Machine Learning: Support and Resistance [YinYangAlgorithms]Overview:

Support and Resistance is normally based upon Pivot Points and Highest Highs and Lowest Lows. Many times coders even incorporate Volume, RSI and other factors into the equation. However there may be a downside to doing a pure technical approach based on historical levels. We live in a time where Machine Learning is becoming more and more used; thus we have decided to create a Machine Learning Support and Resistance Projection based Indicator. Rather than using traditional Support and Resistance calculations using historical data, we have taken a rather different approach. This Indicator instead attempts to Predict and Project where Support and Resistance locations will be based on a Machine Learning Model using a form of KNN (k-Nearest Neighbors).

Since this indicator creates a Projection of where it deems Support and Resistance will be, it has the ability to move its Support and Resistance before the price even gets to it if it believes it will surpass its projections. This may create a more accurate placement of Support and Resistance as they’re not based on historical levels.

This Indicator does not Repaint.

How it works:

This Indicator makes its projections based on the source you provide (by default close) of the previous bar and submits the source, RSI and EMA to our Projection Function to get its projection of the current bar.

The Projection function essentially calculates potential movement after finding the differences between the source the MA from the current bar, previous bar and average over the span of Machine Learning Length.

Potential movement is defined as:

Average Difference + Average(Machine Learning Average, Average Last Distance)

Average Difference: (Absolute value of Current Source - Current MA) - (Absolute value of Machine Learning Average - Machine Learning MA)

Average Last Distance: Average(Current Source - Current MA, Previous Source - Previous MA)

It then predicts the next bars directional movement (bullish or bearish bar) using several factors:

Previous Source > Previous MA

Current Source - Current MA > Average Source - Average MA

Current RSI > Previous RSI

Current RSI > 30 and Previous RSI <= 30

Current RSI < 70 and Previous RSI >= 70

This helps us to predict the direction the next bar may move.

We then calculate a multiplier that we apply to our Potential Movement value to get our final result which is our Current Bars Close Projection.

Our multiplier is calculated using:

(Current RSI > 30 and Previous RSI <= 30) OR (Current RSI < 70 and Previous RSI >= 70)

Current Source - Current MA > Previous Source - Previous MA

We then create an array and fill it with the previous X projections (Machine Learning Length) and send it to another function. This function, if told to, will sort the data accordingly and then output the KNN average of the length given.

We calculate and plot various KNN lengths to create different Zones:

Strong Support: Length of 2 but sort the data Ascending (low to high)

Strong Resistance: Length of 2 but sort the data Descending (high to low)

Support: Length of Machine Length Length / 10 or Min of 2 sorted by Ascending

Resistance: Length of Machine Length Length / 10 or Min of 2 sorted by Descending

There are also 4 other plots you may be wondering what they are, there is your AVG, VWMA, Long Term Memory and Current Projection.

By default your Current Projection is disabled in settings but you can enable it if you are curious to see how the projections for each close are calculated. It is, however, not a crucial point of interest (white line).

The average is simply the average value of the Machine Learning Data (purple line).

The VWMA is a VWMA calculation applied to our Data over a length specified in settings (by default 1)(blue line). The VWMA is crucial when combined with the Avg as they can cross over and under each other. These crosses represent potential Bullish and Bearish zones.

Lastly, but certainly not least, we have the Long Term Memory (maroon line). The Long Term Memory can be displayed either as an ‘Average’, ‘Hard Line’ or ‘None’. The Long Term Average is only updated every Machine Learning Length Bar Index’s and is populated with the average of the Machine Learning Data. For Instance, if Machine Learning Length is set to 100, the Long Term Memory is only updated every 100 bars, and since its length is the same as the Machine Learning Length, that means its data is composed of 10,000 bars worth of data. The Long Term Memory may be very beneficial for determining where Support and Resistance lie over the Long Term within a Machine Learning Algorithm. When set to ‘Average’ it plots the connection lines diagonally, and although they may be more visually appealing, they’re less useful when it comes to actually seeing support and resistance as generally speaking, support and resistance lie on the horizontal. When set to ‘Hard Line’ the Long Term Memory is connected with hard lines and holds the price value until the next time it is updated. This makes it much more useful for potentially identifying Support and Resistance.

Tutorial:

Here is an overview of what the Indicator looks like, now let's start to dissect it.

In the example above we can see how all of the lines between the Major Support and Resistance zones may act as BOTH Support and Resistance depending on which side the price is currently on. In the circle on the left, we can see how it can fluctuate between the two. If you look at the circle on the right, we can see how the Average line acts as a strong support before it fails to maintain it. Generally speaking, most Support and Resistance locations may potentially fail to hold after 3 tests, as the Average did in this example.

As you can see, the Support and Resistance doesn’t wait to be tested before adjusting, which is why there are 2 lines which create their zones. The inner line is the Support/Resistance and the outer line is the Strong Support/Resistance. The Yellow Circle shows the inner line was able to calculate the moving resistance correctly and then adjusted accordingly as it was projecting the price to keep increasing. However, if you look at the White Circle, you can see that since there was first a crash, and then parabolic movement, that the inner zone could not move and predict the resistance as well as the outer zone could.

We consider the price to be ‘Overvalued’ when it is above the VWMA (blue line) and ‘Undervalued’ when it is below the VWMA. It is considered ‘fair’ price when it is within the VWMA to Average zone (between the blue and purple lines). If you look at the example above, you’ll notice where the two yellow circles are, it is not only considered ‘Overvalued’, but it then proceeds to ride the inner resistance line upwards. This is common when the market is overly bullish and vice versa when it is bearish. Please keep in mind, although it is common, it doesn’t mean a correction can’t happen.

In this example above we look at the last bull run that may have started due to the halving. This bull run was very bullish as you can see in the example above. The price was constantly sitting within the Resistance Zone and the VWMA that was very close to it was constantly acting as a Support. Naturally, due to the Algorithm used in this Indicator, as the momentum starts to slow down, the VWMA (blue line) will start to space out more and more from the Resistance Zone. This doesn’t mean the momentum is gone, it just means it may be slowing down.

Unfortunately we have to study the Bear Market with a different perspective than the Bull Market. However, there are still some similarities within the two. If you refer to the example above and the previous example, you can clearly see that the Bull Market loves to stay with the Resistance Zone and use the VWMA as a Support. However, the Bear Market does not. This is a normal occurrence, however we can see from the example above you may see a correction / horizontal movement when the Outer Support Line is touched. If you look at all 3 yellow circles, the Outer Support Line was touched, then either a small correction or horizontal consolidation occurred.

We will conclude our Tutorial here, hopefully you’ll be able to benefit from a moving Support and Resistance calculated with Machine Learning that projects its locations, rather than using traditional calculations.

Settings:

Source: This source is the base for all our calculations

Machine Learning Length: How much projection data are we storing and using to make calculations.

Smoothing Length: We need to smooth calculations such as RSI, EMA and VWMA. What length are we smoothing it with?

VWMA ML Projection Length: How far into our Machine Learning data should we average for our VWMA. Please note the 'Smoothing Length' is still applied here after getting the Projection Average.

Long Term Memory: Long term memory has the same storage length but is only updated once per Machine Learning Length. For instance, if Machine Learning Length is 100, it will save the Average of our data once every 100 bars. This means its memory is an average of 10,000 bars of Machine Learning. 'Average' connects its values diagonally whereas 'Hard Line' holds its value until it changes.

Use Average Last Distance In Potential Movement: This can help accuracy but generally also displaces the Support and Resistance by projecting it further.

Show Current Projection: Projections occur for each bar, and our Machine Learning utilizes these projections by storing and evaluating them. This toggle will display the Current Projection Line which is used to create all our Projections.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

Pesquisar nos scripts por "algo"

Autocorrelation OscillatorReleasing the autocorrelation oscillator.

NOTE! Please be sure to read the description. This is a theoretical indicator and its important to understand the theory behind its use.

About the indicator:

Before getting into the indicator and its functionality, its important to discuss the theoretical underpinnings of the indicator.

The autocorrelation oscillator operates on two theories of market behaviour that go hand in hand. Those theories are the market efficiency theory and the random walk theory (or hypothesis ).

Market efficiency theory: The market efficiency theory or "Efficient Market Hypothesis (EMH)" postulates that all available information is reflected in a ticker's price almost instantaneously and thus it is impossible for an investor or trader to get ahead of the market because we cannot respond to the speed that the market responds. Of course, there are many holes in this theory, the most notable being that the market is a function of humans. Absent humans and their technological integrations into the market, the market would cease to react at all. But that's besides the point. This is a widely accepted theory and one in which I can mathematically observe through statistical tests. The truth behind this theory is the market is efficient for responding to evolving economic and financial information, likely owning to huge amounts of computer and algorithmic integration into trading, and thus the market is more efficient than the average person is capable (absent computerized algorithms and integration) of ascertaining nuanced financial and economic circumstances. By the time we the people can appraise information, the market has already acted on it. And that is the main premise of the EMH.

The next theory is the Random Walk Theory or Hypothesis (RWH). This builds on the EMH and essentially postulates that the market reacts so quickly to price in current circumstances that it is too random for people to truly exploit and benefit from.

The result of these two theories is two-fold and can be summarized as such:

a) The market behaves in a chaotic fashion that is seemingly random and is incapable of being predicted effectively; and

b) The market is more efficient than a person in incorporating key fundamental information, contributing to the high degree of seemingly random behaviour.

So, how does this help us?

It is said, because of the EMH and the RWH, the only way to truly exploit the market for profit is by:

a) Buying and holding and investing under the bias that stocks will eventually rise in value; or

b) For short term trading, exploiting the pricing anomalies within the data.

So how do we exploit pricing anomalies within the data?

Well, in my own research on market efficiency and behaviour, I have identified many ways of figuring out some anomalies. One of the most effective ways is by looking at simple correlation of lagged values, or autocorrelation for short.

What is autocorrelation and how to use it in relation to EMH and RWH?

Autocorrelation refers to the correlative relationship among the values in a series. Put simply, its the relationship of the same variable over time. For example, if we wanted to look at the auto-correlation of a ticker's high price, we would take, say, 5 to 7 previous high prices and correlate them with the current high price in a series dataset. If the EMH and RWH are true, the correlation among all the variables should have an average less than 0.5 or greater than -0.5. This would indicate true randomness in the dataset and thus an efficient market.

However, if the average of all of the sum's of these correlations are greater than or equal to 0.5 or less than or equal to -0.5, that indicates there is a high degree of autocorrelation and thus the EMH ad RWH is being invalidated as the market is not operating efficiently. This is an anomaly and this anomaly can be exploited.

So how do we exploit it?

Well, when the EMH and RWH hypothesis is being invalidated, we can expect what I coin as a "Regression to Chaos" i.e. the market will revert back to an efficient equilibrium state. So if we have a high correlation of the lagged variables and a strong uptrend or downtrend correlation, we can expect an inefficient market to correct back to an efficient market (i.e. have a reversal from the current trend).

So how does the indicator work?

The indicator measures the lagged correlation of the previous 5 highs and lows of a ticker. A high correlation among all of the highs and lows that exceeds 0.8 would be an invalidation of the EMH and RWH and thus signal a correction to come (i.e. a Regression to Chaos).

The indicator will display this by changing colour. Red for a bearish reversal and green for a bullish. Let's take a look below using the ticker MSFT:

Above we can see the indicator identifying observed inefficiencies within the MSFT ticker on the 1 minute timeframe. The green vertical lines correspond to potential bullish reversals as a result of bearish inefficiencies, the red correspond to bearish reversals as a result of bullish inefficiencies.

You can see these lead to reversals within the ticker.

Components of the indicator:

In the chart above we see the following that are being indicated by arrows:

Red Arrows: Show the identified inefficiencies. Red for bullish inefficiencies (i.e. bearish reversal), green for bearish inefficiencies (i.e. bullish reversal)

Yellow Arrow: The lagged variable chart. This will display the current correlation among all the lagged variables the indicator is assessing.

Teal arrow: Displays the current strength of the trend by correlating the trend to time. A strong negative value (i.e. a value less than or equal to -0.5) indicates a strong downtrend, a strong positive value indicates the inverse.

You can unselect the data-tables in the settings menu if you just want to view the correlation line itself. This part of the indicator is customizable. You can also define the lookback period; however, it is strongly recommended to leave it at 14 as this maintains the use of this indicator as an oscillator.

And that is the indicator! Let me know your comments, questions and feedback below.

Safe trades everyone!

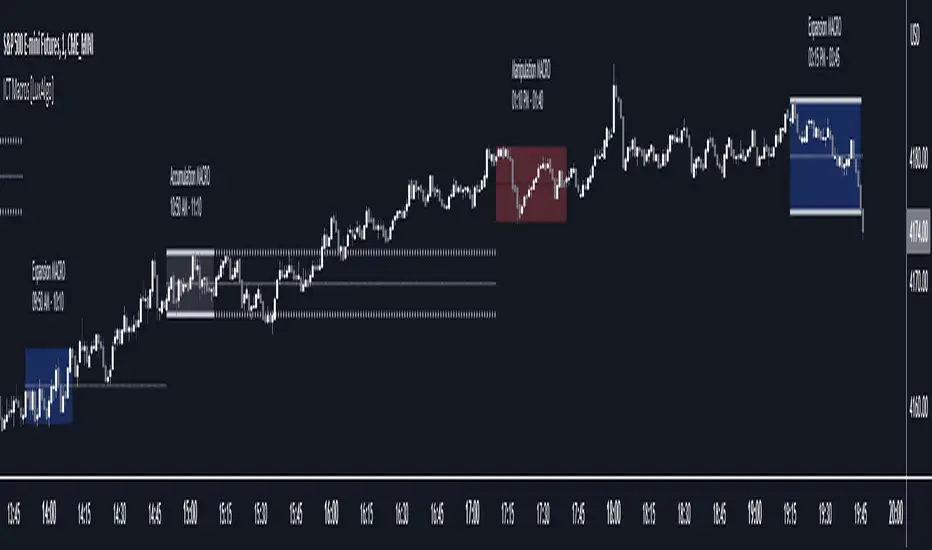

ICT Macros [LuxAlgo]The ICT Macros indicator aims to highlight & classify ICT Macros, which are time intervals where algorithmic trading takes place to interact with existing liquidity or to create new liquidity.

🔶 SETTINGS

🔹 Macros

Macro Time options (such as '09:50 AM 10:10'): Enable specific macro display.

Top Line , Mid Line , Bottom Line and Extending Lines options: Controls the lines for the specific macro.

🔹 Macro Classification

Length : A length to detect Market Structure Brakes and classify macro type based on detection.

Swing Area : Swing or Liquidity Area selection, highest/lowest of the wick or the candle bodies.

Accumulation , Manipulation and Expansion color options for the classified macros.

🔹 Others

Macro Texts : Controls both the size and the visibility of the macro text.

Alert Macro Times in Advance (Minutes) : This option will plot a vertical line presenting the start of the next macro time. The line will not appear all the time, but it will be there based on remaining minutes specified in the option.

Daylight Saving Time (DST) : Adjust time appropriate to Daylight Saving Time of the specific region.

🔶 USAGE

A macro is a way to automate a task or procedure which you perform on a regular basis.

In the context of ICT's teachings, a macro is a small program or set of instructions that unfolds within an algorithm, which influences price movements in the market. These macros operate at specific times and can be related to price runs from one level to another or certain market behaviors during specific time intervals. They help traders anticipate market movements and potential setups during specific time intervals.

To trade these effectively, it is important to understand the time of day when certain macros come into play, and it is strongly advised to introduce the concept of liquidity in your analysis.

Macros can be classified into three categories where the Macro classification is calculated based on the Market Structure prior to macro and the Market Structure during the macro duration:

Manipulation Macro

Manipulation macros are characterized by liquidity being swept both on the buyside and sellside.

Expansion Macro

Expansion macros are characterized by liquidity being swept only on the buyside or sellside. Prices within these macros are highly correlated with the overall trend.

Accumulation Macro

Accumulation macros are characterized by an accumulation of liquidity. Prices within these macros tend to range.

The script returns the maximum/minimum price values reached during the macro interval alongside the average between the maximum/minimum and extends them until a new macro starts. These levels can act as supports and resistances.

🔶 DETAILS

All required data for the macro detection and classification is retrieved using 1 minute data sets, this includes candles as well as pivot/swing highs and lows. This approach guarantees the visually presented objects are same (same highs/lows) on higher timeframes as well as the macro classification remain same as it is in 1 min charts.

8 Macros can be displayed by the script (4 are enabled by default):

02:33 AM 03:00 London Macro

04:03 AM 04:30 London Macro

08:50 AM 09:10 New York Macro

09:50 AM 10:10 New York Macro

10:50 AM 11:10 New York Macro

11:50 AM 12:10 New York Launch Macro

13:10 PM 13:40 New York Macro

15:15 PM 15:45 New York Macro

🔶 ALERTS

When an alert is configured, the user will have the ability to be notified in advance of the next Macro time, where the value specified in 'Alert Macro Times in Advance (Minutes)' option indicates how early to be notified.

🔶 LIMITATIONS

The script is supported on 1 min, 3 mins and 5 mins charts.

🔶 RELATED SCRIPTS

Local Model Kalman Market ModeIntroduction

Heyo guys, I made a new (repainting) indicator called Local Model Kalman Market Mode.

I created it, because I wanted a reliable market mode filter for a potential mean-reversion strategy (e. g. BB Scalping).

On the screenshot you can see an example of how to use it in a BB strategy.

E.g. you would enter long when you have bullish divergence, price is under lower BB, price is under PoC and this indicator here shows range-bound market phase.

You would exit long on cross of the middle band.

Description

The indicator attempts to model the underlying market using different local models (i.e., trending, range-bound, and choppy) and combines them using the T3 Six Pole Kalman Filter to generate an overall estimate of the market.

The Fisher Transform is applied on the price to reach a Gaussian distribution, which increases the accuracy of the indicator itself.

The script first defines state variables for each local model, which include trend direction, trend strength, upper and lower bounds of the range, volatility of the range, level of choppiness, and strength of noise.

Then, likelihood functions are defined for each local model based on the state variables.

Next, the script calculates weights for each local model based on their likelihoods and uses them to calculate state variables for the overall estimate.

Finally, the script combines the state variables using the T3 Six Pole Kalman Filter to generate the overall estimate of the market, which is plotted in blue.

Fundamental Knowledge

To understand the explanation of the indicator and the script, there are a few fundamental concepts that you need to know:

Market: A market is a place where buyers and sellers come together to exchange goods or services.

In the context of trading, the market refers to the exchange where financial instruments such as stocks, currencies, and commodities are bought and sold.

Local models: Local models are statistical models that attempt to capture the characteristics of a particular market regime.

For example, a trending market may have different characteristics than a range-bound market or a choppy market.

The indicator uses different local models to capture the different market regimes.

Trend direction and strength: The trend direction refers to the direction in which the market is moving, either up or down.

The trend strength refers to the magnitude of the trend and how likely it is to continue.

Range-bound market: A range-bound market is a market where prices are trading within a specific range, with a clear upper and lower bound.

Choppiness: Choppiness refers to the degree of irregularity in price movements, often seen in sideways or range-bound markets.

Volatility: Volatility refers to the degree of variation in the price of an asset over time. High volatility implies larger price swings, while low volatility implies smaller price swings.

Kalman filter: A Kalman filter is a mathematical algorithm used to estimate an unknown variable from a series of noisy measurements.

In the context of the indicator, the Kalman filter is used to generate an overall estimate of the market by combining the local models.

T3 Six Pole Kalman Filter: The T3 Six Pole Kalman Filter is a specific type of Kalman filter that is used to smooth and filter time-series data, such as the price data of a financial instrument.

Fisher Transform: The Fisher Transform is a mathematical formula used to transform any probability distribution into a Gaussian normal distribution. It is commonly used in technical analysis to transform non-Gaussian indicators into ones that are more suitable for statistical analysis.

By understanding these fundamental concepts, you should have a basic understanding of how the indicator works and how it generates an overall estimate of the market.

Usage

You can use this indicator on every timeframe.

Users can customize the parameters of the T3 Six Pole Kalman Filter (T3 length, alpha, beta, gamma, and delta) using input functions.

Try out different parameter combinations and use the one you like most.

Thank you for checking this out. Leave me a comment or boost the script, when you wanna support me! 👌

--

Credits to:

▪@HPotter - Fisher Transform

▪@loxx - T3

▪ChatGPT - Helped me to make the research for this indicator and helped to build the core algorithm.

The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)

Are you tired of manually analyzing charts and trying to find profitable trading opportunities? Look no further! Our algorithmic trading strategy, "Flash," is here to simplify your trading process and maximize your profits.

Flash is an advanced trading algorithm that combines three powerful indicators to generate highly selective and accurate trading signals. The Momentum-RSI, Super-Trend Analysis and EMA-Strategy indicators are used to identify the strength and direction of the underlying trend.

The Momentum-RSI signals the strength of the trend and only generates trading signals in confirmed upward or downward trends. The Super-Trend Analysis confirms the trend direction and generates signals when the price breaks through the super-trend line. The EMA-Strategy is used as a qualifier for the generation of trading signals, where buy signals are generated when the EMA crosses relevant trend lines.

Flash is highly selective, as it only generates trading signals when all three indicators align. This ensures that only the highest probability trades are taken, resulting in maximum profits.

Our trading strategy also comes with two profit management options. Option 1 uses the so-called supertrend-indicator which uses the dynamic ATR as a key input, while option 2 applies pre-defined, fixed SL and TP levels.

The settings for each indicator can be customized, allowing you to adjust the length, limit value, factor, and source value to suit your preferences. You can also set the time period in which you want to run the backtest and how many dollar trades you want to open in each position for fully automated trading.

Choose your preferred trade direction and stop-loss/take-profit settings, and let Flash do the rest. Say goodbye to manual chart analysis and hello to consistent profits with Flash. Try it now!

General Comments

This Flash Strategy has been developed in cooperation between Baby_whale_to_moon and JS-TechTrading. Cudos to Baby_whale_to_moon for doing a great job in transforming sophisticated trading ideas into pine scripts.

Detailed Description

The “Flash” script considers the following indicators for the generation of trading signals:

1. Momentum-RSI

2. ‘Super-Trend’-Analysis

3. EMA-Strategy

1. Momentum-RSI

• This indicator signals the strength of the underlying upward- or downward-trend.

• The signal range of this indicator is from 0 to 100. Values > 60 indicate a confirmed upward- or downward-trend.

• The strategy will only generate trading signals in case the stock (or any other financial security) is in a confirmed upward- (long entry signals) or downward-trend (short entry signals).

• This indicator provides information with regards to the strength of the underlying trend and it does not give any insight with regard to the direction of the trend. Therefore, this strategy also considers other indicators which provide technical confirmation with regards to the direction of the underlying trend.

Graph 1 shows this concept:

• The Momentum-RSI indicator gives lower readings during consolidation phases and no trading signals are generated during these periods.

Example (graph 2):

2. Super-Trend Analysis

• The red line in the graph below represents the so-called super-trend-line. Trading signals are only generated in case the price action breaks through this super-trend-line indicating a new confirmed upward-trend (or downward-trend, respectively).

• If that happens, the super trend-line changes its color from red to green, giving confirmation that the trend changed from bearish to bullish and long-entries can be considered.

• The vice-versa approach can be considered for short entries.

Graph 3 explains this concept:

3. Exponential Moving Average / EMA-Strategy

The functionality of this EMA-element of the strategy has been programmed as follows:

• The exponential moving average and two other trend lines are being used as qualifiers for the generation of trading-signals.

• Buy-signals for long-entries are only considered in case the EMA (yellow line in the graph below) crosses the red line.

• Sell-signals for short-entries are only considered in case the EMA (yellow line in the graph below) crosses the green line.

An example is shown in graph 4 below:

We use this indicator to determine the new trend direction that may occur by using the data of the price's past movement.

4. Bringing it all together

This section describes in detail, how this strategy combines the Momentum-RSI, the super-trend analysis and the EMA-strategy.

The strategy only generates trading-signals in case all of the following conditions and qualifiers are being met:

1. Momentum-RSI is higher than the set value of this strategy. The standard and recommended value is 60 (graph 5):

2. The super-trend analysis needs to indicate a confirmed upward-trend (for long-entry signals) or a confirmed downward-trend (for short-entry signals), respectively.

3. The EMA-strategy needs to indicate that the stock or financial security is in a confirmed upward-trend (long-entries) or downward-trend (short-entries), respectively.

The strategy will only generate trading signals if all three qualifiers are being met. This makes this strategy highly selective and is the key secret for its success.

Example for Long-Entry (graph 6):

When these conditions are met, our Long position is opened.

Example for Short-Entry (graph 7):

Trade Management Options (graph 8)

Option 1

In this dynamic version, the so-called supertrend-indicator is being used for the trade exit management. This supertrend-indicator is a sophisticated and optimized methodology which uses the dynamic ATR as one of its key input parameters.

The following settings of the supertrend-indicator can be changed and optimized (graph 9):

The dynamic SL/TP-lines of the supertrend-indicator are shown in the charts. The ATR-length and the supertrend-factor result in a multiplier value which can be used to fine-tune and optimize this strategy based on the financial security, timeframe and overall market environment.

Option 2 (graph 10):

Option 2 applies pre-defined, fixed SL and TP levels which will appear as straight horizontal lines in the chart.

Settings options (graph 11):

The following settings can be changed for the three elements of this strategy:

1. (Length Mom-Rsi): Length of our Mom-RSI indicator.

2. Mom-RSI Limit Val: the higher this number, the more momentum of the underlying trend is required before the strategy will start creating trading signals.

3. The length and factor values of the super trend indicator can be adjusted:ATR Length SuperTrend and Factor Super Trend

4. You can set the source value used by the ema trend indicator to determine the ema line: Source Ema Ind

5. You can set the EMA length and the percentage value to follow the price: Length Ema Ind and Percent Ema Ind

6. The backtesting period can be adjusted: Start and End time of BackTest

7. Dollar cost per position: this is relevant for 100% fully automated trading.

8. Trade direction can be adjusted: LONG, SHORT or BOTH

9. As we explained above, we can determine our stop-loss and take-profit levels dynamically or statically. (Version 1 or Version 2 )

Display options on the charts graph 12):

1. Show horizontal lines for the Stop-Loss and Take-profit levels on the charts.

2. Display relevant Trend Lines, including color setting options for the supertrend functionality. In the example below, green lines indicate a confirmed uptrend, red lines indicate a confirmed downtrend.

Other comments

• This indicator has been optimized to be applied for 1 hour-charts. However, the underlying principles of this strategy are supply and demand in the financial markets and the strategy can be applied to all timeframes. Daytraders can use the 1min- or 5min charts, swing-traders can use the daily charts.

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The combination of the qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

dmn's ICT ToolkitThis is my quality of life indicator for forex trading using the methods and concepts of ICT.

The idea is to automate marking up important price levels and times of the day instead of doing it manually every day.

Killzones

Marks the most volatile times of the day on the chart, during which the intraday high/low usually takes place.

Particularly impactful when there's news released during these times.

London Open (02:00-05:00 EST)

New York Open (08:30-11:00 EST)

London Close (10:00-11:30 EST)

True Day delineation

Vertical line at the start of the "true day" (00:00 EST), start of the algorithmic trading day and aids in visualizing the intraday direction.

New York midnight price level

Noteworthy price level at the start of the "true day".

This price level is referenced by the interbank trading algorithms during the day. Buy below it on bullish days, sell above it on bearish days.

Daily open price level

Reference level for optimal trade entries. Buy below it on bullish days, sell above it on bearish days.

Central Banks Dealers Range (CBDR) (14:00-20:00 EST) &

Central Banks Dealers Flout (CBDF) (15:00-24:00 EST) &

Asian Range (AR) (20:00-24:00 EST)

The standard deviation lines available are used to make predictions for short-term future highs/lows when the CBDR and AR are smaller than 40 pips.

Trade them by looking for 5/15min key levels that converge with the projection levels.

X days Average Daily Range (ADR)

Default to 5 days back, gives an idea of how much movement to expect intraday when the ADR high/low is converging with CBDR/CBDF/AR standard deviations.

Current Daily Range (CDR)

Used for comparison against the ADR to help determine if there's enough intraday range left to enter a trade.

Dynamically changes color based on percentage of the ADR. Green below 50% of ADR, orange between 50 and 100%, red when CDR exceeds ADR.

All of the above are used in conjunction with each other and higher timeframe levels of importance to find entries and target.

Note: Preferably use New York's time zone for your charts.

BTC Indicator By Megalodon TradingThis indicator is designed help you see the potential reversal zones and it helps you accumulate for the long run.

This combines price data on any chart. The chart isolates between 0 and -100. Below -80 is a buy, above -20 is a sell location.

In these locations, try to Slowly Buy and Slowly Sell (accumulate...)

Story Of This Indicator

~I was always obsessed with Fibonacci and used Fibonacci all the time. Thus, i wanted to make a tool to see buying locations and selling locations.

Instead of drawing fibonacci's and manually interpreting buy/sell locations, i wanted algorithms to do the job for me. So, i created this algorithm and many more like it.

If you think i did a good job and want to do further work with me, feel free to contact.

I have a ton of other tools that can change everything for your trading/investing.

Best wishes

~Megalodon

ICT IPDA Look BackThis script automatically calculates and updates ICT's daily IPDA look back time intervals and their respective discount / equilibrium / premium, so you don't have to :)

IPDA stands for Interbank Price Delivery Algorithm. Said algorithm appears to be referencing the past 20, 40, and 60 days intervals as points of reference to define ranges and related PD arrays.

Intraday traders can find most value in the 20 Day Look Back box, by observing imbalances and points of interest.

Longer term traders can reference the 40 and 60 Day Look Back boxes for a clear indication of current market conditions.

Implied Volatility Estimator using Black Scholes [Loxx]Implied Volatility Estimator using Black Scholes derives a estimation of implied volatility using the Black Scholes options pricing model. The Bisection algorithm is used for our purposes here. This includes the ability to adjust for dividends.

Implied Volatility

The implied volatility (IV) of an option contract is that value of the volatility of the underlying instrument which, when input in an option pricing model (such as Black–Scholes), will return a theoretical value equal to the current market price of that option. The VIX , in contrast, is a model-free estimate of Implied Volatility. The latter is viewed as being important because it represents a measure of risk for the underlying asset. Elevated Implied Volatility suggests that risks to underlying are also elevated. Ordinarily, to estimate implied volatility we rely upon Black-Scholes (1973). This implies that we are prepared to accept the assumptions of Black Scholes (1973).

Inputs

Spot price: select from 33 different types of price inputs

Strike Price: the strike price of the option you're wishing to model

Market Price: this is the market price of the option; choose, last, bid, or ask to see different results

Historical Volatility Period: the input period for historical volatility ; historical volatility isn't used in the Bisection algo, this is to serve as a comparison, even though historical volatility is from price movement of the underlying asset where as implied volatility is the volatility of the option

Historical Volatility Type: choose from various types of implied volatility , search my indicators for details on each of these

Option Base Currency: this is to calculate the risk-free rate, this is used if you wish to automatically calculate the risk-free rate instead of using the manual input. this uses the 10 year bold yield of the corresponding country

% Manual Risk-free Rate: here you can manually enter the risk-free rate

Use manual input for Risk-free Rate? : choose manual or automatic for risk-free rate

% Manual Yearly Dividend Yield: here you can manually enter the yearly dividend yield

Adjust for Dividends?: choose if you even want to use use dividends

Automatically Calculate Yearly Dividend Yield? choose if you want to use automatic vs manual dividend yield calculation

Time Now Type: choose how you want to calculate time right now, see the tool tip

Days in Year: choose how many days in the year, 365 for all days, 252 for trading days, etc

Hours Per Day: how many hours per day? 24, 8 working hours, or 6.5 trading hours

Expiry date settings: here you can specify the exact time the option expires

*** the algorithm inputs for low and high aren't to be changed unless you're working through the mathematics of how Bisection works.

Included

Option pricing panel

Loxx's Expanded Source Types

Related Indicators

Cox-Ross-Rubinstein Binomial Tree Options Pricing Model

KERPD Noise Filter - Kaufman Efficiency Ratio and Price DensityThis indicator combines Kaufman Efficiency Ratio (KER) and Price Density theories to create a unique market noise filter that is 'right on time' compared to using KER or Price Density alone. All data is normalized and merged into a single output. Additionally, this indicator provides the ability to consider background noise and background noise buoyancy to allow dynamic observation of noise level and asset specific calibration of the indicator (if desired).

The basic theory surrounding usage is that: higher values = lower noise, while lower values = higher noise in market.

Notes: NON-DIRECTIONAL Kaufman Efficiency Ratio used. Threshold period of 30 to 40 applies to Kaufman Efficiency Ratio systems if standard length of 20 is applied; maintained despite incorporation of Price Density normalized data.

TRADING USES:

-Trend strategies, mean reversion/reversal/contrarian strategies, and identification/avoidance of ranging market conditions.

-Trend strategy where KERPD is above a certain value; generally a trend is forming/continuing as noise levels fall in the market.

-Mean reversion/reversal/contrarian strategies when KERPD exits a trending condition and falls below a certain value (additional signal confluence confirming for a strong reversal in price required); generally a reversal is forming as noise levels increase in the market.

-A filter to screen out ranging/choppy conditions where breakouts are frequently fake-outs and or price fails to move significantly; noise level is high, in addition to the background buoyancy level.

-In an adaptive trading systems to assist in determining whether to apply a trend following algorithm or a mean reversion algorithm.

THEORY / THOUGHT SPACE:

The market is a jungle. When apex predators are present it often goes quiet (institutions moving price), when absent the jungle is loud.

There is always background noise that scales with the anticipation of the silence, which has features of buoyancy that act to calibrate the beginning of the silence and return to background noise conditions.

Trend traders hunt in low noise conditions. Reversion traders hunt in the onset of low noise into static conditions. Ranges can be avoided during high noise and buoyant background noise conditions.

Distance between the noise line and background noise can help inform decision making.

CALIBRATION:

- Set the Noise Threshold % color change line so that the color cut off is where your trend/reversion should begin.

- Set the Background Noise Buoyancy Calibration Decimal % to match the beginning/end of the color change Noise Threshold % line. Match the Background Noise Baseline Decimal %' to the number set for buoyancy.

- Additionally, create your own custom settings; 33/34 and 50 length also provides interesting results.

- A color change tape option can be enabled by un-commenting the lines at the bottom of this script.

Market Usage:

Stock, Crypto, Forex, and Others

Excellent for: NDQ, J225, US30, SPX

Market Conditions:

Trend, Reversal, Ranging

End-pointed SSA of FDASMA [Loxx]End-pointed SSA of FDASMA is a modification of Fractal-Dimension-Adaptive SMA (FDASMA) using End-Pointed Singular Spectrum Analysis. This is a multilayer adaptive indicator.

What is the Fractal Dimension Index?

The goal of the fractal dimension index is to determine whether the market is trending or in a trading range. It does not measure the direction of the trend. A value less than 1.5 indicates that the price series is persistent or that the market is trending. Lower values of the FDI indicate a stronger trend. A value greater than 1.5 indicates that the market is in a trading range and is acting in a more random fashion.

See here for more info:

Fractal-Dimension-Adaptive SMA (FDASMA) w/ DSL

What is Singular Spectrum Analysis ( SSA )?

Singular spectrum analysis ( SSA ) is a technique of time series analysis and forecasting. It combines elements of classical time series analysis, multivariate statistics, multivariate geometry, dynamical systems and signal processing. SSA aims at decomposing the original series into a sum of a small number of interpretable components such as a slowly varying trend, oscillatory components and a ‘structureless’ noise. It is based on the singular value decomposition ( SVD ) of a specific matrix constructed upon the time series. Neither a parametric model nor stationarity-type conditions have to be assumed for the time series. This makes SSA a model-free method and hence enables SSA to have a very wide range of applicability.

For our purposes here, we are only concerned with the "Caterpillar" SSA . This methodology was developed in the former Soviet Union independently (the ‘iron curtain effect’) of the mainstream SSA . The main difference between the main-stream SSA and the "Caterpillar" SSA is not in the algorithmic details but rather in the assumptions and in the emphasis in the study of SSA properties. To apply the mainstream SSA , one often needs to assume some kind of stationarity of the time series and think in terms of the "signal plus noise" model (where the noise is often assumed to be ‘red’). In the "Caterpillar" SSA , the main methodological stress is on separability (of one component of the series from another one) and neither the assumption of stationarity nor the model in the form "signal plus noise" are required.

"Caterpillar" SSA

The basic "Caterpillar" SSA algorithm for analyzing one-dimensional time series consists of:

Transformation of the one-dimensional time series to the trajectory matrix by means of a delay procedure (this gives the name to the whole technique);

Singular Value Decomposition of the trajectory matrix;

Reconstruction of the original time series based on a number of selected eigenvectors.

This decomposition initializes forecasting procedures for both the original time series and its components. The method can be naturally extended to multidimensional time series and to image processing.

The method is a powerful and useful tool of time series analysis in meteorology, hydrology, geophysics, climatology and, according to our experience, in economics, biology, physics, medicine and other sciences; that is, where short and long, one-dimensional and multidimensional, stationary and non-stationary, almost deterministic and noisy time series are to be analyzed.

Included:

Bar coloring

Alerts

Signals

Loxx's Expanded Source Types

[blackcat] L3 RMI Trading StrategyLevel 3

Background

My view of correct usage of RSI and the relationship between RMI and RSI. A proposed RMI indicator with features is introduced

Descriptions

The Relative Strength Index (RSI) is a technical indicator that many people use. Its focus indicates the strength or weakness of a stock. In the traditional usage of this point, when the RSI is above 50, it is strong, otherwise it is weak. Above 80 is overbought, below 20 is oversold. This is what the textbook says. However, if you follow the principles in this textbook and enter the actual trading, you would lose a lot and win a little! What is the reason for this? When the RSI is greater than 50, that is, a stock enters the strong zone. At this time, the emotions of market may just be brewing, and as a result, you run away and watch others win profit. On the contrary, when RSI<20, that is, a stock enters the weak zone, you buy it. At this time, the effect of losing money is spreading. You just took over the chips that were dumped by the whales. Later, you thought that you had bought at the bottom, but found that you were in half mountainside. According to this cycle, there is a high probability that a phenomenon will occur: if you sell, price will rise, and if you buy, price will fall, who have similar experiences should quickly recall whether their RSI is used in this way. Technical indicators are weapons. It can be either a tool of bull or a sharp blade of bear. Don't learn from dogma and give it away. Trading is a game of people. There is an old saying called “people’s hearts are unpredictable”. Do you really think that there is a tool that can detect the true intentions of people’s hearts 100% of the time?

For the above problems, I suggest that improvements can be made in two aspects (in other words, once the strategy is widely spread, it is only a matter of time before it fails. The market is an adaptive and complex system, as long as it can be fully utilized under the conditions that can be used, it is not easy to use. throw or evolve):

1. RSI usage is the opposite. When a stock has undergone a deep adjustment from a high level, and the RSI has fallen from a high of more than 80 to below 50, it has turned from strong to weak, and cannot be bought in the short term. But when the RSI first moved from a low to a high of 80, it just proved that the stock was in a strong zone. There are funds in the activity, put into the stock pool.

Just wait for RSI to intervene in time when it shrinks and pulls back (before it rises when the main force washes the market). It is emphasized here that the use of RSI should be combined with trading volume, rising volume, and falling volume are all healthy performances. A callback that does not break an important moving average is a confirmed buying point or a second step back on an important moving average is a more certain buying point.

2. The RSI is changed to a more stable and adjustable RMI (Relative Momentum Indicator), which is characterized by an additional momentum parameter, which can not only be very close to the RSI performance, but also adjust the momentum parameter m when the market environment changes to ensure more A good fit for a changing market.

The Relative Momentum Index (RMI) was developed by Roger Altman and described its principles in his article in the February 1993 issue of the journal Technical Analysis of Stocks and Commodities. He developed RMI based on the RSI principle. For example, RSI is calculated from the close to yesterday's close in a period of time compared to the ups and downs, while the RMI is compared from the close to the close of m days ago. Therefore, in principle, when m=1, RSI should be equal to RMI. But it is precisely because of the addition of this m parameter that the RMI result may be smoother than the RSI.

Not much more to say, the below picture: when m=1, RMI and RSI overlap, and the result is the same.

The Shanghai 50 Index is from TradingView (m=1)

The Shanghai 50 Index is from TradingView (m=3)

The Shanghai 50 Index is from TradingView (m=5)

For this indicator function, I also make a brief introduction:

1. 50 is the strength line (white), do not operate offline, pay attention online. 80 is the warning line (yellow), indicating that the stock has entered a strong area; 90 is the lightening line (orange), once it is greater than 90 and a sell K-line pattern appears, the position will be lightened; the 95 clearing line (red) means that selling is at a climax. This is seen from the daily and weekly cycles, and small cycles may not be suitable.

2. The purple band indicates that the momentum is sufficient to hold a position, and the green band indicates that the momentum is insufficient and the position is short.

3. Divide the RMI into 7, 14, and 21 cycles. When the golden fork appears in the two resonances, a golden fork will appear to prompt you to buy, and when the two periods of resonance have a dead fork, a purple fork will appear to prompt you to sell.

4. Add top-bottom divergence judgment algorithm. Top_Div red label indicates top divergence; Bot_Div green label indicates bottom divergence. These signals are only for auxiliary judgment and are not 100% accurate.

5. This indicator needs to be combined with VOL energy, K-line shape and moving average for comprehensive judgment. It is still in its infancy, and open source is published in the TradingView community. A more complete advanced version is also considered for subsequent release (because the K-line pattern recognition algorithm is still being perfected).

Remarks

Feedbacks are appreciated.

STD-Filtered, Adaptive Exponential Hull Moving Average [Loxx]STD-Filtered, Adaptive Exponential Hull Moving Average is a Kaufman Efficiency Ratio Adaptive Hull Moving Average that uses EMA instead of WMA for its computation. I've also added standard deviation stepping to further smooth the signal. Using EMA instead of WMA turns the Hull into what's called the AEHMA. You can read more about the EHMA here: eceweb1.rutgers.edu

What is the traditional Hull Moving Average?

The Hull Moving Average (HMA) attempts to minimize the lag of a traditional moving average while retaining the smoothness of the moving average line. Developed by Alan Hull in 2005, this indicator makes use of weighted moving averages to prioritize more recent values and greatly reduce lag. The resulting average is more responsive and well-suited for identifying entry points.

What is Kaufman's Efficiency Ratio?

The Efficiency Ratio (ER) was first presented by Perry Kaufman in his 1995 book ‘Smarter Trading‘. It is calculated by dividing the price change over a period by the absolute sum of the price movements that occurred to achieve that change. The resulting ratio ranges between 0 and 1 with higher values representing a more efficient or trending market.

The value of the ER ranges between 0 and 1. It has the value of 1 when prices move in the same direction for the full time over which the indicator is calculated, e.g. n bars period. It has a value of 0 when prices are unchanged over the n periods. When prices move in wide swings within the interval, the sum of the denominator becomes very large compared to the numerator and ER approaches zero.

Some uses for ER:

A qualifier for a trend following trade; a trend is considered “persistent” only when RE is above a certain value, e.g. 0.3 or 0.4 .

A filter to screen out choppy stocks/markets, where breakouts are frequently “fakeouts”.

In an adaptive trading system, helping to determine whether to apply a trend following algorithm or a mean reversion algorithm.

It is used in the calculation of Kaufman’s Adaptive Moving Average (KAMA).

How to calculate the Hull Adaptive Moving Average (HAMA)

Find Signal to Noise ratio (SNR)

Normalize SNR from 0 to 1

Calculate adaptive alphas

Apply EMAs

Included

Bar coloring

Signals

Alerts

Loxx's Expanded Source Types

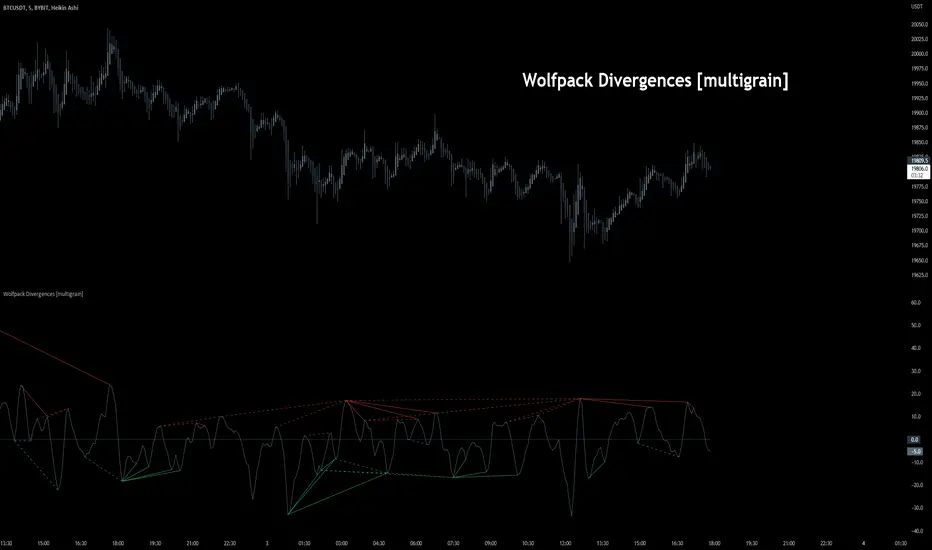

Wolfpack Divergences [multigrain]█ OVERVIEW

A fast and improved divergence finding algorithm that aims to be better than the built-in TradingView divergence algorithm.

█ CONCEPTS

Wolfpack

Wolfpack is an oscillator made popular by darrellfischer1 all the way back in 2017. Since then the Wolfpack oscillator has been utilized by a number of notable strategy/indicator creators. At some point it was realized that the oscillator was simply the Moving Average Crossover Divergence oscillator with the fast and slow length of 3 and 8, respectively. The true significance and reasoning behind these lengths are unknown, however one may surmise that they are chosen due to their relevance as Fibonacci numbers.

Divergences

Divergence is when the price of an asset is moving in the opposite direction of a technical indicator, such as an oscillator, or is moving contrary to other data. Divergence warns that the current price trend may be weakening, and in some cases may lead to the price changing direction.

█ USAGE

Wolfpack

Similar to many other oscillators, when the Wolfpack oscillator reports a value above the zero-line, this indicates a bullish trend in the price. Subsequently, a value below the zero-line indicate a bearish trend in the price.

Divergences

Divergence in technical analysis may signal a major positive or negative price move. A positive divergence occurs when the price of an asset makes a new low while an indicator, such as money flow, starts to climb. Conversely, a negative divergence is when the price makes a new high but the indicator being analyzed makes a lower high.

Nearest Neighbor Extrapolation of Price [Loxx]I wasn't going to post this because I don't like how this calculates by puling in the Open price, but I'm posting it anyway. This does work in it's current form but there is a. better way to do this. I'll revisit this in the future.

Anyway...

The k-Nearest Neighbor algorithm (k-NN) searches for k past patterns (neighbors) that are most similar to the current pattern and computes the future prices based on weighted voting of those neighbors. This indicator finds only one nearest neighbor. So, in essence, it is a 1-NN algorithm. It uses the Pearson correlation coefficient between the current pattern and all past patterns as the measure of distance between them. Also, this version of the nearest neighbor indicator gives larger weights to most recent prices while searching for the closest pattern in the past. It uses a weighted correlation coefficient, whose weight decays linearly from newer to older prices within a price pattern.

This indicator also includes an error window that shows whether the calculation is valid. If it's green and says "Passed", then the calculation is valid, otherwise it'll show a red background and and error message.

Inputs

Npast - number of past bars in a pattern;

Nfut -number of future bars in a pattern (must be < Npast).

lastbar - How many bars back to start forecast? Useful to show past prediction accuracy

barsbark - This prevents Pine from trying to calculate on all past bars

Related indicators

Hodrick-Prescott Extrapolation of Price

Itakura-Saito Autoregressive Extrapolation of Price

Helme-Nikias Weighted Burg AR-SE Extra. of Price

Weighted Burg AR Spectral Estimate Extrapolation of Price

Levinson-Durbin Autocorrelation Extrapolation of Price

Fourier Extrapolator of Price w/ Projection Forecast

Hodrick-Prescott Extrapolation of Price [Loxx]Hodrick-Prescott Extrapolation of Price is a Hodrick-Prescott filter used to extrapolate price.

The distinctive feature of the Hodrick-Prescott filter is that it does not delay. It is calculated by minimizing the objective function.

F = Sum((y(i) - x(i))^2,i=0..n-1) + lambda*Sum((y(i+1)+y(i-1)-2*y(i))^2,i=1..n-2)

where x() - prices, y() - filter values.

If the Hodrick-Prescott filter sees the future, then what future values does it suggest? To answer this question, we should find the digital low-frequency filter with the frequency parameter similar to the Hodrick-Prescott filter's one but with the values calculated directly using the past values of the "twin filter" itself, i.e.

y(i) = Sum(a(k)*x(i-k),k=0..nx-1) - FIR filter

or

y(i) = Sum(a(k)*x(i-k),k=0..nx-1) + Sum(b(k)*y(i-k),k=1..ny) - IIR filter

It is better to select the "twin filter" having the frequency-independent delay Тdel (constant group delay). IIR filters are not suitable. For FIR filters, the condition for a frequency-independent delay is as follows:

a(i) = +/-a(nx-1-i), i = 0..nx-1

The simplest FIR filter with constant delay is Simple Moving Average (SMA):

y(i) = Sum(x(i-k),k=0..nx-1)/nx

In case nx is an odd number, Тdel = (nx-1)/2. If we shift the values of SMA filter to the past by the amount of bars equal to Тdel, SMA values coincide with the Hodrick-Prescott filter ones. The exact math cannot be achieved due to the significant differences in the frequency parameters of the two filters.

To achieve the closest match between the filter values, I recommend their channel widths to be similar (for example, -6dB). The Hodrick-Prescott filter's channel width of -6dB is calculated as follows:

wc = 2*arcsin(0.5/lambda^0.25).

The channel width of -6dB for the SMA filter is calculated by numerical computing via the following equation:

|H(w)| = sin(nx*wc/2)/sin(wc/2)/nx = 0.5

Prediction algorithms:

The indicator features the two prediction methods:

Metod 1:

1. Set SMA length to 3 and shift it to the past by 1 bar. With such a length, the shifted SMA does not exist only for the last bar (Bar = 0), since it needs the value of the next future price Close(-1).

2. Calculate SMA filer's channel width. Equal it to the Hodrick-Prescott filter's one. Find lambda.

3. Calculate Hodrick-Prescott filter value at the last bar HP(0) and assume that SMA(0) with unknown Close(-1) gives the same value.

4. Find Close(-1) = 3*HP(0) - Close(0) - Close(1)

5. Increase the length of SMA to 5. Repeat all calculations and find Close(-2) = 5*HP(0) - Close(-1) - Close(0) - Close(1) - Close(2). Continue till the specified amount of future FutBars prices is calculated.

Method 2:

1. Set SMA length equal to 2*FutBars+1 and shift SMA to the past by FutBars

2. Calculate SMA filer's channel width. Equal it to the Hodrick-Prescott filter's one. Find lambda.

3. Calculate Hodrick-Prescott filter values at the last FutBars and assume that SMA behaves similarly when new prices appear.

4. Find Close(-1) = (2*FutBars+1)*HP(FutBars-1) - Sum(Close(i),i=0..2*FutBars-1), Close(-2) = (2*FutBars+1)*HP(FutBars-2) - Sum(Close(i),i=-1..2*FutBars-2), etc.

The indicator features the following inputs:

Method - prediction method

Last Bar - number of the last bar to check predictions on the existing prices (LastBar >= 0)

Past Bars - amount of previous bars the Hodrick-Prescott filter is calculated for (the more, the better, or at least PastBars>2*FutBars)

Future Bars - amount of predicted future values

The second method is more accurate but often has large spikes of the first predicted price. For our purposes here, this price has been filtered from being displayed in the chart. This is why method two starts its prediction 2 bars later than method 1. The described prediction method can be improved by searching for the FIR filter with the frequency parameter closer to the Hodrick-Prescott filter. For example, you may try Hanning, Blackman, Kaiser, and other filters with constant delay instead of SMA.

Related indicators

Itakura-Saito Autoregressive Extrapolation of Price

Helme-Nikias Weighted Burg AR-SE Extra. of Price

Weighted Burg AR Spectral Estimate Extrapolation of Price

Levinson-Durbin Autocorrelation Extrapolation of Price

Fourier Extrapolator of Price w/ Projection Forecast

Real-Fast Fourier Transform of Price w/ Linear Regression [Loxx]Real-Fast Fourier Transform of Price w/ Linear Regression is a indicator that implements a Real-Fast Fourier Transform on Price and modifies the output by a measure of Linear Regression. The solid line is the Linear Regression Trend of the windowed data, The green/red line is the Real FFT of price.

What is the Discrete Fourier Transform?

In mathematics, the discrete Fourier transform (DFT) converts a finite sequence of equally-spaced samples of a function into a same-length sequence of equally-spaced samples of the discrete-time Fourier transform (DTFT), which is a complex-valued function of frequency. The interval at which the DTFT is sampled is the reciprocal of the duration of the input sequence. An inverse DFT is a Fourier series, using the DTFT samples as coefficients of complex sinusoids at the corresponding DTFT frequencies. It has the same sample-values as the original input sequence. The DFT is therefore said to be a frequency domain representation of the original input sequence. If the original sequence spans all the non-zero values of a function, its DTFT is continuous (and periodic), and the DFT provides discrete samples of one cycle. If the original sequence is one cycle of a periodic function, the DFT provides all the non-zero values of one DTFT cycle.

What is the Complex Fast Fourier Transform?

The complex Fast Fourier Transform algorithm transforms N real or complex numbers into another N complex numbers. The complex FFT transforms a real or complex signal x in the time domain into a complex two-sided spectrum X in the frequency domain. You must remember that zero frequency corresponds to n = 0, positive frequencies 0 < f < f_c correspond to values 1 ≤ n ≤ N/2 −1, while negative frequencies −fc < f < 0 correspond to N/2 +1 ≤ n ≤ N −1. The value n = N/2 corresponds to both f = f_c and f = −f_c. f_c is the critical or Nyquist frequency with f_c = 1/(2*T) or half the sampling frequency. The first harmonic X corresponds to the frequency 1/(N*T).

The complex FFT requires the list of values (resolution, or N) to be a power 2. If the input size if not a power of 2, then the input data will be padded with zeros to fit the size of the closest power of 2 upward.

What is Real-Fast Fourier Transform?

Has conditions similar to the complex Fast Fourier Transform value, except that the input data must be purely real. If the time series data has the basic type complex64, only the real parts of the complex numbers are used for the calculation. The imaginary parts are silently discarded.

Inputs:

src = source price

uselreg = whether you wish to modify output with linear regression calculation

Windowin = windowing period, restricted to powers of 2: "4", "8", "16", "32", "64", "128", "256", "512", "1024", "2048"

Treshold = to modified power output to fine tune signal

dtrendper = adjust regression calculation

barsback = move window backward from bar 0

mutebars = mute bar coloring for the range

Further reading:

Real-valued Fast Fourier Transform Algorithms IEEE Transactions on Acoustics, Speech, and Signal Processing, June 1987

Related indicators utilizing Fourier Transform

Fourier Extrapolator of Variety RSI w/ Bollinger Bands

Fourier Extrapolation of Variety Moving Averages

Fourier Extrapolator of Price w/ Projection Forecast

Phase Accumulation, Smoothed Williams %R Histogram [Loxx]Phase Accumulation, Smoothed Williams %R Histogram is a Williams %R indicator using dynamic inputs from Ehlers Phase Accumulation Dominant Cycle Period Algorithm. This indicator includes alerts and signals and is in a smoothed histogram form. The version of Phase Accumulation in this indicator is a modified form of of Ehlers algorithm to allow for better smoothing and cycle length selection.

What is Williams %R?

Williams %R , also known as the Williams Percent Range, is a type of momentum indicator that moves between 0 and -100 and measures overbought and oversold levels. The Williams %R may be used to find entry and exit points in the market. The indicator is very similar to the Stochastic oscillator and is used in the same way. It was developed by Larry Williams and it compares a stock’s closing price to the high-low range over a specific period, typically 14 days or periods.

What is Phase Accumulation?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included:

-Toggle on/off bar coloring

-Toggle on/off signals

-Alerts long/short

-Loxx's Expanded Source Types Library

Jurik DMX Histogram [Loxx]Jurik DMX Histogram is the ultra-smooth, low lag version of your classic DMI indicator.

What is the directional movement index?

The directional movement index (DMI) is an indicator developed by J. Welles Wilder in 1978 that identifies in which direction the price of an asset is moving. The indicator does this by comparing prior highs and lows and drawing two lines: a positive directional movement line (+DI) and a negative directional movement line (-DI). An optional third line, called the average directional index (ADX), can also be used to gauge the strength of the uptrend or downtrend.

When +DI is above -DI, there is more upward pressure than downward pressure in the price. Conversely, if -DI is above +DI, then there is more downward pressure on the price. This indicator may help traders assess the trend direction. Crossovers between the lines are also sometimes used as trade signals to buy or sell.

What is Jurik Volty used in the Juirk Filter?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman’s adaptive moving average ( KAMA ) and Tushar Chande’s variable index dynamic average ( VIDYA ) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index ( RSI ), commodity channel index ( CCI ), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

Included

- Toggle on/off bar coloring

Adaptive, Jurik-Filtered, JMA/DWMA MACD [Loxx]Adaptive, Jurik-Filtered, JMA/DWMA MACD is MACD oscillator with a twist. The traditional calculation of MACD is the between two EMAs of price. This traditional approach yields a very noisy and lagged signal. To solve this problem, JMA/DWMA MACD uses the difference between adaptive Juirk-Filtered price and adaptive DWMA to yield a marked improvement over traditional MACD.

What is JMA / DWMA oscillator (MACD)?

Of all the different combinations of moving average filters to use for a MACD oscillator, we prefer using the JMA - DWMA combination.

JMA is ideal for the fast moving average line because it is quick to respond to reversals, is smooth and can be set to have no overshoot. DWMA (double weighted moving average) is ideal for the slower line as is tends to delay reversing direction until JMA crosses it.

What is Jurik Volty used in the Juirk Filter?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman’s adaptive moving average ( KAMA ) and Tushar Chande’s variable index dynamic average ( VIDYA ) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index ( RSI ), commodity channel index ( CCI ), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

Included

- Toggle on/off bar coloring

Adaptive, Jurik-Filtered, Floating RSI [Loxx]Adaptive, Jurik-Filtered, Floating RSI is an adaptive RSI indicator that smooths the RSI signal with a Jurik Filter.

This indicator contains three different types of RSI. They are following.

Wilders' RSI:

The Relative Strength Index ( RSI ) is a well versed momentum based oscillator which is used to measure the speed (velocity) as well as the change (magnitude) of directional price movements. Essentially RSI , when graphed, provides a visual mean to monitor both the current, as well as historical, strength and weakness of a particular market. The strength or weakness is based on closing prices over the duration of a specified trading period creating a reliable metric of price and momentum changes. Given the popularity of cash settled instruments (stock indexes) and leveraged financial products (the entire field of derivatives); RSI has proven to be a viable indicator of price movements.

RSX RSI:

RSI is a very popular technical indicator, because it takes into consideration market speed, direction and trend uniformity. However, the its widely criticized drawback is its noisy (jittery) appearance. The Jurk RSX retains all the useful features of RSI , but with one important exception: the noise is gone with no added lag.

Rapid RSI:

Rapid RSI Indicator, from Ian Copsey's article in the October 2006 issue of Stocks & Commodities magazine.

RapidRSI resembles Wilder's RSI , but uses a SMA instead of a WilderMA for internal smoothing of price change accumulators.

This indicator also uses adaptive cycles to calculate input lengths

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman’s adaptive moving average ( KAMA ) and Tushar Chande’s variable index dynamic average ( VIDYA ) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index ( RSI ), commodity channel index ( CCI ), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.