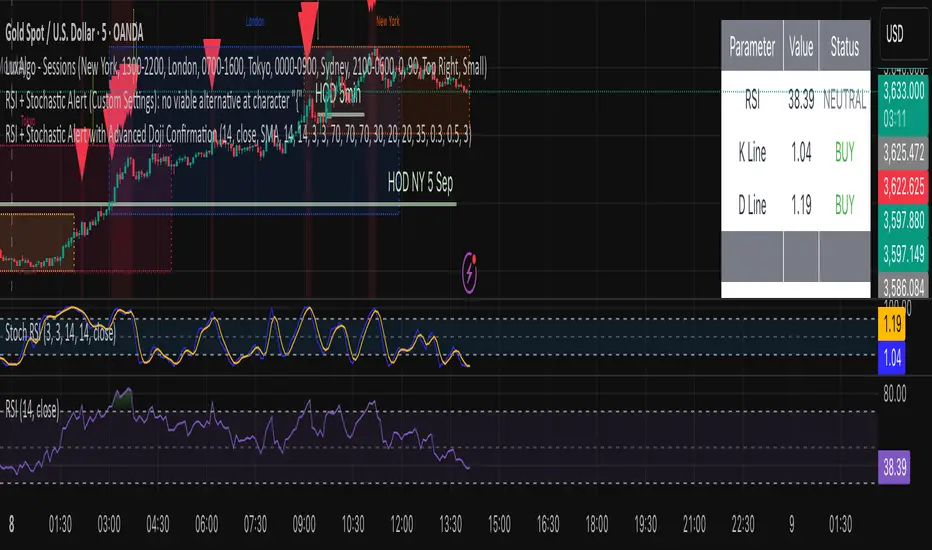

GC Checklist Signals (All Timeframes, v6)GC (COMEX Gold) checklist strategy with a 3:1 reward-to-risk to your training bot. It enforces your rules:

Heiken Ashi chart logic for color, wicks, and doji detection

100-EMA filter (only buys above / sells below)

Market structure: higher-low above EMA for buys; lower-high below EMA for sells (simple pivot check)

Clean pullback: at least 2 opposite-color candles; clean = no top wicks (buys) / no bottom wicks (sells)

Entry: on high-volume doji (body ≤ ~12% of range and volume ≥ last 1–3 candles), as soon as it closes

Stops: sell = above doji high; buy = below doji low

Indicador Pine Script®