Relative Strength (RS) By @Byte2Bull📈 Relative Strength (RS) By @Byte2Bull

📌 Overview

This indicator plots a Relative Strength (RS) line that compares the performance of the chart symbol to any benchmark symbol (index, ETF, or stock). By comparing the stock’s price movement to that of the benchmark, this tool highlights whether a stock is outperforming or underperforming the market.

RS value = (Price of symbol / Price of benchmark) × 100

It highlights hidden leaders and emerging strength through dynamic line plots, customizable moving average, and powerful new high detection features, enabling more informed trading decisions.

🛠 Key Features

⦿ Custom Benchmark Selection

Compare any stock with your chosen benchmark (default: NSE:NIFTYMIDSML400), such as NIFTY50, BANKNIFTY, or sector indices.

⦿ Relative Strength Line with Dynamic Coloring

Green when RS is above its moving average (strength/outperformance).

Red when RS is below its moving average (weakness/underperformance).

⦿ Configurable Moving Average

Apply either EMA or SMA over RS with customizable length. This helps smooth out volatility and provides a clear reference trend.

⦿ New High Detection

Marks when RS makes a new high.

Highlights when RS makes a new high before price does → a powerful early signal of hidden strength.

⦿ MA Crossover

Optional marker for when RS crosses above its moving average, signaling potential start of leadership.

⦿ Visual Enhancements

Adjustable line thickness.

Fill area between RS and its MA with green/red shading for quick interpretation.

Customizable colors for all key signals.

⦿ Built-in Alerts

Set alerts for:

RS New High

RS New High Before Price

Bullish MA Crossover

🎯 How to Use

⦿ Identify Market Leaders:

A stock with RS consistently above its MA is likely leading the market.

⦿ Spot Early Strength:

If RS makes a new high before the stock price, it may signal strong relative demand — often preceding breakouts.

⦿ Filter Weakness:

Stocks with RS below the MA are lagging and may be best avoided during bullish phases.

⦿ Combine with Price Action & Volume:

RS works best alongside price breakouts, trend analysis, and volume confirmations.

Comparação de Força Relativa

Relative Performance Indicator - TrendSpider StyleRelative Performance Indicator - TrendSpider Style

📈 Overview

This Relative Performance (RP) indicator measures how your stock is performing compared to a benchmark index, displayed as a percentile ranking from 0-100. Based on TrendSpider's methodology, it answers the critical question: "Is this stock a leader or a laggard?"

Unlike simple ratio charts, this indicator uses percentile ranking to normalize relative performance, making it easy to identify when a stock is showing exceptional strength (>80) or concerning weakness (<20) compared to its historical relationship with the benchmark.

✨ Key Features

Three Calculation Modes:

Quarterly: 3-month relative performance for swing trading

Yearly: Weighted 4-quarter performance for position trading

TechRank: Composite of 6 technical indicators for multi-factor analysis

Clean Visual Design:

Green fills above 80 (strong outperformance)

Red fills below 20 (significant underperformance)

Dotted median line at 50 for quick reference

Current value label for instant reading

Flexible Benchmarks:

Compare against major indices (SPY, QQQ, IWM)

Sector ETFs for within-sector analysis

Custom symbols for specialized comparisons

Built-in Alerts:

Strong performance zone entry (>80)

Weak performance zone entry (<20)

Median crossovers (50 level)

📊 How To Use

Buy Signals:

RP crosses above 80: Stock entering leadership status

RP holding above 60: Maintaining relative strength

RP rising while price consolidating: Accumulation phase

Sell/Avoid Signals:

RP drops below 50: Losing relative strength

RP below 20: Significant underperformance

RP falling while price rising: Bearish divergence

Sector Rotation:

Compare multiple assets to find strongest sectors

Rotate into high RP assets (>70)

Exit low RP positions (<30)

🎯 Reading The Values

80-100: Exceptional outperformance - Strong buy/hold

60-80: Moderate outperformance - Hold positions

40-60: Market perform - No edge

20-40: Underperformance - Caution/reduce

0-20: Severe underperformance - Avoid/exit

⚙️ Calculation Method

Calculates percentage performance of both your stock and the benchmark

Finds the performance differential

Ranks this differential against historical values using percentile analysis

Normalizes to 0-100 scale for easy interpretation

This percentile approach adapts to different market conditions and volatility regimes, providing consistent signals whether in trending or choppy markets.

💡 Pro Tips

For Growth Stocks: Use quarterly mode with QQQ as benchmark

For Value Stocks: Use yearly mode with SPY as benchmark

For Small Caps: Compare against IWM, not SPY

For Sector Analysis: Use sector ETFs (XLK, XLF, XLE, etc.)

Combine with Price Action: High RP + price breakout = powerful signal

⚠️ Important Notes

RP is relative, not absolute - stocks can fall with high RP if the market falls harder

Choose appropriate benchmarks for meaningful comparisons

Best used in conjunction with price action and volume analysis

Historical lookback period affects sensitivity (adjustable in settings)

🔧 Customization

Fully customizable visual settings, thresholds, calculation periods, and smoothing options. Adjust the normalization lookback period (default 252 days) to fine-tune sensitivity to your trading timeframe.

📌 Credit

Inspired by TrendSpider's Relative Performance implementation, adapted for TradingView with enhanced customization options and Pine Script v6 optimization.

Tags to include: relativeperformance, relativestrength, percentile, ranking, sectorrotation, benchmark, outperformance, trendspider, marketbreadth, strengthindicator

Category: Momentum Indicators / Trend Analysis

Feel free to modify this description to match your style or add any specific points you want to emphasize!

RFSIRFSI (Relative Force Strength Index) is a technical indicator that measures the relative strength of an asset compared to a benchmark (default: SPY - S&P 500 ETF). It helps identify performance divergences and generate entry/exit signals based on crossovers.

RFSI (Relative Force Strength Index) est un indicateur technique qui mesure la force relative d'un actif par rapport à un benchmark (par défaut : SPY - ETF S&P 500). Il permet d'identifier les divergences de performance et de générer des signaux d'entrée/sortie basés sur des croisements.

Multiple Relative Strength IndicatorThis indicator is used to display multiple Relative strength of a stock compared with another.

Default value for the first Relative strength period is 55

Default value for the second Relative strength period is 21

Default value for the comparable Index is CNX500

You can add the sectorial index for sector comparison

KRX RS OverlayKRX RS Overlay (Manual, Pine v6) (한국어 설명 아래에)

What it does

Plots a Relative Strength (RS) line of the current symbol versus a selected Korean market index on the price chart (overlay). RS is computed as Close(symbol) / Close(benchmark) and rebased to 100 N bars ago for easy comparison. An SMA of RS is included for signal smoothing.

Benchmarks (manual selection only)

• KOSPI (KRX:KOSPI) — default

• KOSDAQ (KRX:KOSDAQ)

• KOSPI200 (KRX:KOSPI200)

• KOSDAQ150 (KRX:KOSDAQ150)

Inputs

• Benchmark: choose one of the four indices above (default: KOSPI)

• Rebase N bars ago to 100: sets the normalization point (e.g., 252 ≈ 1 trading year on daily)

• RS SMA length: smoothing period for the RS line

• Show 100 base line: toggle the reference line at 100

How to read

• RS rising → the symbol is outperforming the selected index.

• RS above RS-SMA and sloping up → strengthening leadership vs. the benchmark.

• RS crossing above RS-SMA → momentum-style confirmation (an alert is provided).

Tips

• Works on any timeframe; the benchmark is requested on the same timeframe.

• If the RS line scale conflicts with price, place the indicator on the Left scale (Chart Settings → Scales) or set the series to use the left axis.

Notes

• This script is manual only (no auto index detection).

• Educational use; not financial advice.

⸻

KRX RS 오버레이 (수동, Pine v6)

기능

현재 종목을 선택한 한국 지수와 비교한 상대강도(RS) 라인을 가격 차트 위(오버레이)에 표시합니다. RS는 종목 종가 / 지수 종가로 계산하며, 비교를 쉽게 하기 위해 N봉 전 = 100으로 리베이스합니다. 신호 완화를 위해 RS의 SMA도 함께 제공합니다.

벤치마크(수동 선택만 지원)

• KOSPI (KRX:KOSPI) — 기본값

• KOSDAQ (KRX:KOSDAQ)

• KOSPI200 (KRX:KOSPI200)

• KOSDAQ150 (KRX:KOSDAQ150)

입력값

• Benchmark: 위 4개 지수 중 선택(기본: KOSPI)

• Rebase N bars ago to 100: 리베이스 기준(일봉 252 ≈ 1년)

• RS SMA length: RS 스무딩 기간

• Show 100 base line: 100 기준선 표시 여부

해석 가이드

• RS 상승 → 선택 지수 대비 초과성과.

• RS가 RS-SMA 위 & 우상향 → 벤치마크 대비 리더십 강화.

• RS가 RS-SMA 상향 돌파 → 모멘텀 확인(알림 제공).

팁

• 모든 타임프레임에서 동작하며, 지수도 동일 타임프레임으로 요청됩니다.

• 가격 축과 스케일이 겹치면 왼쪽 스케일로 표시하도록 설정하세요(차트 설정 → Scales).

유의사항

• 자동 지수 판별 기능은 포함하지 않았습니다(수동 전용).

Relative Strength Comparison-Num_Den_inputsThis RSC chart lets you give inputs for both Numerator and Denominator

Relative Strength Comparison-NewShRelative Strength Comparison Script created by Shahbaz on 19th Sep 2025

RSI MA Cross + Divergence Signal (V2) Core Logic

RSI + Moving Average

The script calculates a standard RSI (default 14).

It then overlays a moving average (SMA/EMA/WMA, default 9).

When RSI crosses above its MA → bullish momentum.

When RSI crosses below its MA → bearish momentum.

Divergence Filter

Signals are only valid if there’s confirmed divergence:

Bullish divergence: Price makes a lower low, RSI makes a higher low.

Bearish divergence: Price makes a higher high, RSI makes a lower high.

Overbought / Oversold Filter

Optional extra:

Bullish signals only valid if RSI ≤ 30 (oversold).

Bearish signals only valid if RSI ≥ 70 (overbought).

This ensures signals happen in “stretched” conditions.

Risk & Trade Management

Entries taken only when all conditions align.

Exits can be managed with ATR stops, partial take-profits, breakeven moves, and trailing stops (we coded these in the strategy version).

Cooldown, session filters, and daily loss guard to keep risk tight.

🔹 Strengths

✅ High selectivity: Combining RSI cross + divergence + OB/OS means signals are rare but higher quality.

✅ Great at catching reversals: Divergence highlights where price may be running out of steam.

✅ Risk management baked in: ATR stops + partial exits smooth out equity curve.

✅ Works across markets: ES, FX, crypto — anywhere RSI divergences are respected.

✅ Flexible: You can loosen/tighten filters depending on aggressiveness.

🔹 Weaknesses

❌ Lag from pivots: Divergence only confirms after a few bars → you enter late sometimes.

❌ Choppy in ranges: In sideways markets, RSI divergences appear often and whipsaw.

❌ Filters reduce signals: With all filters ON (divergence + OB/OS + trend + session), signals can be very rare — may under-trade.

❌ Not standalone: Needs higher-timeframe context (trend, liquidity pools) to avoid counter-trend entries.

🔹 Best Ways to Trade It

Use Higher Timeframe Bias

Run the strategy on 15m/1H, but only trade in direction of higher timeframe trend (e.g., 4H EMA).

Example: If daily is bullish → only take bullish divergences.

Pair With Structure

Look for signals at key zones: HTF support/resistance, VWAP, or FVGs.

Divergence + RSI cross inside an FVG is a strong entry trigger.

Adjust OB/OS for Volatility

For crypto/FX: use 35/65 instead of 30/70 (markets trend harder).

For ES/S&P: 30/70 works fine.

Risk Management Is King

Use partial exits: take profit at 1R, trail rest.

Size by % of equity (we coded this into the strategy).

Avoid News Spikes

Divergences break down around CPI, NFP, Fed announcements — stay flat.

🔹 When It Shines

Trending markets that make extended pushes → clean divergences.

Reversal zones (oversold → bullish bounce, overbought → bearish fade).

Swing trading (15m–4H) — less noise than 1m/5m scalping.

🔹 When to Avoid

Low volatility chop → lots of false divergences.

During high-impact news → RSI swings wildly.

In strong one-way trends without pullbacks — divergence keeps calling tops/bottoms too early.

✅ Summary:

This is a reversal-focused RSI divergence strategy with strict filters. It’s powerful when combined with higher-timeframe bias + structure confluence, but weak if traded blindly in choppy or news-driven conditions. Best to treat it as a precision entry trigger, not a full system — layer it on top of your FVG/ORB framework for maximum edge.

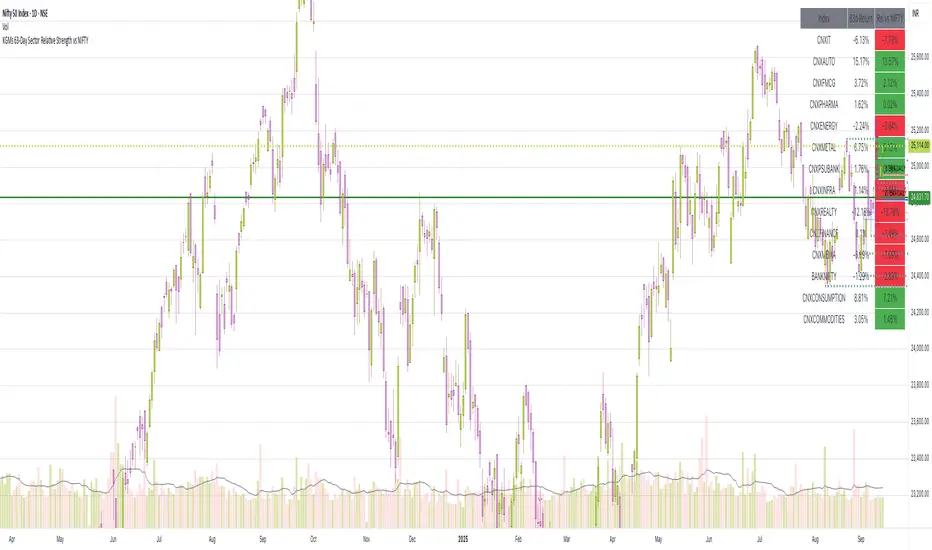

63-Day Sector Relative Strength vs NIFTYThis script calculates and displays the 63-day returns of major NSE sectoral indices and their relative strength versus the NIFTY 50.

It,

Covered Indices: CNXIT, CNXAUTO, CNXFMCG, CNXPHARMA, CNXENERGY, CNXMETAL, CNXPSUBANK, CNXINFRA, CNXREALTY, CNXFINANCE, CNXMEDIA, BANKNIFTY, CNXCONSUMPTION, CNXCOMMODITIES

How to use this: Quickly identify which sectors are outperforming or underperforming relative to the NIFTY over the past 63 trading sessions (approx. 3 months).

ETFs Sector PerformanceDisplays a table of the Top 8 performing ETFs over a selected period (1M / 2M / 3M / 6M) to quickly identify industry strength.

Pre-Set Universe (39 ETFs)

ITA — iShares U.S. Aerospace & Defense ETF

DBA — Invesco DB Agriculture Fund

BOTZ — Global X Robotics & Artificial Intelligence ETF

JETS — U.S. Global Jets ETF

XLB — Materials Select Sector SPDR Fund

XBI — SPDR S&P Biotech ETF

PKB — Invesco Dynamic Building & Construction ETF

ICLN — iShares Global Clean Energy ETF

SKYY — First Trust Cloud Computing ETF

DBC — Invesco DB Commodity Index Tracking Fund

XLY — Consumer Discretionary Select Sector SPDR Fund

XLP — Consumer Staples Select Sector SPDR Fund

BLOK — Amplify Transformational Data Sharing ETF

KARS — KraneShares Electric Vehicles & Future Mobility ETF

XLE — Energy Select Sector SPDR Fund

ESPO — VanEck Video Gaming and eSports ETF

XLF — Financial Select Sector SPDR Fund

PBJ — Invesco Dynamic Food & Beverage ETF

ITB — iShares U.S. Home Construction ETF

XLI — Industrial Select Sector SPDR Fund

PAVE — Global X U.S. Infrastructure Development ETF

PEJ — Invesco Dynamic Leisure & Entertainment ETF

LIT — Global X Lithium & Battery Tech ETF

IHI — iShares U.S. Medical Devices ETF

XME — SPDR S&P Metals & Mining ETF

FCG — First Trust Natural Gas ETF

URA — Global X Uranium ETF

PPH — VanEck Pharmaceutical ETF

QTUM — Defiance Quantum Computing & Machine Learning ETF

IYR — iShares U.S. Real Estate ETF

XRT — SPDR S&P Retail ETF

SOXX — iShares Semiconductor ETF

BOAT — SonicShares Global Shipping ETF

IGV — iShares Expanded Tech-Software Sector ETF

TAN — Invesco Solar ETF

SLX — VanEck Steel ETF

IYZ — iShares U.S. Telecommunications ETF

IYT — iShares U.S. Transportation ETF

XLU — Utilities Select Sector SPDR Fund

Dual Relative Strength (Fast & Slow, Single Baseline)Dual-Period RS Setup (Fast + Slow)

1. Fast RS (Early Leadership)

• Indicator: Relative Strength (by modhelius)

• Comparative Symbol: NIFTY

• Period: 26 weeks (~6 months)

• Purpose: Detects early shifts in relative strength before price fully confirms.

⸻

2. Slow RS (Confirmation)

• Add the same indicator again.

• Comparative Symbol: NIFTY

• Period: 52 weeks (1 year)

• Purpose: Confirms sustained leadership. Helps filter noise & false positives.

Dual Relative Strength (vs NIFTY) Nikrun1. Fast RS (Early Leadership)

• Indicator: Relative Strength (by modhelius)

• Comparative Symbol: NIFTY

• Period: 26 weeks (~6 months)

• Purpose: Detects early shifts in relative strength before price fully confirms.

⸻

2. Slow RS (Confirmation)

• Add the same indicator again.

• Comparative Symbol: NIFTY

• Period: 52 weeks (1 year)

• Purpose: Confirms sustained leadership. Helps filter noise & false positives.

⸻

3. Visuals

• Style tip:

• Make RS(26) = blue line (fast, responsive).

• Make RS(52) = thicker black/green line (slow, authority).

• Keep zero line visible so you instantly see outperformance/underperformance.

⸻

RS Alpha by The Noiseless TraderRS Alpha by The Noiseless Trader plots a clean, benchmark‑relative strength line for any symbol and (optionally) a mean line to assess trend and momentum in relative performance. It’s designed for uncluttered, professional RS analysis and works across any timeframe.

Compare any symbol vs a benchmark (default: NSE:NIFTY).

Optional log‑normalized RS for return‑aware comparisons.

Optional RS Mean with trend coloring (rising/falling).

Optional RS Trend zero‑line coloring based on short‑range slope.

Lightweight alerts for rising/falling RS mean.

Tip: Use RS to identify leaders (RS > 0 with rising mean) and laggards (RS < 0 with falling mean), then align setups with your price action rules.

Reading the indicator

Leadership: RS > 0 and RS Mean rising → outperformance vs benchmark.

Weakness: RS < 0 and RS Mean falling → underperformance vs benchmark.

Inflections: Watch RS crossing above/below its Mean for early shifts.

Zero‑line context: With RS Trend on, the zero line subtly reflects short‑term slope (green for positive, maroon for negative).

Alerts

Rising Strength – RS Mean turning/remaining upward.

Declining Strength – RS Mean turning/remaining downward.

(Use these as context; execute entries on your price‑action rules.)

Best practices

Pair RS with your trend/structure rules (e.g., higher highs + RS leadership).

For sectors/baskets, keep the Comparative Symbol consistent to rank peers.

Log‑normalized RS helps when comparing assets with very different volatilities or large base effects.

Test multiple length and Mean settings; 60 is a balanced default for swing/positional work.

Credits

Original concept & code: © bharatTrader

Modifications & refinements: The Noiseless Trader

Dual Custom Index with SpreadDual Custom Index with Spread

Create powerful custom indices from any instruments and analyze their relative strength dynamics

Overview

This advanced indicator allows you to build two completely customizable indices from your choice of instruments and analyze their spread relationship. Perfect for inter-market analysis, sector rotation strategies, currency strength comparisons, and sophisticated relative performance studies.

Key Features

🔧 Fully Customizable Index Construction

Build each index from up to 6 instruments with individual weightings

Enable/disable instruments on the fly without losing settings

Automatic weight validation ensures mathematically accurate calculations

Invert functionality for instruments that move opposite to index strength

📊 Advanced ADX-Based Methodology

Uses sophisticated ADX +DI/-DI directional bias calculations

Normalized bias calculation for consistent scaling across different instruments

Optimized default settings for intraday trading with full customization options

Professional-grade smoothing and filtering options

📈 Dual Analysis Modes

Difference Mode: Shows absolute strength difference (Index1 - Index2)

Ratio Mode: Shows relative performance ratio (Index1 / Index2)

Additional spread smoothing for cleaner signals

🎨 Professional Display Options

Custom labels with full color, size, and positioning control

Dynamic "Follow Line" labels that move with your data

Static corner positioning for reference displays

Clean error messaging and validation feedback

Use Cases

Gold Trading: Create gold strength vs USD strength indices for precise market timing

Sector Analysis: Compare technology vs financial sector strength for rotation strategies

Currency Strength: Build custom currency baskets for advanced forex analysis

Commodity Spreads: Analyze relative strength between different commodity groups

Regional Markets: Compare strength between different geographical market indices

Crypto Analysis: Track relative performance between different cryptocurrency sectors

Technical Specifications

Instruments per Index: Up to 6 with individual enable/disable

Weight Validation: Automatic 100% total weight enforcement

Calculation Method: ADX-based directional bias with trend strength weighting

Smoothing Options: Multiple levels of customizable smoothing

Error Handling: Professional validation with clear user feedback

Optimization Tips

Intraday Trading: Use DI Length 3-7 for faster response

Daily Analysis: Use DI Length 10-14 for smoother signals

Noisy Markets: Increase Final Smoothing for cleaner signals

Trending Markets: Lower smoothing values for faster reaction

Perfect for traders who need sophisticated inter-market analysis tools beyond standard indicators. Whether you're analyzing gold vs dollar dynamics, sector rotation opportunities, or custom currency strength relationships, this indicator provides institutional-grade analysis capabilities with complete customization flexibility.

Awesome Indicator# Moving Average Ribbon with ADR% - Complete Trading Indicator

## Overview

The **Moving Average Ribbon with ADR%** is a comprehensive technical analysis indicator that combines multiple analytical tools to provide traders with a complete picture of price trends, volatility, relative performance, and position sizing guidance. This multi-faceted indicator is designed for both swing and positional traders looking for data-driven entry and exit signals.

## Key Components

### 1. Moving Average Ribbon System

- **4 Customizable Moving Averages** with default periods: 13, 21, 55, and 189

- **Multiple MA Types**: SMA, EMA, SMMA (RMA), WMA, VWMA

- **Color-coded visualization** for easy trend identification

- **Flexible configuration** allowing users to modify periods, types, and colors

### 2. Average Daily Range Percentage (ADR%)

- Calculates the average daily volatility as a percentage

- Uses a 20-period simple moving average of (High/Low - 1) * 100

- Helps traders understand the stock's typical daily movement range

- Essential for position sizing and stop-loss placement

### 3. Volume Analysis (Up/Down Ratio)

- Analyzes volume distribution over the last 55 periods

- Calculates the ratio of volume on up days vs down days

- Provides insight into buying vs selling pressure

- Values > 1 indicate more buying volume, < 1 indicate more selling volume

### 4. Absolute Relative Strength (ARS)

- **Dual timeframe analysis** with customizable reference points

- **High ARS**: Performance relative to benchmark from a high reference point (default: Sep 27, 2024)

- **Low ARS**: Performance relative to benchmark from a low reference point (default: Apr 7, 2025)

- Uses NSE:NIFTY as default comparison symbol

- Color-coded display: Green for outperformance, Red for underperformance

### 5. Relative Performance Table

- **5 timeframes**: 1 Week, 1 Month, 3 Months, 6 Months, 1 Year

- Shows stock performance **relative to benchmark index**

- Formula: (Stock Return - Index Return) for each period

- **Color coding**:

- Lime: >5% outperformance

- Yellow: -5% to +5% relative performance

- Red: <-5% underperformance

### 6. Dynamic Position Allocation System

- **6-factor scoring system** based on price vs EMAs (21, 55, 189)

- Evaluates:

- Price above/below each EMA

- EMA alignment (21>55, 55>189, 21>189)

- **Allocation recommendations**:

- 100% allocation: Score = 6 (all bullish signals)

- 75% allocation: Score = 4

- 50% allocation: Score = 2

- 25% allocation: Score = 0

- 0% allocation: Score = -2, -4, -6 (bearish signals)

## Display Tables

### Performance Table (Top Right)

Shows relative performance vs benchmark across multiple timeframes with intuitive color coding for quick assessment.

### Metrics Table (Bottom Right)

Displays key statistics:

- **ADR%**: Average Daily Range percentage

- **U/D**: Up/Down volume ratio

- **Allocation%**: Recommended position size

- **High ARS%**: Relative strength from high reference

- **Low ARS%**: Relative strength from low reference

## How to Use This Indicator

### For Trend Analysis

1. **Moving Average Ribbon**: Look for price above ascending MAs for bullish trends

2. **MA Alignment**: Bullish when shorter MAs are above longer MAs

3. **Color coordination**: Use consistent color scheme for quick visual analysis

### For Entry/Exit Timing

1. **Performance Table**: Enter when showing consistent outperformance across timeframes

2. **Volume Analysis**: Confirm entries with U/D ratio > 1.5 for strong buying

3. **ARS Values**: Look for positive ARS readings for relative strength confirmation

### For Position Sizing

1. **Allocation System**: Use the recommended allocation percentage

2. **ADR% Consideration**: Adjust position size based on volatility

3. **Risk Management**: Lower allocation in high ADR% stocks

### For Risk Management

1. **ADR% for Stop Loss**: Set stops at 1-2x ADR% below entry

2. **Relative Performance**: Reduce positions when consistently underperforming

3. **Volume Confirmation**: Be cautious when U/D ratio deteriorates

## Best Practices

### Timeframe Recommendations

- **Intraday**: Use lower MA periods (5, 13, 21, 55)

- **Swing Trading**: Default settings work well (13, 21, 55, 189)

- **Position Trading**: Consider higher periods (21, 50, 100, 200)

### Market Conditions

- **Trending Markets**: Focus on MA alignment and relative performance

- **Sideways Markets**: Rely more on ADR% for range trading

- **Volatile Markets**: Reduce allocation percentage regardless of signals

### Customization Tips

1. Adjust reference dates for ARS calculation based on significant market events

2. Change comparison symbol to sector-specific indices for better relative analysis

3. Modify MA periods based on your trading style and market characteristics

## Technical Specifications

- **Version**: Pine Script v6

- **Overlay**: Yes (plots on price chart)

- **Real-time Updates**: Yes

- **Data Requirements**: Minimum 252 bars for complete calculations

- **Compatible Timeframes**: All standard timeframes

## Limitations

- Performance calculations require sufficient historical data

- ARS calculations depend on selected reference dates

- Volume analysis may be less reliable in low-volume stocks

- Relative performance is only as good as the chosen benchmark

This indicator is designed to provide a comprehensive analysis framework rather than simple buy/sell signals. It's recommended to use this in conjunction with your overall trading strategy and risk management rules.

EMA72 com Difusor - Cor Dinâmica e Espessuras Ajustadas17 EMA

72 EMA (with diffuser included, green signals buy, red signals sell)

72 EMA on the weekly chart

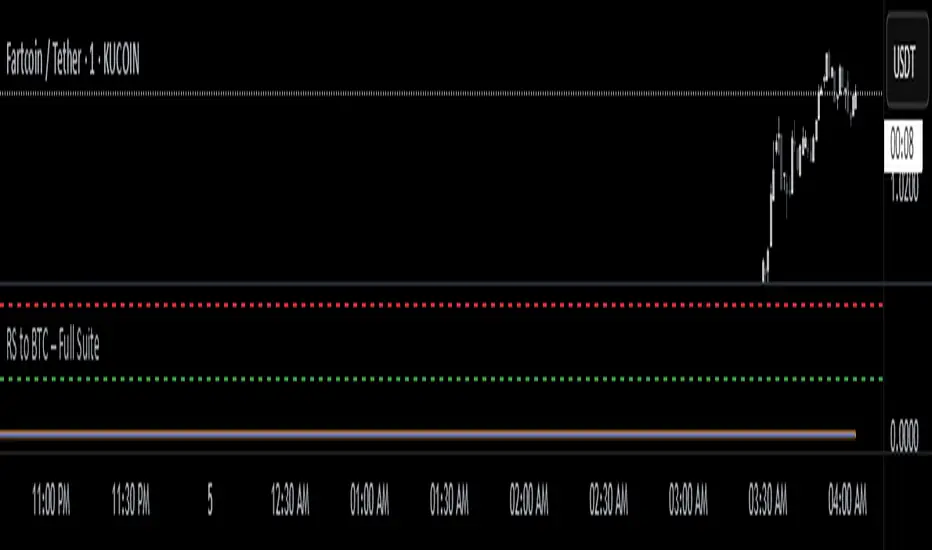

RS to BTC – EYASU V1RS to BTC – Full Suite

📝 Description:

This script tracks the relative strength of any coin against Bitcoin (RSBTC) in real-time. It is designed for altcoin traders who want to identify which coins are outperforming or underperforming BTC across multiple timeframes.

Features:

📈 RSBTC Line: Real-time plot of the altcoin’s price divided by BTC price

🟦 RSBTC Moving Average: Smooths the RS line to help identify trends

🔵 RSBTC RSI (Hidden by default): Highlights momentum of RS to detect overbought/oversold zones

🚨 Alerts: Set alerts for RSBTC crossing its moving average and RSI levels

Ideal for:

Spotting early altcoin breakouts

Timing entries/exits based on BTC-relative performance

Filtering for strong/weak coins before macro news

📱 Fully mobile compatible. Load it on any USDT chart — it auto-detects BTC and gives RS instantly.

Created by: @Eyasustock

License: Mozilla Public License 2.0

D2E (Distance to EMA)D2E (Distance to EMA) measures how far price is from its daily Exponential Moving Average (EMA), both as a percentage and in dollar terms. It helps traders quickly assess how extended price is from its mean, making it useful for spotting overbought/oversold conditions, pullback opportunities, or trend exhaustion.

The indicator optionally plots threshold zones as bands on the chart: yellow lines mark a standard deviation based on a user-defined % distance, while red lines flag more extreme moves. When price crosses these thresholds, it may suggest potential reversals or continuation depending on context.

A compact on-chart table shows the current EMA, % deviation, and dollar difference from price. Text color changes based on how far price has moved—green (normal), yellow (near threshold), or red (beyond extreme).

Customizable settings include:

• EMA Length (default 20)

• Threshold % and Extreme Threshold %

• Table Position (top/bottom left/right)

• Table Font Size (Tiny to Huge)

Threshold lines are hidden by default but can be toggled on via the Style tab, where you can also adjust their color and thickness.

Built-in alert conditions are included for when price crosses above or below either threshold level.

📉 % Drop from 52WH & ATH (Color Coded)This indicator displays the percentage drop of the current price from:

🔹 52-week high (approx. 1 year)

🔹 All-time high (ATH)

Each value is color-coded to reflect market positioning and risk level:

✅ Green: Drop less than 25% (low drawdown, relatively strong)

⚠️ Yellow: Drop between 25%–35% (moderate drawdown)

🔴 Red: Drop more than 35% (deep drawdown, potentially oversold)

The values appear in a compact info box at the top-right of the chart and work on any timeframe and asset, including stocks, crypto, indices, etc.

This tool is ideal for:

📉 Spotting deep corrections

🟢 Identifying strong relative performers

📊 Managing entry/exit based on risk zones

RSI Mansfield +RSI Mansfield+ – Adaptive Relative Strength Indicator with Divergences

Overview

RSI Mansfield+ is an advanced relative strength indicator that compares your instrument’s performance against a configurable benchmark index or asset (e.g., Bitcoin Dominance, S&P 500). It combines Mansfield normalization, adaptive smoothing techniques, and automatic detection of bullish and bearish divergences (regular and hidden), delivering a comprehensive tool for assessing relative strength across any market and timeframe.

Originality and Motivation

Unlike traditional relative strength scripts, this indicator introduces several distinctive improvements:

Mansfield Normalization: Scales the ratio between the asset and the benchmark relative to its moving average, transforming it into a normalized oscillator that fluctuates around zero, making it easier to spot outperformance or underperformance.

Adaptive Smoothing: Automatically selects whether to use EMA or SMA based on the market type (crypto or stocks) and timeframe (intraday, daily, weekly, monthly), avoiding manual configuration and providing more robust results under varying volatility conditions.

Divergence Detection: Identifies four types of divergences in the Mansfield oscillator to help anticipate potential reversal points or trend confirmations.

Multi-Market Support: Offers benchmark selection among major crypto and global stock indices from a single input.

These enhancements make RSI Mansfield+ more practical and powerful than conventional relative strength scripts with static benchmarks or without divergence capabilities.

Core Concepts

Relative Strength (RS): Compares price evolution between your asset and the selected benchmark.

Mansfield Normalization: Measures how much the RS deviates from its historical moving average, expressed as a scaled oscillator.

Divergences: Detects regular and hidden bullish or bearish divergences within the Mansfield oscillator.

Timeframe Adaptation: Dynamically adjusts moving average lengths based on timeframe and market type.

How It Works

Benchmark Selection

Choose among over 10 indices or market domains (BTC Dominance, ETH Dominance, S&P 500, European indices, etc.).

Ratio Calculation

Computes the price-to-benchmark ratio and smooths it with the adaptive moving average.

Normalization and Scaling

Transforms deviations into a Mansfield oscillator centered around zero.

Dynamic Coloring

Green indicates relative outperformance, red signals underperformance.

Divergence Detection

Automatically identifies bullish and bearish (regular and hidden) divergences by comparing oscillator pivots against price pivots.

Baseline Reference

A clear zero line helps interpret relative strength trends.

Usage Guidelines

Benchmark Comparison

Ideal for traders analyzing whether an asset is outperforming or lagging its sector or market.

Divergence Analysis

Helps detect potential reversal or continuation signals in relative strength.

Multi-Timeframe Compatibility

Can be applied to intraday, daily, weekly, or monthly charts.

Interpretation

Oscillator >0 and green: outperforming the benchmark.

Oscillator <0 and red: underperforming.

Bullish divergences: potential relative strength reversal to the upside.

Bearish divergences: possible loss of momentum or reversal to the downside.

Credits

The concept of Mansfield Relative Strength is based on Stan Weinstein’s original work on relative performance analysis. This script was built entirely from scratch in TradingView Pine Script v6, incorporating original logic for adaptive smoothing, normalized scaling, and divergence detection, without reusing any external open-source code.

BTC/Fiat Divergence & Spread Monitor📄 BTC/Fiat Divergence & Spread Monitor

This indicator visualizes Bitcoin’s relative performance across multiple fiat currencies and highlights periods of unusual divergence. It helps traders assess which fiat pairs BTC has outperformed or underperformed over a configurable lookback period and monitor the dynamic spread between the strongest and weakest pairs.

Features:

Relative Performance Matrix:

Ranks BTC returns in 6 fiat pairs, displaying a color-coded table of percentage changes and ranks.

Divergence Spread Oscillator:

Calculates the spread between the top and bottom performing pairs and normalizes this using a Z-Score. The oscillator helps identify when fiat pricing divergence is unusually high or compressed.

Dynamic Smoothing:

Optional Hull Moving Average smoothing to reduce noise in the spread signal.

Customizable Inputs:

Lookback period for percent change.

Z-Score normalization window.

Smoothing length.

Symbol selection for each fiat pair.

Visual Mode Toggle:

Switch between relative performance lines and spread oscillator view.

Potential Use Cases:

Fiat Rotation:

Identify which fiat is relatively weak or strong to optimize your exit currency when taking BTC profits.

Volatility Detection:

Use the spread Z-Score to detect periods of high divergence across fiat pairs, signaling macro FX volatility or dislocations.

Regime Analysis:

Track when fiat spreads are converging or expanding, potentially signaling market regime shifts.

Risk Management:

When divergence is extreme (Z-Score > +1), consider reducing position sizing or waiting for reversion.

Disclaimer:

This indicator is provided for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial professional before making trading decisions. Use at your own risk.

Tip:

Experiment with different lookback periods and smoothing settings to adapt the indicator to your timeframe and trading style.

EMA50 Z-Score IndicatorEMA50 Z-Score Indicator

The EMA50 Z-Score Indicator is a quantitative tool that standardizes the behavior of the 50-period Exponential Moving Average (EMA) using statistical normalization. It measures how far the current EMA50 deviates from its recent historical average in terms of standard deviations, offering a probabilistic lens into trend extension and potential reversion zones.

Purpose

Traditional moving averages provide directional trend data but lack statistical context. This indicator addresses that by applying a Z-Score transformation to the EMA50, which allows traders to assess whether the trend is overextended—either to the upside or downside—relative to its own recent history.

Methodology

The indicator calculates the Z-Score using the following formula:

Z = (EMA50 - SMA of EMA50) / Standard Deviation of EMA50

The Z-Score is computed over a user-defined lookback period (default: 100 periods), allowing it to adapt to various market conditions while preserving statistical validity.

Interpretation

Overbought Conditions: When the Z-Score exceeds a predefined positive threshold (e.g., +1.25 or +2.0), the EMA50 is statistically extended to the upside. This may indicate elevated trend momentum or exhaustion, depending on context.

Oversold Conditions: When the Z-Score falls below a predefined negative threshold (e.g., −1.25 or −2.0), the EMA50 is compressed relative to its norm, potentially signaling undervaluation or capitulation.

Neutral Conditions: A Z-Score near zero indicates that the EMA50 is near its historical average, suggesting the trend is behaving within expected bounds.