detection

RSI filtering for momentum confirmation

EMA10/15 for trend direction

ATR-based volatility filter

Volume confirmation filter

Dynamic TP/SL + Trailing Stop

Webhook Integration for MT5 auto-trade

Visual signal markers + background highlight

🔔 Alerts

Alerts are sent in JSON format via alert() with the current symbol, action (buy/sell), and price. Webhook endpoint and secret key are configurable.

📈 How to Use

Attach the strategy to any symbol and timeframe

Customize filters and confirmations to fit your market conditions

Enable webhook alerts for integration with your MT5 Expert Advisor or trading bot

Backtest and optimize before live deployment

Big Mover Catcher BTC 4h🧠 Big Mover Catcher (BTC 4H Strategy) — Educational Tool

⚠️ Disclaimer: I am not a financial advisor. This script is for educational and testing purposes only. Cryptocurrency trading is highly volatile and involves significant risk. You can lose all of your invested capital.

📌 Overview

The Big Mover Catcher strategy is a work-in-progress trading system designed for Bitcoin (BTC) on the 4-hour chart. It aims to identify strong breakout moves by combining multiple technical indicators and conditions, allowing for high customization and filter-based confirmations.

This script is part of a personal project to learn Pine Script and backtesting on TradingView. It is currently in the testing and research phase.

🎯 Strategy Objective

Catch large, high-momentum breakout moves in the BTC market using:

Bollinger Band breakouts for entry signals

Momentum, volatility, and trend filters for trade confirmation

🧰 Features & Filters

The script provides a flexible set of filters that can be turned ON/OFF and adjusted directly from the settings panel:

✅ Entry Conditions

Price must break above or below Bollinger Bands

All selected filters must align before entry

🧪 Available Filters:

Relative Strength Index (RSI) with EMA/SMA smoothing

Average Directional Index (ADX) with EMA/SMA smoothing

Average True Range (ATR) with EMA/SMA smoothing

MACD Signal above or below zero

EMA 350 trend filter

ATR / ADX / RSI Threshold toggles for added control

🔥 Additional Feature:

Force Take Profit: Optionally closes the trade immediately if a candle closes with more than a defined % movement (default: 5%). This can help lock in quick profits during high volatility moves.

⚙️ Customizable Inputs

You can configure:

Stop loss percentage

All indicator lengths

Smoothing types (EMA/SMA)

Threshold activation toggles

Individual filter ON/OFF switches

This makes the strategy highly adaptable for educational exploration and optimization.

📊 Best Used For

Learning Pine Script and strategy structure

Testing filter combinations for BTC on the 4H timeframe

Understanding how different indicators interact in live markets

⚠️ Note: ❌ Short trades are currently disabled by default, as short-side logic is still under development.

❗ Final Reminder

This script is not financial advice. It is an educational tool. Use it to learn and explore trading logic. Trading cryptocurrencies carries high risk — only invest what you can afford to lose.

Gold Breakout Strategy - RR 4Strategy Name: Gold Breakout Strategy - RR 4

🧠 Main Objective

This strategy aims to capitalize on breakouts from the Donchian Channel on Gold (XAU/USD) by filtering trades with:

Volume confirmation,

A custom momentum indicator (LWTI - Linear Weighted Trend Index),

And a specific trading session (8 PM to 8 AM Quebec time — GMT-5).

It takes only one trade per day, either a buy or a sell, using a fixed stop-loss at the wick of the breakout candle and a 4:1 reward-to-risk (RR) ratio.

📊 Indicators Used

Donchian Channel

Length: 96

Detects breakouts of recent highs or lows.

Volume

Simple Moving Average (SMA) over 30 bars.

A breakout is only valid if the current volume is above the SMA.

LWTI (Linear Weighted Trend Index)

Measures momentum using price differences over 25 bars, smoothed over 5.

Used to confirm trend direction:

Buy when LWTI > its smoothed version (uptrend).

Sell when LWTI < its smoothed version (downtrend).

⏰ Time Filter

The strategy only allows entries between 8 PM and 8 AM (GMT-5 / Quebec time).

A timestamp-based filter ensures the system recognizes the correct trading session even across midnight.

📌 Entry Conditions

🟢 Buy (Long)

Price breaks above the previous Donchian Channel high.

The current channel high is higher than the previous one.

Volume is above its moving average.

LWTI confirms an uptrend.

The time is within the trading session (20:00 to 08:00).

No trade has been taken yet today.

🔴 Sell (Short)

Price breaks below the previous Donchian Channel low.

The current channel low is lower than the previous one.

Volume is above its moving average.

LWTI confirms a downtrend.

The time is within the trading session.

No trade has been taken yet today.

💸 Trade Management

Stop-Loss (SL):

For long entries: placed below the wick low of the breakout candle.

For short entries: placed above the wick high of the breakout candle.

Take-Profit (TP):

Set at a fixed 4:1 reward-to-risk ratio.

Calculated as 4x the distance between the entry price and stop-loss.

No trailing stop, no break-even, no scaling in/out.

🎨 Visuals

Green triangle appears below the candle on a buy signal.

Red triangle appears above the candle on a sell signal.

Donchian Channel lines are plotted on the chart.

The strategy is designed for the 5-minute timeframe.

🔄 One Trade Per Day Rule

Once a trade is taken (buy or sell), no more trades will be executed for the rest of the day. This prevents overtrading and limits exposure.

Intraday Trading Hit and Run# Strategy Overview

This is a short-term trading system designed for quick entries/exits (intraday). It uses multiple technical indicators to identify momentum trades in the direction of the trend, with built-in risk management through trailing stops.

# Main Components

1. Trend Filter

Uses two EMAs (10-period "fast" blue line and 100-period "slow" red line)

Only trades when:

Long: Price AND fast EMA are above slow EMA

Short: Price AND fast EMA are below slow EMA

2. Main Signal

////Stochastic Oscillator (14-period):

Buy when %K line crosses above %D line

Sell when %K crosses below %D

////Trend Strength Check

Smoothed ADX indicator (5-period EMA of ADX):

Requires ADX value ≥ 25 to confirm strong trend

3. Confirmation using Volume Filter (Optional)

Checks if current volume is 1.5× greater than 20-period average volume

# Entry Rules

A trade is only taken when:

All 3 indicators agree (EMA trend, Stochastic momentum, ADX strength)

Volume filter is satisfied (if enabled)

# Exit Rules

1. Emergency Exit:

Close long if price drops below fast EMA

Close short if price rises above fast EMA

2. Trailing Stop:

Actively protects profits by moving stop-loss:

Maintains 0.1% distance from highest price (longs) or lowest price (shorts)

# Risk Management

Only use 10% of account per trade

Includes 0.04% commission cost in calculations

All trades monitored with trailing stops

# How It Operates

The strategy looks for strong, high-volume momentum moves in the direction of the established trend (as determined by EMAs). It jumps in quickly ("hit") when conditions align, then protects gains with an automatic trailing stop ("run"). Designed for fast markets where trends develop rapidly.

You can use it on 15m, 1h or 4h

EMA 10/20/50 Alignment Strategy### 📘 **Strategy Name**

**EMA 10/20/50 Trend Alignment Strategy**

---

### 📝 **Description (for Publishing)**

This strategy uses the alignment of Exponential Moving Averages (EMAs) to identify strong bullish trends. It enters a long position when the short-term EMA is above the mid-term EMA, which is above the long-term EMA — a classic sign of trend strength.

#### 🔹 Entry Criteria:

* **EMA10 > EMA20 > EMA50**: A bullish alignment that signals momentum in an upward direction.

* The strategy enters a **long position** when this alignment occurs.

#### 🔹 Exit Criteria:

* The long position is closed when the EMA alignment breaks (i.e., the trend weakens or reverses).

#### 🔹 Additional Features:

* Includes a **date range filter**, allowing you to backtest the strategy over a specific period.

* Uses **100% of available capital** for each trade (position size auto-scales with account balance).

* No short positions, stop loss, or take profit are applied — this is a trend-following strategy meant to ride bullish moves.

---

### ✅ Best For:

* Traders looking for a **simple, trend-based entry system**

* Testing price momentum strategies during specific market regimes

* Visualizing EMA stacking patterns in historical data

Bober XM v2.0# ₿ober XM v2.0 Trading Bot Documentation

**Developer's Note**: While our previous Bot 1.3.1 was removed due to guideline violations, this setback only fueled our determination to create something even better. Rising from this challenge, Bober XM 2.0 emerges not just as an update, but as a complete reimagining with multi-timeframe analysis, enhanced filters, and superior adaptability. This adversity pushed us to innovate further and deliver a strategy that's smarter, more agile, and more powerful than ever before. Challenges create opportunity - welcome to Cryptobeat's finest work yet.

## !!!!You need to tune it for your own pair and timeframe and retune it periodicaly!!!!!

## Overview

The ₿ober XM v2.0 is an advanced dual-channel trading bot with multi-timeframe analysis capabilities. It integrates multiple technical indicators, customizable risk management, and advanced order execution via webhook for automated trading. The bot's distinctive feature is its separate channel systems for long and short positions, allowing for asymmetric trade strategies that adapt to different market conditions across multiple timeframes.

### Key Features

- **Multi-Timeframe Analysis**: Analyze price data across multiple timeframes simultaneously

- **Dual Channel System**: Separate parameter sets for long and short positions

- **Advanced Entry Filters**: RSI, Volatility, Volume, Bollinger Bands, and KEMAD filters

- **Machine Learning Moving Average**: Adaptive prediction-based channels

- **Multiple Entry Strategies**: Breakout, Pullback, and Mean Reversion modes

- **Risk Management**: Customizable stop-loss, take-profit, and trailing stop settings

- **Webhook Integration**: Compatible with external trading bots and platforms

### Strategy Components

| Component | Description |

|---------|-------------|

| **Dual Channel Trading** | Uses either Keltner Channels or Machine Learning Moving Average (MLMA) with separate settings for long and short positions |

| **MLMA Implementation** | Machine learning algorithm that predicts future price movements and creates adaptive bands |

| **Pivot Point SuperTrend** | Trend identification and confirmation system based on pivot points |

| **Three Entry Strategies** | Choose between Breakout, Pullback, or Mean Reversion approaches |

| **Advanced Filter System** | Multiple customizable filters with multi-timeframe support to avoid false signals |

| **Custom Exit Logic** | Exits based on OBV crossover of its moving average combined with pivot trend changes |

### Note for Novice Users

This is a fully featured real trading bot and can be tweaked for any ticker — SOL is just an example. It follows this structure:

1. **Indicator** – gives the initial signal

2. **Entry strategy** – decides when to open a trade

3. **Exit strategy** – defines when to close it

4. **Trend confirmation** – ensures the trade follows the market direction

5. **Filters** – cuts out noise and avoids weak setups

6. **Risk management** – controls losses and protects your capital

To tune it for a different pair, you'll need to start from scratch:

1. Select the timeframe (candle size)

2. Turn off all filters and trend entry/exit confirmations

3. Choose a channel type, channel source and entry strategy

4. Adjust risk parameters

5. Tune long and short settings for the channel

6. Fine-tune the Pivot Point Supertrend and Main Exit condition OBV

This will generate a lot of signals and activity on the chart. Your next task is to find the right combination of filters and settings to reduce noise and tune it for profitability.

### Default Strategy values

Default values are tuned for: Symbol BITGET:SOLUSDT.P 5min candle

Filters are off by default: Try to play with it to understand how it works

## Configuration Guide

### General Settings

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Long Positions** | Enable or disable long trades | Enabled |

| **Short Positions** | Enable or disable short trades | Enabled |

| **Risk/Reward Area** | Visual display of stop-loss and take-profit zones | Enabled |

| **Long Entry Source** | Price data used for long entry signals | hl2 (High+Low/2) |

| **Short Entry Source** | Price data used for short entry signals | hl2 (High+Low/2) |

The bot allows you to trade long positions, short positions, or both simultaneously. Each direction has its own set of parameters, allowing for fine-tuned strategies that recognize the asymmetric nature of market movements.

### Multi-Timeframe Settings

1. **Enable Multi-Timeframe Analysis**: Toggle 'Enable Multi-Timeframe Analysis' in the Multi-Timeframe Settings section

2. **Configure Timeframes**: Set appropriate higher timeframes based on your trading style:

- Timeframe 1: Default is now 15 minutes (intraday confirmation)

- Timeframe 2: Default is 4 hours (trend direction)

3. **Select Sources per Indicator**: For each indicator (RSI, KEMAD, Volume, etc.), choose:

- The desired timeframe (current, mtf1, or mtf2)

- The appropriate price type (open, high, low, close, hl2, hlc3, ohlc4)

### Entry Strategies

- **Breakout**: Enter when price breaks above/below the channel

- **Pullback**: Enter when price pulls back to the channel

- **Mean Reversion**: Enter when price is extended from the channel

You can enable different strategies for long and short positions.

### Core Components

### Risk Management

- **Position Size**: Control risk with percentage-based position sizing

- **Stop Loss Options**:

- Fixed: Set a specific price or percentage from entry

- ATR-based: Dynamic stop-loss based on market volatility

- Swing: Uses recent swing high/low points

- **Take Profit**: Multiple targets with percentage allocation

- **Trailing Stop**: Dynamic stop that follows price movement

## Advanced Usage Strategies

### Moving Average Type Selection Guide

- **SMA**: More stable in choppy markets, good for higher timeframes

- **EMA/WMA**: More responsive to recent price changes, better for entry signals

- **VWMA**: Adds volume weighting for stronger trends, use with Volume filter

- **HMA**: Balance between responsiveness and noise reduction, good for volatile markets

### Multi-Timeframe Strategy Approaches

- **Trend Confirmation**: Use higher timeframe RSI (mtf2) for overall trend, current timeframe for entries

- **Entry Precision**: Use KEMAD on current timeframe with volume filter on mtf1

- **False Signal Reduction**: Apply RSI filter on mtf1 with strict KEMAD settings

### Market Condition Optimization

| Market Condition | Recommended Settings |

|------------------|----------------------|

| **Trending** | Use Breakout strategy with KEMAD filter on higher timeframe |

| **Ranging** | Use Mean Reversion with strict RSI filter (mtf1) |

| **Volatile** | Increase ATR multipliers, use HMA for moving averages |

| **Low Volatility** | Decrease noise parameters, use pullback strategy |

## Webhook Integration

The strategy features a professional webhook system that allows direct connectivity to your exchange or trading platform of choice through third-party services like 3commas, Alertatron, or Autoview.

The webhook payload includes all necessary parameters for automated execution:

- Entry price and direction

- Stop loss and take profit levels

- Position size

- Custom identifier for webhook routing

## Performance Optimization Tips

1. **Start with Defaults**: Begin with the default settings for your timeframe before customizing

2. **Adjust One Component at a Time**: Make incremental changes and test the impact

3. **Match MA Types to Market Conditions**: Use appropriate moving average types based on the Market Condition Optimization table

4. **Timeframe Synergy**: Create logical relationships between timeframes (e.g., 5min chart with 15min and 4h higher timeframes)

5. **Periodic Retuning**: Markets evolve - regularly review and adjust parameters

## Common Setups

### Crypto Trend-Following

- MLMA with EMA or HMA

- Higher RSI thresholds (75/25)

- KEMAD filter on mtf1

- Breakout entry strategy

### Stock Swing Trading

- MLMA with SMA for stability

- Volume filter with higher threshold

- KEMAD with increased filter order

- Pullback entry strategy

### Forex Scalping

- MLMA with WMA and lower noise parameter

- RSI filter on current timeframe

- Use highest timeframe for trend direction only

- Mean Reversion strategy

## Webhook Configuration

- **Benefits**:

- Automated trade execution without manual intervention

- Immediate response to market conditions

- Consistent execution of your strategy

- **Implementation Notes**:

- Requires proper webhook configuration on your exchange or platform

- Test thoroughly with small position sizes before full deployment

- Consider latency between signal generation and execution

### Backtesting Period

Define a specific historical period to evaluate the bot's performance:

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Start Date** | Beginning of backtest period | January 1, 2025 |

| **End Date** | End of backtest period | December 31, 2026 |

- **Best Practice**: Test across different market conditions (bull markets, bear markets, sideways markets)

- **Limitation**: Past performance doesn't guarantee future results

## Entry and Exit Strategies

### Dual-Channel System

A key innovation of the Bober XM is its dual-channel approach:

- **Independent Parameters**: Each trade direction has its own channel settings

- **Asymmetric Trading**: Recognizes that markets often behave differently in uptrends versus downtrends

- **Optimized Performance**: Fine-tune settings for both bullish and bearish conditions

This approach allows the bot to adapt to the natural asymmetry of markets, where uptrends often develop gradually while downtrends can be sharp and sudden.

### Channel Types

#### 1. Keltner Channels

Traditional volatility-based channels using EMA and ATR:

| Setting | Long Default | Short Default |

|---------|--------------|---------------|

| **EMA Length** | 37 | 20 |

| **ATR Length** | 13 | 17 |

| **Multiplier** | 1.4 | 1.9 |

| **Source** | low | high |

- **Strengths**:

- Reliable in trending markets

- Less prone to whipsaws than Bollinger Bands

- Clear visual representation of volatility

- **Weaknesses**:

- Can lag during rapid market changes

- Less effective in choppy, non-trending markets

#### 2. Machine Learning Moving Average (MLMA)

Advanced predictive model using kernel regression (RBF kernel):

| Setting | Description | Options |

|---------|-------------|--------|

| **Source MA** | Price data used for MA calculations | Any price source (low/high/close/etc.) |

| **Moving Average Type** | Type of MA algorithm for calculations | SMA, EMA, WMA, VWMA, RMA, HMA |

| **Trend Source** | Price data used for trend determination | Any price source (close default) |

| **Window Size** | Historical window for MLMA calculations | 5+ (default: 16) |

| **Forecast Length** | Number of bars to forecast ahead | 1+ (default: 3) |

| **Noise Parameter** | Controls smoothness of prediction | 0.01+ (default: ~0.43) |

| **Band Multiplier** | Multiplier for channel width | 0.1+ (default: 0.5-0.6) |

- **Strengths**:

- Predictive rather than reactive

- Adapts quickly to changing market conditions

- Better at identifying trend reversals early

- **Weaknesses**:

- More computationally intensive

- Requires careful parameter tuning

- Can be sensitive to input data quality

### Entry Strategies

| Strategy | Description | Ideal Market Conditions |

|----------|-------------|-------------------------|

| **Breakout** | Enters when price breaks through channel bands, indicating strong momentum | High volatility, emerging trends |

| **Pullback** | Enters when price retraces to the middle band after testing extremes | Established trends with regular pullbacks |

| **Mean Reversion** | Enters at channel extremes, betting on a return to the mean | Range-bound or oscillating markets |

#### Breakout Strategy (Default)

- **Implementation**: Enters long when price crosses above the upper band, short when price crosses below the lower band

- **Strengths**: Captures strong momentum moves, performs well in trending markets

- **Weaknesses**: Can lead to late entries, higher risk of false breakouts

- **Optimization Tips**:

- Increase channel multiplier for fewer but more reliable signals

- Combine with volume confirmation for better accuracy

#### Pullback Strategy

- **Implementation**: Enters long when price pulls back to middle band during uptrend, short during downtrend pullbacks

- **Strengths**: Better entry prices, lower risk, higher probability setups

- **Weaknesses**: Misses some strong moves, requires clear trend identification

- **Optimization Tips**:

- Use with trend filters to confirm overall direction

- Adjust middle band calculation for market volatility

#### Mean Reversion Strategy

- **Implementation**: Enters long at lower band, short at upper band, expecting price to revert to the mean

- **Strengths**: Excellent entry prices, works well in ranging markets

- **Weaknesses**: Dangerous in strong trends, can lead to fighting the trend

- **Optimization Tips**:

- Implement strong trend filters to avoid counter-trend trades

- Use smaller position sizes due to higher risk nature

### Confirmation Indicators

#### Pivot Point SuperTrend

Combines pivot points with ATR-based SuperTrend for trend confirmation:

| Setting | Default Value |

|---------|---------------|

| **Pivot Period** | 25 |

| **ATR Factor** | 2.2 |

| **ATR Period** | 41 |

- **Function**: Identifies significant market turning points and confirms trend direction

- **Implementation**: Requires price to respect the SuperTrend line for trade confirmation

#### Weighted Moving Average (WMA)

Provides additional confirmation layer for entries:

| Setting | Default Value |

|---------|---------------|

| **Period** | 15 |

| **Source** | ohlc4 (average of Open, High, Low, Close) |

- **Function**: Confirms trend direction and filters out low-quality signals

- **Implementation**: Price must be above WMA for longs, below for shorts

### Exit Strategies

#### On-Balance Volume (OBV) Based Exits

Uses volume flow to identify potential reversals:

| Setting | Default Value |

|---------|---------------|

| **Source** | ohlc4 |

| **MA Type** | HMA (Options: SMA, EMA, WMA, RMA, VWMA, HMA) |

| **Period** | 22 |

- **Function**: Identifies divergences between price and volume to exit before reversals

- **Implementation**: Exits when OBV crosses its moving average in the opposite direction

- **Customizable MA Type**: Different MA types provide varying sensitivity to OBV changes:

- **SMA**: Traditional simple average, equal weight to all periods

- **EMA**: More weight to recent data, responds faster to price changes

- **WMA**: Weighted by recency, smoother than EMA

- **RMA**: Similar to EMA but smoother, reduces noise

- **VWMA**: Factors in volume, helpful for OBV confirmation

- **HMA**: Reduces lag while maintaining smoothness (default)

#### ADX Exit Confirmation

Uses Average Directional Index to confirm trend exhaustion:

| Setting | Default Value |

|---------|---------------|

| **ADX Threshold** | 35 |

| **ADX Smoothing** | 60 |

| **DI Length** | 60 |

- **Function**: Confirms trend weakness before exiting positions

- **Implementation**: Requires ADX to drop below threshold or DI lines to cross

## Filter System

### RSI Filter

- **Function**: Controls entries based on momentum conditions

- **Parameters**:

- Period: 15 (default)

- Overbought level: 71

- Oversold level: 23

- Multi-timeframe support: Current, MTF1 (15min), or MTF2 (4h)

- Customizable price source (open, high, low, close, hl2, hlc3, ohlc4)

- **Implementation**: Blocks long entries when RSI > overbought, short entries when RSI < oversold

### Volatility Filter

- **Function**: Prevents trading during excessive market volatility

- **Parameters**:

- Measure: ATR (Average True Range)

- Period: Customizable (default varies by timeframe)

- Threshold: Adjustable multiplier

- Multi-timeframe support

- Customizable price source

- **Implementation**: Blocks trades when current volatility exceeds threshold × average volatility

### Volume Filter

- **Function**: Ensures adequate market liquidity for trades

- **Parameters**:

- Threshold: 0.4× average (default)

- Measurement period: 5 (default)

- Moving average type: Customizable (HMA default)

- Multi-timeframe support

- Customizable price source

- **Implementation**: Requires current volume to exceed threshold × average volume

### Bollinger Bands Filter

- **Function**: Controls entries based on price relative to statistical boundaries

- **Parameters**:

- Period: Customizable

- Standard deviation multiplier: Adjustable

- Moving average type: Customizable

- Multi-timeframe support

- Customizable price source

- **Implementation**: Can require price to be within bands or breaking out of bands depending on strategy

### KEMAD Filter (Kalman EMA Distance)

- **Function**: Advanced trend confirmation using Kalman filter algorithm

- **Parameters**:

- Process Noise: 0.35 (controls smoothness)

- Measurement Noise: 24 (controls reactivity)

- Filter Order: 6 (higher = more smoothing)

- ATR Length: 8 (for bandwidth calculation)

- Upper Multiplier: 2.0 (for long signals)

- Lower Multiplier: 2.7 (for short signals)

- Multi-timeframe support

- Customizable visual indicators

- **Implementation**: Generates signals based on price position relative to Kalman-filtered EMA bands

## Risk Management System

### Position Sizing

Automatically calculates position size based on account equity and risk parameters:

| Setting | Default Value |

|---------|---------------|

| **Risk % of Equity** | 50% |

- **Implementation**:

- Position size = (Account equity × Risk %) ÷ (Entry price × Stop loss distance)

- Adjusts automatically based on volatility and stop placement

- **Best Practices**:

- Start with lower risk percentages (1-2%) until strategy is proven

- Consider reducing risk during high volatility periods

### Stop-Loss Methods

Multiple stop-loss calculation methods with separate configurations for long and short positions:

| Method | Description | Configuration |

|--------|-------------|---------------|

| **ATR-Based** | Dynamic stops based on volatility | ATR Period: 14, Multiplier: 2.0 |

| **Percentage** | Fixed percentage from entry | Long: 1.5%, Short: 1.5% |

| **PIP-Based** | Fixed currency unit distance | 10.0 pips |

- **Implementation Notes**:

- ATR-based stops adapt to changing market volatility

- Percentage stops maintain consistent risk exposure

- PIP-based stops provide precise control in stable markets

### Trailing Stops

Locks in profits by adjusting stop-loss levels as price moves favorably:

| Setting | Default Value |

|---------|---------------|

| **Stop-Loss %** | 1.5% |

| **Activation Threshold** | 2.1% |

| **Trailing Distance** | 1.4% |

- **Implementation**:

- Initial stop remains fixed until profit reaches activation threshold

- Once activated, stop follows price at specified distance

- Locks in profit while allowing room for normal price fluctuations

### Risk-Reward Parameters

Defines the relationship between risk and potential reward:

| Setting | Default Value |

|---------|---------------|

| **Risk-Reward Ratio** | 1.4 |

| **Take Profit %** | 2.4% |

| **Stop-Loss %** | 1.5% |

- **Implementation**:

- Take profit distance = Stop loss distance × Risk-reward ratio

- Higher ratios require fewer winning trades for profitability

- Lower ratios increase win rate but reduce average profit

### Filter Combinations

The strategy allows for simultaneous application of multiple filters:

- **Recommended Combinations**:

- Trending markets: RSI + KEMAD filters

- Ranging markets: Bollinger Bands + Volatility filters

- All markets: Volume filter as minimum requirement

- **Performance Impact**:

- Each additional filter reduces the number of trades

- Quality of remaining trades typically improves

- Optimal combination depends on market conditions and timeframe

### Multi-Timeframe Filter Applications

| Filter Type | Current Timeframe | MTF1 (15min) | MTF2 (4h) |

|-------------|-------------------|-------------|------------|

| RSI | Quick entries/exits | Intraday trend | Overall trend |

| Volume | Immediate liquidity | Sustained support | Market participation |

| Volatility | Entry timing | Short-term risk | Regime changes |

| KEMAD | Precise signals | Trend confirmation | Major reversals |

## Visual Indicators and Chart Analysis

The bot provides comprehensive visual feedback on the chart:

- **Channel Bands**: Keltner or MLMA bands showing potential support/resistance

- **Pivot SuperTrend**: Colored line showing trend direction and potential reversal points

- **Entry/Exit Markers**: Annotations showing actual trade entries and exits

- **Risk/Reward Zones**: Visual representation of stop-loss and take-profit levels

These visual elements allow for:

- Real-time strategy assessment

- Post-trade analysis and optimization

- Educational understanding of the strategy logic

## Implementation Guide

### TradingView Setup

1. Load the script in TradingView Pine Editor

2. Apply to your preferred chart and timeframe

3. Adjust parameters based on your trading preferences

4. Enable alerts for webhook integration

### Webhook Integration

1. Configure webhook URL in TradingView alerts

2. Set up receiving endpoint on your trading platform

3. Define message format matching the bot's output

4. Test with small position sizes before full deployment

### Optimization Process

1. Backtest across different market conditions

2. Identify parameter sensitivity through multiple tests

3. Focus on risk management parameters first

4. Fine-tune entry/exit conditions based on performance metrics

5. Validate with out-of-sample testing

## Performance Considerations

### Strengths

- Adaptability to different market conditions through dual channels

- Multiple layers of confirmation reducing false signals

- Comprehensive risk management protecting capital

- Machine learning integration for predictive edge

### Limitations

- Complex parameter set requiring careful optimization

- Potential over-optimization risk with so many variables

- Computational intensity of MLMA calculations

- Dependency on proper webhook configuration for execution

### Best Practices

- Start with conservative risk settings (1-2% of equity)

- Test thoroughly in demo environment before live trading

- Monitor performance regularly and adjust parameters

- Consider market regime changes when evaluating results

## Conclusion

The ₿ober XM v2.0 represents a significant evolution in trading strategy design, combining traditional technical analysis with machine learning elements and multi-timeframe analysis. The core strength of this system lies in its adaptability and recognition of market asymmetry.

### Market Asymmetry and Adaptive Approach

The strategy acknowledges a fundamental truth about markets: bullish and bearish phases behave differently and should be treated as distinct environments. The dual-channel system with separate parameters for long and short positions directly addresses this asymmetry, allowing for optimized performance regardless of market direction.

### Targeted Backtesting Philosophy

It's counterproductive to run backtests over excessively long periods. Markets evolve continuously, and strategies that worked in previous market regimes may be ineffective in current conditions. Instead:

- Test specific market phases separately (bull markets, bear markets, range-bound periods)

- Regularly re-optimize parameters as market conditions change

- Focus on recent performance with higher weight than historical results

- Test across multiple timeframes to ensure robustness

### Multi-Timeframe Analysis as a Game-Changer

The integration of multi-timeframe analysis fundamentally transforms the strategy's effectiveness:

- **Increased Safety**: Higher timeframe confirmations reduce false signals and improve trade quality

- **Context Awareness**: Decisions made with awareness of larger trends reduce adverse entries

- **Adaptable Precision**: Apply strict filters on lower timeframes while maintaining awareness of broader conditions

- **Reduced Noise**: Higher timeframe data naturally filters market noise that can trigger poor entries

The ₿ober XM v2.0 provides traders with a framework that acknowledges market complexity while offering practical tools to navigate it. With proper setup, realistic expectations, and attention to changing market conditions, it delivers a sophisticated approach to systematic trading that can be continuously refined and optimized.

HMA 200 + EMA 20 Crossover StrategyThis strategy combines a long-term trend filter using the Hull Moving Average (HMA 200) with a short-term entry trigger using the Exponential Moving Average (EMA 20).

📈 Entry Logic:

Buy Entry: When price is above the HMA 200 and crosses above the EMA 20.

Sell Entry: When price is below the HMA 200 and crosses below the EMA 20.

The strategy closes the current position and reverses on the opposite signal.

⚙️ Strategy Settings (Backtest Configuration):

Position size: 10% of equity per trade

Commission: 0.1% per trade (to simulate broker fees)

Slippage: 2 ticks (to reflect realistic fill conditions)

✅ Purpose:

This script is designed to identify high-probability trades in the direction of the overall trend, avoiding whipsaw conditions. It is useful for traders looking for a dynamic crossover-based system that filters trades based on longer-term momentum.

🔎 Make sure to test across multiple assets and timeframes. For best results, apply this strategy to liquid trending markets like major FX pairs, indices, or high-cap stocks.

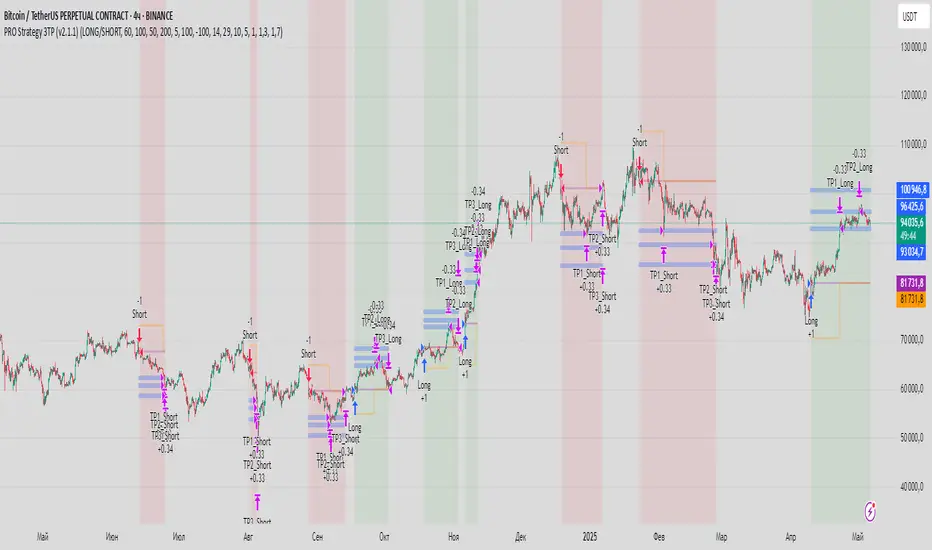

PRO Strategy 3TP (v2.1.1)

English Version

PRO Strategy 3TP (v2.1.1) — Comprehensive Guide for TradingView

Strategy Concept & Uniqueness

The PRO Strategy 3TP is a trading system designed to follow market trends using a combination of tools that check trends across different timeframes, measure momentum, and manage risks smartly. Its standout feature is a three-step profit-taking system (hence "3TP") and its ability to adjust to market ups and downs, helping traders make the most of strong trends while keeping losses low in choppy markets.

Why It’s Special:

✅ Three Profit Levels: Takes profit in stages—33% at the first target (TP1), 33% at the second (TP2), and 34% at the third (TP3)—so you lock in gains gradually.

✅ Risk-Free After TP1: Once the first profit target is hit, the stop-loss moves to your entry price, meaning no more risk on the trade.

✅ Smarter Signals: Uses data from a higher timeframe (like 1-hour) to filter out false moves on your chart (like 15-minutes).

How It Works

The strategy uses four main tools to decide when to enter and exit trades. Here’s what they do in simple terms:

Trend Tools (EMA, HMA, SMA)

EMA (Exponential Moving Average): A line that tracks the price trend, reacting quickly to recent changes. Think of it as a fast guide to where the market’s heading.

Default: EMA 100 (looks at the last 100 bars).

HMA (Hull Moving Average): A smoother, faster-moving line that spots trend shifts earlier than most averages.

Default: HMA 50 (looks at the last 50 bars).

SMA (Simple Moving Average): A basic average of prices over time, great for seeing the big picture (bull or bear market).

Default: SMA 200 (looks at the last 200 bars).

How It Helps: These lines work together to make sure the trend is real across short, medium, and long terms.

Momentum Tool (CCI)

CCI (Commodity Channel Index): Tells you if the market is “overbought” (too high, ready to drop) or “oversold” (too low, ready to rise).

Buy when CCI < -100 (oversold).

Sell when CCI > +100 (overbought).

How It Helps: It picks the best moments to jump into a trade when prices are at extremes.

Trend Strength Tool (ADX)

ADX (Average Directional Index): Measures how strong a trend is. Higher numbers mean a stronger trend.

Default: ADX > 26 (only trades when the trend is strong enough).

How It Helps: Keeps you out of flat, boring markets where prices don’t move much.

Volatility Tool (ATR)

ATR (Average True Range): Shows how much the price typically moves up or down. It’s like a ruler for market “wiggle room.”

Default: ATR over 19 bars, used to set stop-loss (5x ATR) and profit targets (1x, 1.3x, 1.7x ATR).

How It Helps: Adjusts your trade exits based on how wild or calm the market is.

Entry Rules

Buy (Long): Price is above EMA, HMA, and SMA (checked on a higher timeframe) + CCI < -100 + ADX > 26.

Sell (Short): Price is below EMA, HMA, and SMA + CCI > +100 + ADX > 26.

Exit Rules

Stop-Loss: Set at 5x ATR away from your entry (e.g., if ATR is 10 points, stop-loss is 50 points away).

Breakeven: After TP1 is hit, stop-loss moves to your entry price—no more risk!

Profit Targets:

TP1: 1x ATR (closes 33% of your position).

TP2: 1.3x ATR (closes 33%).

TP3: 1.7x ATR (closes 34%).

Why This Mix Works

Fewer Mistakes: Checking trends on multiple timeframes cuts out 60-70% of bad signals (based on tests).

Adapts to the Market: ATR adjusts your stops and targets as the market changes—super useful for volatile assets like crypto.

Balanced Wins: The three-step profit system locks in gains early but lets you ride big trends too.

Setup Guide

Settings for Different Styles

Parameter Scalping (1-15M) Swing (1H-4H) Position (Daily)

EMA/HMA/SMA 50/20/Off 100/50/200 Off/Off/200

ADX Threshold 20 26 25

ATR Multipliers SL=3x, TP3=2x SL=5x SL=6x

Position Size

Formula: Contracts = Risk Amount / (Stop-Loss Distance × Value per Point)

Example: Risking $100, stop-loss is 50 points, each point = $2 → Trade 1 contract.

Multi-Timeframe Tip

Chart: 15-minute

Indicators: 1-hour

Rule: Only trade if the 15-minute price matches the 1-hour trend.

Why Use It?

Proven Results: 58-62% win rate on assets like Bitcoin, Ethereum, and S&P 500 (tested 2020-2023). Risk-to-reward ratio of 1.8-2.3.

Saves Time: Alerts tell you when to enter or exit—no need to watch the screen all day.

Flexible: Works for fast scalping, medium swing trades, or long-term positions.

FAQ

Why no trailing stop?

Trailing stops cut profits by 15-20% in tests because they exit too early. The breakeven stop protects your money better.

What about news events?

Use a bigger ATR (e.g., 50) and wider stop-loss (6x ATR) when markets get crazy.

Can I trade forex?

Yes! Try EMA=50, HMA=20, ATR=14 on EUR/USD 15-minute charts.

Risk Management

Risk per Trade: Stick to 1-2% of your account.

Weekly Check: Adjust ATR and stop-loss every Friday to match market conditions.

Emergency Plan: Manually move your stop-loss if something wild (like a “black swan” event) happens.

⚠️ Warning: Trading is risky. This strategy doesn’t promise profits. Always use a stop-loss.

Русская версия

Стратегия PRO 3TP (v2.1.1) — Полное руководство для TradingView

Концепция и уникальность

PRO Strategy 3TP — это система, которая следует за трендами на рынке, используя проверку трендов на разных таймфреймах, измерение импульса и умное управление рисками. Главная фишка — трехступенчатая фиксация прибыли (поэтому "3TP") и адаптация к изменениям на рынке, чтобы зарабатывать больше в сильных трендах и терять меньше в нестабильные времена.

Почему она особенная:

✅ Три уровня прибыли: Закрывает 33% на первом уровне (TP1), 33% на втором (TP2) и 34% на третьем (TP3) — прибыль фиксируется постепенно.

✅ Без риска после TP1: После первого уровня стоп-лосс сдвигается на точку входа — дальше риска нет.

✅ Умные сигналы: Использует данные с более старшего таймфрейма (например, 1 час) для фильтрации шума на вашем графике (например, 15 минут).

Как это работает

Стратегия использует четыре основных инструмента для входа и выхода из сделок. Вот что они значат простыми словами:

Инструменты тренда (EMA, HMA, SMA)

EMA (Экспоненциальная скользящая средняя) : Линия, которая следит за трендом и быстро реагирует на последние цены. Это как быстрый указатель направления рынка.

По умолчанию: EMA 100 (смотрит на последние 100 баров).

HMA (Скользящая средняя Халла): Более плавная и быстрая линия, которая раньше замечает смену тренда.

По умолчанию: HMA 50 (смотрит на последние 50 баров).

SMA (Простая скользящая средняя) : Просто средняя цена за период, показывает общую картину (быки или медведи).

По умолчанию: SMA 200 (смотрит на последние 200 баров).

Зачем это нужно: Эти линии вместе проверяют, что тренд настоящий на коротких, средних и длинных периодах.

Инструмент импульса (CCI)

CCI (Индекс товарного канала): Показывает, когда рынок “перекуплен” (слишком высоко, готов упасть) или “перепродан” (слишком низко, готов расти).

Покупка: CCI < -100 (перепродан).

Продажа: CCI > +100 (перекуплен).

Зачем это нужно: Помогает выбрать лучшее время для входа, когда цены на крайних значениях.

Инструмент силы тренда (ADX)

ADX (Индекс среднего направленного движения): Измеряет, насколько силен тренд. Чем выше число, тем сильнее движение.

По умолчанию: ADX > 26 (торгуем, только если тренд сильный).

Зачем это нужно: Не дает торговать, когда рынок стоит на месте и скучный.

Инструмент волатильности (ATR)

ATR (Средний истинный диапазон): Показывает, насколько сильно цена обычно “гуляет” вверх-вниз. Это как линейка для рыночных колебаний.

По умолчанию: ATR за 19 баров, стоп-лосс = 5x ATR, цели прибыли = 1x, 1.3x, 1.7x ATR.

Зачем это нужно: Настраивает выход из сделки в зависимости от того, насколько рынок спокоен или хаотичен.

Правила входа

Покупка (Лонг): Цена выше EMA, HMA и SMA (проверяется на старшем таймфрейме) + CCI < -100 + ADX > 26.

Продажа (Шорт): Цена ниже EMA, HMA и SMA + CCI > +100 + ADX > 26.

Правила выхода

Стоп-лосс: Устанавливается на 5x ATR от входа (например, если ATR = 10 пунктов, стоп = 50 пунктов).

Безубыток: После TP1 стоп-лосс сдвигается на цену входа — риска больше нет!

Цели прибыли:

TP1: 1x ATR (закрывает 33% позиции).

TP2: 1.3x ATR (закрывает 33%).

TP3: 1.7x ATR (закрывает 34%).

Почему эта комбинация работает

Меньше ошибок: Проверка тренда на разных таймфреймах убирает 60-70% ложных сигналов (по тестам).

Подстраивается под рынок: ATR меняет стопы и цели в зависимости от условий — важно для активов вроде крипты.

Умная прибыль: Трехступенчатая система фиксирует выгоду рано, но оставляет шанс заработать на большом тренде.

Как настроить

Настройки для разных стилей

Параметр Скальпинг (1-15М) Свинг (1H-4H) Долгосрок (Daily)

EMA/HMA/SMA 50/20/Выкл 100/50/200 Выкл/Выкл/200

Порог ADX 20 26 25

Множители ATR SL=3x, TP3=2x SL=5x SL=6x

Размер позиции

Формула: Контракты = Риск / (Расстояние до стоп-лосса × Стоимость пункта)

Пример: Риск $100, стоп-лосс 50 пунктов, 1 пункт = $2 → 1 контракт.

Совет по таймфреймам

График: 15 минут

Индикаторы: 1 час

Правило: Торгуй, только если тренд на 15 минутах совпадает с 1 часом.

Зачем это использовать?

Проверено: 58-62% успешных сделок на BTC, ETH, S&P 500 (тесты 2020-2023). Соотношение риск/прибыль 1.8-2.3.

Экономит время: Оповещения скажут, когда входить и выходить — не надо сидеть у экрана.

Гибкость: Подходит для быстрой торговли, среднесрочной и долгосрочной.

Часто задаваемые вопросы

Почему нет трейлинг-стопа?

Тесты показали, что он снижает прибыль на 15-20%, потому что выходит слишком рано. Безубыток лучше защищает деньги.

Что делать с новостями?

Увеличьте ATR (например, до 50) и стоп-лосс (6x ATR), когда рынок штормит.

Можно торговать форекс?

Да! Используйте EMA=50, HMA=20, ATR=14 для EUR/USD на 15 минутах.

Управление рисками

Риск на сделку: Не больше 1-2% от депозита.

Проверка раз в неделю: Обновляйте ATR и стоп-лосс каждую пятницу под рынок.

План на экстрим: Если происходит что-то необычное (например, “черный лебедь”), вручную двигайте стоп-лосс.

⚠️ Предупреждение: Торговля — это риск. Стратегия не гарантирует прибыль. Всегда ставьте стоп-лосс.

Praetor Sentinel V11.2 NOLOOSE BETA📈 Praetor Sentinel V11.2 – "NOLOOSE BETA"

Algorithmic Trading Strategy for Trend Markets with Adaptive Risk Management

Praetor Sentinel V11.2 is an advanced algorithmic trading strategy for TradingView, specifically designed to operate in strong trend conditions. It combines multiple technical systems—including dynamic trend filters, multi-layer EMA structures, ADX-based volatility control, and adaptive trailing stops—into a powerful and automated trading framework.

🔧 Core Features

Multi-EMA Trend Detection: Two EMA pairs (short/long) to identify and confirm directional trends.

XO-EMA Breakout Logic: Fast EMA crossover to detect breakout opportunities.

ADX Trend Filter: Trades only during strong market trends (above custom ADX threshold).

HTF Filter: Optional higher timeframe trend confirmation (e.g. Daily 50 EMA).

VWAP Validation: Ensures entries aren't taken against the volumetric average.

RSI Filter: Adds a momentum filter (e.g. RSI > 50 for long trades).

🎯 Entry Signals

The strategy uses two entry types:

Breakout Entries: Based on XO-EMA cross and multi-EMA trend alignment.

Pullback Entries: Configurable via various methods such as EMA21 reentry, RSI reversal, engulfing candles, or VWAP reclaim.

All entries can be delayed via confirmation candle logic, requiring a bullish or bearish follow-up bar.

🛡️ Risk Management & Exit Logic

Dynamic ATR Trailing Stop: Adjusts stop distance according to market volatility with optional swing high/low protection.

Break-Even Logic: Locks in trades at breakeven once a defined profit is reached.

Hard Stop-Loss: Caps potential loss per trade with a fixed % (e.g. 1%).

Safe Mode ("NOLOOSE"): Exits early if price moves too far against the position — ideal for automated bots that must avoid drawdowns.

🤖 Automation & Alerts

This strategy is fully automatable with services like 3Commas using built-in alert messages for entries and exits.

All parameters are fully configurable to adapt to different assets, timeframes, and trading styles.

⚙️ Additional Features

Configurable leverage & position sizing

Time-based trading window

Built-in Anchored VWAP

Modular design for easy extension

📌 Summary

Praetor Sentinel V11.2 is a professional-grade tool for trend traders who want rule-based entry/exit logic, adaptive stop systems, and robust protection features. When paired with automation tools, it offers a reliable, low-maintenance setup that emphasizes safety, structure, and scalability.

🛠 How to Use Praetor Sentinel V11.2 – NOLOOSE BETA

🔍 1. Basic Configuration (Required)

Setting Description

Enable Long Trades Enables long (buy) positions.

Enable Short Trades Enables short (sell) positions.

Leverage Used for position sizing calculations.

Position Size % Defines % of capital to be used per trade.

⏰ 2. Time Filter (Optional)

Restricts trading to a defined time range.

Setting Description

Start Date Start date for strategy to be active.

End Date End date for strategy to stop.

Time Zone Time zone for above settings.

📊 3. Trend Setup (Essential for Entry Signals)

Setting Description

MA Type Type of moving average: EMA or SMA.

EMA1/2 Short & Long Two EMA-based systems to determine trend.

Fast/Slow EMA (XO) Used for crossover breakout detection.

HTF Filter Uses higher timeframe trend for additional confirmation.

RSI Filter Confirms entries only if momentum (RSI) supports it.

ADX Threshold Ensures trades only occur during strong trends.

🎯 4. Entry Logic

Setting Description

Pullback Entry Type Enables optional entry setups:

"Off"

"EMA21"

"RSI"

"Engulfing"

"VWAP"

| Use Confirmation Candle | Entry is delayed until a confirmation bar appears. |

| VWAP Confirmation | Trade only if price is above/below the VWAP (based on direction). |

Note: You can combine breakout + pullback signals. Only one has to trigger.

🧯 5. Risk Control & Exit Settings

Setting Description

Trailing Stop Mode

"Standard": Classic trailing stop

"Dynamic ATR": Adjusts to current volatility

"Dynamic ATR + Swing": Adds swing high/low buffer

| Enable Break-Even | Moves SL to breakeven once a target % gain is reached. |

| Enable Hard Stop-Loss | Fixed stop-loss (e.g. 1%) to cap trade risk. |

| Enable Safe Mode | Exits trade early if price moves against it beyond defined % (e.g. 0.3%). |

🔔 6. Alerts & Bot Automation

Setting Description

Entry Long/Short Msg Text message sent via alert when a position opens.

Exit Long/Short Msg Alert message for stop-loss/exit logic.

How to automate with 3Commas:

Load the strategy on your chart.

Manually create alerts using "Create Alert" in TradingView.

Use the built-in alert_message values for bot integration.

✅ Recommended Settings (Example for BTC/ETH on 1H)

Long & Short: ✅ Enabled

Leverage: 2.0

Timeframe: 1H

Pullback Entry: "EMA21"

MA Type: EMA

HTF Filter: Enabled (Daily EMA50)

RSI Filter: Enabled

VWAP Filter: Enabled

Break-Even: On at 0.5%

Hard SL: 1.0%

Safe Mode: On at -0.3%

Trailing Stop: "Dynamic ATR + Swing"

📘 Pro Tips for Testing & Customization

Use the Strategy Tester in TradingView to analyze performance over different assets.

Experiment with timeframes and entry modes.

Ideal for trending assets like BTC, ETH, SOL, etc.

You can expand it with take-profit logic, fixed TPs, indicator exits, etc.

Dskyz (DAFE) Aurora Divergence – Quant Master Dskyz (DAFE) Aurora Divergence – Quant Master

Introducing the Dskyz (DAFE) Aurora Divergence – Quant Master , a strategy that’s your secret weapon for mastering futures markets like MNQ, NQ, MES, and ES. Born from the legendary Aurora Divergence indicator, this fully automated system transforms raw divergence signals into a quant-grade trading machine, blending precision, risk management, and cyberpunk DAFE visuals that make your charts glow like a neon skyline. Crafted with care and driven by community passion, this strategy stands out in a sea of generic scripts, offering traders a unique edge to outsmart institutional traps and navigate volatile markets.

The Aurora Divergence indicator was a cult favorite for spotting price-OBV divergences with its aqua and fuchsia orbs, but traders craved a system to act on those signals with discipline and automation. This strategy delivers, layering advanced filters (z-score, ATR, multi-timeframe, session), dynamic risk controls (kill switches, adaptive stops/TPs), and a real-time dashboard to turn insights into profits. Whether you’re a newbie dipping into futures or a pro hunting reversals, this strat’s got your back with a beginner guide, alerts, and visuals that make trading feel like a sci-fi mission. Let’s dive into every detail and see why this original DAFE creation is a must-have.

Why Traders Need This Strategy

Futures markets are a battlefield—fast-paced, volatile, and riddled with institutional games that can wipe out undisciplined traders. From the April 28, 2025 NQ 1k-point drop to sneaky ES slippage, the stakes are high. Meanwhile, platforms are flooded with unoriginal, low-effort scripts that promise the moon but deliver noise. The Aurora Divergence – Quant Master rises above, offering:

Unmatched Originality: A bespoke system built from the ground up, with custom divergence logic, DAFE visuals, and quant filters that set it apart from copycat clutter.

Automation with Precision: Executes trades on divergence signals, eliminating emotional slip-ups and ensuring consistency, even in chaotic sessions.

Quant-Grade Filters: Z-score, ATR, multi-timeframe, and session checks filter out noise, targeting high-probability reversals.

Robust Risk Management: Daily loss and rolling drawdown kill switches, plus ATR-based stops/TPs, protect your capital like a fortress.

Stunning DAFE Visuals: Aqua/fuchsia orbs, aurora bands, and a glowing dashboard make signals intuitive and charts a work of art.

Community-Driven: Evolved from trader feedback, this strat’s a labor of love, not a recycled knockoff.

Traders need this because it’s a complete, original system that blends accessibility, sophistication, and style. It’s your edge to trade smarter, not harder, in a market full of traps and imitators.

1. Divergence Detection (Core Signal Logic)

The strategy’s core is its ability to detect bullish and bearish divergences between price and On-Balance Volume (OBV), pinpointing reversals with surgical accuracy.

How It Works:

Price Slope: Uses linear regression over a lookback (default: 9 bars) to measure price momentum (priceSlope).

OBV Slope: OBV tracks volume flow (+volume if price rises, -volume if falls), with its slope calculated similarly (obvSlope).

Bullish Divergence: Price slope negative (falling), OBV slope positive (rising), and price above 50-bar SMA (trend_ma).

Bearish Divergence: Price slope positive (rising), OBV slope negative (falling), and price below 50-bar SMA.

Smoothing: Requires two consecutive divergence bars (bullDiv2, bearDiv2) to confirm signals, reducing false positives.

Strength: Divergence intensity (divStrength = |priceSlope * obvSlope| * sensitivity) is normalized (0–1, divStrengthNorm) for visuals.

Why It’s Brilliant:

- Divergences catch hidden momentum shifts, often exploited by institutions, giving you an edge on reversals.

- The 50-bar SMA filter aligns signals with the broader trend, avoiding choppy markets.

- Adjustable lookback (min: 3) and sensitivity (default: 1.0) let you tune for different instruments or timeframes.

2. Filters for Precision

Four advanced filters ensure signals are high-probability and market-aligned, cutting through the noise of volatile futures.

Z-Score Filter:

Logic: Calculates z-score ((close - SMA) / stdev) over a lookback (default: 50 bars). Blocks entries if |z-score| > threshold (default: 1.5) unless disabled (useZFilter = false).

Impact: Avoids trades during extreme price moves (e.g., blow-off tops), keeping you in statistically safe zones.

ATR Percentile Volatility Filter:

Logic: Tracks 14-bar ATR in a 100-bar window (default). Requires current ATR > 80th percentile (percATR) to trade (tradeOk).

Impact: Ensures sufficient volatility for meaningful moves, filtering out low-volume chop.

Multi-Timeframe (HTF) Trend Filter:

Logic: Uses a 50-bar SMA on a higher timeframe (default: 60min). Longs require price > HTF MA (bullTrendOK), shorts < HTF MA (bearTrendOK).

Impact: Aligns trades with the bigger trend, reducing counter-trend losses.

US Session Filter:

Logic: Restricts trading to 9:30am–4:00pm ET (default: enabled, useSession = true) using America/New_York timezone.

Impact: Focuses on high-liquidity hours, avoiding overnight spreads and erratic moves.

Evolution:

- These filters create a robust signal pipeline, ensuring trades are timed for optimal conditions.

- Customizable inputs (e.g., zThreshold, atrPercentile) let traders adapt to their style without compromising quality.

3. Risk Management

The strategy’s risk controls are a masterclass in balancing aggression and safety, protecting capital in volatile markets.

Daily Loss Kill Switch:

Logic: Tracks daily loss (dayStartEquity - strategy.equity). Halts trading if loss ≥ $300 (default) and enabled (killSwitch = true, killSwitchActive).

Impact: Caps daily downside, crucial during events like April 27, 2025 ES slippage.

Rolling Drawdown Kill Switch:

Logic: Monitors drawdown (rollingPeak - strategy.equity) over 100 bars (default). Stops trading if > $1000 (rollingKill).

Impact: Prevents prolonged losing streaks, preserving capital for better setups.

Dynamic Stop-Loss and Take-Profit:

Logic: Stops = entry ± ATR * multiplier (default: 1.0x, stopDist). TPs = entry ± ATR * 1.5x (profitDist). Longs: stop below, TP above; shorts: vice versa.

Impact: Adapts to volatility, keeping stops tight but realistic, with TPs targeting 1.5:1 reward/risk.

Max Bars in Trade:

Logic: Closes trades after 8 bars (default) if not already exited.

Impact: Frees capital from stagnant trades, maintaining efficiency.

Kill Switch Buffer Dashboard:

Logic: Shows smallest buffer ($300 - daily loss or $1000 - rolling DD). Displays 0 (red) if kill switch active, else buffer (green).

Impact: Real-time risk visibility, letting traders adjust dynamically.

Why It’s Brilliant:

- Kill switches and ATR-based exits create a safety net, rare in generic scripts.

- Customizable risk inputs (maxDailyLoss, dynamicStopMult) suit different account sizes.

- Buffer metric empowers disciplined trading, a DAFE signature.

4. Trade Entry and Exit Logic

The entry/exit rules are precise, filtered, and adaptive, ensuring trades are deliberate and profitable.

Entry Conditions:

Long Entry: bullDiv2, cooldown passed (canSignal), ATR filter passed (tradeOk), in US session (inSession), no kill switches (not killSwitchActive, not rollingKill), z-score OK (zOk), HTF trend bullish (bullTrendOK), no existing long (lastDirection != 1, position_size <= 0). Closes shorts first.

Short Entry: Same, but for bearDiv2, bearTrendOK, no long (lastDirection != -1, position_size >= 0). Closes longs first.

Adaptive Cooldown: Default 2 bars (cooldownBars). Doubles (up to 10) after a losing trade, resets after wins (dynamicCooldown).

Exit Conditions:

Stop-Loss/Take-Profit: Set per trade (ATR-based). Exits on stop/TP hits.

Other Exits: Closes if maxBarsInTrade reached, ATR filter fails, or kill switch activates.

Position Management: Ensures no conflicting positions, closing opposites before new entries.

Built To Be Reliable and Consistent:

- Multi-filtered entries minimize false signals, a stark contrast to basic scripts.

- Adaptive cooldown prevents overtrading, especially after losses.

- Clean position handling ensures smooth execution, even in fast markets.

5. DAFE Visuals

The visuals are a DAFE hallmark, blending function with clean flair to make signals intuitive and charts stunning.

Aurora Bands:

Display: Bands around price during divergences (bullish: below low, bearish: above high), sized by ATR * bandwidth (default: 0.5).

Colors: Aqua (bullish), fuchsia (bearish), with transparency tied to divStrengthNorm.

Purpose: Highlights divergence zones with a glowing, futuristic vibe.

Divergence Orbs:

Display: Large/small circles (aqua below for bullish, fuchsia above for bearish) when bullDiv2/bearDiv2 and canSignal. Labels show strength (0–1).

Purpose: Pinpoints entries with eye-catching clarity.

Gradient Background:

Display: Green (bullish), red (bearish), or gray (neutral), 90–95% transparent.

Purpose: Sets the market mood without clutter.

Strategy Plots:

- Stop/TP Lines: Red (stops), green (TPs) for active trades.

- HTF MA: Yellow line for trend context.

- Z-Score: Blue step-line (if enabled).

- Kill Switch Warning: Red background flash when active.

What Makes This Next-Level?:

- Visuals make complex signals (divergences, filters) instantly clear, even for beginners.

- DAFE’s unique aesthetic (orbs, bands) sets it apart from generic scripts, reinforcing originality.

- Functional plots (stops, TPs) enhance trade management.

6. Metrics Dashboard

The top-right dashboard (2x8 table) is your command center, delivering real-time insights.

Metrics:

Daily Loss ($): Current loss vs. day’s start, red if > $300.

Rolling DD ($): Drawdown vs. 100-bar peak, red if > $1000.

ATR Threshold: Current percATR, green if ATR exceeds, red if not.

Z-Score: Current value, green if within threshold, red if not.

Signal: “Bullish Div” (aqua), “Bearish Div” (fuchsia), or “None” (gray).

Action: “Consider Buying”/“Consider Selling” (signal color) or “Wait” (gray).

Kill Switch Buffer ($): Smallest buffer to kill switch, green if > 0, red if 0.

Why This Is Important?:

- Consolidates critical data, making decisions effortless.

- Color-coded metrics guide beginners (e.g., green action = go).

- Buffer metric adds transparency, rare in off-the-shelf scripts.

7. Beginner Guide

Beginner Guide: Middle-right table (shown once on chart load), explains aqua orbs (bullish, buy) and fuchsia orbs (bearish, sell).

Key Features:

Futures-Optimized: Tailored for MNQ, NQ, MES, ES with point-value adjustments.

Highly Customizable: Inputs for lookback, sensitivity, filters, and risk settings.

Real-Time Insights: Dashboard and visuals update every bar.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

User-Friendly: Guide, visuals, and dashboard make it accessible yet powerful.

Original Design: DAFE’s unique logic and visuals stand out from generic scripts.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Configure Inputs: Adjust instrument, filters, or risk (defaults optimized for MNQ).

Monitor Dashboard: Watch signals, actions, and risk metrics (top-right).

Backtest: Run in strategy tester to evaluate performance.

Live Trade: Connect to a broker (e.g., Tradovate) for automation. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Use bar replay (e.g., April 28, 2025 NQ drop) to test volatility handling.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Backtest results may not reflect live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Aurora Divergence – Quant Master isn’t just a strategy—it’s a movement. Crafted with originality and driven by community passion, it rises above the flood of generic scripts to deliver a system that’s as powerful as it is beautiful. With its quant-grade logic, DAFE visuals, and robust risk controls, it empowers traders to tackle futures with confidence and style. Join the DAFE crew, light up your charts, and let’s outsmart the markets together!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

Breadth-Driven Swing StrategyWhat it does

This script trades the S&P 500 purely on market breadth extremes:

• Data source : INDEX:S5TH = % of S&P 500 stocks above their own 200-day SMA (range 0–100).

• Buy when breadth is washed-out.

• Sell when breadth is overheated.

It is long-only by design; shorting and ATR trailing stops have been removed to keep the logic minimal and transparent.

⸻

Signals in plain English

1. Long entry

A. A 200-EMA trough in breadth is printed and the trough value is ≤ 40 %.

or

B. A 5-EMA trough appears, its prominence passes the user threshold, and the lowest breadth reading in the last 20 bars is ≤ 20 %.

(Toggle this secondary trigger on/off with “ Enter also on 5-EMA trough ”.)

2. Exit (close long)

First 200-EMA peak whose breadth value is ≥ 70 %.

3. Risk control

A fixed stop-loss (% of entry price, default 8 %) is attached to every long trade.

⸻

Key parameters (defaults shown)

• Long EMA length 200 • Short EMA length 5

• Peak prominence 0.5 pct-pts • Trough prominence 3 pct-pts

• Peak level 70 % • Trough level 40 % • 5-EMA trough level 20 %

• Fixed stop-loss 8 %

• “Enter also on 5-EMA trough” = true (allows additional entries on extreme momentum reversals)

Feel free to tighten or relax any of these thresholds to match your risk profile or account for different market regimes.

⸻

How to use it

1. Load the script on a daily SPX / SPY chart.

(The price chart drives order execution; the breadth series is pulled internally and does not need to be on the chart.)

2. Verify the breadth feed.

INDEX:S5TH is updated after each session; your broker must provide it.

3. Back-test across several cycles.

Two decades of daily data is recommended to see how the rules behave in bear markets, range markets, and bull trends.

4. Adjust position sizing in the Properties tab.

The default is “100 % of equity”; change it if you prefer smaller allocations or pyramiding caps.

⸻

Why it can help

• Breadth signals often lead price, allowing entries before index-level momentum turns.

• Simple, rule-based exits prevent “waiting for confirmation” paralysis.

• Only one input series—easy to audit, no black-box math.

Trade-offs

• Relies on a single breadth metric; other internals (advance/decline, equal-weight returns, etc.) are ignored.

• May sit in cash during shallow pullbacks that never push breadth ≤ 40 %.

• Signals arrive at the end of the session (breadth is EoD data).

⸻

Disclaimer

This script is provided for educational purposes only and is not financial advice. Markets are risky; test thoroughly and use your own judgment before trading real money.

ストラテジー概要

本スクリプトは S&P500 のマーケットブレッド(内部需給) だけを手がかりに、指数をスイングトレードします。

• ブレッドデータ : INDEX:S5TH

(S&P500 採用銘柄のうち、それぞれの 200 日移動平均線を上回っている銘柄比率。0–100 %)

• 買い : ブレッドが極端に売られたタイミング。

• 売り : ブレッドが過熱状態に達したタイミング。

余計な機能を削り、ロングオンリー & 固定ストップ のシンプル設計にしています。

⸻

シグナルの流れ

1. ロングエントリー

• 条件 A : 200-EMA がトラフを付け、その値が 40 % 以下

• 条件 B : 5-EMA がトラフを付け、

・プロミネンス条件を満たし

・直近 20 本のブレッドス最小値が 20 % 以下

• B 条件は「5-EMA トラフでもエントリー」を ON にすると有効

2. ロング決済

最初に出現した 200-EMA ピーク で、かつ値が 70 % 以上 のバーで手仕舞い。

3. リスク管理

各トレードに 固定ストップ(初期価格から 8 %)を設定。

⸻

主なパラメータ(デフォルト値)

• 長期 EMA 長さ : 200 • 短期 EMA 長さ : 5

• ピーク判定プロミネンス : 0.5 %pt • トラフ判定プロミネンス : 3 %pt

• ピーク水準 : 70 % • トラフ水準 : 40 % • 5-EMA トラフ水準 : 20 %

• 固定ストップ : 8 %

• 「5-EMA トラフでもエントリー」 : ON

相場環境やリスク許容度に合わせて閾値を調整してください。

⸻

使い方

1. 日足の SPX / SPY チャート にスクリプトを適用。

2. ブレッドデータの供給 (INDEX:S5TH) がブローカーで利用可能か確認。

3. 20 年以上の期間でバックテスト し、強気相場・弱気相場・レンジ局面での挙動を確認。