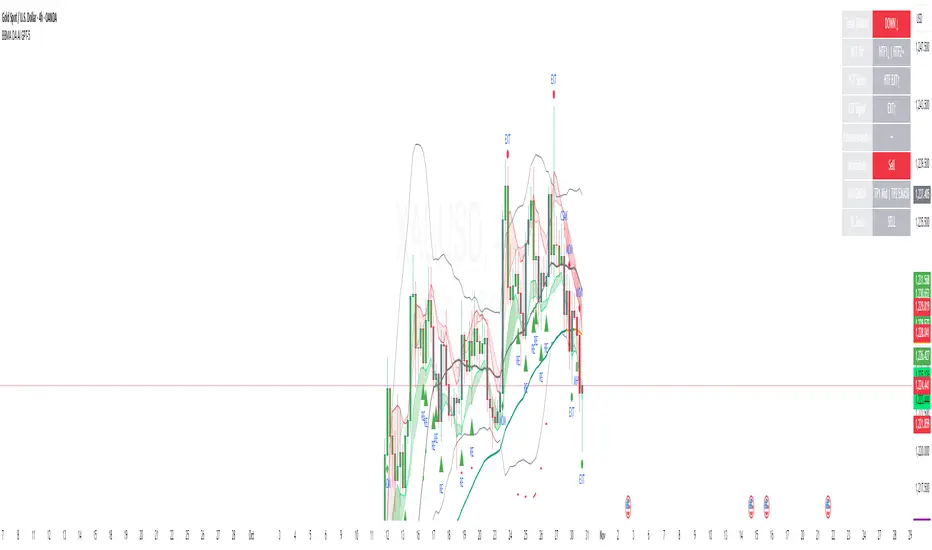

BBMA OA - AI GPT-5This indicator is an AI-assisted implementation of the BBMA OA (Bollinger Bands + Moving Average) trading strategy, originally introduced by Malaysian trader Oma Ally. The code was generated and optimized using the GPT-5 AI model to ensure clean Pine Script v6 structure and compatibility.

The system combines Bollinger Bands (20, 2) with EMA50, EMA200, and MA5/10 High-Low to identify the four main BBMA OA patterns:

Extreme

Market Hilang Volume (MHV)

Candle Arah Kukuh (CSAK)

Re-entry (RRE, REE, REM)

Features:

Multi Time Frame confirmation for higher accuracy

Automatic signal detection with visual markers

Trend ribbon and candle coloring

Optimized Pine Script v6, free from errors/warnings

⚠ This is an adaptation of Oma Ally’s concept for educational purposes, not an official version. Past performance does not guarantee future results.

Indicador Pine Script®